ID : MRU_ 431695 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

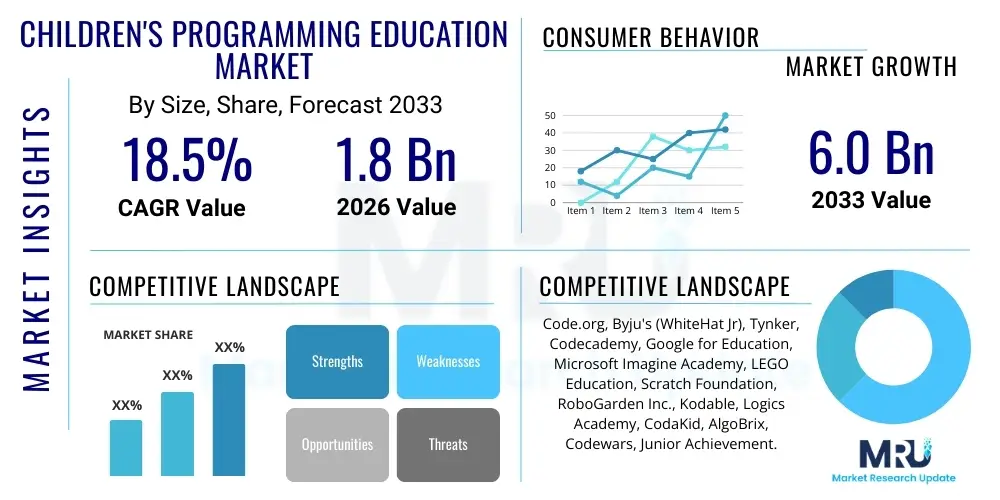

The Children's Programming Education Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 6.0 Billion by the end of the forecast period in 2033.

The Children's Programming Education Market encompasses educational products and services designed to teach computational thinking and coding skills to children, typically ranging from ages 4 to 18. This burgeoning sector is driven fundamentally by the recognition that digital literacy is an essential skill for future workforce readiness, transcending traditional notions of purely vocational training. Products range from visual, block-based programming tools like Scratch for younger learners to text-based languages such as Python and JavaScript utilized in curriculum designed for middle and high school students. The core objective is not merely code memorization but fostering problem-solving abilities, logical reasoning, and creativity through structured computational challenges.

Major applications of children's programming education span formal K-12 schooling, extracurricular activities, and direct-to-consumer (D2C) online platforms. The market has observed a significant shift toward blended learning models, where asynchronous digital content is complemented by synchronous instructor-led sessions, catering to varying parental preferences and geographical access requirements. The benefits derived from these programs are profound, extending beyond technical proficiency to improved academic performance in science and mathematics, enhanced critical thinking, and a greater capacity for iterative design and debugging—skills highly valued across all modern industries.

Driving factors fueling this market include increasing governmental emphasis on STEM (Science, Technology, Engineering, and Mathematics) education integration across mandatory schooling curricula worldwide. Furthermore, elevated disposable incomes in key emerging economies, coupled with growing parental investment in supplemental education perceived as future-proofing their children's careers, contribute significantly to market expansion. The rapid proliferation of accessible educational technologies, including low-cost hardware like Raspberry Pi and microcontrollers, makes sophisticated programming concepts more tangible and engaging for young audiences, accelerating the adoption rate across diverse socioeconomic strata.

The Children's Programming Education Market is characterized by robust growth and continuous innovation, largely driven by the global imperative to cultivate a digitally skilled generation. Business trends indicate a strong move toward platform consolidation, with major EdTech companies acquiring specialized coding curriculum providers to offer comprehensive educational ecosystems. Geographic expansion remains a key focus, particularly targeting the vast, untapped potential within the Asia Pacific region, where dense populations and high educational competitiveness drive premium spending on supplementary learning resources. Hybrid delivery models are dominating, offering the flexibility of online learning alongside the structured interaction of in-person camps or tutoring, thereby maximizing market reach and customer retention.

Regional trends highlight North America and Europe as mature markets leading in curriculum standardization and integrating advanced concepts like Artificial Intelligence (AI) and Machine Learning (ML) into early programming courses. Conversely, the Asia Pacific (APAC) region, spearheaded by countries like China and India, is registering the highest growth rate, fueled by substantial government investment in digital infrastructure and intense pressure on students to excel in highly competitive academic environments. Latin America and the Middle East and Africa (MEA) are emerging regions experiencing accelerated growth, driven by increasing internet penetration and partnerships between international curriculum providers and local educational ministries aiming to modernize their public schooling systems.

Segmentation trends reveal that the K-6 segment (early learners utilizing block-based coding) remains the largest by volume, primarily due to the foundational nature of these products and widespread school adoption. However, the K-12 segment, focusing on advanced languages like Python for practical application development, is projected to exhibit the fastest Compound Annual Growth Rate, reflecting the shift toward preparing older students for immediate higher education or professional pathways in technology. Delivery mode analysis shows that online learning platforms hold significant market share due to their scalability and accessibility, but specialized coding bootcamps and subscription-based curriculum services are rapidly gaining traction due to perceived higher quality and personalized instructor attention.

Common user questions regarding AI's impact on children's programming education center heavily on curriculum relevance, personalization capabilities, and the potential displacement of traditional programming languages. Users frequently ask if current coding curricula are future-proof against generative AI tools, how AI can customize learning paths for children with varying aptitudes, and what ethical and safety guidelines are being implemented for AI-powered educational software. Furthermore, there is significant interest in understanding how teaching computational thinking evolves when children can utilize AI assistants to write and debug code. The key themes summarized from these inquiries underscore a dual expectation: AI must enhance the efficiency and personalization of learning, while simultaneously teaching students how to critically interact with and eventually develop AI technologies themselves, ensuring programming education remains a core skill despite automation.

The market dynamics are significantly influenced by a confluence of accelerating drivers (D) and substantial growth opportunities (O), counterbalanced by specific restraints (R) pertaining primarily to cost and standardization. The major drivers include the inescapable necessity of digital skills in the 21st century workforce, leading to high parental willingness to invest, complemented by technological advancements that make coding platforms highly engaging through gamification and immersive virtual environments. Opportunities are manifest in the integration of specialized technologies like robotics and the metaverse into coding curricula, along with substantial scope for expanding penetration into public school systems globally through large-scale, cost-effective digital deployment models. Conversely, restraints involve the high initial cost of premium coding bootcamps, the persistent shortage of qualified programming instructors, particularly in developing regions, and the lack of a standardized global curriculum structure, which can confuse parents and institutions regarding educational quality.

Impact forces currently shaping the market trajectory are predominantly technological and socio-economic. The rapid evolution of educational technology platforms—moving from simple online tutorials to sophisticated, adaptive learning systems leveraging AI—exerts strong upward pressure on market growth (Impact Force: High). Socio-economic factors, such as rising global middle-class wealth and the ensuing 'educational arms race' among parents in countries like India and China, ensure sustained high demand. Regulatory policies, especially governmental moves to mandate computational thinking in early grades, provide a structural foundation for long-term institutional adoption. The combined effect of these impact forces suggests a market that is highly resilient to cyclical economic downturns, focused heavily on quality differentiation, and poised for exponential scaling through digital infrastructure.

The strategic deployment of capital by venture firms into specialized EdTech startups focused on K-12 coding underscores the market's high growth potential. Market players must navigate the challenge of maintaining content relevance against the pace of technological change (e.g., the rise of generative AI) while simultaneously addressing equity issues regarding access to high-quality instruction. Successfully mitigating restraints—specifically training a large cohort of qualified instructors and offering flexible, standardized content bundles—will be crucial for capitalizing on the broad opportunities presented by integrating coding education into mainstream academic life.

The Children's Programming Education Market is extensively segmented based on criteria such as delivery mode, programming language, end-user age group, and platform type, reflecting the diversity of educational needs and technological maturity across demographics. Analysis of these segments reveals distinct growth patterns and competitive landscapes. The segmentation allows market participants to tailor their content and distribution strategies effectively, targeting specific cohorts, such as leveraging block-based visual platforms for primary school students (Age 4-8) via direct-to-consumer online subscriptions, or focusing on enterprise software licensing models that provide Python and JavaScript curricula to large school districts (End-User: K-12 Institutions).

The value chain for the Children's Programming Education Market begins with the Upstream phase, involving the creation of educational technology, content, and curriculum standards. Key upstream participants include educational software developers who build coding platforms (like Scratch Foundation or specialized EdTech firms), content developers who design age-appropriate course materials, and hardware manufacturers providing educational robotics kits and computing devices (e.g., micro:bit). The quality and innovation at this stage directly dictate the pedagogical efficacy and engagement levels of the downstream products. Intellectual property rights concerning proprietary curriculum design and the interoperability of software platforms are critical determinants of competitive advantage in this segment.

The midstream phase focuses on the delivery and facilitation of education. This is dominated by training providers, including independent coding schools, franchised tutoring centers, and the instructional arms of online platforms. A crucial component here is the effective training and retention of qualified instructors, as the quality of human instruction remains a significant differentiator in premium markets. Distribution channels are varied, encompassing direct sales models (online subscription services to parents), indirect channels (licensing curriculum to existing public or private schools), and channel partners (telecom providers or device retailers bundled with educational software). The operational efficiency of these platforms, including stable video conferencing and interactive coding environments, is vital for maintaining customer satisfaction, especially in live online tutoring models.

The Downstream phase involves the end-users and the ultimate consumption of the service. Primary downstream actors are parents and individual students making direct purchasing decisions, and K-12 institutions procuring licenses for mass student deployment. Effective market penetration requires tailored marketing strategies addressing the specific needs of these two major buyer groups—where parents prioritize perceived career benefits and individualized attention, institutions prioritize scalability, curriculum mapping to national standards, and verifiable efficacy data. Direct distribution via proprietary online learning management systems (LMS) is highly effective for maintaining control over the user experience, while indirect distribution through strategic school partnerships ensures widespread institutional adoption, particularly in regions where government tenders dominate procurement decisions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 6.0 Billion |

| Growth Rate | CAGR 18.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Code.org, Byju's (WhiteHat Jr), Tynker, Codecademy, Google for Education, Microsoft Imagine Academy, LEGO Education, Scratch Foundation, RoboGarden Inc., Kodable, Logics Academy, CodaKid, AlgoBrix, Codewars, Junior Achievement. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape within the Children's Programming Education Market is characterized by a blend of foundational open-source tools and proprietary, sophisticated EdTech platforms designed specifically for scalability and pedagogical efficacy. Foundational tools include visual programming environments such as Scratch and Blockly, which utilize drag-and-drop interfaces to introduce programming logic without the frustration of syntax errors, making them ideal for younger demographics (4-10 years old). As students progress, platforms transition to supporting industry-standard text-based languages, with Python dominating due to its simplicity, readability, and widespread use in data science and AI applications. This tiered technological approach ensures a smooth learning curve from abstract concepts to practical application development.

A significant technological development is the integration of advanced learning management systems (LMS) and adaptive technology. These proprietary platforms leverage cloud computing to deliver high-availability, interactive coding environments accessible via web browsers, eliminating the need for complex local software installations. Adaptive learning technology, powered by machine learning algorithms, monitors student engagement metrics, error rates, and time-on-task to dynamically adjust curriculum flow and resource allocation. This level of technological sophistication moves the market beyond static video tutorials toward highly personalized, data-driven instructional methodologies that maximize efficiency and cater to diverse learning styles within a single digital ecosystem.

Furthermore, hardware integration and immersive technologies are increasingly prominent. Educational robotics kits (utilizing platforms like LEGO Education or Arduino) provide tangible, kinesthetic learning experiences where children can immediately see the physical results of their code, significantly boosting engagement. Virtual Reality (VR) and Augmented Reality (AR) are beginning to be piloted to create immersive coding environments, allowing children to manipulate digital objects or build virtual worlds using programming logic. The overall technological direction emphasizes highly engaging, scalable, and data-rich ecosystems that connect visual interfaces, standardized coding practices, and real-world physical computing applications, thereby future-proofing the educational offerings against rapid shifts in IT demands.

The global market for Children's Programming Education demonstrates significant regional disparities in maturity, growth rates, and primary consumption models. North America is characterized by high market penetration, driven by early adoption of STEM mandates in major school districts and substantial private sector investment in coding camps and subscription services. The region excels in content innovation, particularly in integrating advanced concepts like cybersecurity and game development into high school curricula. Consumers are willing to pay a premium for specialized, instructor-led, and accreditation-focused programs, maintaining the region's strong revenue contribution, despite a moderate growth rate compared to emerging markets.

Europe presents a diverse landscape, with Nordic countries leading in incorporating computational thinking into public compulsory education from an early age, often through government-funded initiatives that prioritize equity of access. Western European countries like the UK, France, and Germany show strong demand for certified vocational programming tracks for teenagers. However, the market growth across Europe is often moderated by linguistic barriers and decentralized educational governance, requiring providers to localize content extensively and gain certifications aligned with specific national curricula, such as the UK’s computing curriculum standards.

Asia Pacific (APAC) stands out as the engine of future market growth, expected to record the highest CAGR during the forecast period. This rapid expansion is fueled by massive middle-class populations, intense competition for university admission, and supportive government policies in countries like China, India, Singapore, and South Korea, which view programming education as a critical national strategy for technological superiority. D2C models, particularly online tutoring platforms like WhiteHat Jr (Byju’s), have achieved tremendous scale in this region by tapping into high parental aspiration and providing convenient, instructor-led classes delivered outside of traditional school hours.

Latin America and the Middle East and Africa (MEA) are emerging markets exhibiting accelerating adoption, predominantly driven by increasing smartphone penetration and government initiatives aimed at digital transformation. While challenges related to internet infrastructure quality and affordability persist, the low market maturity presents substantial opportunities for providers offering scalable, low-cost digital curricula. Partnerships with local telecom operators and subsidized access programs are common strategies for initial market entry in these regions, focusing primarily on foundational digital literacy and entry-level programming skills such as Scratch and introductory Python.

The Children's Programming Education Market is projected to experience robust expansion, recording a CAGR of 18.5% between the forecast years of 2026 and 2033, driven by global digital literacy mandates.

The Asia Pacific (APAC) region is forecasted to exhibit the highest Compound Annual Growth Rate due to large, educationally competitive populations and increasing governmental support for mandatory computational learning in K-12 schools.

The curricula for older students predominantly feature industry-standard, text-based languages such as Python and JavaScript, while younger learners (Ages 4-8) typically begin with visual, block-based platforms like Scratch or Blockly.

AI is transforming delivery through adaptive learning systems that personalize pacing and content difficulty based on real-time student performance data, alongside providing automated grading and instant feedback on coding assignments.

The market primarily utilizes Online/Virtual Learning (both self-paced and live instructor-led), Offline/Physical Learning (coding camps and centers), and increasingly, Hybrid Models that combine digital flexibility with structured in-person or live virtual instruction.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.