ID : MRU_ 433152 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

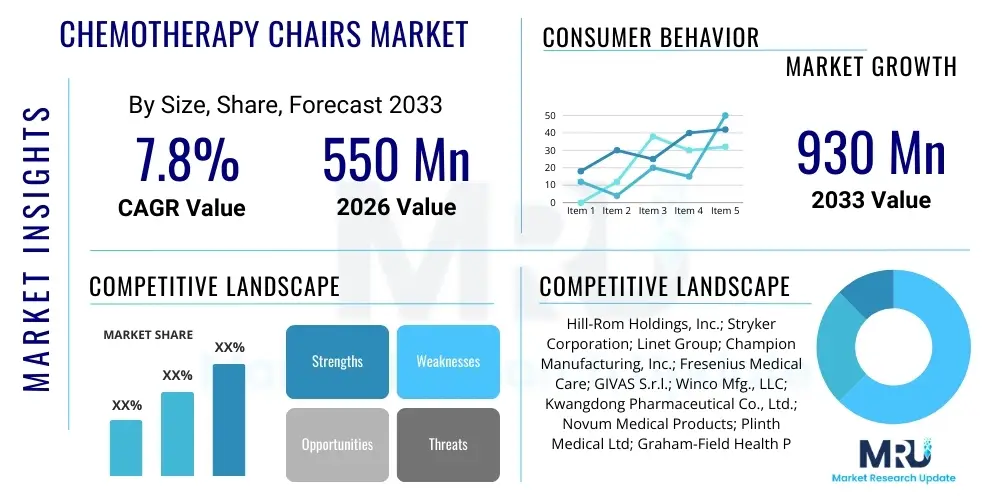

The Chemotherapy Chairs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $550 Million in 2026 and is projected to reach $930 Million by the end of the forecast period in 2033.

The Chemotherapy Chairs Market is dedicated to providing advanced, specialized seating systems crucial for the administration of infusion treatments, primarily chemotherapy, dialysis, and prolonged intravenous therapies. These chairs transcend conventional medical recliners by incorporating features specifically tailored to the oncological patient population, who often endure long periods of immobility and require rapid, safe repositioning. Design priorities center on exceptional ergonomic support to mitigate pressure ulcers, comprehensive adjustability, including specialized positioning for medical emergencies such as Trendelenburg, and the utilization of highly durable, non-porous materials that meet stringent clinical hygiene protocols. The technological sophistication embedded in these chairs, particularly in electric models, transforms the infusion experience from a purely clinical procedure into a more patient-centric service, reflecting the global trend toward improved quality of care in oncology settings.

The core functionality of modern chemotherapy chairs centers around maximizing patient safety and comfort during treatment sessions that can frequently span several hours. Beyond basic recline functions, advanced models integrate features like weight distribution measurement, built-in heating elements to combat chemotherapy-induced cold sensitivity, and adjustable armrests designed to optimize vein access for peripheral intravenous lines and ports. Major applications are concentrated within dedicated cancer treatment ecosystems, extending from university research hospitals and large municipal facilities to local community clinics and private infusion centers. The adoption is fueled by verifiable benefits, including enhanced workflow efficiency for nursing staff due to easy patient access and maneuvering, coupled with substantial improvements in patient satisfaction scores related to comfort and control over their environment, which are increasingly important metrics in value-based healthcare systems.

Driving the robust expansion of this market are several interconnected macro-economic and clinical factors. Foremost among these is the undeniable increase in global cancer incidence and prevalence, driven by aging populations and lifestyle factors, directly translating into a heightened requirement for infusion equipment globally. Concurrently, there is a systemic shift in healthcare delivery, particularly in developed economies, where outpatient infusion centers are replacing costly inpatient treatment days, drastically increasing the installed base requirement for specialized infusion chairs. Moreover, continuous innovation by key market players in connectivity, material science (antimicrobial coatings, pressure mapping foam), and power systems ensures that purchasers have access to continually improving, highly reliable equipment, thereby accelerating the replacement cycle for older, less functional manual chairs across established facilities.

The Chemotherapy Chairs Market exhibits a solid growth trajectory, fundamentally underpinned by demographic shifts and evolving clinical practices focused on outpatient care. Current business trends indicate intense competitive differentiation focusing on proprietary electric actuation systems that offer smooth, silent, and reliable movement, alongside modular design approaches that allow easy component replacement and feature upgrades. Manufacturers are actively pursuing partnerships with specialized healthcare technology providers to integrate chairs with hospital IT infrastructure, moving them toward 'smart' assets capable of relaying status, usage data, and maintenance alerts. Furthermore, sustainability and lifecycle management are becoming prominent procurement factors, favoring manufacturers who can demonstrate reduced environmental impact and prolonged operational lifespans for their equipment.

Geographically, market dynamics show a clear dichotomy: mature markets in North America and Western Europe command the largest installed bases and drive high-value sales focused on replacement and technological upgrade cycles. These regions prioritize sophisticated features like connectivity, advanced ergonomics, and compliance with strict regulatory bodies. In contrast, high-growth regions, particularly the Asia Pacific and Latin America, are characterized by infrastructural expansion, resulting in high volume demand. While cost-effectiveness initially dictates product choice in these regions (favoring hydraulic or basic electric models), the increasing establishment of international-standard private hospitals is concurrently accelerating demand for premium, imported chair solutions, creating a dual-tier market structure within these emerging geographies.

Analysis of segment trends confirms the continued market dominance of electric/powered chairs, largely due to their enhanced clinical utility and ability to provide complex repositioning effortlessly, which is critical for minimizing risk during lengthy infusions. The application sector is witnessing a pronounced shift; while hospitals remain foundational buyers, the fastest incremental growth is projected from specialized Ambulatory Surgical Centers (ASCs) and dedicated oncology clinics, reflecting the global focus on efficient, decentralized care models. Within materials, medical-grade vinyl remains the segment leader, valued for its cost-effectiveness, superior cleanability, and integration of infection control properties, addressing stringent hygiene protocols inherent in infusion therapy environments.

The integration of Artificial Intelligence (AI) into the Chemotherapy Chairs ecosystem, though indirect, is poised to revolutionize operational management and enhance patient safety within infusion centers. User inquiries frequently center on leveraging AI for predictive asset management—specifically, how algorithms can analyze usage frequency, motor performance metrics, and historical maintenance logs to accurately predict the optimal time for preventative intervention, thereby avoiding disruptive chair downtime during peak operating hours. Another central theme of inquiry revolves around the potential for AI-driven personalized comfort settings, where systems learn individual patient biometric responses and subjective feedback over a course of treatments to automate adjustments proactively, optimizing the therapeutic environment without continuous manual input from clinical staff. These expectations highlight a transition towards intelligent, adaptive clinical environments.

In practice, the near-term application of AI focuses heavily on optimizing clinic logistics and resource allocation. By feeding chair occupancy data, treatment duration, and patient scheduling information into proprietary AI engines, facility managers can achieve significantly improved throughput and reduce idle time. For instance, AI can dynamically adjust nurse-to-chair ratios based on predicted patient acuity and complexity of the infusion regimen being administered across all active stations. This not only makes the patient flow more efficient but also ensures that the high capital investment associated with advanced chemotherapy chairs is maximally leveraged, demonstrating an enhanced return on investment crucial for health systems operating under tight budgetary constraints. Furthermore, this data provides procurement teams with concrete evidence for future equipment purchasing decisions and capacity planning.

Looking ahead, the development of sophisticated AI layers integrated with chair technology will usher in new paradigms for continuous, non-invasive patient monitoring. Imagine a chair equipped with integrated sensors capable of measuring subtle changes in heart rate variability, skin temperature, or shifts in posture indicating discomfort or potential adverse reactions. The AI would process this data stream, cross-referencing it with the specific chemotherapy agent being administered and the patient's medical history. If an anomaly is detected that exceeds pre-set clinical thresholds, the AI system could trigger an immediate, high-priority alert directly to the attending nurse’s wearable device or the central monitoring station. This predictive and real-time intervention capability moves beyond simple monitoring, positioning the smart chemotherapy chair as an integral, life-saving diagnostic aid, thereby increasing both the perceived value and the technological barrier to entry in this segment.

The trajectory of the Chemotherapy Chairs Market is significantly influenced by a robust set of Drivers, Restraints, and Opportunities (DRO), which collectively shape its expansion and challenges. A primary driver is the accelerating global demographic trend of an aging population, which inherently leads to a higher incidence of age-related cancers and, consequently, a greater demand for specialized oncology treatments. This is complemented by continuous innovation in drug development, extending the duration and frequency of chemotherapy regimens, necessitating more comfortable and functional seating solutions for prolonged use. Further driving adoption is the strategic healthcare policy shift globally, particularly in developed nations, mandating the expansion of ambulatory care services, which inherently requires high volumes of infusion chairs to manage the outpatient caseload efficiently and cost-effectively, reducing overall hospital operational expenditure.

Conversely, the market faces structural restraints that limit unrestricted growth. The most significant constraint is the high initial capital outlay required for advanced electric and hydraulic chemotherapy chairs, which poses a considerable barrier, especially for newly established clinics or facilities in developing economies with limited budgetary allocations for capital equipment. Moreover, the complexity and cost associated with maintaining, servicing, and sourcing proprietary spare parts for motorized chairs can translate into high operating expenditures (OpEx) for end-users, requiring specialized technical expertise often unavailable in smaller facilities. Furthermore, the market must constantly navigate the complex and varied medical device regulatory landscapes across different countries, requiring substantial investment in compliance and certification, which slows product time-to-market and increases pre-commercialization costs.

Opportunities for exponential market growth are concentrated in three key areas: geographic expansion into underserved emerging markets; product diversification into highly specialized sub-segments, such as bariatric and pediatric oncology; and technological synergy. The ongoing decentralization of healthcare, pushing services closer to the patient (including home infusion), creates new niches for highly portable and user-friendly models, potentially leveraging lighter materials and simplified controls. Furthermore, integrating smart technology—such as built-in bio-sensors, IoT connectivity for remote diagnostics, and sophisticated pressure-relief systems—presents compelling opportunities for manufacturers to differentiate their products and capture a higher-value market segment focused on comprehensive patient monitoring and unparalleled comfort during infusion, aligning with modern precision medicine initiatives.

The segmentation of the Chemotherapy Chairs Market provides a clear framework for analyzing demand preferences, competitive dynamics, and regional market maturity. Segmentation is primarily based on Product Type (Manual, Hydraulic, Electric), Application (Hospitals, Specialty Clinics), and Material, reflecting the diverse needs concerning budget, clinical environment, and required functionality. Understanding these segments is critical for manufacturers to tailor their product offerings and marketing strategies effectively, ensuring they meet the specific compliance and operational requirements of varying healthcare settings globally, thereby maximizing market penetration and sales efficiency, particularly in procurement processes involving large hospital networks.

The Electric/Powered Chair segment represents the core value driver due to its indispensable role in facilitating complex patient repositioning, managing emergency scenarios with rapid Trendelenburg capability, and reducing physical strain on nurses. While they command a premium price, their adoption is justified by improved patient outcomes and superior operational safety records, making them the standard choice in developed economies. Conversely, Manual chairs maintain relevance in smaller clinics and budget-conscious markets, especially where power reliability is a concern, serving as reliable, low-maintenance alternatives, although their utility is severely limited for non-ambulatory or critically ill patients requiring complex medical positioning.

Within the Application segment, the shift towards Specialized Clinics and Ambulatory Surgical Centers (ASCs) is the most defining trend. As healthcare administrators seek to reduce the overall cost burden associated with inpatient care, high-volume infusion procedures are increasingly outsourced to these specialized, efficient outpatient settings. This transition demands chairs optimized for continuous usage, requiring exceptional durability and quick-clean surfaces. The Material segmentation reflects a constant balance between patient comfort and stringent hygiene demands, with medical-grade vinyl remaining the staple choice due to its robustness and resistance to cleaning agents, critical for maintaining infection control standards stipulated by healthcare bodies.

The Chemotherapy Chairs Value Chain commences with highly specialized upstream activities, primarily encompassing the meticulous sourcing of certified, medical-grade components. This involves acquiring high-tensile steel or aluminum alloys for frame construction, specialized actuation systems (motors, pistons, hydraulics), and medical plastics and foam that meet strict fire safety and toxicity standards. Upstream risk management focuses intently on supply chain resilience, ensuring the consistent quality of electronic components sourced globally, and navigating commodity price volatility, especially for metals. Manufacturers must maintain high inventory levels of specialized parts to support the warranty and maintenance phase downstream, ensuring minimal disruption to clinical operations for their end-users. Precision manufacturing and assembly, often subject to stringent ISO 13485 quality standards, follow this sourcing phase.

Midstream activities involve the core processes of manufacturing, extensive product stress testing, and achieving essential regulatory clearance (such as FDA approval, CE marking, or equivalent national certifications), which represent significant value-add stages and high entry barriers. Highly automated factories focus on modular design techniques to simplify assembly, enhance customization for regional variances (e.g., voltage requirements, specific load capacities), and streamline post-market servicing. The immediate downstream segment centers on market distribution, which is a critical determinant of global market reach and market share penetration. Distribution leverages a robust dual-channel strategy: Direct sales are utilized for major tenders or large purchasing groups, allowing for higher profit margins and direct control over branding, installation, and customized training protocols.

Indirect sales rely heavily on established regional medical equipment distributors who possess crucial local market knowledge, handle complex import logistics and customs clearance, provide localized installation, and are absolutely essential for penetrating smaller clinics and remote areas where a manufacturer lacks a dedicated presence. The final value delivery stage is defined by comprehensive post-sale services, including complex installation, in-depth staff training on advanced motorized functions, and establishing robust ongoing maintenance contracts, which are crucial for generating high-margin recurring revenue and ensuring long-term customer satisfaction and loyalty. Successful players continuously optimize this downstream segment by utilizing digital tools for remote diagnostics and inventory tracking, ensuring prompt availability of necessary spare parts and minimizing the Mean Time to Repair (MTTR), directly impacting the operational continuity and quality reputation of oncology centers.

The core customer base for chemotherapy chairs consists predominantly of institutions and facilities specializing in the diagnosis and long-term management of cancer patients requiring systemic therapy. The largest and most influential buyers are tertiary care hospitals and major cancer centers, which invest heavily in high-capacity, advanced electric chairs to manage high patient volumes and complex treatment schedules. Procurement decisions in these facilities are often driven by centralized purchasing departments, focusing on criteria such as extreme durability, comprehensive warranty coverage, advanced infection control capabilities, and the total cost of ownership over the equipment's lifespan, often requiring chairs that integrate seamlessly with facility-wide IT and monitoring systems to facilitate data exchange.

A rapidly expanding customer segment includes specialized, freestanding ambulatory surgical centers (ASCs) and dedicated outpatient infusion clinics. These buyers prioritize operational efficiency and patient comfort, seeking chairs that optimize space utilization and facilitate quick patient turnover. For these centers, modularity, ease of cleaning, and features enhancing patient self-sufficiency (like easy-to-reach controls and charging ports) are highly valued because they directly contribute to faster patient transitions and higher revenue throughput. The purchasing cycle in ASCs tends to be faster and more focused on specific feature sets tailored to routine outpatient infusion procedures, often favoring manufacturers who offer quick delivery and installation timelines.

Additionally, government healthcare agencies, military hospitals, and non-profit organizations focused on palliative care represent significant, albeit often tender-driven, customer segments. These institutions focus intensely on competitive pricing and proven compliance records. In niche markets, particularly those focusing on geriatric care, home health services, or bariatric specialties, smaller, highly portable, or custom-built chairs might be purchased for individual patient care. These buyers, though smaller in volume, demand extremely specialized ergonomic and safety features, demonstrating a willingness to invest significantly in solutions that address complex patient needs outside the standard high-volume clinical environment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $550 Million |

| Market Forecast in 2033 | $930 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hill-Rom Holdings, Inc.; Stryker Corporation; Linet Group; Champion Manufacturing, Inc.; Fresenius Medical Care; GIVAS S.r.l.; Winco Mfg., LLC; Kwangdong Pharmaceutical Co., Ltd.; Novum Medical Products; Plinth Medical Ltd; Graham-Field Health Products; Optima Medical Inc.; Med-Mizer, Inc.; United Medical Co.; Merivaara Corp.; Burlodge UK Ltd.; Malvestio S.p.a.; UMF Medical; Drive DeVilbiss Healthcare; Shaoxing Shangyu Fengming Medical Devices Co., Ltd.; Tarsus Medical; GF Health Products, Inc.; Infinium Medical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution within the Chemotherapy Chairs Market is characterized by a drive toward advanced electromechanical systems designed for precision and patient safety. Central to this landscape are robust, multi-axis electric actuators and control systems that enable smooth, reliable movement through a wide range of positions, including the critical Trendelenburg position necessary for specific clinical interventions. These sophisticated power systems feature integrated failsafes and high-capacity battery backup capabilities, ensuring uninterrupted functionality and patient safety even during electrical failures. Furthermore, the electronic interface often includes programmable memory presets, allowing nurses to quickly recall optimal, personalized positioning for repeated patients, significantly enhancing workflow efficiency and minimizing the risk of positional errors during critical treatment phases.

A second major technological front involves material innovation focused intensely on pressure management and rigorous infection control. Manufacturers are increasingly utilizing complex viscoelastic foams and multi-layer gel padding systems that conform precisely to the patient's body contours, dynamically redistributing pressure away from vulnerable bony prominences. This is crucial for mitigating the risk of pressure ulcers, a serious complication during long, immobile infusion sessions. These specialized comfort materials are universally encased in high-performance, medical-grade vinyl or polyurethane textiles treated with persistent antimicrobial agents (e.g., silver or copper ions). This surface technology ensures that the chairs are highly resistant to harboring pathogens and can withstand aggressive, frequent cleaning protocols required by stringent hospital infection prevention guidelines.

The most forward-looking technology involves robust connectivity and seamless data integration, pushing the chairs into the realm of 'smart' medical devices. High-end chairs are increasingly equipped with embedded IoT modules, allowing them to communicate their operational status, usage frequency, and precise maintenance requirements wirelessly to centralized hospital Asset Information Management Systems (AIMS). This functionality facilitates remote diagnostics and enables highly accurate predictive maintenance scheduling, transitioning equipment management from costly, reactive repair to proactive, cost-saving intervention. Future technological standards are expected to integrate sophisticated sensor arrays capable of measuring biofeedback (such as subtle shifts in posture or skin temperature) and environmental conditions, feeding data into AI systems to create a truly adaptive, optimized therapeutic environment tailored to the patient’s precise physiological state during chemotherapy.

North America maintains its stronghold as the most significant market region, driven by unparalleled spending on advanced oncology equipment and a high concentration of leading specialized cancer treatment centers. The region's market is characterized by a high preference for technologically advanced products, specifically premium electric chairs with integrated connectivity features, complex safety mechanisms, and robust data logging capabilities. Regulatory compliance, particularly FDA standards, dictates stringent product specifications, fostering an environment where innovation in patient safety and seamless data integration is paramount. The presence of major global market players and favorable governmental and private reimbursement policies for outpatient infusion therapy further solidify North America’s dominance in terms of market value and cutting-edge technological adoption.

The European market, constituting the second-largest share, demonstrates mature demand stabilized by universal government healthcare programs and pervasive private insurance coverage. Countries across Western Europe, particularly the Nordics, Germany, and Central Europe, prioritize equipment with exceptional longevity, rigorous ergonomic design, and full compliance with strict European Conformity (CE) standards. Procurement decisions often favor manufacturers who can demonstrate a low total cost of ownership (TCO) over a functional lifespan typically exceeding ten years, emphasizing repairability and readily available spare parts, fitting within public sector budgetary constraints. The rising overall cancer burden, coupled with the continued expansion of private healthcare options, ensures sustained growth, although often at a more moderate, stable pace compared to the burgeoning markets of the East.

Asia Pacific (APAC) is unequivocally identified as the fastest-growing regional market globally. This explosive growth is attributable to massive government and private sector investment in rapidly expanding healthcare infrastructure, dramatically increasing public awareness of cancer screening, and significantly improved access to advanced treatment for large, previously underserved populations. While manual and basic hydraulic chairs satisfy the initial bulk demand in rural and lower-tier urban hospitals due to acute cost sensitivity, major metropolitan hubs like Shanghai, Singapore, and Sydney are adopting high-specification electric models at a rapid pace to align their facilities with international clinical standards. This region presents both the largest opportunity for high-volume sales and the greatest complexity regarding price point sensitivity and navigating highly diverse regulatory and logistical frameworks across its many constituent nations.

Market growth is predominantly driven by the increasing global prevalence of cancer requiring systemic treatment, the accelerated shift toward cost-effective outpatient infusion therapy replacing expensive inpatient stays, and continuous technological advancements improving chair ergonomics, patient comfort, and clinical workflow efficiency features.

Electric or powered chemotherapy chairs currently hold the largest market share in terms of value. This dominance is due to their superior safety features, highly adjustable and programmable positioning capabilities, and ability to minimize physical strain on nursing staff during patient handling and critical repositioning procedures.

AI integration focuses on optimizing operational performance and monitoring. This includes using AI algorithms for predictive maintenance to prevent equipment failures, optimizing scheduling for better clinic throughput efficiency, and processing sensor data for real-time, non-invasive patient vital sign monitoring during prolonged infusion sessions, improving safety.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period. This rapid expansion is fueled by massive public and private investment in healthcare infrastructure, increasing access to oncology care, and the modernization of clinical facilities in major urban centers across the region.

Hospitals prioritize several key attributes: extreme durability for multi-shift use, stringent infection control capabilities (antimicrobial, non-porous surfaces), low total cost of ownership (TCO) over the product lifecycle, and the chair's ability to seamlessly integrate with existing electronic health record (EHR) and centralized asset management systems.

Hydraulic chairs rely on a foot pump or manual lever system for lifting and adjusting height, making them less expensive but requiring physical effort. Electric chairs use quiet, motorized actuators for all adjustments (height, recline, tilt), offering greater precision, ease of use, and essential rapid emergency positioning capabilities via simple electronic controls.

Manufacturers utilize medical-grade materials, primarily vinyl and polyurethane, that are non-porous and often treated with embedded antimicrobial agents. These materials are engineered to resist the absorption of fluids and withstand harsh, frequent cleaning chemicals, which is crucial for preventing the spread of healthcare-associated infections (HAIs) in high-risk oncology settings.

While hospitals and clinics remain the dominant application segment, homecare is an emerging niche. Growth is driven by the increasing trend of specialized at-home infusion services, requiring highly portable, easily maneuverable, and simple-to-operate chairs that prioritize patient comfort in a residential environment without compromising safety features.

Future development focuses on enhanced biofeedback mechanisms, integrating advanced pressure-mapping sensors for ulcer prevention, incorporating IoT connectivity for predictive maintenance alerts, and developing modular designs that allow for easier upgrades and customization based on specific patient cohorts (e.g., bariatric or pediatric oncology).

The greatest restraint in developing regions is the high initial capital expenditure (CapEx) required for advanced, motorized chemotherapy chairs. This economic constraint necessitates that facilities often opt for less feature-rich manual or basic hydraulic models, thereby limiting the immediate adoption rate of high-end, clinically optimal equipment despite growing demand.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.