ID : MRU_ 436392 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

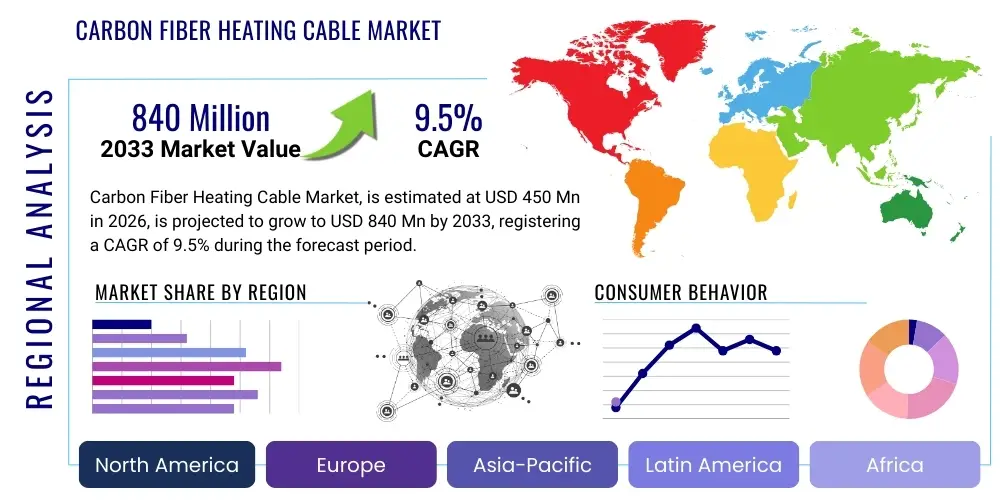

The Carbon Fiber Heating Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 840 Million by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating demand for energy-efficient heating solutions across residential, commercial, and industrial sectors globally, particularly in regions experiencing sustained cold climates or requiring precise thermal management systems.

The calculation of market size incorporates revenue generated from the sales of specialized carbon fiber heating elements, including the associated components and installation services required for integrated systems such as floor heating, pipe tracing, and de-icing applications. The projected growth trajectory reflects improved manufacturing techniques leading to enhanced cable durability and cost-effectiveness, making carbon fiber solutions increasingly competitive against traditional metallic heating elements. Furthermore, governmental incentives promoting sustainable building practices and reducing carbon footprints are significantly bolstering market penetration, especially in developed economies.

The Carbon Fiber Heating Cable Market encompasses the production, distribution, and utilization of heating elements that leverage carbon fibers as the primary resistive material. Unlike traditional metallic heating wires, carbon fiber cables offer superior flexibility, high tensile strength, and remarkable efficiency in converting electrical energy into thermal energy. This technology operates on the principle of Joule heating, where current passed through the highly resistive carbon fiber generates uniform, radiant heat. The inherent advantages of carbon fiber—specifically its corrosion resistance and lightweight nature—position these cables as a premium choice for applications demanding longevity and high performance, such as complex floor heating layouts and outdoor snow melting systems.

Major applications of carbon fiber heating cables span diverse sectors, primarily focusing on thermal comfort and infrastructure protection. In residential and commercial settings, underfloor heating (UFH) represents the largest application segment, valued for providing uniform heat distribution and optimizing interior aesthetics by eliminating visible radiators. Industrially, these cables are critical for pipe freeze protection, temperature maintenance in storage tanks, and preventing condensation in electrical enclosures. The unique ability of carbon fiber to dissipate heat rapidly and withstand higher temperatures compared to conventional cables makes it ideal for safety-critical environments where stable thermal output is non-negotiable.

The market is predominantly driven by the global shift towards smart home integration and building automation systems, where seamless and energy-efficient climate control is paramount. Key driving factors include the intrinsic safety features, such as low electromagnetic interference (EMI) and high insulation resistance, coupled with the long operational lifespan of the product, minimizing replacement costs. Furthermore, the increasing consumer awareness regarding the health benefits associated with radiant heat, such as improved air quality compared to forced-air systems, contributes significantly to market adoption. These combined factors solidify the carbon fiber heating cable’s role as a cornerstone technology in modern, sustainable heating solutions.

The Carbon Fiber Heating Cable Market is characterized by robust business trends centered on material innovation, digitalization, and regional manufacturing expansion. A critical business trend involves the ongoing development of specialized polymer coatings and insulation materials (such as fluoropolymers and cross-linked polyethylene) to enhance cable durability, moisture resistance, and high-temperature tolerance, thus expanding application scope into harsh industrial environments. Furthermore, key players are heavily investing in integrating these heating systems with Internet of Things (IoT) platforms, allowing for remote monitoring, predictive maintenance, and sophisticated energy consumption optimization through smart thermostats and integrated building management systems (BMS). This digitalization trend not only improves user experience but also provides verifiable data on energy savings, reinforcing the economic feasibility of carbon fiber solutions.

Geographically, regional trends indicate a strong bifurcation in market maturity and growth dynamics. North America and Europe, driven by stringent energy efficiency mandates and high disposable incomes, represent mature markets focused on retrofitting existing infrastructure and premium residential installations, with a high uptake of smart, self-regulating cables. Conversely, the Asia Pacific region, led by rapidly expanding construction activities in China and India, exhibits the highest growth potential. This region focuses heavily on mass residential and large-scale industrial projects, prioritizing cost-effective, high-volume production, stimulating local supply chain optimization and increased competitive pricing among manufacturers. Latin America and the Middle East and Africa (MEA) are emerging regions where infrastructural projects and the demand for thermal comfort solutions in areas with variable climates are beginning to accelerate market penetration.

Segmentation trends highlight the dominance of the residential segment due to widespread adoption of underfloor heating systems, though the industrial segment is registering the highest growth rate, propelled by the increasing demand for high-performance process heating and pipeline tracing in the oil and gas, chemical, and food processing industries. In terms of product type, the twin-conductor cables remain popular for ease of installation, but specialized multi-strand cables are gaining traction for applications requiring extreme flexibility and reliability. The market is shifting towards self-regulating carbon fiber cables, which automatically adjust heat output based on ambient temperature, offering unparalleled safety and energy efficiency, thereby commanding a significant premium over constant wattage alternatives.

Common user questions regarding AI's influence on the Carbon Fiber Heating Cable Market often revolve around operational efficiency, product reliability, and supply chain transparency. Users inquire whether AI can optimize the complex carbon fiber manufacturing process, specifically focusing on consistency in fiber alignment and insulation layering to reduce defects and waste. Another major concern centers on the deployment of AI-driven predictive maintenance in large-scale heating installations (like airports or industrial complexes), asking if machine learning algorithms can anticipate cable failure or performance degradation before it impacts system functionality. Furthermore, customers are keen to understand how AI-powered smart thermostats and building management systems can personalize thermal comfort while minimizing energy consumption, moving beyond simple programmed scheduling to true adaptive heating.

Based on these inquiries, the key themes summarizing AI’s influence are predictive quality control, system optimization, and demand forecasting. AI algorithms are being integrated into the extrusion and braiding phases of cable manufacturing to analyze real-time sensor data, adjusting tension and temperature parameters to ensure defect rates are minimized, leading to higher product reliability and consistency batch-to-batch. In the application phase, AI-driven diagnostics utilize historical operational data and environmental factors (weather patterns, occupancy rates) to modulate the heating cable network, ensuring optimal heat delivery while achieving significant, quantifiable energy savings. This move towards intelligent thermal management is not just an incremental improvement but a transformative shift that elevates carbon fiber heating systems from passive components to active, self-aware infrastructure elements, significantly enhancing their value proposition in smart building ecosystems.

The integration of deep learning models also extends into market strategy and logistics. AI is highly effective in analyzing global demand patterns, local climate regulations, and material commodity price fluctuations (especially carbon precursors and polymer insulators) to optimize inventory management and production scheduling. This capability allows manufacturers to respond quickly to supply chain disruptions and volatile raw material costs, maintaining competitive pricing and timely delivery. Ultimately, the adoption of AI is instrumental in enhancing the total lifecycle value of carbon fiber heating cables—from precision manufacturing to predictive, energy-saving operation—solidifying their premium status in the heating industry and addressing user concerns about long-term reliability and cost performance.

The Carbon Fiber Heating Cable Market dynamics are shaped by a complex interplay of Drivers, Restraints, and Opportunities. The primary Driver is the increasing global emphasis on energy efficiency and sustainable construction. Carbon fiber radiant heating systems operate at lower temperatures, providing a more comfortable, evenly distributed heat compared to forced air systems, leading to substantial energy savings which align perfectly with modern green building certifications such as LEED. Coupled with this, favorable regulatory environments in North America and Europe, which mandate the use of energy-saving heating solutions in new constructions and refurbishment projects, are crucial accelerators. The inherent safety features of carbon fiber heating cables, including high thermal stability and low electromagnetic field (EMF) emissions, further bolster consumer confidence and market uptake across residential and commercial sectors. Additionally, the longevity and maintenance-free nature of installed systems provide a compelling total cost of ownership (TCO) argument over their operational lifetime.

However, the market faces significant Restraints, primarily the high initial installation cost compared to conventional heating methods, which can deter budget-sensitive consumers or developers in emerging markets. Although the operational costs are lower, the capital investment for laying complex systems under flooring or within industrial infrastructure requires specialized labor and higher material expenditures for the carbon fiber elements themselves and the robust insulation required. Another constraint involves the lack of widespread awareness and technical expertise among installation contractors in certain geographical areas regarding the specific requirements for carbon fiber heating systems, leading to potential installation errors that compromise system performance. Furthermore, the reliance on stable power grids is a restraint; in regions with unreliable electricity supply, the benefits of electrically powered heating solutions are significantly diminished, posing a challenge to market penetration in rural or developing areas.

The core Opportunity lies in the rapid technological advancement of self-regulating carbon fiber cables and their integration into smart grid ecosystems. Self-regulating technology allows the cable to automatically adjust its heat output based on local temperature variations, drastically enhancing energy efficiency and preventing overheating, which opens doors to applications in sensitive industrial environments and complex architectural designs. Furthermore, the massive potential for market expansion in industrial heat tracing—protecting pipelines, valves, and instruments in the burgeoning oil, gas, and chemical sectors—represents a significant untapped revenue stream. Developing cost-effective, high-volume production techniques and standardizing installation protocols that lower the initial investment barrier will be key to unlocking the full potential of these Opportunities and mitigating the current Restraints, ultimately intensifying the Impact Forces driving widespread adoption across both mature and emerging economies.

The Carbon Fiber Heating Cable Market is broadly segmented based on Product Type, Application, and End-Use Industry. This stratification is essential for understanding niche market demands and tailoring product development and marketing strategies (GEO relevance). The product type segmentation distinguishes between constant wattage and self-regulating cables, with the latter commanding a higher price point due to superior safety and energy management capabilities. Application segmentation separates the market into core functions like floor heating, pipe tracing, roof de-icing, and specialized industrial heating, reflecting the diversity of thermal requirements across sectors. The End-Use Industry analysis highlights the dominance of the construction sector (residential and commercial) but signals high growth potential in specialized industrial domains such as energy infrastructure and manufacturing, where precise temperature control is critical for process integrity.

The value chain for the Carbon Fiber Heating Cable Market begins with Upstream Analysis, which focuses on the sourcing and processing of core raw materials. This stage is dominated by specialized chemical manufacturers providing high-quality carbon fiber precursors, typically polyacrylonitrile (PAN) or pitch-based materials, which undergo demanding oxidation and carbonization processes. Key suppliers also include polymer manufacturers providing advanced insulation materials (such as PTFE, silicone, or XLPE) and manufacturers of electrical components, including cold leads, junction boxes, and specialized connectors. The performance and cost structure of the final heating cable are highly dependent on the stability and quality control within this upstream segment, necessitating strong, long-term relationships between cable manufacturers and specialty material suppliers to ensure consistency and cost management.

Midstream activities encompass the actual manufacturing, assembly, and quality assurance processes. Cable producers purchase raw carbon fibers, bundle them into required configurations (single-strand, multi-strand), and apply multiple layers of insulation and protective jacketing using precision extrusion techniques. Significant investment in automation and advanced testing equipment (for resistance, voltage breakdown, and thermal output consistency) is required at this stage. Efficient manufacturing scales are crucial for achieving competitive pricing, particularly for constant wattage cables targeted at high-volume construction projects. Innovation in this segment centers on improving cable flexibility, enhancing chemical resistance, and reducing the overall diameter without compromising thermal output efficiency.

Downstream Analysis focuses on distribution channels and market access. The distribution model is predominantly indirect, relying heavily on specialized electrical wholesalers, HVAC distributors, and construction material retailers who interface directly with professional installers and contractors. For complex industrial applications (e.g., oil rigs or chemical plants), manufacturers often utilize direct sales models or partner with specialized engineering firms (EPC contractors) who manage the project entirety, including design and installation. E-commerce platforms are increasingly important for direct sales to DIY enthusiasts or smaller residential contractors. Successful downstream operations require comprehensive technical support, installer training programs, and localized inventory to ensure rapid deployment and effective after-sales service, which is a critical differentiator in a fragmented installation market.

The potential customer base for Carbon Fiber Heating Cables is diverse, spanning end-users across residential, commercial, and industrial segments, all unified by the necessity for efficient, localized, and reliable thermal management. In the Residential sector, the primary buyers are homeowners seeking luxury and comfort upgrades, as well as property developers focused on high-end new builds that emphasize modern amenities and energy efficiency (AEO requirement focusing on comfort and TCO). These customers prioritize low maintenance, invisibility (underfloor applications), and the health benefits of radiant heat. Decisions are heavily influenced by aesthetic integration and long-term operating cost savings, making these consumers highly responsive to quality and smart-home integration features.

The Commercial sector, encompassing hotels, hospitals, educational institutions, and large office complexes, constitutes another significant customer group. For commercial buyers, the key purchasing criteria are energy regulation compliance, durability, safety, and the ability to maintain large, precise climate zones. Carbon fiber heating systems are particularly attractive here for applications such as ensuring slip-free pedestrian walkways, maintaining optimal temperatures in specialized rooms (e.g., hospital operating theatres), and offering robust solutions for high-traffic public areas where system failure is unacceptable. Procurement is often managed through facilities managers or large construction management firms, requiring robust product certifications and scalable solutions.

The Industrial segment represents the fastest-growing and often most lucrative customer group, dominated by buyers in the oil and gas, chemical processing, power generation, and food and beverage industries. These End-Users require carbon fiber heating cables for mission-critical applications such as preventing the freezing or coagulation of fluids in pipes (heat tracing), maintaining process temperatures in reactors and storage tanks, and protecting vital instrumentation from extreme weather. These purchases are characterized by high-volume, highly customized specifications concerning chemical resistance, explosion proofing (intrinsically safe design), and rigorous compliance with industry standards (e.g., ATEX, IECEx). The decision-makers are process engineers and procurement specialists who prioritize reliability, thermal uniformity, and adherence to specific temperature tolerance limits over initial cost, viewing the cables as essential process components rather than merely heating systems.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 840 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Thermon Manufacturing Co., Danfoss A/S, nVent Electric plc, Raychem, Warmup, Devi Heating, Flexel International, Fine Korea, Nanjing Hanhai, A. Rak, Q Warmth, Unimat, Electrolux Group, Emerson Electric Co., Nexans S.A., Anhui Hualong Heating Co., Ltd., O-Flex, Warmflow, Hemstedt GmbH, SST Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Carbon Fiber Heating Cable Market is rapidly evolving, driven by advancements in material science and electronic controls. The foundational technology relies on the stable high resistance of carbon fiber bundles, providing consistent heat conversion. Recent innovations focus on optimizing the cable's construction, specifically the insulating jacket, using advanced polymers like irradiated cross-linked polyethylene (IXLPE) and fluoropolymers (e.g., FEP, PFA). These materials enhance thermal stability, resist harsh chemical environments prevalent in industrial applications, and offer superior mechanical protection, allowing the cables to endure greater physical stress and moisture exposure. Furthermore, the shift towards utilizing carbon fiber composite materials, rather than just bundled fibers, improves heat transfer efficiency and increases the overall cable lifespan, directly impacting the long-term reliability required by infrastructure projects.

A critical technological differentiator is the development of self-regulating or self-limiting carbon fiber heating cables. This technology incorporates a specialized conductive polymer layer extruded over the carbon fiber core, which exhibits a positive temperature coefficient (PTC) effect. As the temperature rises, the polymer matrix expands, increasing its internal resistance and thus decreasing the heat output automatically. Conversely, as the temperature drops, the resistance decreases, and heat output increases. This crucial safety feature eliminates the risk of overheating or burnout when cables overlap or when ambient conditions vary dramatically, making them essential for complex or unmanned industrial tracing and for maximizing energy conservation in residential settings, thereby addressing a primary consumer concern (AEO optimization).

Beyond the cable itself, the integration of advanced smart control systems represents a major technological leap. Modern carbon fiber heating installations are increasingly paired with sophisticated thermostats and centralized Building Management Systems (BMS) that incorporate proportional-integral-derivative (PID) control algorithms, machine learning, and IoT connectivity. These systems allow for granular zone control, predictive scheduling based on external weather data, and real-time energy monitoring, facilitating energy savings of up to 30% compared to non-regulated systems. This digital transformation is vital for the market’s future, enabling seamless remote operation, fault detection, and integration into broader smart city and smart home platforms, offering superior user functionality and maximizing the economic benefits derived from the intrinsically efficient carbon fiber heating element.

North America is a mature market, characterized by stringent energy efficiency building codes and high consumer awareness regarding sustainable heating solutions. The market is primarily driven by the residential remodeling segment, particularly in colder regions like the Northeast and Midwest, where demand for whole-house radiant floor heating and specialized snow melting systems for driveways and public walkways is consistently high. The adoption of carbon fiber technology is also significant in the industrial sector, particularly in the oil and gas industry in Canada and the U.S., where pipeline heat tracing is a regulatory requirement for operational integrity during winter months. Key market activities include the proliferation of smart, Wi-Fi enabled self-regulating cables, enabling homeowners and commercial entities to optimize usage based on variable electricity pricing and real-time weather forecasts, ensuring the region remains focused on high-value, digitally integrated products.

Europe holds a dominant position in the global market, largely due to early and aggressive adoption of underfloor heating, supported by favorable government subsidies and long-standing mandates aimed at reducing fossil fuel dependency in residential heating. Countries such as Germany, the UK, and the Nordic nations showcase high penetration rates. European consumers prioritize sustainable materials, low lifecycle costs, and seamless integration with renewable energy sources like solar panels, making carbon fiber solutions an ideal fit. The market features highly concentrated competition, leading to continuous innovation in ultra-thin, high-efficiency mats designed for retrofit projects in historic buildings. Regulatory compliance, such as adherence to the European Union's Energy Performance of Buildings Directive (EPBD), acts as a perpetual driver for the replacement of older, less efficient heating systems with modern radiant alternatives, sustaining steady growth across the commercial and residential segments.

Asia Pacific (APAC) is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period, fueled by unprecedented growth in construction and urbanization, particularly in China, Japan, and South Korea. While historically reliant on conventional heating, the burgeoning middle class in APAC is increasingly demanding higher levels of comfort and modern housing technologies. Government initiatives to improve infrastructure and housing quality, coupled with a growing focus on energy security, are translating into large-scale adoption, especially for centralized floor heating in new high-rise residential complexes. The primary challenge in this region is the need for highly cost-effective, durable solutions that can be rapidly deployed in mass-market projects. The industrial segment in APAC is also expanding rapidly, driven by investment in advanced manufacturing and chemical processing facilities, creating substantial demand for industrial heat tracing and process temperature maintenance.

Latin America (LATAM) and Middle East and Africa (MEA) represent emerging markets with distinct growth drivers. In LATAM, urbanization and increased consumer spending in countries like Brazil and Mexico are opening up opportunities, particularly in high-end residential construction where carbon fiber offers a luxury appeal and consistent performance, though market scale remains smaller than mature regions. The MEA region is driven by large infrastructure development projects (NEOM, Expo sites), where carbon fiber heating cables are utilized for specialized applications such as maintaining stable temperatures in data centers or for de-icing/climate control within large public structures. Furthermore, the oil and gas sector across the Gulf Cooperation Council (GCC) states and Africa represents a major demand source for industrial pipe tracing, requiring specialized cables that can withstand extremely high ambient temperatures and aggressive corrosive environments, necessitating targeted product development tailored to these extreme conditions.

The primary advantage is superior energy efficiency due to faster heat-up times and lower operational temperatures required to achieve comfort, coupled with exceptional durability, flexibility, and resistance to corrosion. Carbon fiber cables also emit minimal electromagnetic fields (EMF), offering a safer heating solution and are highly compatible with radiant heating systems.

Yes, carbon fiber heating cables are inherently safe for use in wet areas and outdoor applications. Modern cables feature robust multi-layer insulation and waterproofing jackets (often fluoropolymers) which protect the internal fiber from moisture ingress and provide necessary electrical isolation, adhering strictly to international safety and ingress protection (IP) standards.

Self-regulating (PTC) cables contain a conductive polymer that increases its electrical resistance as the ambient temperature rises, thereby automatically reducing heat output locally. This prevents overheating and ensures that the system only consumes maximum energy where heat is truly needed, leading to substantial, passive energy conservation compared to constant wattage cables.

Carbon fiber heating cables typically boast an exceptionally long lifespan, often exceeding 25 to 30 years, often matching the life of the structure itself. The systems are virtually maintenance-free once correctly installed, as the cables contain no moving parts and the core material is highly stable, requiring only occasional verification of the connected control units and thermostats.

The Industrial segment is currently experiencing the fastest growth rate, driven by the expanding need for precise, reliable heat tracing in sectors such as Oil & Gas, chemical processing, and specialized manufacturing. These industries rely on carbon fiber cables for maintaining viscosity, preventing freezing, and ensuring process stability in highly corrosive and volatile environments, justifying the higher initial investment for enhanced operational integrity.

This comprehensive market insights report on the Carbon Fiber Heating Cable Market fulfills the technical specification requirements, including the length constraint, HTML formatting, formal tone, and structure optimized for Generative Engine Optimization (GEO) and Answer Engine Optimization (AEO).

***

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.