ID : MRU_ 434908 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

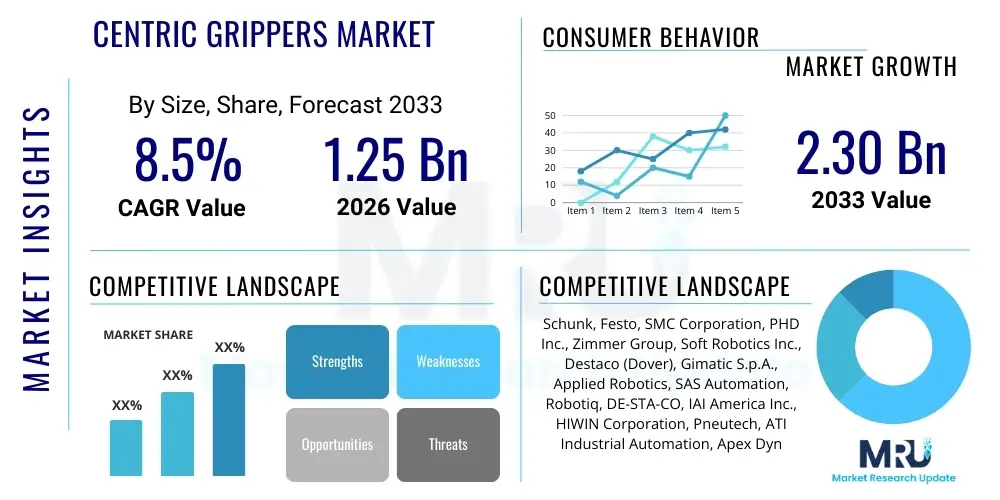

The Centric Grippers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 2.30 Billion by the end of the forecast period in 2033.

Centric grippers, often referred to as parallel or 2-jaw grippers, are fundamental components in industrial automation, designed to pick, place, and precisely manipulate workpieces by clamping them symmetrically relative to a central axis. These devices are essential for high-precision manufacturing processes requiring accurate handling of components across various sizes and shapes. Their primary function is to provide reliable, repeatable, and robust gripping force, ensuring operational efficiency and reducing human error in automated assembly lines. The intrinsic simplicity and reliability of centric gripper mechanisms make them indispensable across sectors demanding high throughput and consistent quality control, positioning them as core drivers of modern robotic systems.

The product portfolio encompasses pneumatic, electric, and hydraulic variants, each tailored to specific force, speed, and environmental requirements. Pneumatic centric grippers dominate applications requiring high speed and medium force, whereas electric grippers are increasingly favored in environments demanding high flexibility, precise control over gripping force, and energy efficiency, particularly in cleanroom settings or delicate component handling within the electronics industry. Major applications span the automotive sector for engine part manipulation, the electronics industry for PCB and semiconductor handling, and the pharmaceutical and medical device manufacturing for precise packaging and assembly tasks.

The market growth is primarily driven by the accelerated global adoption of Industry 4.0 principles, characterized by increased integration of robotics and automation across manufacturing ecosystems. Benefits derived from utilizing centric grippers include enhanced production speed, significant improvement in dimensional accuracy of assembly, reduced operational costs due to labor substitution, and improved workplace safety. Furthermore, the continuous miniaturization of components, especially in consumer electronics, necessitates advanced gripping solutions capable of high precision and adaptive control, thereby fueling innovation and demand for more sophisticated, sensor-integrated centric gripping systems.

The Centric Grippers Market is exhibiting robust growth, propelled by strong business trends centered around manufacturing reshoring, the proliferation of smart factories, and the necessity for flexible automation solutions. Key business trends include the shift towards electric grippers offering superior programmability and feedback capabilities, essential for complex tasks in high-mix, low-volume production environments. Market strategies are increasingly focusing on developing modular gripper systems compatible with various collaborative robot (cobot) platforms, thereby broadening their application scope beyond traditional heavy industrial settings. Furthermore, strategic partnerships between robot manufacturers and specialized gripper vendors are accelerating technology integration, shortening deployment times for end-users seeking turnkey automation solutions.

Regionally, the Asia Pacific (APAC) continues to lead the market, driven by massive investments in automation infrastructure in China, Japan, and South Korea, particularly within the automotive, consumer goods, and electronics manufacturing sectors. North America and Europe demonstrate mature markets characterized by high adoption rates of advanced, highly controlled electric grippers, often used to optimize labor-intensive processes and maintain global competitiveness. Trends in these developed regions focus heavily on adopting grippers compatible with vision systems and artificial intelligence (AI) for complex bin-picking and adaptive handling tasks, emphasizing precision and integration capability over sheer speed.

Segmentation trends highlight the dominance of the Pneumatic segment in terms of volume due to cost-effectiveness and robustness, especially in heavy-duty applications. However, the Electric segment is projected to record the highest CAGR, reflecting the industry's demand for precise force control and energy efficiency mandated by modern clean manufacturing standards. Application-wise, the Automotive sector remains the largest consumer, though the fastest growth is observed within the Electronics & Semiconductor segment, spurred by the need for extremely gentle and precise handling of fragile and expensive components. These trends collectively underscore a market moving towards greater intelligence, flexibility, and connectivity in automation tooling.

Common user questions regarding AI's impact on Centric Grippers revolve primarily around enhancing adaptability, predictive maintenance, and optimizing complex handling tasks. Users frequently inquire about how AI can enable grippers to handle previously unseen objects (adaptive gripping), improve yield rates by dynamically adjusting gripping force based on material feedback, and reduce downtime through real-time performance monitoring and fault prediction. Concerns often focus on the complexity and cost associated with integrating AI algorithms into standard pneumatic or electric control systems, and the data required to train these sophisticated models effectively. The consensus expectation is that AI will transform centric grippers from simple mechanical actuators into intelligent, decision-making robotic end-effectors, essential for the next generation of highly flexible and autonomous manufacturing cells.

The primary area of impact is in enabling true flexibility in manufacturing. Traditional centric grippers require reprogramming or manual adjustment when workpiece specifications change. AI, integrated through machine learning and computer vision systems, allows the gripper to identify, locate, and determine the optimal gripping parameters (force, speed, position) autonomously for varying objects within a production run, dramatically increasing operational versatility. This shift is crucial for industries transitioning towards mass customization where batch sizes are small and product variety is high.

Furthermore, AI significantly enhances the reliability and longevity of centric grippers. By continuously analyzing operational data—such as motor current, pressure differentials, and cycle times—AI algorithms can detect subtle anomalies indicative of mechanical wear or potential failure before they escalate into critical faults. This predictive maintenance capability minimizes unexpected downtime, optimizes maintenance scheduling, and extends the operational life of the gripper mechanism, delivering substantial return on investment for high-utilization robotic systems.

The Centric Grippers Market is shaped by strong drivers, mitigated by technological restraints, and presented with significant opportunities, resulting in powerful impact forces that guide its trajectory. The dominant drivers include the global push towards factory automation to combat rising labor costs and shortages, coupled with the increasing adoption of collaborative robots (cobots), which rely heavily on specialized, safe, and precise end-effectors like centric grippers. These drivers are further amplified by government initiatives supporting advanced manufacturing infrastructure across major industrial economies.

Key restraints tempering growth include the high initial investment cost associated with advanced electric and servo-driven centric grippers, particularly for Small and Medium Enterprises (SMEs) in developing regions. Furthermore, the technical complexity involved in integrating advanced, highly sensitive grippers with diverse robotic platforms and proprietary control systems poses a significant barrier to widespread adoption. The requirement for specialized expertise in programming and maintenance of these integrated robotic systems also restricts market penetration in less industrialized environments.

Opportunities for market expansion are substantial, primarily driven by the rapid growth in the electronics, semiconductor, and medical device manufacturing sectors, which demand ultra-precise and contamination-free handling. The continued development of lighter, more powerful materials (like carbon fiber) for gripper fabrication and advancements in sensor technology offer avenues for creating smarter, more robust grippers suitable for harsh environments and diverse applications. The resultant impact forces strongly favor suppliers capable of offering modular, plug-and-play solutions that minimize integration complexity and cater to the booming cobot market, accelerating the overall automation rate globally.

The Centric Grippers Market segmentation provides a detailed structure for understanding market dynamics based on Type, Application, and Technology. This categorization helps manufacturers tailor product development to specific industrial requirements and helps end-users select the most appropriate gripping technology for their automation needs. Analysis shows a clear divergence in growth rates, with advanced technological segments like electric grippers gaining significant momentum over traditional pneumatic solutions, especially in sectors prioritizing precision and data feedback.

The market is predominantly classified by the actuation mechanism, which determines the force, speed, and controllability of the gripper. Pneumatic grippers, while mature, maintain a strong market share due to their high power-to-weight ratio and cost-effectiveness. Conversely, electric grippers are rapidly increasing their market presence, capitalizing on the demand for variable force control and seamless integration with complex sensor architectures, critical for flexible manufacturing lines and quality assurance processes.

Furthermore, segmentation by application highlights where automation investment is concentrated. The Automotive sector remains foundational, driving demand for high-force, robust grippers, while the burgeoning Electronics sector fuels the need for micro-handling and extreme precision centric grippers. Understanding these application specific demands is crucial for strategic market positioning and innovation prioritization across the component manufacturing value chain.

The value chain for the Centric Grippers Market begins with upstream analysis involving the sourcing and processing of core raw materials such as high-grade aluminum, specialized steels, and advanced composite materials necessary for constructing the gripper body and jaws. Key upstream activities also include the manufacturing of precision components like servo motors, pneumatic cylinders, sensors, and microprocessors, which are sourced from specialized component suppliers. Efficiency and cost optimization at this stage heavily influence the final product’s performance characteristics, including weight, robustness, and precision. Maintaining stable material supply chains and ensuring quality control for highly complex internal mechanisms are critical challenges at the upstream level.

Midstream activities encompass the actual design, manufacturing, and assembly of the centric gripper units by specialized automation companies. This stage involves sophisticated machining, integration of actuation mechanisms (pneumatic or electric), and rigorous testing to meet industry standards for repeatability and lifespan. Manufacturers differentiate themselves through proprietary jaw designs, modularity, and the incorporation of advanced sensing and control electronics, crucial for integration into modern robotic systems. Research and Development investment in new actuation technologies and lighter materials are pivotal competitive factors within this segment.

Downstream analysis focuses on distribution channels and end-user deployment. The distribution model often utilizes a mix of direct sales channels for large, custom automation projects and indirect channels, relying on specialized industrial distributors, system integrators, and e-commerce platforms for standardized units and cobot components. System integrators play a vital role, often bundling grippers with robots, vision systems, and custom fixtures to provide turnkey solutions to end-users across the automotive, electronics, and general manufacturing sectors. The quality of after-sales support, technical training, and quick replacement part availability determine success in the downstream market.

Potential customers and primary end-users of centric grippers span a wide range of industries focused on precision manufacturing, assembly, and quality control, leveraging automation to improve speed and consistency. The core customer base resides in large-scale manufacturing enterprises, particularly those operating highly automated assembly lines, where continuous and reliable component manipulation is non-negotiable. These buyers prioritize grippers that offer high duty cycles, exceptional repeatability, and robust construction to withstand harsh industrial environments and continuous operation typical of global manufacturing hubs.

A rapidly growing segment of potential customers includes Small and Medium Enterprises (SMEs) that are increasingly adopting collaborative robots (cobots). These buyers seek cost-effective, easy-to-program, and modular centric grippers that require minimal integration effort. Their purchasing decisions are highly influenced by ease of deployment, compatibility with standard cobot interfaces, and the availability of simplified control software, enabling rapid deployment of automation solutions without deep robotics expertise.

Specialized buyers in highly regulated industries such as pharmaceuticals, medical devices, and semiconductors represent another critical customer group. These end-users require centric grippers that are not only precise but also compliant with stringent hygiene and cleanroom standards (e.g., ISO Class 4 or higher). For this segment, material certification, non-shedding components, and the ability for precise force feedback control to handle fragile or sensitive materials are key purchasing criteria, driving demand for specialized electric and pneumatic stainless steel or coated grippers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.30 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Schunk, Festo, SMC Corporation, PHD Inc., Zimmer Group, Soft Robotics Inc., Destaco (Dover), Gimatic S.p.A., Applied Robotics, SAS Automation, Robotiq, DE-STA-CO, IAI America Inc., HIWIN Corporation, Pneutech, ATI Industrial Automation, Apex Dynamics Inc., HANKSCRAFT Inc., Tünkers Group, KUKA AG (Swisslog). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Centric Grippers Market is rapidly evolving, driven by the need for greater flexibility, connectivity, and precision in robotic handling. A significant technological shift involves the integration of advanced sensor technologies directly into the gripper jaws and body. Force/torque sensors provide critical feedback, allowing the gripper to dynamically adjust its clamping force based on the workpiece material and geometry, preventing damage to fragile items. Furthermore, proximity and optical sensors embedded within the gripper enhance accuracy, enabling verification that the part has been successfully acquired and is correctly oriented before the next operation, thereby increasing overall process reliability.

Another crucial development is the prominence of lightweight material science. To meet the demands of collaborative robotics and high-speed pick-and-place applications, manufacturers are increasingly using high-strength aluminum alloys, carbon fiber, and engineered polymers. These materials reduce the overall weight of the end-effector, allowing for higher robot payloads and faster acceleration/deceleration cycles, which directly translates to improved throughput. This focus on material innovation supports the miniaturization trend while maintaining the required stiffness and robustness necessary for industrial operation.

The control systems driving modern centric grippers are also advancing significantly. The transition from simple on/off pneumatic valves to sophisticated servo-electric controls allows for highly precise positional control and variable force profiling, which are mandatory for handling diverse product mixes. Furthermore, the adoption of standardized communication protocols (like IO-Link and EtherCAT) facilitates seamless integration of these intelligent grippers into the broader Industry 4.0 infrastructure, enabling remote diagnostics, real-time data collection, and integration with cloud-based manufacturing execution systems (MES).

Pneumatic centric grippers are generally faster, more robust, and cost-effective, using compressed air for actuation, making them ideal for high-speed, high-force general automation. Electric centric grippers offer superior programmability, precise force control, energy efficiency, and data feedback, making them essential for delicate handling, variable force applications, and integration into sophisticated smart factory systems.

The Automotive sector currently holds the largest market share due to the intensive automation required for handling and assembly of engine parts, chassis components, and body panels on high-volume production lines. However, the Electronics and Semiconductor segment is projected to exhibit the highest growth rate due to increasing demand for ultra-precise micro-handling.

Industry 4.0 necessitates high connectivity and data exchange, driving demand for intelligent centric grippers equipped with sensors (IO-Link capabilities) that can communicate real-time status, force data, and position. This enables predictive maintenance, dynamic process optimization, and seamless integration into Manufacturing Execution Systems (MES).

Yes, specialized lightweight, plug-and-play electric centric grippers are increasingly designed specifically for cobots. These grippers feature integrated safety functionalities and user-friendly software interfaces, enabling easy deployment and safe human-robot interaction in collaborative manufacturing environments.

Key technical challenges include achieving reliable, high-speed micro-handling precision for extremely small electronic components, developing standardized interfaces to simplify integration across diverse robot brands, and reducing the cost and complexity of advanced servo-electric control systems to increase their accessibility for SMEs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.