ID : MRU_ 437708 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

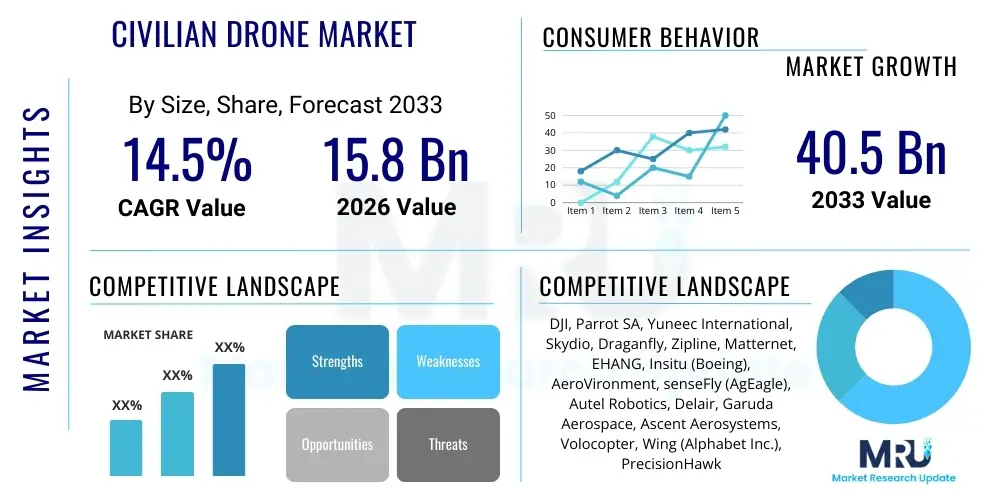

The Civilian Drone Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2026 and 2033. The market is estimated at USD 15.8 Billion in 2026 and is projected to reach USD 40.5 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the increasing adoption of professional-grade Unmanned Aerial Vehicles (UAVs) across critical infrastructure sectors, including energy, construction, and telecommunications, alongside the significant maturation of regulatory frameworks in major economies which facilitate expanded operational scope, particularly for Beyond Visual Line of Sight (BVLOS) missions. The economic efficiency and superior data acquisition capabilities offered by modern civilian drone platforms are replacing traditional, slower, and often dangerous inspection methods, cementing the drone market's transition from a niche technology to an essential enterprise tool.

The Civilian Drone Market encompasses the manufacturing, sales, and service provision of UAVs designed for non-military, professional, and recreational purposes. These sophisticated flying platforms, ranging from lightweight quadcopters used for photography to heavy-lift hexacopters utilized in logistics and infrastructure inspection, integrate cutting-edge technologies like advanced sensor suites (LiDAR, thermal cameras, hyperspectral imaging), sophisticated flight control systems, and complex navigation software. The primary function is to gather, analyze, and transmit high-resolution spatial and visual data efficiently, offering unprecedented perspectives and operational insights across diverse industrial landscapes. The evolution from consumer toys to enterprise-grade robotics marks the crucial phase of market development, highlighting enhanced reliability, increased payload capacity, and superior endurance as key product differentiation attributes.

Major applications of civilian drones span a vast spectrum, including precision agriculture for crop health monitoring, detailed infrastructure inspection (bridges, pipelines, wind turbines), surveying and mapping (geospatial data collection, 3D modeling), public safety (search and rescue, surveillance), media and entertainment, and, increasingly, commercial delivery and logistics in urban and remote settings. These applications leverage drones' ability to operate in hazardous or hard-to-reach areas, significantly reducing operational costs and minimizing risks associated with human labor. Furthermore, the real-time data processing capabilities, often facilitated by edge computing integration, allow immediate decision-making, which is critical in dynamic environments like emergency response or time-sensitive construction projects.

Key driving factors propelling the market growth include the favorable harmonization of global drone regulations, which allows for broader commercial use cases, particularly in advanced operations like autonomous BVLOS flights. The continual decrease in hardware costs coupled with improvements in battery technology (enhancing flight endurance) and the integration of artificial intelligence for autonomous navigation and data analysis further bolster market expansion. Benefits realized by end-users—such as enhanced worker safety, reduction in operational downtime, superior data accuracy, and significant cost savings compared to traditional methods (like using manned aircraft or scaffolding)—make the investment in drone technology increasingly justifiable across large-scale industrial operations globally.

The Civilian Drone Market exhibits robust growth driven by technological convergence and regulatory adaptation. Business trends are characterized by fierce competition among hardware manufacturers, leading to rapid feature enhancements, miniaturization of sensors, and increased focus on security and data privacy compliance. A significant shift is observed towards Software-as-a-Service (SaaS) models, where the value proposition moves beyond the physical UAV to include sophisticated data processing, fleet management, and AI-driven analytics platforms. Enterprise adoption is accelerating, preferring integrated solutions that combine hardware reliability with software intelligence, moving away from fragmented drone usage towards systematic, scalable drone programs managed centrally, particularly in sectors such as oil and gas, utilities, and public works.

Regional trends indicate North America and Europe maintaining leadership due to advanced regulatory acceptance (e.g., FAA regulatory updates and EASA framework) and strong corporate investment in automation technologies. Asia Pacific, particularly China and India, is emerging as the fastest-growing region, fueled by massive infrastructure projects, dense manufacturing bases, and rapid urbanization, which necessitate scalable aerial mapping and logistics solutions. Furthermore, increasing investment in defense modernization often leads to technology spillover into civilian applications, accelerating local production and innovation. The Middle East and Africa (MEA) are showing promising growth, primarily driven by investments in smart city development and agricultural modernization projects utilizing precision farming techniques.

Segment trends underscore the dominance of the professional segment over the recreational segment in terms of revenue growth and technological sophistication. Fixed-wing and Hybrid Vertical Takeoff and Landing (VTOL) drones are gaining traction for long-range surveillance and corridor mapping tasks, challenging the dominance of traditional multirotor designs, especially in energy and agricultural applications where endurance is paramount. Payload segmentation highlights a growing demand for high-end specialized payloads, such as LiDAR scanners and high-resolution multispectral cameras, necessary for precise engineering and scientific applications. Service delivery models, encompassing drone maintenance, pilot training, and data analysis outsourcing, are witnessing the highest CAGR, reflecting the shift among enterprises to consume drone capabilities as a managed service rather than managing complex internal drone operations.

User inquiries concerning the impact of Artificial Intelligence (AI) on the Civilian Drone Market predominantly revolve around three critical themes: autonomy and safety, data processing efficiency, and regulatory implications for automated flight. Users frequently ask how AI can enhance drone collision avoidance (sense-and-avoid capabilities), whether fully autonomous BVLOS flights are technically and legally feasible, and how AI-driven analytics can transform raw sensor data into actionable business intelligence. The key concern is often the reliability and ethical implications of machine learning algorithms operating in complex, dynamic airspace, and the regulatory uncertainty surrounding AI validation for flight safety. Expectations are high regarding AI's potential to dramatically reduce operational complexity and labor costs, standardizing and accelerating data capture and inspection workflows across industrial applications.

AI is fundamentally restructuring the operational parameters of civilian drones, moving them from remotely piloted devices to intelligent, autonomous platforms. At the edge, AI processors enable real-time object detection, classification, and path planning, which are essential for safe navigation, particularly in cluttered environments like construction sites or urban airspace. This shift facilitates complex maneuvers and dynamic mission adjustments without continuous human input, which is the necessary prerequisite for scaling large drone fleets. Furthermore, AI algorithms optimize energy consumption by calculating the most efficient flight paths and managing complex payloads, thereby extending operational windows and improving mission throughput, which directly impacts the economic viability of drone services.

In the downstream segment, AI’s impact is perhaps most transformative in data analysis. Traditional drone data processing, often involving manual identification of defects or features in vast datasets, is time-consuming and prone to human error. AI-driven computer vision models automatically detect anomalies (e.g., cracks in infrastructure, plant disease in agriculture, unauthorized construction), classify them based on severity, and generate predictive maintenance reports. This automation dramatically reduces the time-to-insight, ensuring that organizations can utilize drone-collected data immediately for strategic planning and corrective action. The integration of deep learning and neural networks is key to handling the massive volume and diversity of data generated by modern high-fidelity drone sensors.

The market is predominantly influenced by robust drivers stemming from technological advancements and economic incentives, juxtaposed with critical restraints rooted in regulatory hurdles and public perception. Opportunities arise primarily from untapped verticals and the commercialization of specialized technologies like heavy-lift cargo drones and counter-UAS (C-UAS) systems for airspace management. The interplay of these forces, particularly the acceleration of regulatory reform spurred by demonstrated economic utility, dictates the overall market trajectory. The impact forces are currently net positive, indicating a strong momentum toward widespread enterprise integration, provided that industry stakeholders successfully collaborate with regulatory bodies to mitigate safety and privacy concerns, thereby unlocking the full commercial potential of drone operations globally.

Key drivers include the demonstrable Return on Investment (ROI) across industries due to reduced inspection time and increased safety; continuous innovation in hardware components such as extended battery life and lighter, stronger composite materials; and the increasing accessibility of high-fidelity sensors (LiDAR, high-resolution EO/IR). The availability of drone pilot training and certification programs is professionalizing the industry, ensuring competent operations. Conversely, the major restraints involve fragmented and slow-to-adapt regulatory environments, particularly concerning BVLOS and urban operations, which stifle scalability. Public apprehension regarding privacy invasion, noise pollution, and security risks associated with malicious drone use (drones being weaponized or used for smuggling) also poses a significant non-technical constraint on market expansion.

The primary opportunities lie in the specialized cargo and medical logistics sector, which requires robust, high-payload UAVs for delivery to remote or inaccessible locations. Furthermore, the integration of 5G and future 6G networks offers opportunities for reliable, low-latency command and control (C2), essential for large-scale autonomous fleet management in urban air mobility (UAM) concepts. The impact forces, such as competitive pressure for automation in construction and infrastructure, coupled with governmental mandates for modernization and digitalization, are compelling industries to invest heavily. The convergence of AI, IoT, and drone technology is creating a powerful ecosystem that forces legacy businesses to adopt these platforms to maintain competitive relevance and operational resilience in the modern industrial landscape.

The Civilian Drone Market is comprehensively segmented based on technology, payload capacity, application, and end-user, reflecting the diverse requirements of professional and consumer users. Technology segmentation distinguishes between rotary-wing, fixed-wing, and hybrid platforms, each optimized for different flight profiles and mission requirements—rotary for agility and hovering, fixed-wing for long-range coverage, and hybrid combining the best of both. The application segments, ranging from surveying to inspection and delivery, highlight where the highest value is generated, while end-user classification (e.g., Construction, Agriculture, Energy) provides insight into industry-specific adoption rates and procurement behaviors. The market dynamic is increasingly defined by the Professional segment, demanding custom hardware and integrated software solutions tailored for industrial precision.

The Civilian Drone Market value chain begins with upstream activities, focusing heavily on the research, development, and manufacturing of core components. This segment is dominated by specialized suppliers of propulsion systems (motors, propellers), advanced battery technologies (high-density Li-Po/Li-ion), sophisticated flight controllers, and specialized sensor payloads (e.g., thermal cameras, advanced LiDAR units). Key competitive advantages at this stage include proprietary algorithm development for flight stability and energy efficiency, and access to secure, reliable supply chains for critical microprocessors and materials. The quality and performance of these upstream components directly determine the reliability, endurance, and operational ceiling of the final drone platform, making component standardization and modularity crucial for mass production and maintenance efficiency.

Midstream activities involve the assembly of the components into final UAV platforms, focusing on industrial design, system integration, and software development, particularly for Ground Control Stations (GCS) and mission planning software. Manufacturers often operate dual distribution channels: direct sales to large enterprise clients seeking highly customized fleet solutions and indirect sales through a global network of authorized distributors, resellers, and system integrators who provide local support, training, and value-added services. The complexity of regulatory compliance and the need for localized technical support often necessitate the use of regional integrators who can tailor solutions to meet specific national airspace requirements and customer application needs, particularly in regions with nascent drone ecosystems.

Downstream activities center on service delivery, which is the fastest-growing and highest-margin segment of the value chain. This involves data acquisition services, post-processing analytics, data management, and specialized consulting. For enterprise customers, the value is not in the drone itself but in the actionable insights derived from the data. Therefore, the downstream segment includes AI and machine learning providers who transform raw aerial images and point clouds into maintenance reports, volumetric measurements, and digitized assets. Direct distribution is crucial for managing proprietary software updates and specialized technical support for sophisticated enterprise fleets, while indirect channels handle lower-cost consumer and prosumer models efficiently through e-commerce and retail partnerships.

Potential customers for professional civilian drones represent a broad spectrum of industries united by the need for enhanced aerial data collection, operational efficiency, and safety. End-users fall primarily into sectors characterized by large, distributed assets requiring frequent monitoring or complex spatial analysis, where traditional methods are cost-prohibitive or dangerous. This includes major utility companies operating power lines, pipelines, and vast renewable energy farms (wind and solar), which require precise, automated inspection for preventative maintenance and rapid fault identification. Additionally, large infrastructure owners, such as national transportation departments responsible for bridges, roads, and rail networks, constitute a high-value customer base, prioritizing drones for detailed structural integrity checks and construction progress monitoring.

The agricultural sector, particularly large-scale industrial farming and agribusinesses, is a significant adopter, utilizing drones for precision farming applications such as crop scouting, variable rate application of fertilizers and pesticides, and yield prediction. These buyers seek solutions that integrate seamlessly with existing farm management software and provide multispectral analysis for immediate vegetative health assessment. Government agencies—including municipal planning bodies, emergency services (police, fire, search and rescue), and environmental protection organizations—represent another critical segment. Their purchasing decisions are often driven by mandates for public safety enhancement, disaster response speed, and accurate geospatial data for regulatory mapping and enforcement activities.

Furthermore, specialized segments such as mining and quarrying operations require drones for volumetric surveying, stockpile measurement, and pit wall stability monitoring, providing highly accurate and repeatable data essential for financial auditing and safety compliance. The emerging logistics and e-commerce industry, which includes major retailers and dedicated delivery services, represents the future mass market for heavy-lift and medium-lift drones, provided regulatory barriers surrounding large-scale urban air logistics can be overcome. These customers prioritize reliability, payload capacity, and sophisticated fleet management capabilities to integrate aerial transport into their established supply chain networks, focusing on last-mile delivery efficiency.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 15.8 Billion |

| Market Forecast in 2033 | USD 40.5 Billion |

| Growth Rate | 14.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DJI, Parrot SA, Yuneec International, Skydio, Draganfly, Zipline, Matternet, EHANG, Insitu (Boeing), AeroVironment, senseFly (AgEagle), Autel Robotics, Delair, Garuda Aerospace, Ascent Aerosystems, Volocopter, Wing (Alphabet Inc.), PrecisionHawk, Quantum-Systems, UAV-Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Civilian Drone Market is characterized by a rapid fusion of aerospace engineering, sensor technology, and advanced computing. A fundamental technology is the integration of highly sophisticated Global Navigation Satellite System (GNSS) receivers, which enable precise Real-Time Kinematic (RTK) and Post-Processed Kinematic (PPK) correction methods. This integration is crucial for achieving centimeter-level accuracy essential for complex surveying, 3D modeling, and inspection tasks, ensuring that the collected data meets rigorous engineering standards. Furthermore, the development of robust, miniaturized flight controllers equipped with advanced Inertial Measurement Units (IMUs) and redundancy systems is increasing the safety and reliability of professional operations, making drones viable for missions over sensitive or populated areas where system failure is unacceptable.

A second pivotal technology area is sensor and payload innovation. There is increasing market demand for multi-sensor integration capabilities, where drones carry complementary sensors like high-resolution visible-light cameras alongside thermal (IR) sensors, LiDAR scanners, or multispectral/hyperspectral cameras simultaneously. LiDAR technology, in particular, has become indispensable for generating accurate Digital Elevation Models (DEMs) and dense point clouds, especially in vegetated or complex terrain where traditional photogrammetry struggles. The continual refinement of these sensors, achieving higher spatial resolution and faster data capture rates while minimizing payload weight, is a primary competitive frontier among manufacturers, directly impacting the quality and scope of data services offered.

The third critical area is related to connectivity and data management, specifically the adoption of secure, high-bandwidth communication links. The integration of 4G LTE and emerging 5G connectivity is vital for maintaining reliable Command and Control (C2) beyond visual line of sight (BVLOS), minimizing reliance on short-range radio frequency communication, and enabling real-time transmission of high-volume data back to cloud-based processing platforms. Furthermore, the development of advanced battery chemistries and fuel cell technology is essential for addressing the persistent limitation of flight endurance. Companies are heavily investing in hydrogen fuel cells and high-density solid-state batteries to achieve multi-hour flight times necessary for long-corridor inspections and extended logistics missions, thereby significantly improving the economic feasibility of large-scale drone operations.

The primary driver is the widespread acceptance of drone technology for industrial inspection and mapping, offering significant cost savings, higher data accuracy (especially with integrated LiDAR and RTK/PPK systems), and substantial enhancement of worker safety compared to traditional manual methods or manned aviation.

Regulatory harmonization, particularly the standardization of rules for Beyond Visual Line of Sight (BVLOS) operations and the creation of standardized certification pathways by bodies like the FAA and EASA, is crucial. These reforms allow scalable operations (like long-distance delivery and linear infrastructure inspection), unlocking higher value commercial use cases.

The professional service delivery segment, including data processing, software platforms (Drone-as-a-Service), and advanced analytics powered by Artificial Intelligence, is projected to achieve the highest CAGR, reflecting the shift in enterprise value from hardware ownership to actionable data insights.

Key technological challenges include improving battery energy density for significantly longer flight endurance, ensuring robust and secure communication links for large-scale autonomous fleet management, and perfecting AI-driven sense-and-avoid capabilities necessary for routine urban airspace integration.

North America currently leads in overall market revenue and advanced technological innovation, particularly in autonomous flight (AI integration). However, the Asia Pacific region, specifically China, dominates manufacturing volume and is projected to exhibit the fastest revenue growth rate due to rapid infrastructure development and large-scale industrial adoption.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.