ID : MRU_ 431614 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

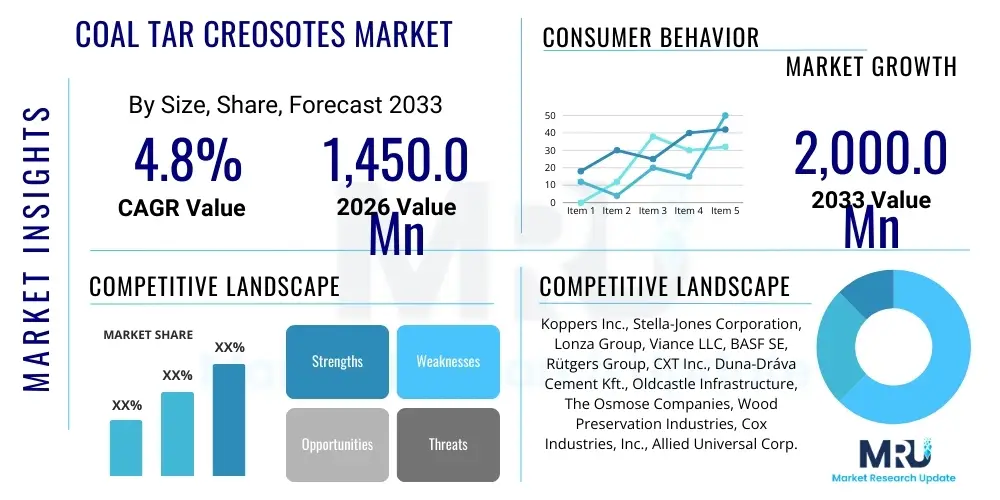

The Coal Tar Creosotes Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at $1,450.0 Million in 2026 and is projected to reach $2,000.0 Million by the end of the forecast period in 2033.

Coal tar creosote, an oil derived from the high-temperature treatment of coal tar, is fundamentally a mixture of numerous compounds, primarily polycyclic aromatic hydrocarbons (PAHs). Its primary utility lies in its exceptional properties as a wood preservative, offering robust protection against fungal decay, wood-boring insects, and marine organisms. The product’s deep penetration capabilities and long residual lifespan make it highly valued in infrastructure applications where durability and resistance to harsh environmental conditions are paramount. Historically, creosote has been the preferred treatment for demanding applications such as railroad ties, utility poles, and marine pilings due to its proven efficacy over decades, establishing a critical niche within the chemical and construction sectors.

The major applications driving the market demand include the rail transportation sector, where creosote-treated wood maintains the structural integrity and longevity of railway sleepers under heavy loads and continuous exposure to moisture. Additionally, the telecommunications and power transmission industries rely heavily on creosote-treated utility poles to ensure long service life and minimize replacement costs in widely dispersed geographical areas. The inherent benefits of coal tar creosote, such as its cost-effectiveness compared to alternative materials like concrete or steel, combined with its established performance track record in aggressive environments, continue to underpin market stability, particularly in developed economies with extensive existing infrastructure requiring maintenance or replacement.

Driving factors for the Coal Tar Creosotes market include the ongoing expansion and modernization of global railway networks, particularly in emerging economies, alongside steady demand for replacement infrastructure components in North America and Europe. Furthermore, the longevity provided by creosote treatment—often exceeding 30 to 50 years—offers significant economic benefits by reducing lifecycle maintenance costs for utility and transportation companies. Despite regulatory pressures related to environmental and health concerns surrounding PAHs, the lack of a universally equivalent, cost-effective substitute with the same level of proven durability in heavy-duty applications ensures sustained, albeit modulated, market demand.

The Coal Tar Creosotes Market is characterized by moderate growth, heavily influenced by cyclical infrastructure spending and stringent environmental regulations, particularly concerning product registration and application standards in major consumer markets like the European Union. Business trends indicate a strategic consolidation among major producers, focusing on optimizing distillation processes to meet evolving regulatory requirements regarding PAH concentration and ensuring compliance across various jurisdictions. The dominance of the rail sector and the utility sector as primary demand centers dictates the overall market trajectory, with demand remaining highly inelastic due to the product's unique performance attributes, especially in situations demanding extreme longevity and resilience against biological degradation.

Regionally, North America maintains the largest market share, driven by extensive existing railway infrastructure and utility pole networks requiring continuous replacement and maintenance. Asia Pacific is emerging as the fastest-growing region, fueled by rapid urbanization and massive investments in new transportation and energy infrastructure, though regulatory adoption in this region is more varied. Segment trends show that the Railroad Ties application segment commands the majority of the market volume, emphasizing the dependency of the market on governmental and private railway expenditures. While alternative wood preservatives are gaining traction in less demanding applications, creosote maintains its stronghold where service life extension and robust protection are non-negotiable performance criteria.

The market faces a pivotal dynamic balancing robust efficacy against high regulatory scrutiny. Key strategies for market participants involve investing in improved application techniques, ensuring worker safety, and engaging in proactive dialogue with regulatory bodies to secure continued authorization for critical infrastructure uses. Innovations in preservation processes, such as the blending of creosote with supplementary preservatives to enhance penetration or reduce leaching, are also observable trends aimed at improving the environmental profile of treated products while retaining performance integrity. Overall, the market remains stable but constrained by the necessary adherence to complex chemical handling and usage guidelines.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Coal Tar Creosotes Market often center on its potential to optimize supply chains, predict infrastructure failure rates, and potentially accelerate the development of greener alternatives. Key themes revolve around leveraging machine learning for predictive maintenance scheduling, allowing railway and utility operators to precisely identify creosote-treated assets nearing the end of their service life, thus streamlining replacement cycles and maximizing the lifespan of treated wood. Users are also concerned about whether AI-driven materials science research could rapidly uncover viable, large-scale substitutes that bypass the regulatory challenges associated with PAHs, fundamentally altering the competitive landscape for creosote producers and applicators. The primary expectation is that AI will enhance operational efficiency in end-use industries rather than directly transforming the chemical production process of creosote itself.

The market dynamics for coal tar creosotes are fundamentally shaped by a rigorous interplay between the infrastructural requirement for highly durable materials and intense regulatory scrutiny concerning polycyclic aromatic hydrocarbons (PAHs). Drivers predominantly stem from the expansive and essential nature of global railway and utility networks, where the cost-benefit analysis overwhelmingly favors the long-term protection offered by creosote, especially in areas subjected to high moisture or biological hazard. However, restraints are significant, primarily dictated by evolving environmental regulations, especially in Europe and North America, leading to usage restrictions and escalating compliance costs. Opportunities reside in developing new formulations that minimize leaching and comply with stricter environmental standards, focusing on niche, non-substitutable applications like marine environments. The impact forces show a strong push from sustainable alternatives and a pull from necessary infrastructure renewal.

The primary driver remains the indispensable demand for long-lasting, heavy-duty wood preservation solutions in the transportation sector. Railway operators prioritize safety and longevity, making creosote the benchmark standard for sleepers where alternative treatments have yet to demonstrate comparable performance under severe mechanical stress and weather variability. Additionally, the rising cost of concrete and steel substitutes makes creosote-treated wood an economically viable choice for large-scale infrastructure projects. This economic advantage, coupled with the established history of performance, acts as a powerful stabilizing force against market fluctuations, particularly in government-backed infrastructure development programs.

Conversely, the most substantial restraint is the classification of creosote as a restricted substance due to the presence of carcinogenic PAHs, necessitating specialized handling, treatment, and disposal protocols. This leads to higher operational complexities and limits its use in consumer-facing or less demanding agricultural applications. The pervasive search for sustainable and green building materials also presents a long-term threat, pushing researchers toward less toxic alternatives, which, if commercialized effectively, could slowly erode creosote's market share in non-critical applications. Successfully navigating these restraints requires significant investment in product stewardship and regulatory affairs.

The Coal Tar Creosotes market is segmented primarily based on the application method and the end-use industry, reflecting the specialized nature of its deployment in infrastructure maintenance and construction. Application segmentation reveals a significant concentration of market volume within the railroad and utility pole sectors, which demand pressurized treatments for deep penetration and maximal longevity. End-use segmentation highlights the transportation and telecommunication sectors as the dominant consumers, demonstrating a high dependency on creosote's efficacy for ensuring critical national infrastructure resilience. Understanding these segments is crucial for manufacturers to align production capacities with regional infrastructural spending cycles and regulatory environments.

The value chain for the Coal Tar Creosotes market begins upstream with the coking industry and steel production, as crude coal tar, the raw material, is a byproduct of coal carbonization. Primary producers of creosote distill crude coal tar to extract the desired fraction, ensuring the product meets specific technical and regulatory standards. The midstream involves the treatment facilities, which are specialized wood preservation plants equipped with pressurized cylinders necessary for infusing the creosote deeply into the wood matrix. Distribution channels are typically direct or highly specialized, moving the finished treated wood products from the treating facilities directly to large institutional buyers such as railroad companies, electric utilities, and governmental infrastructure agencies, bypassing traditional retail channels due to the nature of the product and associated handling requirements.

Upstream analysis highlights the dependence of the creosote market on the overall activity and output of the steel industry. Fluctuations in steel production directly affect the availability and pricing of crude coal tar, creating a fundamental supply-side constraint. Furthermore, the regulatory environment for coking operations impacts the quality and consistency of the feedstock. Downstream, the key value drivers are the performance specifications mandated by end-users, requiring suppliers to maintain rigorous quality control over the preservation process, including penetration depth and retention rates, which are critical for long-term infrastructure guarantees. The longevity provided by the treatment significantly adds value in the downstream market.

The distribution channel is predominantly characterized by direct sales contracts between wood treaters and major infrastructure companies. Indirect distribution is minimal, typically reserved for specialized resellers serving smaller civil engineering or marine projects. The complexity and bulk of the treated materials, coupled with regulatory requirements, necessitate a tightly controlled, business-to-business (B2B) supply structure. Efficiency in logistics and proximity to major rail lines or ports are critical components of the value chain, minimizing transportation costs for the heavy, treated timbers and ensuring timely delivery for extensive infrastructure maintenance projects.

The primary customers for coal tar creosotes are large-scale industrial and governmental entities involved in maintaining or expanding critical infrastructure. These entities demand products with proven longevity, high resistance to biological degradation, and structural integrity under demanding operational conditions. The dominant buyer segments include national and regional railway operators, both freight and passenger, who require vast quantities of highly durable railroad ties for new construction and replacement programs. Additionally, electricity generation and transmission companies, along with telecommunication providers, are major buyers for utility poles, prioritizing low lifecycle costs and reliability in remote or harsh environments.

A significant, though smaller, segment of the market consists of marine construction firms and port authorities. These customers require creosote-treated pilings and timbers for docks, jetties, and bulkheads, where the preservative’s efficacy against destructive marine borers is unparalleled by most alternative treatments. The procurement process for these potential customers is highly structured, often involving multi-year contracts, rigorous technical specifications, and compliance checks related to environmental and safety standards. The decision criteria are heavily weighted towards performance track record and total cost of ownership rather than initial material cost, reflecting the high costs associated with premature infrastructure failure and replacement.

Secondary potential customers include specialized civil engineering firms contracted for large infrastructure projects and governmental departments managing public works, such as flood defense systems or bridge construction where wood components require maximum protection. Although regulatory restrictions limit consumer-level or residential use in many jurisdictions, the industrial and commercial segments remain robust. Market penetration success relies heavily on demonstrating compliance with evolving health and safety regulations, alongside providing extensive warranties that underscore the product's long service life.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1,450.0 Million |

| Market Forecast in 2033 | $2,000.0 Million |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Koppers Inc., Stella-Jones Corporation, Lonza Group, Viance LLC, BASF SE, Rütgers Group, CXT Inc., Duna-Dráva Cement Kft., Oldcastle Infrastructure, The Osmose Companies, Wood Preservation Industries, Cox Industries, Inc., Allied Universal Corp., PPG Industries, Crown Renewable Energy, Arch Wood Protection, ISK Biocides, Remedial Preservation Services, Timber Preservers, Inc., Eastern Greenbrier Railcar. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Coal Tar Creosotes market is primarily centered on the efficiency and environmental compliance of the preservation process, rather than the core chemistry of creosote itself. The predominant technology remains the full-cell (Rueping and Bethell) pressure treatment processes, which ensure maximum penetration and retention of the preservative deep into the wood cellular structure. Advanced treatment facilities utilize sophisticated computer-controlled vacuum and pressure cycles to optimize creosote absorption based on wood species, density, and intended application. These pressurized methods are critical for achieving the 30-to-50-year service life expected in railway and utility infrastructure, distinguishing the treated product from superficially coated materials.

Recent technological advancements focus heavily on environmental stewardship and improving worker safety during the treatment phase. This includes implementing closed-loop systems to minimize volatile organic compound (VOC) emissions and control creosote runoff, ensuring compliance with strict occupational health and environmental standards. Furthermore, there is growing research into applying barrier technologies or co-preservatives. For instance, technologies that combine creosote with copper compounds or oil-borne preservatives aim to create synergistic effects, potentially reducing the required creosote loading while maintaining or enhancing protection against specific hazards, thereby addressing environmental concerns related to PAH leaching.

Another area of technological importance involves non-destructive testing (NDT) methods, such as sonic or resistance micro-drilling, used by end-users to assess the remaining service life and penetration depth of the creosote in existing assets like utility poles or railroad ties. These technologies are crucial for predictive maintenance, allowing infrastructure owners to justify the continued use of creosote-treated wood by demonstrating its ongoing structural integrity. The use of advanced sensors and data analytics in treating plants also falls under this landscape, facilitating tighter process control and mandatory record-keeping necessary for meeting increasingly complex certification and regulatory reporting requirements globally.

The demand for coal tar creosotes is predominantly driven by critical infrastructure sectors, specifically the treatment of railroad ties (sleepers) and utility poles. Creosote’s unparalleled durability and resistance to harsh environmental conditions, including fungal decay and insect damage, make it essential for ensuring the long service life of these vital assets.

Environmental regulations significantly restrain market growth, particularly in Europe. Regulations like REACH restrict creosote use to professional, industrial applications where no suitable alternatives exist, increasing compliance costs and requiring specialized handling protocols to mitigate risks associated with polycyclic aromatic hydrocarbons (PAHs).

North America currently holds the largest market share, fueled by its extensive, established rail network and utility infrastructure. High maintenance and replacement cycles within these sectors necessitate the continued use of highly durable preservatives like creosote to manage long-term operational costs effectively.

Main alternatives include copper-based preservatives (such as Chromated Copper Arsenate or CCA, increasingly restricted, and Ammoniacal Copper Quaternary or ACQ), and oil-borne preservatives (like Pentachlorophenol, also restricted). However, few alternatives match creosote’s longevity and performance in severe, heavy-duty applications like marine pilings or high-stress railroad environments.

Technology primarily impacts the process through advanced pressure treatment methods (full-cell processes) and the implementation of environmental controls, such as closed-loop systems, to optimize penetration and reduce emissions. Furthermore, non-destructive testing technologies are used downstream to verify efficacy and determine the remaining lifespan of treated wood assets.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.