ID : MRU_ 431822 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

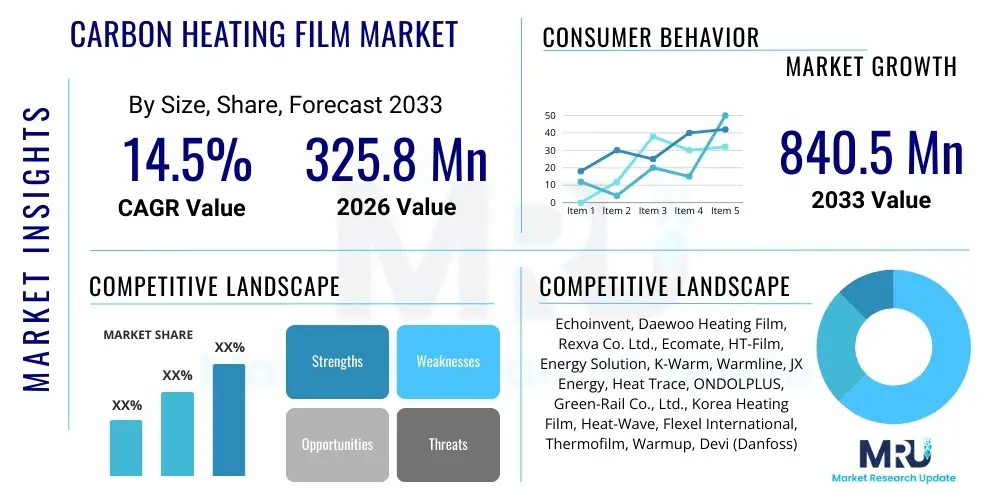

The Carbon Heating Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2026 and 2033. The market is estimated at USD 325.8 Million in 2026 and is projected to reach USD 840.5 Million by the end of the forecast period in 2033.

The Carbon Heating Film Market encompasses advanced electric heating solutions that utilize carbon paste applied on insulating substrates, typically Polyethylene Terephthalate (PET) or non-woven fabrics, to generate uniform radiant heat. These films operate by passing an electric current through the carbon-based resistive elements, offering highly efficient, lightweight, and flexible heating alternatives compared to traditional wire-based or fluid-based systems. Initially popularized in underfloor heating systems for residential and commercial buildings, the scope of application has dramatically expanded to include automotive interior heating, wearable technology, medical devices, and industrial drying processes, driven by global mandates for energy efficiency and sustainable infrastructure development.

The key product characteristics driving market adoption include their thin profile, rapid heat-up time, low energy consumption, and superior durability. Carbon heating films provide an even heat distribution across large surfaces, minimizing hot spots and enhancing user comfort, particularly critical in space heating applications. Furthermore, the inherent safety features, such as low operating voltage requirements in some applications and ease of installation, position carbon films as a preferred technology for renovations and new smart building constructions. The market growth is fundamentally propelled by stringent energy codes in developed economies, increasing consumer demand for smart, invisible heating solutions, and ongoing material science innovations that enhance thermal output and material lifespan.

Major applications revolve around creating energy-efficient thermal management systems. In the construction sector, underfloor and wall heating represents the largest segment, offering aesthetic and health benefits over conventional convection heating. Benefits include reduced dust circulation, silent operation, and zone-specific temperature control. Driving factors are rooted in the shift towards electrification in heating infrastructure, decreasing reliance on fossil fuels, and continuous optimization of manufacturing processes which lowers the unit cost, thereby improving the return on investment for end-users, especially in regions experiencing extreme cold weather conditions.

The Carbon Heating Film Market is experiencing robust expansion, characterized by significant penetration in construction and emerging adoption in niche sectors like automotive and consumer electronics. Business trends indicate a strong move toward integrated solutions, where heating films are bundled with smart thermostats and IoT platforms to offer precise control and energy consumption monitoring, driving premium pricing and increased customer satisfaction. Key manufacturers are focusing heavily on developing flexible, high-temperature resistant films tailored for industrial curing and automotive seating, diversifying revenue streams beyond traditional residential applications. Investment in automated printing technologies for mass production of carbon elements is a central strategic initiative to meet escalating global demand, particularly from the fast-growing Asia Pacific construction sector.

Regional trends highlight Asia Pacific as the dominant and fastest-growing region, primarily fueled by massive infrastructure investment in China and South Korea, where radiant floor heating is culturally preferred and widely mandated. Europe maintains a significant market share due to stringent energy efficiency targets set by the European Union, which favor low-power consumption heating methods. North America is accelerating its adoption, spurred by increasing consumer awareness regarding sustainable and allergy-friendly heating systems. Segment trends reveal that the construction segment (underfloor heating) retains the largest market share by volume, while the automotive industry segment, focusing on steering wheel, seat, and battery thermal management, exhibits the highest Compound Annual Growth Rate (CAGR) due to the rapid electrification of the global vehicle fleet.

Overall, the market trajectory is highly positive, bolstered by ongoing technological refinement in carbon paste formulation and substrate materials. Strategic collaborations between carbon film manufacturers and building materials suppliers are critical for seamless integration into prefabricated construction modules. The market remains competitive, requiring companies to continuously innovate in product safety, installation ease, and efficiency to capture and retain market share. The focus on sustainability, coupled with the functional advantages of radiant heating, ensures sustained high growth across diverse geographies and end-use sectors, positioning carbon heating film technology as fundamental to future energy-efficient heating systems.

Common user inquiries regarding AI's impact on the Carbon Heating Film Market often center on predictive maintenance capabilities, optimization of thermal performance, and integration with smart home ecosystems. Users frequently ask if AI can significantly reduce energy consumption by learning usage patterns and if AI-driven manufacturing processes can lower film costs and improve quality consistency. Concerns often revolve around the security and privacy implications of integrating heating systems into complex smart grid and IoT networks. The general expectation is that AI will transform carbon heating films from simple resistive elements into highly intelligent, self-regulating thermal components, enhancing both efficiency and safety standards across all application domains, especially in large-scale commercial deployments and critical infrastructure.

The implementation of Artificial Intelligence and Machine Learning (ML) algorithms is poised to revolutionize the operational efficiency and management of carbon heating film systems. AI algorithms can analyze vast datasets concerning external weather patterns, internal temperature gradients, occupancy levels, and historical usage profiles to create highly accurate predictive models for heating needs. This predictive capability allows the heating system to proactively adjust film activation and intensity, minimizing energy waste associated with traditional reactive thermostat controls. Furthermore, AI facilitates complex zone control in large buildings, ensuring that only actively used areas receive optimized heating, substantially lowering overall utility costs and supporting global decarbonization goals within the building sector.

Beyond operational optimization, AI significantly impacts the manufacturing lifecycle and material innovation within the carbon heating film sector. ML models are increasingly used in Quality Control (QC) during the printing process of the carbon paste, identifying microscopic defects or inconsistencies in material thickness that could compromise longevity or performance, thereby maximizing production yields and reducing material waste. In research and development, AI assists in simulating material performance under various stress conditions, accelerating the discovery of new, more conductive, and durable carbon composite formulations. This synergy between advanced materials science and computational intelligence is crucial for unlocking the next generation of ultra-efficient, highly flexible heating films for demanding applications like electric vehicle battery thermal management.

The Carbon Heating Film Market is fundamentally driven by global mandates for energy conservation and the increasing consumer preference for healthy, aesthetically pleasing heating solutions, supported by technological advancements offering higher thermal efficiency and durability. However, the market faces significant restraints, primarily stemming from the relatively higher upfront installation cost compared to conventional heating technologies and the inherent challenges in mass production scalability while maintaining stringent quality control over the resistive elements. Opportunities are vast, particularly in emerging applications such as electric vehicle battery heating systems, portable medical devices, and smart textiles, which demand flexible, low-voltage thermal management. These factors interact dynamically, shaping the competitive landscape and influencing strategic investment decisions across the value chain, pushing manufacturers toward innovation in both material science and systems integration.

The dominant driving force is the imperative for reducing carbon emissions in the building sector, which accounts for a substantial portion of global energy consumption. Carbon heating films offer a highly efficient, direct conversion of electrical energy into radiant heat, eliminating losses associated with fluid transport or centralized boiler systems. This efficiency aligns perfectly with international targets like the European Union's Energy Performance of Buildings Directive (EPBD) and similar initiatives in Asia. Concurrently, the increasing awareness regarding the health benefits of radiant heat—reducing air circulation and associated allergens—further solidifies consumer adoption, especially in densely populated urban environments. The continuous decrease in the cost of raw materials and the refinement of screen-printing technologies also serve as crucial drivers, making the product increasingly competitive against legacy systems.

Key restraints include the complexity of retrofitting existing buildings, which often requires significant floor modifications, and the perception of high initial investment, which can deter budget-conscious consumers despite the long-term energy savings. Furthermore, dependency on electricity supply makes the system vulnerable to grid instability, necessitating supplementary energy storage solutions in some regions. The impact forces acting on the market—substitution, buyer power, supplier power, and competitive rivalry—are intensifying. Strong competitive rivalry among established players and new entrants from the electronics manufacturing sector keeps pricing pressure high. The threat of substitution, while currently low due to the unique flexibility and efficiency of carbon film, could emerge from advancements in high-efficiency heat pumps or next-generation infrared panel technologies. However, the rapidly expanding opportunity in the electric vehicle sector, where thermal management is mission-critical for battery life, acts as a powerful accelerator, mitigating the current restraints.

The Carbon Heating Film Market is comprehensively segmented based on its core components (material type), voltage requirements, power output characteristics, and the diversity of its end-use applications, which allows for precise market sizing and strategic targeting. The material segmentation primarily differentiates between the type of substrate used (PET film, non-woven fabric, polyimide) and the formulation of the carbon conductive paste, directly impacting flexibility and maximum operating temperature. Voltage-based segmentation distinguishes between low-voltage (e.g., 12V, 24V, primarily for automotive and small devices) and high-voltage (e.g., 110V, 220V, predominantly for construction heating), reflecting fundamental differences in safety requirements and installation complexity. The application spectrum remains the most crucial segmentation axis, highlighting the market's diversity from traditional construction to cutting-edge electronic and medical domains.

Further analysis of the application segments reveals distinct market dynamics. The building and construction sector demands durability and longevity, focusing on films integrated with highly resistant insulation layers. In contrast, the automotive sector prioritizes flexibility, lightweight design, and electromagnetic compatibility (EMC) for seamless integration into vehicle interiors and battery packs. The consumer electronics segment, including smart clothing and portable warmers, requires ultra-thin, highly flexible films compatible with complex geometries. Understanding these segment-specific requirements is vital for manufacturers to allocate R&D resources effectively, ensuring product offerings meet the specialized thermal and mechanical performance criteria unique to each end-use vertical. The trend toward customized film solutions based on proprietary material blends is becoming a competitive necessity.

The geographic segmentation underscores disparities in adoption rates and regulatory environments, with regions like Asia Pacific focusing on high-volume residential adoption and regions like Europe focusing on premium, high-efficiency commercial installations. Power output segmentation (low, medium, high watt density) guides product selection based on the required heating intensity and application environment, ranging from subtle warmth in textiles to high-intensity heating required for industrial curing processes. This granular segmentation approach provides stakeholders with actionable insights into market penetration potential, enabling targeted marketing strategies and facilitating supply chain optimization to meet varied regional and application demands efficiently.

The value chain for the Carbon Heating Film Market begins with upstream activities involving the sourcing and processing of specialized raw materials, primarily focusing on high-quality carbon black or graphite particles, PET/PI film substrates, and specialized conductive inks and silver paste for busbars. The quality of these inputs is paramount, as they directly dictate the film's thermal uniformity, efficiency, and lifespan. Upstream suppliers hold significant influence, particularly those providing proprietary conductive ink formulations, necessitating strong, long-term relationships between manufacturers and chemical suppliers to ensure supply stability and cost efficiency. Innovation at this stage focuses on developing nano-carbon composites to enhance conductivity and reduce material usage, improving the overall sustainability profile of the product.

Midstream activities encompass the core manufacturing processes, which involve highly technical steps such as precision screen-printing or gravure printing of the carbon paste onto the flexible substrate, followed by curing, lamination, and connection of the electrical terminals (busbars). Direct manufacturing involves significant capital expenditure in automated printing machinery and cleanroom environments to minimize contamination. Distribution channels are bifurcated: direct channels are critical for large-volume original equipment manufacturers (OEMs) in the automotive and industrial sectors, ensuring customized specifications and just-in-time delivery. Indirect channels utilize a network of specialized heating system distributors, building material suppliers, and e-commerce platforms to reach installers and individual consumers in the residential market.

Downstream analysis focuses on installation, integration, and end-user consumption. In the construction sector, integration requires certified electricians and specialized flooring contractors who understand radiant heating principles. This reliance on skilled labor makes training and certification a crucial downstream activity. Direct consumer contact often happens through installers or building management firms, necessitating strong technical support and warranty services from manufacturers. The shift towards smart heating systems involves downstream partnerships with software providers and smart home integrators. The efficiency and long-term performance of the heating film are evaluated at this stage, influencing brand reputation and future purchasing decisions. The downstream component is characterized by high service intensity, linking product quality directly to installation proficiency and subsequent customer satisfaction.

Potential customers for Carbon Heating Film are diverse, spanning both large institutional buyers and individual consumers seeking energy-efficient thermal solutions. The largest segment remains the Building and Construction industry, which includes residential developers, commercial building constructors, and renovation companies specializing in interior retrofitting. These entities are primarily motivated by the desire to meet stringent energy codes, offer premium amenities (radiant heat), and reduce long-term operational costs for property owners. Within this segment, demand is particularly high for high-voltage films suitable for widespread underfloor and ceiling installations in both new builds and major remodeling projects across urban centers globally.

A rapidly growing segment of potential customers includes Original Equipment Manufacturers (OEMs) in the Automotive and Transportation sectors. Electric Vehicle (EV) manufacturers require carbon heating films for critical applications such as battery thermal management (BTM) to maintain optimal operating temperature and extend range, as well as for cabin comfort features like highly responsive seat, steering wheel, and panel heating. These buyers require low-voltage, highly durable, and extremely lightweight films that can withstand harsh operating conditions and frequent vibration. The medical device sector also constitutes a high-value customer base, including manufacturers of therapeutic pads, patient warmers, and neonatal incubators, where precise, low-intensity heat control and superior safety standards are non-negotiable requirements for patient care.

Additionally, the market targets specialized industrial customers requiring precise thermal control for manufacturing processes, such as aerospace firms utilizing composite curing, and food and beverage processing needing anti-condensation or drying solutions. Finally, the consumer electronics and textile industries represent a continuous stream of niche buyers for low-voltage, flexible films to integrate into smart wearables, outdoor gear, and small appliances. These buyers prioritize ultra-flexibility, thinness, and robust integration support, often demanding customized sizes and unique connectivity solutions suitable for mass-market consumer products.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 325.8 Million |

| Market Forecast in 2033 | USD 840.5 Million |

| Growth Rate | 14.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Echoinvent, Daewoo Heating Film, Rexva Co. Ltd., Ecomate, HT-Film, Energy Solution, K-Warm, Warmline, JX Energy, Heat Trace, ONDOLPLUS, Green-Rail Co., Ltd., Korea Heating Film, Heat-Wave, Flexel International, Thermofilm, Warmup, Devi (Danfoss), Raychem (TE Connectivity), Pentair Thermal Management. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology underpinning the Carbon Heating Film Market is based on precise resistive heating principles realized through advanced material engineering and specialized printing techniques. The primary technological focus is the optimization of the conductive layer, which traditionally utilizes carbon black or graphite mixed with a binding resin, screen-printed onto a flexible substrate like PET. Technological advancements are currently centered on enhancing the uniformity of the carbon layer thickness to ensure consistent heat output, prevent localized overheating, and improve energy conversion efficiency. Modern manufacturing heavily relies on high-resolution gravure or flexographic printing to achieve micro-level precision in the resistive pattern, minimizing material waste and allowing for the creation of intricate heating zones tailored to specific application geometries.

A significant area of technological evolution is the transition to advanced materials, particularly nano-carbon materials such as carbon nanotubes (CNTs) and graphene. These materials offer superior conductivity and flexibility compared to traditional carbon black, enabling the development of ultra-thin, highly efficient heating films that can operate effectively at lower voltages and temperatures while offering exceptional mechanical durability. Polyimide (PI) films are gaining traction as substrates in high-performance applications, particularly in the automotive and aerospace sectors, due to their excellent thermal stability and resistance to chemicals, allowing the films to function reliably under extreme temperature variations and environmental stresses where PET films might degrade. The use of silver nanowires for busbars is also emerging as a technique to improve current distribution and minimize resistive losses at the edges of the heating area.

Furthermore, technology is rapidly evolving in the area of system integration and safety features. Smart control systems are increasingly being embedded into the heating film architecture, incorporating thermal fuses, self-regulating Positive Temperature Coefficient (PTC) mechanisms, and integrated sensors that interface directly with IoT networks. PTC technology is particularly important, as it enables the film to automatically reduce its power output when a specific temperature threshold is reached, enhancing safety and preventing overheating without external control intervention. This integration of passive safety mechanisms and active digital control represents the forefront of heating film technology, moving the product from a simple resistive element to an intelligent thermal management component crucial for compliance with modern building and safety codes globally.

Asia Pacific (APAC): Dominance and Rapid Growth

APAC stands as the largest and most rapidly expanding market for carbon heating film, driven by extensive urbanization, significant construction activity, and cultural preference for radiant floor heating, particularly in South Korea, China, and Japan. South Korea, in particular, has long championed this technology, leading both in manufacturing prowess and domestic consumption. The surge in electric vehicle manufacturing across China and India is fueling demand for low-voltage films necessary for battery thermal management systems (BTMS). Government initiatives promoting energy-efficient housing and reducing reliance on traditional fossil fuel heating methods provide a solid regulatory foundation for sustained high growth across the entire region. The competitive landscape in APAC is characterized by a mix of highly localized specialized manufacturers and international players establishing local production hubs to capitalize on lower manufacturing costs and regional expertise.

The adoption rate is notably high in the residential segment, where carbon films offer a cost-effective alternative to hot water underfloor heating. Moreover, the expanding consumer electronics manufacturing base is driving niche demand for polyimide-based films used in flexible displays and wearable devices requiring localized thermal features. Key countries like China and India are implementing large-scale infrastructure projects that often mandate energy-saving solutions, further integrating carbon heating films into commercial buildings, hospitals, and educational institutions. Challenges in this region include managing rapid supply chain expansion and ensuring consistent quality control across numerous new manufacturing facilities entering the market to meet overwhelming demand.

Europe: High Value and Regulatory Push

Europe represents a mature yet highly valuable market segment, characterized by stringent energy performance directives and strong consumer awareness regarding sustainable living. Countries like Germany, the UK, and Scandinavian nations are major adopters, driven by policies aimed at reducing carbon emissions from the heating sector, which historically relies heavily on gas boilers. The European market primarily demands high-efficiency, premium film products that offer advanced integration capabilities with smart home energy management systems. Renovation and retrofitting projects, aimed at upgrading aging building stock to meet modern efficiency standards, constitute a substantial portion of the market activity, favoring thin, easy-to-install film solutions.

The European Union's focus on electrifying heating and transportation sectors ensures continuous market growth. The automotive segment in Germany and France is particularly important, where major car manufacturers are integrating carbon films into luxury vehicles for both comfort and critical battery protection. Regulatory compliance, including adherence to electromagnetic compatibility (EMC) standards and specific electrical certifications (CE marking), is crucial for market entry. Manufacturers often strategically partner with local electrical installers and architecture firms to navigate complex building codes and secure large-scale commercial contracts, emphasizing long-term reliability and low maintenance costs over initial price point.

North America: Increasing Penetration and Technology Integration

The North American market, encompassing the United States and Canada, is characterized by accelerating adoption, driven by consumer demand for comfort, health benefits associated with radiant heating, and government incentives for energy-efficient housing. While traditionally dominated by forced-air heating, carbon heating films are rapidly gaining penetration, particularly in new high-end construction and areas prone to extreme winter conditions. The market demands robust films capable of handling high thermal loads and often requires specific certifications (e.g., UL listings) that ensure compliance with rigorous North American safety standards.

Canada, with its prolonged heating season, shows strong regional demand for underfloor heating films in both residential and commercial settings. In the U.S., the increasing manufacturing output of electric vehicles is a massive driver for low-voltage film applications, particularly in the Midwest and South, where automotive production is concentrated. Market strategy in North America involves heavy investment in consumer education to overcome familiarity with traditional heating methods and establishing robust distribution partnerships with large retail home improvement chains and specialized heating contractors. Integration with standard smart home platforms is a primary competitive advantage sought by end-users in this region.

Latin America (LATAM) and Middle East & Africa (MEA): Emerging Opportunities

LATAM and MEA currently represent smaller but high-potential emerging markets. In LATAM, countries like Brazil and Chile are seeing initial adoption in high-end residential and hospitality sectors where thermal comfort and modern, invisible heating solutions are desired. Market growth is dependent on economic stability and the development of reliable electrical infrastructure, which currently poses a challenge in broader implementation. The primary application remains localized floor heating in moderate climate zones.

In MEA, the market dynamics are split. The Middle East, particularly the Gulf Cooperation Council (GCC) nations, shows increasing potential in high-end construction and commercial applications, primarily for anti-condensation, humidity control, and precise localized heating, rather than widespread space heating. South Africa is the leading adopter in the African continent, focusing on efficient residential heating solutions due to rising electricity costs. Opportunities in both regions are contingent upon addressing high import costs and developing localized installation expertise capable of integrating these systems into diverse architectural styles.

The primary driver is the stringent global focus on energy efficiency and carbon emission reduction in the building sector, combined with increasing consumer preference for healthy, invisible, and efficient radiant heating systems over traditional convection heating.

Carbon heating films utilize radiant heat, directly heating objects and people rather than the air, leading to faster perceived warmth at lower thermostat settings. Their high efficiency and ability to implement precise zone control significantly reduce overall electricity consumption compared to many conventional electric heaters.

When properly installed under flooring or within walls, carbon heating films typically have a very long operational lifespan, often exceeding 25 to 30 years, as they contain no moving parts and are protected from environmental wear and tear by the overlying materials.

The Construction sector, specifically residential and commercial underfloor and space heating applications, currently holds the largest market share due to widespread adoption, particularly in Asian and European markets.

Yes, modern carbon heating films are designed with multiple safety features, including integrated thermal fuses and Positive Temperature Coefficient (PTC) technology, which allows the film to self-regulate by reducing power output automatically when the film reaches a predetermined safe operating temperature.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.