ID : MRU_ 432856 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

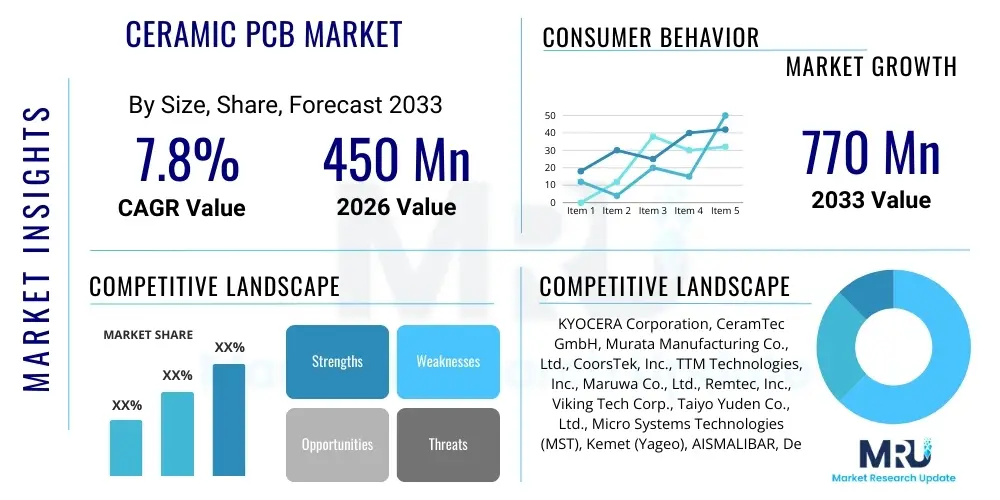

The Ceramic PCB Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 770 Million by the end of the forecast period in 2033.

The Ceramic PCB (Printed Circuit Board) market encompasses advanced electronic substrates made from ceramic materials such as Alumina (Al2O3), Aluminum Nitride (AlN), and Beryllium Oxide (BeO). These specialized substrates are designed to overcome the thermal and electrical limitations inherent in traditional FR4 or polymer-based PCBs. Ceramic PCBs are characterized by their superior thermal dissipation capabilities, low coefficient of thermal expansion (CTE) matching that of semiconductor chips, high mechanical stability, and excellent high-frequency performance, making them indispensable in demanding electronic environments. The primary product description centers around substrates manufactured using technologies like Thick Film, Thin Film, Direct Bonded Copper (DBC), and Active Brazed Copper (ABC), each optimized for different power handling and complexity requirements.

Major applications driving the current market growth include high-power electronic modules, LED lighting systems, automotive electronics (especially in electric vehicles and advanced driver-assistance systems - ADAS), and aerospace and defense communications equipment. In the realm of power electronics, ceramic PCBs are crucial for insulating high voltages while efficiently dissipating the significant heat generated by components like IGBTs and MOSFETs. Furthermore, the push towards miniaturization and higher operating frequencies in telecommunications infrastructure, particularly 5G and future 6G networks, necessitates the use of substrates that minimize signal loss and maintain integrity under extreme thermal cycling, capabilities ceramic materials inherently possess.

The core benefits fueling market expansion revolve around reliability and longevity in harsh conditions. Ceramic materials offer exceptional resistance to moisture, chemicals, and temperature fluctuations, significantly extending the lifespan of the electronic device. Driving factors include the escalating global demand for Electric Vehicles (EVs) and hybrid vehicles, which rely heavily on high-power density converters and inverters utilizing ceramic substrates. Additionally, the increasing complexity of medical imaging equipment and industrial laser systems, requiring stable performance under continuous high heat flux, ensures sustained demand for these specialized circuit boards. The inherent robustness of ceramic PCBs positions them as critical components in the technological evolution towards smaller, faster, and more powerful electronic devices across multiple high-reliability sectors.

The Ceramic PCB market is experiencing robust growth driven primarily by structural shifts in the automotive and telecommunications sectors. Business trends indicate a strong focus on capacity expansion, particularly for Aluminum Nitride (AlN) substrates, favored for their ultra-high thermal conductivity essential in high-frequency power modules and RF applications. Key industry players are aggressively investing in advanced manufacturing processes like Active Brazed Copper (ABC) technology to meet the stringent performance requirements of next-generation power semiconductor devices. Mergers and acquisitions are observable, aimed at consolidating specialized expertise in high-precision processing and thin-film metallization, thereby enhancing market competitiveness and driving economies of scale necessary to offset high raw material costs.

Regionally, Asia Pacific (APAC) currently dominates the market share, largely due to the concentration of major semiconductor manufacturers, automotive component suppliers, and extensive consumer electronics production bases in countries like China, South Korea, Japan, and Taiwan. North America and Europe, while smaller in production volume, are significant early adopters and demand centers, especially driven by the stringent reliability needs of the aerospace, defense, and high-end medical device industries. The trend across all regions is a progressive shift from traditional Alumina substrates to higher-performance materials like AlN and even specialized Zirconia, reflecting the universal need for better heat management across high-power applications.

Segment trends highlight the dominance of the Direct Bonded Copper (DBC) technology segment, essential for high-power modules, which consistently accounts for the largest revenue share. However, the Thin Film technology segment is projected to exhibit the highest Compound Annual Growth Rate (CAGR), driven by its suitability for high-precision, fine-line circuitry required in miniaturized RF and sensor applications, including advanced radar systems. Application-wise, the automotive sector remains the primary growth catalyst, particularly the adoption of Wide Bandgap (WBG) semiconductors (SiC and GaN) in EVs, which mandates the use of highly reliable, thermally efficient ceramic substrates for optimal performance and efficiency gains.

Common user inquiries regarding AI's impact on the Ceramic PCB market primarily focus on three key areas: how AI-driven design optimization influences substrate layout and material selection; the role of AI in enhancing manufacturing efficiency and quality control during complex production processes (such as metallization and etching); and the demand implications of AI hardware acceleration, specifically in data centers and edge computing where high-density, low-latency processing relies heavily on advanced thermal management solutions. Users are concerned about whether AI can truly mitigate the high cost and yield issues associated with complex ceramic processing and how the rapidly changing requirements of AI chips (e.g., increased power density) translate into evolving specifications for thermal substrates. The consensus theme is that AI acts both as a demand driver, necessitating powerful substrates, and as an optimization tool, promising efficiency gains in production.

AI's primary influence is accelerating the design cycle and enabling the creation of highly complex, thermally optimized ceramic PCB layouts that would be computationally prohibitive for traditional human designers. Machine learning algorithms are being employed to simulate thermal stress, predict fatigue under cycling, and optimize the material interface between the ceramic substrate and the copper layer, particularly relevant for DBC and ABC technologies. This predictive modeling capability reduces prototyping costs and time-to-market for specialized modules. Furthermore, AI-powered defect detection systems utilizing computer vision are significantly improving quality control in high-volume production, ensuring that minute flaws in the copper bonding or ceramic surface finish are identified instantly, thereby boosting manufacturing yield rates which are historically challenging in ceramic processing.

From a demand perspective, the proliferation of specialized AI accelerators (TPUs, GPUs, and custom ASICs) designed for high-throughput computing requires advanced packaging solutions capable of managing extreme thermal loads. Ceramic PCBs, especially those utilizing high-performance materials like Aluminum Nitride, are essential for cooling these power-hungry components in dense server farms and high-performance computing (HPC) environments. The future roadmap for AI implementation, including autonomous vehicles and industrial robotics leveraging edge AI, mandates highly reliable components that can withstand severe operating temperatures and vibrations, cementing the necessity of ceramic substrates as foundational technology for the AI revolution.

The Ceramic PCB market is primarily driven by the relentless advancement of power electronics, necessitated by the transition to electric mobility and renewable energy infrastructure, which demands components capable of managing high current and high voltage while maintaining reliability. The inherent superior thermal management provided by ceramic materials (especially AlN) is a key factor, directly addressing the limitations of polymer substrates when paired with Wide Bandgap (WBG) semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN). These semiconductors operate at higher temperatures and frequencies, making the low coefficient of thermal expansion (CTE) mismatch between the ceramic substrate and the chip crucial for preventing thermal stress failures. Additionally, the opportunity arising from the expansion of high-frequency 5G/6G communication systems and specialized radar applications (like those in ADAS) further necessitates ceramic substrates due to their low dielectric loss and stable performance at GHz frequencies.

However, the market faces significant restraints, most notably the high manufacturing cost associated with ceramic processing. Producing ceramic PCBs, particularly those involving DBC and ABC technologies, requires complex, high-temperature sintering and bonding processes, leading to elevated unit costs compared to conventional PCBs. Furthermore, the brittleness of ceramic materials poses challenges in large-format manufacturing and handling, contributing to potential yield losses. The competitive pressure from alternative thermal management solutions, such as metal core PCBs (MCPCBs) or sophisticated liquid cooling systems, though less effective in extreme conditions, sometimes presents a cost-effective alternative for mid-range power applications, constraining the rapid adoption of ceramic solutions in less critical sectors.

The key impact force shaping the market trajectory is the increasing global regulatory push for energy efficiency across all sectors, particularly transportation and industrial power conversion. This regulatory environment mandates the use of SiC and GaN devices, which inherently drives demand for thermally robust ceramic substrates. The confluence of technological opportunity (miniaturization, WBG adoption) and cost restraint means that manufacturers must focus intensely on improving production efficiency and developing lower-cost, high-performance ceramic alternatives. The market success is therefore heavily dependent on innovation in processing techniques (e.g., laser etching and advanced photolithography for fine-line circuitry) to reduce costs while maintaining the requisite thermal and electrical performance, positioning ceramic PCBs as non-negotiable components in critical high-reliability, high-power applications.

The Ceramic PCB market is broadly segmented based on material type, manufacturing technology, and end-use application, providing a granular view of market dynamics. Material segmentation highlights the dominance of Alumina (Al2O3) due to its cost-effectiveness and good performance in moderate power applications, contrasted with the rapid growth of Aluminum Nitride (AlN), which commands a premium but is essential for ultra-high-power and high-frequency modules where superior thermal management is non-negotiable. Manufacturing technology segmentation differentiates the market based on complexity and power handling capacity, with Direct Bonded Copper (DBC) being the volumetric leader, while Thin Film technology caters to highly integrated and precise RF circuitry. Understanding these segment dynamics is crucial for strategic market positioning and product development, especially concerning the varying price points and performance matrices required by different end-user industries.

The value chain for the Ceramic PCB market begins with the Upstream Analysis, which involves the procurement and processing of highly purified ceramic powders, primarily Alumina and Aluminum Nitride. Key raw material suppliers provide these powders, which are then converted into ceramic sheets or green tapes through processes like tape casting or pressing. The quality and purity of these materials are paramount, directly influencing the final substrate's thermal conductivity and dielectric properties. This stage requires specialized chemical processing capabilities, often controlled by a limited number of high-tech suppliers globally. Upstream activities are critical as fluctuations in raw material costs and supply chain stability for high-purity ceramic powders significantly impact the profitability and pricing of the finished PCBs.

The core manufacturing and midstream phase involves converting the raw ceramic material into a functional PCB. This stage is highly complex and differentiated by technology. For DBC PCBs, this involves directly bonding a thick copper layer onto the ceramic substrate at high temperatures in a controlled atmosphere. For Thin Film technology, it involves sputtering or vacuum deposition of metal layers followed by high-resolution lithography. Manufacturers utilize various Distribution Channels to reach the end-user market. Direct sales channels are predominant for specialized, high-volume contracts with Tier 1 automotive suppliers or aerospace integrators, ensuring technical specifications and customized designs are handled efficiently. Indirect channels, involving specialized distributors and value-added resellers, typically handle smaller-volume orders and serve fragmented markets like custom R&D and lower-volume industrial control systems.

Downstream analysis focuses on the integration of the ceramic PCBs into final electronic modules, often handled by Original Equipment Manufacturers (OEMs) or specialized module assemblers. For instance, in the automotive sector, ceramic PCBs are integrated into inverter modules or battery management systems. The purchasing decisions of these end-users are driven by technical performance (thermal stability, CTE matching) and long-term reliability rather than pure cost. The trend is moving towards close collaboration between ceramic PCB manufacturers and downstream integrators, ensuring seamless module design and optimal thermal interface material selection. This collaborative model, utilizing Direct channels, ensures that the high complexity and specific performance requirements of applications like high-power lasers and SiC/GaN power modules are consistently met.

The primary potential customers and end-users of the Ceramic PCB market are large-scale enterprises engaged in manufacturing high-reliability and high-power electronic systems where thermal management and signal integrity are critical determinants of product success. The largest consumer base resides in the Automotive sector, specifically manufacturers of Electric Vehicles (EVs), Hybrid Electric Vehicles (HEVs), and autonomous driving systems. These companies require ceramic substrates for their battery chargers, DC-DC converters, and motor control inverters, where SiC and GaN devices generate substantial heat that must be dissipated immediately to prevent performance degradation and ensure safety. Potential buyers include Tier 1 suppliers like Bosch, Continental, and Delphi, as well as major vehicle OEMs integrating power electronics in-house.

Another major customer segment is the Industrial sector, encompassing manufacturers of high-power lasers, railway traction systems, high-frequency industrial heating equipment, and high-reliability power supplies. These industrial buyers value the mechanical durability and chemical resistance offered by ceramic PCBs, ensuring continuous operation in harsh factory environments. Companies specializing in renewable energy infrastructure, such as solar power inverters and wind turbine control systems, are also rapidly growing customer groups. These applications demand exceptional thermal cycling capabilities and long lifespan, areas where ceramic substrates significantly outperform traditional metal core solutions, thus justifying the higher acquisition cost.

The Aerospace and Defense segment constitutes a high-value, albeit lower-volume, customer base. Potential customers here include defense contractors and avionics manufacturers that need lightweight, radiation-resistant, and thermally stable PCBs for radar systems, satellite communication equipment, and critical flight control systems. In this segment, the use of Thin Film ceramic technology for high-precision RF components is essential. Furthermore, the Medical equipment manufacturing industry, producing devices like high-resolution MRI machines and sophisticated diagnostic imaging systems, represents crucial buyers who prioritize absolute reliability and signal integrity, making ceramic PCBs a preferred substrate choice for their high-precision sensor and processing units.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 770 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | KYOCERA Corporation, CeramTec GmbH, Murata Manufacturing Co., Ltd., CoorsTek, Inc., TTM Technologies, Inc., Maruwa Co., Ltd., Remtec, Inc., Viking Tech Corp., Taiyo Yuden Co., Ltd., Micro Systems Technologies (MST), Kemet (Yageo), AISMALIBAR, Denka Company Limited, NGK Insulators, Ltd., A-TECH Ceramics, ACX Corporation, Cicor Group, KOA Corporation, Heilongjiang Core Power Semiconductor Technology Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Ceramic PCB market is defined by several advanced manufacturing processes engineered to optimize thermal dissipation and electrical performance. The most prevalent technology, Direct Bonded Copper (DBC), involves bonding high-purity copper foil directly onto ceramic substrates (typically Alumina or AlN) at high temperatures, forming a robust metallurgical bond without the use of adhesives. This technology is critical for high-power applications, such as automotive inverters, because it maximizes thermal transfer and current carrying capacity. Recent technological advances in DBC focus on achieving ultra-thin copper layers and complex, multi-layer structures to increase power density while reducing overall module size, which is vital for space-constrained EV applications. Optimization of the DBC process to handle larger substrate sizes and reduce residual internal stress remains a major area of research and development.

A significant technological development is Active Brazed Copper (ABC) technology, which utilizes a specialized brazing material to join the copper and ceramic, offering even higher mechanical strength and often allowing for the use of thicker copper layers than DBC, making it suitable for extremely demanding applications with aggressive thermal cycling. Parallelly, Thin Film technology dominates the high-frequency and miniaturization segment. Thin Film processes utilize sophisticated vacuum deposition and photolithography techniques, similar to semiconductor manufacturing, to create extremely fine line widths and precise patterns (often less than 50 micrometers). This precision is indispensable for complex microwave circuits, high-performance sensors, and multi-chip modules (MCMs) used in aerospace radar and 5G base stations, where signal integrity is paramount and standard Thick Film resolution is insufficient.

Furthermore, the materials technology front is evolving rapidly, moving beyond standard Alumina to highly engineered ceramic compositions. Aluminum Nitride (AlN) is increasingly becoming the substrate of choice for new designs due to its high thermal conductivity (5-10 times greater than Alumina), directly supporting the adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) power devices. Research is also focused on developing Low-Temperature Co-fired Ceramic (LTCC) and High-Temperature Co-fired Ceramic (HTCC) processes tailored for embedded components and complex 3D structures, enabling the integration of passive components directly within the substrate body. These co-fired technologies are key enablers for greater miniaturization and increased functional density in RF modules and sensor applications, consolidating multiple components onto a single, robust ceramic platform.

The Ceramic PCB market exhibits pronounced regional variances in terms of production capacity, technological adoption, and demand structure, primarily dictated by the concentration of advanced manufacturing industries and government electrification policies.

Ceramic PCBs offer significantly superior thermal conductivity, enabling efficient heat dissipation from power components, and possess a Coefficient of Thermal Expansion (CTE) closely matched to semiconductor chips (SiC/GaN), which prevents mechanical stress and improves device longevity, especially under severe thermal cycling conditions prevalent in automotive and industrial power modules.

Direct Bonded Copper (DBC) technology currently dominates the EV inverter market segment. DBC provides an excellent balance between high thermal performance, robust mechanical strength, and high current carrying capacity, making it ideal for the high-power modules used in EV battery management and motor control systems.

Aluminum Nitride is gaining market share due to its vastly superior thermal conductivity, which is crucial for maximizing the performance and reliability of Wide Bandgap (WBG) semiconductors (SiC and GaN). While Alumina is more cost-effective, AlN is essential for ultra-high-power density and high-frequency applications where effective heat removal is non-negotiable.

The aerospace and defense sector acts as a key driver for technological advancement, specifically in Thin Film ceramic technology. This sector requires high-precision, fine-line circuitry, light weight, and radiation resistance for advanced radar and communication systems, pushing manufacturers toward innovative, high-resolution deposition and patterning techniques.

The primary restraint is the high unit manufacturing cost, stemming from the complex, high-temperature processing required for materials like DBC and ABC. High raw material purification costs and the inherent brittleness of ceramic materials, leading to higher yield loss rates, contribute significantly to the elevated overall production expense.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.