ID : MRU_ 435202 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

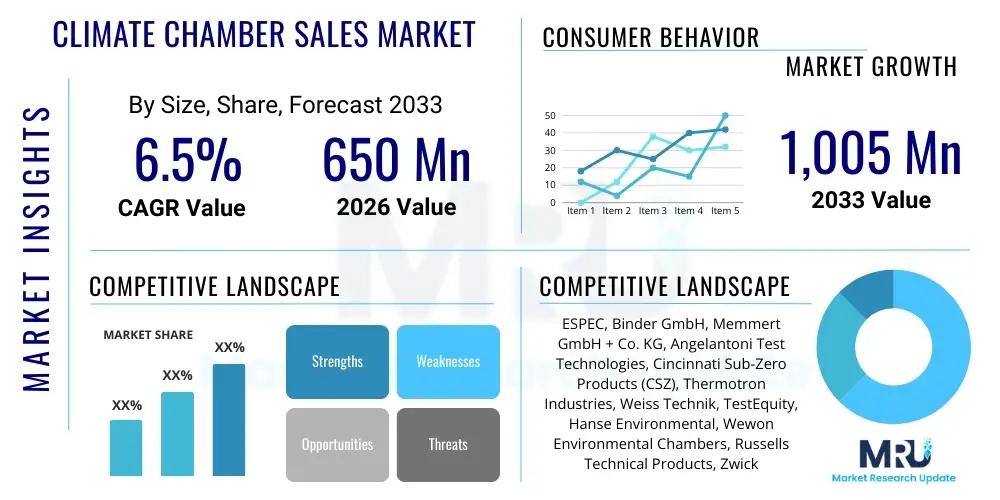

The Climate Chamber Sales Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 650 Million in 2026 and is projected to reach USD 1,005 Million by the end of the forecast period in 2033.

Climate chambers, also known as environmental chambers or climatic test chambers, are essential laboratory and industrial equipment designed to simulate specific environmental conditions such as extreme temperature ranges, humidity levels, and pressure. These chambers are critical for testing the reliability, stability, and durability of materials, components, and finished products across diverse industries before they are released to the consumer market or integrated into complex systems. The demand for increasingly rigorous testing standards, driven by global regulatory mandates and the complexity of modern technology, solidifies the climate chamber market's foundational growth trajectory.

The primary applications of these chambers span sectors including automotive, aerospace, electronics, pharmaceuticals, and material science research. In the automotive industry, for example, chambers are used to test battery performance and electronic control units (ECUs) under conditions mimicking harsh road environments. For electronics manufacturers, climate testing ensures device functionality and longevity, especially for components used in 5G infrastructure or ruggedized industrial equipment. The key benefit derived from using climate chambers is the ability to accelerate product failure analysis and optimize design iterations, drastically reducing time-to-market while simultaneously enhancing product quality and safety.

Market expansion is fundamentally driven by the accelerating pace of technological innovation, particularly in the electric vehicle (EV) battery sector and advanced semiconductor manufacturing. The mandatory quality control protocols established by international standards organizations (like ISO and IEC) necessitate precise environmental testing equipment. Furthermore, increasing global investment in pharmaceutical research and development, especially for drug stability testing required by regulatory bodies such as the FDA and EMA, acts as a significant catalyst propelling the sales of high-precision humidity and temperature chambers globally.

The Climate Chamber Sales Market is characterized by intense technological competition focused on energy efficiency, precision control, and integration capabilities, representing a major business trend. Manufacturers are increasingly developing modular and customizable systems that can handle both standard climatic testing and specialized stress screening tests (such as Highly Accelerated Life Testing – HALT), allowing end-users flexibility and cost efficiency. The shift towards sustainable manufacturing practices is also driving demand for chambers that utilize natural refrigerants (like CO2) and optimize power consumption, influencing procurement decisions across industrialized economies.

Regionally, the Asia Pacific (APAC) area dominates market growth, primarily fueled by the rapid expansion of its automotive production, particularly electric vehicle manufacturing hubs in China and South Korea, and the robust presence of semiconductor fabrication plants. North America and Europe maintain a strong position, driven by stringent regulatory frameworks in aerospace and pharmaceuticals, necessitating advanced, high-accuracy chambers for sophisticated research and quality assurance. Segment-wise, the Floor Standing type chambers capture the largest revenue share due to their capacity for testing large components (like automotive batteries or solar panels), while the Pharmaceutical and Biotechnology application segment is projected to exhibit the highest CAGR, spurred by global investment in life sciences R&D and drug stability analysis requirements.

The market faces inherent challenges related to the high initial capital expenditure required for purchasing and maintaining these sophisticated machines, alongside the technical complexities involved in integrating them into complex testing workflows. However, the opportunity landscape is vast, centered around the development of chambers capable of simulating ultra-low temperatures essential for space component testing and the incorporation of advanced remote monitoring systems facilitated by IoT technologies. Successful market penetration relies on strategic partnerships between chamber manufacturers and specialized testing laboratories, focusing on delivering integrated, turnkey testing solutions.

Common user questions regarding AI’s influence typically revolve around how artificial intelligence can enhance the efficiency, predictive maintenance, and data analysis capabilities of climate chambers. Users frequently inquire about AI's role in optimizing test cycles, minimizing energy use, and interpreting complex datasets generated during accelerated stress testing (AST). The synthesis of these queries reveals a strong expectation that AI integration will shift climate chambers from passive environmental simulators to active, intelligent testing platforms capable of real-time fault prediction and automated parameter adjustments. The primary themes center on achieving higher testing throughput, reducing human error, and creating digitized, traceable testing records compliant with Industry 4.0 standards, thereby maximizing return on investment for high-cost testing equipment.

The market dynamic is heavily influenced by four primary forces: the rising demand for sophisticated product reliability testing across high-tech sectors (Driver), the substantial initial investment required and complexity of calibration (Restraint), the burgeoning need for highly specialized testing environments (Opportunity), and the intense competitive pressure among major global suppliers (Impact Force). These elements collectively determine strategic investments, pricing strategies, and product development cycles within the industry. The increasing electrification of the automotive sector stands out as the most immediate driver, creating an unprecedented need for battery testing chambers that can simulate extreme temperature cycling under load.

Restraints, such as the high operational costs associated with energy consumption and specialized technical personnel needed for chamber operation and maintenance, pose limitations, particularly for small and medium-sized enterprises (SMEs). Furthermore, the long replacement cycle of high-quality climate chambers means that market growth relies heavily on expansion into new application areas rather than frequent replacements in established labs. Addressing these restraints requires manufacturers to focus on producing energy-efficient models and offering comprehensive maintenance contracts and simplified user interfaces.

Opportunities are largely concentrated in emerging technologies such as hydrogen fuel cells, advanced medical devices, and space exploration components, all requiring bespoke, extreme-condition chambers (e.g., thermal vacuum testing). The push towards Industry 4.0 encourages the development of interconnected, IoT-enabled chambers that integrate seamlessly with laboratory information management systems (LIMS). The key impact forces include intense intellectual property protection and the necessity for global standardization (ISO/IEC certification), which raises entry barriers for new manufacturers and fosters consolidation among established market leaders.

The Climate Chamber Sales Market is meticulously segmented based on the chamber design (Type), the specific purpose of the testing (Application), and the ultimate purchaser or consumer (End-Use Industry). This multi-dimensional segmentation allows for precise market sizing and strategic targeting, reflecting the specialized requirements of different user groups. For instance, pharmaceutical companies require extremely stable humidity control for stability testing, whereas automotive companies prioritize rapid thermal cycling capabilities for component endurance testing. The segmentation structure helps manufacturers tailor product offerings, distribution networks, and marketing messages to specific high-value customer needs.

The segmentation by Type, distinguishing between Benchtop and Floor Standing units, reveals a clear correlation with the size and complexity of the tested articles, impacting average selling prices significantly. Benchtop models cater to small electronics and material samples, emphasizing portability and affordability, while Floor Standing models are designed for large-scale production testing and complex assemblies. Analyzing Application segmentation shows that high-growth areas, particularly pharmaceuticals and electronics, are driving demand for technologically advanced and specialized chambers capable of meeting evolving regulatory requirements and tighter testing tolerances.

The value chain for the Climate Chamber Sales Market begins with upstream analysis, which involves the sourcing of critical raw materials and specialized components. Key upstream suppliers provide high-precision refrigeration compressors (often cascade systems for ultra-low temperatures), advanced humidity sensors, high-grade insulation materials, and sophisticated programmable logic controllers (PLCs) or microprocessors for precise environmental control. Establishing stable relationships with reliable suppliers of these specialized components is crucial, as the quality and accuracy of the final chamber are directly dependent on the performance of these sub-systems. Manufacturers must focus on vertical integration or strong supplier partnerships to mitigate supply chain risks and ensure quality consistency.

The midstream stage encompasses manufacturing, assembly, software integration, and stringent quality control. This is where market differentiators such as energy efficiency, user interface design, and compliance with standards (e.g., CE, UL, ISO 17025) are established. Direct and indirect distribution channels define the downstream analysis. Direct sales channels involve manufacturers selling directly to large enterprises or government labs, allowing for customized specifications and installation services. Indirect channels, involving authorized distributors, channel partners, and regional representatives, are vital for reaching smaller R&D labs and international markets, requiring robust training and technical support infrastructure.

The final element of the value chain involves after-sales service, including installation, calibration, preventive maintenance, and technical support. Given the complexity and high cost of these chambers, comprehensive service agreements represent a significant revenue stream and a critical factor in customer retention. The effectiveness of the service network directly influences brand reputation and customer satisfaction. The efficiency of the distribution channel—whether direct (offering bespoke solutions) or indirect (offering scale and rapid deployment)—is paramount for market share acquisition and sustaining competitive advantage.

Potential customers for climate chambers are predominantly sophisticated technical organizations requiring stringent validation of product performance under controlled environmental conditions. The primary end-users fall into three major categories: industrial manufacturing companies (especially those in mobility and electronics), specialized testing service providers, and governmental/academic research institutions. These buyers prioritize high-reliability, traceability, and adherence to specific international testing standards. Purchasing decisions are typically centralized, involving quality assurance teams, R&D engineers, and procurement specialists, with longevity and precision being more important than upfront cost.

In the industrial segment, the rapid development cycles of Electric Vehicles (EVs) have positioned battery manufacturers and Tier 1 suppliers as highly valuable customers. They require large-scale, explosion-proof, and highly specialized chambers for thermal runaway testing and performance cycling. Similarly, semiconductor and consumer electronics companies rely on climate chambers to ensure the reliability of components operating in extreme field conditions, driving demand for benchtop and smaller, faster thermal cycling chambers for efficient failure analysis during the design phase.

Contract testing laboratories (CTLs) represent another robust customer base, as they offer testing services to companies lacking internal capacity or specific accreditations. CTLs require versatile, high-throughput chambers that can accommodate various customer specifications and maintain ISO/IEC 17025 accreditation. Academic and research institutions purchase these chambers primarily for fundamental material science studies, climate impact research, and educational purposes, often focusing on flexibility and ease of programming for diverse experimental setups.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 650 Million |

| Market Forecast in 2033 | USD 1,005 Million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ESPEC, Binder GmbH, Memmert GmbH + Co. KG, Angelantoni Test Technologies, Cincinnati Sub-Zero Products (CSZ), Thermotron Industries, Weiss Technik, TestEquity, Hanse Environmental, Wewon Environmental Chambers, Russells Technical Products, ZwickRoell, Presto Group, Vötsch Industrietechnik, Tabai Espec, Tenney Environmental, Darwin Chambers Company, Equilam, FDM - Friuli Display & Measurement, Parameter Generation & Control. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution within the climate chamber market is primarily centered on enhancing precision, optimizing energy usage, and improving connectivity. A core technological trend involves the transition from traditional mechanical refrigeration systems to advanced cascade refrigeration systems utilizing environmentally friendly, low Global Warming Potential (GWP) refrigerants, such as R-452A and increasingly natural refrigerants like CO2 (R-744). These advanced systems are essential for achieving the rapid temperature transition rates required for thermal shock testing, maintaining high stability across wide temperature ranges, and reducing the ecological footprint of the testing infrastructure, aligning with global sustainability mandates.

Connectivity and control software represent another critical technological frontier. Modern climate chambers incorporate sophisticated Programmable Logic Controllers (PLCs) and integrated touch-screen interfaces, allowing for complex, multi-stage test profile creation and storage. Key players are heavily investing in IoT enablement, providing remote monitoring and diagnostics capabilities. This allows engineers to manage chambers globally, receive real-time alerts on parameter deviations, and access detailed data logging compliant with regulatory requirements (like FDA 21 CFR Part 11 for pharmaceuticals). Data security and seamless integration with existing laboratory management systems (LIMS) are paramount technological requirements for high-end users.

Furthermore, specialized chamber design technologies are gaining prominence, including dynamic moisture control systems that achieve precise humidity levels quickly and high-efficiency vacuum pumps necessary for altitude and space simulation chambers used in aerospace testing. For automotive applications, safety technology, such as active ventilation and inert gas purging systems designed to mitigate risks during lithium-ion battery testing, represents a rapidly evolving and critical area of technological innovation. The focus remains on developing chambers that offer superior thermal uniformity and reduced recovery time after specimen introduction, maximizing test accuracy and efficiency.

The primary driver is the necessity for stringent product reliability and qualification testing across high-tech sectors, particularly driven by rapid technological advancements in electric vehicle (EV) battery systems, 5G electronics, and the need to comply with evolving international testing standards like ISO and IEC.

IoT integration transforms climate chambers by enabling remote monitoring, real-time diagnostics, and predictive maintenance scheduling. This functionality significantly reduces system downtime, optimizes resource allocation, and ensures the continuous accuracy and compliance of testing environments, enhancing overall operational efficiency.

The Pharmaceutical and Biotechnology application segment is projected to experience the highest CAGR. This growth is fueled by increasing global investment in drug stability testing, mandatory compliance with regulatory guidelines (FDA, EMA) for storage condition validation, and the expansion of biological research.

APAC prioritizes volume sales driven by electronics and EV production, favoring efficient, high-throughput chambers. North America and Europe focus on high-precision, specialized chambers for aerospace and defense, alongside strong demand for sustainable systems using low-GWP refrigerants.

The market is shifting towards environmentally sustainable refrigeration solutions, including the adoption of low Global Warming Potential (GWP) refrigerants like R-452A and natural refrigerants such as CO2 (R-744), replacing older hydrofluorocarbons (HFCs) to meet stringent environmental regulations and reduce the operational ecological footprint.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.