ID : MRU_ 438991 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

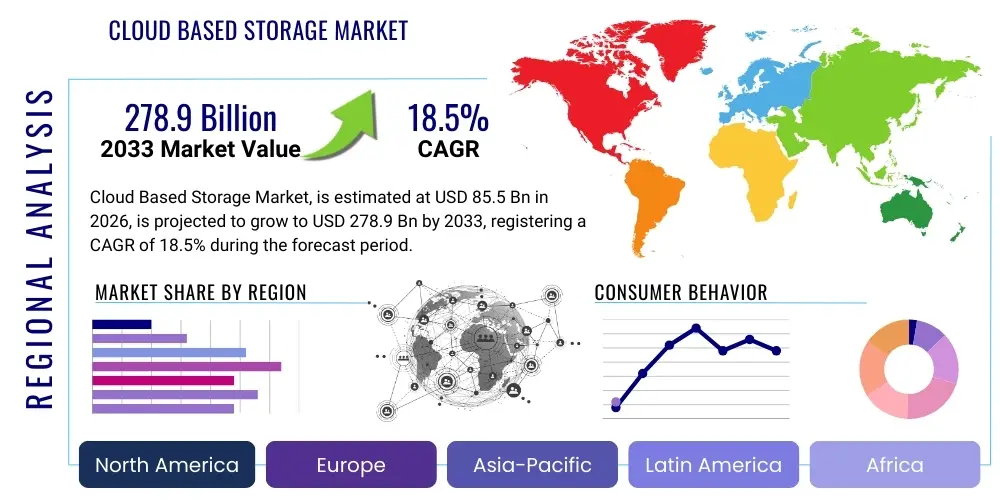

The Cloud Based Storage Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at $85.5 Billion USD in 2026 and is projected to reach $278.9 Billion USD by the end of the forecast period in 2033.

The Cloud Based Storage Market encompasses services that enable users and applications to store, manage, and access digital data remotely via the internet, utilizing pooled computing resources provided by a third-party service provider. This paradigm shift from traditional on-premise infrastructure offers unprecedented scalability, elasticity, and operational cost savings. Key product descriptions include Infrastructure-as-a-Service (IaaS) storage components like block, file, and object storage, alongside Platform-as-a-Service (PaaS) solutions focused on database and data warehousing. The underlying technology relies heavily on virtualization, advanced networking capabilities, and robust data center architecture to deliver continuous availability and performance.

Major applications of cloud storage span enterprise data backup and recovery, primary data archiving, content delivery networks (CDNs), and large-scale big data analytics platforms. Enterprises across numerous verticals leverage these services to facilitate digital transformation initiatives, ensure business continuity, and support remote work environments. Benefits inherent to cloud storage include significantly reduced capital expenditure (CapEx), enhanced data security through centralized management and encryption protocols, and rapid deployment capabilities that accelerate time-to-market for new services. Furthermore, the pay-as-you-go model inherent in most cloud offerings allows organizations to optimize resource consumption based on fluctuating business demands.

Driving factors stimulating market growth include the exponential increase in global data generation, largely fueled by the proliferation of IoT devices, high-resolution media, and social platforms. The accelerating adoption of hybrid and multi-cloud strategies by large enterprises seeking resilience and vendor diversification is further expanding the market scope. Regulatory mandates requiring robust data retention and disaster recovery protocols also compel businesses to transition towards scalable and compliant cloud storage solutions. These technological and operational drivers collectively underscore the essential role cloud storage plays in modern global IT infrastructure.

The Cloud Based Storage Market is currently undergoing a dynamic transformation, characterized by significant business trends focusing on serverless architecture and enhanced data sovereignty tools. Major cloud providers are aggressively investing in regional data center expansion to comply with localized regulatory requirements, intensifying competition based on latency and localized governance. From a component standpoint, the demand is shifting notably towards advanced storage management solutions incorporating AI for automated tiering and cost optimization, moving beyond basic infrastructure provision. This strategic business evolution is focused on delivering highly specialized services tailored to specific vertical workloads, particularly in areas requiring high performance computing (HPC) and massive scalability, such as life sciences and financial modeling.

Regional trends indicate North America maintaining market dominance due to early adoption, the presence of major hyperscale vendors, and robust digital infrastructure. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth rate, driven by rapid digitalization across emerging economies, large-scale government cloud adoption initiatives, and the massive data consumption generated by its rapidly expanding internet user base. Europe is focused on regulatory compliance, with GDPR requirements driving investment in regional data residency and advanced encryption solutions, favoring private and hybrid deployment models that offer greater control over sensitive data assets. The Middle East and Africa (MEA) and Latin America are poised for accelerated growth as local enterprises increasingly bypass legacy infrastructure directly in favor of cloud solutions.

Segment trends reveal a sustained dominance of Object Storage due to its suitability for unstructured data, archival purposes, and massive data lakes essential for big data analytics and machine learning applications. Hybrid Cloud deployments are gaining significant traction, particularly among large enterprises seeking to balance security, performance, and cost by retaining mission-critical workloads on-premise while leveraging public cloud scalability for variable workloads. In terms of verticals, the IT and Telecommunications sector remains the largest consumer, but the Healthcare and BFSI sectors are showing the most rapid growth, spurred by regulatory pressures to securely manage vast volumes of sensitive customer and clinical data, driving demand for compliant, scalable storage architectures.

Common user inquiries concerning the intersection of AI and cloud storage primarily revolve around scalability challenges posed by AI-generated data, the necessity for high-performance storage systems to feed machine learning (ML) models, and the role of AI in automating storage management. Users are particularly keen on understanding how cloud providers are integrating AI tools for intelligent data tiering, predictive capacity planning, and automated security incident response. The consensus theme is that AI acts as both a massive consumer and an essential manager of cloud storage. The generation of huge datasets required to train foundational models necessitates massive, highly performant object and file storage, while conversely, AI and ML algorithms are increasingly being used within the storage infrastructure itself to optimize performance, enhance data protection, and significantly reduce operational overhead for cloud customers.

The dynamics of the Cloud Based Storage Market are shaped by a complex interplay of internal and external forces driving adoption and imposing constraints, alongside compelling future opportunities. The primary driver is the pervasive digital transformation across all industry verticals, compelling organizations to migrate monolithic legacy systems to agile, scalable cloud environments. Simultaneously, the restraints revolve heavily around persistent data security concerns, particularly regarding compliance across diverse jurisdictions and the risk of vendor lock-in, where exiting a major cloud provider becomes economically or technically prohibitive. Opportunities are predominantly found in emerging technologies such as edge computing, which requires localized cloud storage capabilities, and the development of serverless storage solutions that abstract away infrastructure management entirely, offering highly granular operational efficiency.

The impact forces further define the market trajectory, driven significantly by the increasing data gravity—the tendency for data to attract applications and services toward it—which solidifies the position of hyperscale cloud providers. Regulatory mandates, particularly those related to data residency and sovereignty (like GDPR in Europe or specific localization laws in Asia), act as both a restraint and an opportunity, forcing providers to localize services but simultaneously creating new, specialized market segments. The bargaining power of customers is moderate, as while there are many small providers, the dominant position of the top three cloud vendors limits genuine price competition for premium services. However, the threat of substitutes is low, as traditional on-premise storage cannot match the agility and cost structure of cloud services in the long term, cementing the cloud’s strategic advantage.

The competitive landscape is characterized by intensive innovation, with providers continuously launching specialized services, high-performance computing (HPC) options, and integrated data governance platforms to gain a competitive edge. This competitive environment benefits end-users through continuous price reductions and feature enhancements. Technological shifts, such as the move towards NVMe over Fabrics (NVMe-oF) in cloud data centers, offer significant performance improvements, further driving the replacement cycle of older, slower storage technologies. Therefore, the market growth is underpinned by fundamental technological necessity, moderated by enterprise risk aversion related to control and security, but propelled forward by continuous service innovation and global data proliferation.

The Cloud Based Storage Market segmentation provides a granular view of distinct offerings and consumption patterns, differentiating the market based on deployment model, component type, fundamental storage architecture, organizational size, and end-use vertical. Understanding these segments is crucial for strategic planning as they reflect varied customer needs ranging from cost efficiency for small businesses to high-performance compliance for regulated industries. The market is increasingly defined by the complexity of services offered, moving beyond simple raw capacity provision to integrated data management, security, and analytics layers that cater to specific operational requirements, such as optimizing database performance or handling petabytes of archive data.

A key segmentation trend highlights the growing maturity of hybrid and multi-cloud environments. Hybrid models allow organizations to seamlessly integrate their existing on-premise data centers with public cloud resources, maintaining control over core assets while leveraging the public cloud for burst capacity or disaster recovery. Simultaneously, the distinction between object, file, and block storage remains critical, with object storage dominating the capacity landscape due to its unstructured data capabilities, while file and block storage cater to traditional server workloads, databases, and containerized applications requiring high throughput and low latency. This differentiated offering strategy allows providers to address the full spectrum of enterprise IT requirements effectively, leading to highly specialized solutions within each market segment.

The value chain of the Cloud Based Storage Market is highly integrated and complex, starting with upstream suppliers and extending through service layers to the final end-user consumption. Upstream analysis focuses on the providers of foundational hardware and core software, including semiconductor manufacturers supplying CPUs and GPUs, solid-state drive (SSD) and hard disk drive (HDD) manufacturers providing raw capacity, and networking equipment vendors. These suppliers are critical as they dictate the base cost, performance, and capacity metrics of the entire cloud infrastructure. Hyperscale vendors engage in massive direct procurement, often designing custom hardware specifications to maximize efficiency and negotiating favorable pricing due to the sheer volume of their acquisitions, thereby exerting considerable power over the component market.

Midstream activities involve the cloud service providers (CSPs) themselves, who integrate the foundational hardware and software into a cohesive, scalable infrastructure, virtualizing resources, and developing proprietary management tools and APIs. This phase includes the deployment of global data centers, establishment of interconnected networks, and continuous security infrastructure development. The distribution channel is predominantly direct, especially for the three largest hyperscalers (Amazon Web Services, Microsoft Azure, Google Cloud Platform), who sell their storage services directly through online consoles, self-service platforms, and dedicated sales teams. However, indirect channels, including strategic partnerships with systems integrators, managed service providers (MSPs), and specialized value-added resellers (VARs), are crucial for reaching SMEs and facilitating complex enterprise migration projects requiring specialized expertise and localized support.

Downstream analysis focuses on the end-users and the consumption patterns of the various storage services. This stage involves the utilization of managed services for tasks like backup, disaster recovery, and archiving, often complemented by third-party data management software that sits atop the cloud infrastructure. The efficiency of the value chain is increasingly determined by software-defined networking and storage capabilities that automate provisioning and scaling, linking the raw capacity efficiently to application demands. The overall power dynamic is centralized with the large CSPs, who control both the infrastructure and the primary distribution channels, placing the onus on technology integration and superior service delivery to capture and retain customers.

The potential customers for the Cloud Based Storage Market are broadly segmented into two primary categories: Small and Medium Enterprises (SMEs) and Large Enterprises, spanning nearly every sector of the global economy. SMEs represent a vast pool of potential buyers driven primarily by the need for cost-effective, easily deployable storage solutions that eliminate the need for significant initial capital investment in IT infrastructure. Their buying criteria emphasize simplicity, reliability, and subscription-based pricing models, often favoring public cloud or managed service providers who can handle the complexity of security and maintenance, enabling them to focus resources on core business operations.

Large enterprises, conversely, are typically sophisticated buyers with stringent requirements relating to compliance, performance, integration with legacy systems, and data residency. These organizations, especially those in BFSI, Healthcare, and Government, are the primary consumers of high-performance block storage for transactional systems and massive object storage capacity for data lakes and archives. They often opt for hybrid or multi-cloud strategies to mitigate risks and leverage best-of-breed services from different providers. Their purchase decisions involve long-term contractual agreements and deep integrations, often leveraging professional services for complex migration and security implementations, making them the most lucrative segment in terms of absolute revenue generation.

Specific end-user applications also define key customer clusters. For instance, media and entertainment companies require massive, scalable file and object storage for content creation and distribution (CDNs). Research and development organizations and academic institutions need high-throughput storage for HPC and large-scale simulation data. E-commerce platforms rely heavily on scalable cloud storage for transactional data, customer profiles, and seasonal load balancing. The versatility and scalability of cloud storage mean that virtually any organization generating digital data, regardless of size or industry, is a potential customer, driving the market’s expansive reach and continuous growth across all geographies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $85.5 Billion USD |

| Market Forecast in 2033 | $278.9 Billion USD |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Corporation, Google LLC, IBM Corporation, Dell Technologies, Oracle Corporation, Hewlett Packard Enterprise (HPE), Pure Storage, NetApp, VMware, Rackspace Technology, Alibaba Cloud, Tencent Cloud, Huawei Technologies, Dropbox, Box, Western Digital, Hitachi Vantara, Cisco Systems, Scality. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Cloud Based Storage Market is defined by innovation centered on speed, scalability, and enhanced data control mechanisms. Core to this landscape is the widespread adoption of Software-Defined Storage (SDS) architectures, which decouple storage management functions (like provisioning, replication, and backup) from the underlying hardware. SDS facilitates the agile deployment of storage resources across diverse environments—public, private, and hybrid—providing the flexibility necessary for modern, complex enterprise workloads. Furthermore, the rapid integration of Non-Volatile Memory Express (NVMe) technology, particularly NVMe over Fabrics (NVMe-oF), is dramatically reducing latency for cloud block and file storage services, making cloud performance comparable or superior to high-end dedicated on-premise arrays, which is essential for mission-critical databases and financial trading applications.

Another crucial technological development involves advanced security and encryption techniques. Providers are moving beyond basic data-at-rest encryption to offering sophisticated homomorphic encryption and confidential computing capabilities, allowing data processing to occur while the data remains encrypted, addressing critical concerns in regulated industries like healthcare. Data management features are heavily reliant on highly available, distributed file systems and object storage protocols that ensure durability and redundancy across multiple availability zones. Technologies like erasure coding are replacing traditional RAID systems in hyperscale environments to achieve petabyte-scale data protection with significantly lower storage overhead compared to simple data replication techniques.

Finally, the rise of serverless and containerized environments (Kubernetes) is dictating the need for ephemeral, highly scalable storage solutions accessible via robust APIs. This shift requires specialized storage interfaces (like CSI drivers) that seamlessly integrate persistent storage volumes directly into microservices architectures. Looking forward, the introduction of technologies supporting edge computing, such as localized data caching and micro-data centers, ensures that cloud storage functionality extends to remote locations, supporting low-latency applications like industrial IoT and connected vehicles. These technological advancements collectively reduce total cost of ownership (TCO) while continuously improving performance, reliability, and security compliance for enterprise consumers globally.

Regional dynamics heavily influence the adoption and segmentation of the Cloud Based Storage Market, reflecting varying levels of technological maturity, regulatory environments, and data generation rates. North America maintains the highest market share, fueled by the earliest and broadest adoption of cloud services, the presence of major hyperscale providers (AWS, Microsoft, Google), and high IT expenditure across financial, technology, and media sectors. The region continues to drive innovation in high-performance cloud storage and serverless architectures, with strong demand particularly from Silicon Valley and the financial hubs on the East Coast, focusing on cutting-edge analytics and AI-driven storage optimization.

The Asia Pacific (APAC) region is poised for the most rapid market expansion, driven by massive investments in digital infrastructure, government initiatives promoting cloud adoption (e.g., Digital India, China’s industrial cloud policies), and the sheer volume of data generated by a large and rapidly digitizing population. Key growth markets within APAC include China, India, Japan, and South Korea, where the focus is on scalable public cloud infrastructure and localized data centers to meet regulatory demands. The primary drivers are mobile internet usage, e-commerce growth, and the expansion of the manufacturing sector utilizing IoT for operational efficiency.

Europe represents a highly mature but compliance-sensitive market. Growth here is robust, driven primarily by the need for data sovereignty and adherence to stringent regulations like the GDPR. Consequently, European enterprises exhibit a preference for private and hybrid cloud models, leveraging regional providers and localized infrastructure provided by global players. This emphasis on control and residency drives significant investment into advanced security, governance, and compliant backup solutions. Latin America and the Middle East & Africa (MEA) are emerging markets showing accelerated growth, characterized by enterprises leapfrogging legacy systems directly to cloud solutions, seeking flexibility and reduced CapEx. Growth in MEA is bolstered by government digital transformation agendas (like Saudi Vision 2030) and burgeoning telecommunications sectors requiring scalable infrastructure.

The Cloud Based Storage Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033, driven by increasing data generation and enterprise digital transformation initiatives.

Object storage is ideal for unstructured data (e.g., backups, archives, data lakes) and offers high scalability. File storage is used for shared folders and applications requiring a hierarchical structure. Block storage is primarily used for high-performance applications like databases and virtual machines, demanding low latency access.

AI significantly impacts cloud storage by requiring massive, scalable storage capacity (data lakes) for model training, demanding ultra-high-performance (low-latency block/file storage) to feed training pipelines, and by providing advanced AI-driven tools to automate storage management, tiering, and optimization.

Highly regulated industries often favor Hybrid Cloud and Private Cloud deployment models. These models provide the scalability benefits of the cloud while allowing organizations to maintain stringent control over sensitive data residency, security, and specific compliance mandates.

The major restraints include persistent concerns regarding data security breaches and compliance across multiple international jurisdictions, as well as the significant risk and complexity associated with vendor lock-in when committing large data volumes to a single hyperscale provider.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.