ID : MRU_ 437995 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

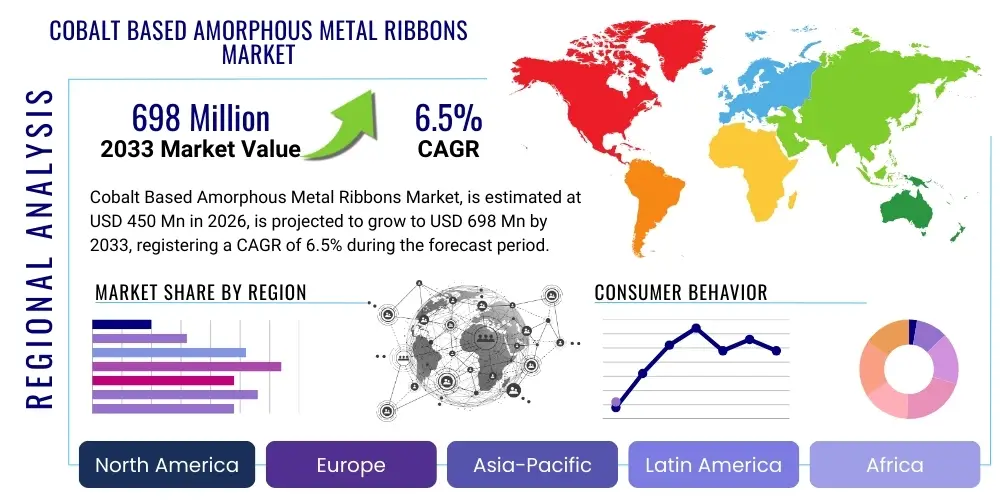

The Cobalt Based Amorphous Metal Ribbons Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 698 Million by the end of the forecast period in 2033. This steady growth trajectory is primarily fueled by the increasing global demand for high-efficiency electronic components, particularly in the automotive and telecommunications sectors where minimizing energy loss and ensuring high-frequency performance are critical design parameters. The inherent superior magnetic properties of cobalt-based amorphous materials, such as extremely low core loss and high magnetic permeability, position them as essential materials in next-generation power electronics and precision magnetic sensors, driving continuous expansion across specialized industrial applications.

Cobalt based amorphous metal ribbons are specialized metallic alloys characterized by a non-crystalline, or glassy, internal structure, distinct from traditional crystalline metals. These ribbons are typically manufactured using ultra-rapid solidification techniques, such as melt spinning, where molten alloy is quenched onto a rapidly rotating drum, cooling at rates exceeding 10^6 Kelvin per second. The resulting structure, free of grain boundaries, defects, and crystalline anisotropy, imparts extraordinary soft magnetic properties. Key alloys often include cobalt, iron, silicon, and boron, with cobalt being dominant when extremely low magnetostriction and high permeability are prioritized, particularly crucial for high-performance applications like Earth leakage circuit breakers (ELCBs), magnetic shielding, and advanced signal processing equipment. The unique combination of material properties makes these ribbons indispensable components in modern efficient electrical infrastructure.

The primary applications for these advanced materials span across critical industries requiring precision and energy efficiency. In the power sector, they are used in high-frequency transformer cores, pulse transformers, and switch-mode power supply (SMPS) devices, significantly reducing energy losses compared to conventional crystalline silicon steel cores. Furthermore, the outstanding sensitivity and low noise characteristics of cobalt amorphous ribbons make them highly desirable in advanced sensing applications, including high-precision current sensors, magnetic field sensors (such as those utilized in navigation systems and non-destructive testing), and anti-theft systems. The continuous miniaturization trend in electronics and the push for higher operating frequencies in telecommunications infrastructure further solidify the market position of these specialized ribbons, demanding stringent material specifications that only amorphous structures can reliably meet.

The driving factors for market growth are intrinsically linked to global mandates for energy conservation and the rapid expansion of electric vehicles (EVs) and renewable energy systems. The benefits derived from using cobalt based amorphous metal ribbons—including significantly reduced eddy current losses, improved thermal stability, and lighter weight components—translate directly into enhanced system performance and reduced operational costs. The transition towards smart grids, increased deployment of wireless charging technologies, and the necessity for sophisticated electromagnetic compatibility (EMC) solutions also contribute substantially to the burgeoning demand, compelling manufacturers to invest in advanced production capabilities and alloy diversification. However, the high cost associated with raw cobalt and the complexity of the manufacturing process remain key challenges that the industry is actively addressing through process optimization and material substitution research.

The Cobalt Based Amorphous Metal Ribbons Market is experiencing robust growth driven by accelerating demand in high-end electronics, renewable energy infrastructure, and the rapidly expanding electric vehicle industry. Business trends indicate a strong focus on strategic mergers and acquisitions among established players to consolidate manufacturing expertise and control intellectual property related to proprietary alloy compositions and melt spinning techniques. Furthermore, there is an observable shift towards vertically integrated business models, where manufacturers are seeking to secure long-term raw material supply, especially cobalt, which faces significant supply chain volatility. Innovation cycles are shortening, driven by the need for ribbons capable of operating efficiently at ultra-high frequencies and elevated temperatures, which is particularly relevant for 5G and advanced power management applications.

Regionally, the Asia Pacific (APAC) continues to dominate the production and consumption landscape, largely due to the presence of major electronics manufacturing hubs in China, Japan, and South Korea, which are heavy users of amorphous cores in consumer electronics and industrial machinery. North America and Europe, while lagging in sheer production volume, are significant centers for research, development, and high-value applications, particularly in aerospace, defense, and high-performance automotive components. These Western regions are characterized by stringent quality standards and a demand for highly customized, low-volume specialty materials. European regulations promoting energy efficiency, such as the Ecodesign Directive, further stimulate the adoption of high-efficiency components utilizing amorphous ribbons in power distribution and industrial motors.

Segment-wise, the market is primarily segmented by Application (e.g., Magnetic Shielding, Sensors, Power Devices) and End-Use Industry (e.g., Automotive, Telecommunications, Industrial). The Sensors segment is forecast to exhibit the highest Compound Annual Growth Rate, propelled by the increasing integration of sophisticated magnetic sensing devices in autonomous vehicles and IoT applications, where precision and miniaturization are paramount. In terms of product type, ribbons with Ultra-Low Magnetostriction characteristics are witnessing heightened demand, especially for noise-sensitive applications and precision instruments. The overarching trend across all segments emphasizes efficiency maximization, durability under harsh operating conditions, and the continuous push towards thinner gauges and wider ribbon widths to optimize core assembly processes.

User inquiries regarding the role of Artificial Intelligence (AI) in the Cobalt Based Amorphous Metal Ribbons Market frequently center on three critical areas: optimizing the complex rapid solidification manufacturing process, accelerating material discovery and alloy design, and predicting material performance under varied operational stress. Common concerns revolve around how AI can mitigate the high cost and volatility of raw cobalt by finding viable substitutions or enhancing yield rates in the melt spinning process. Users expect AI tools to analyze real-time cooling parameters (such as wheel speed, ejection pressure, and melt temperature) to minimize defects and ensure consistent ribbon quality, thereby addressing one of the primary historical challenges in amorphous metal production. Furthermore, there is strong interest in using machine learning to model the intrinsic magnetic behavior of new, untested alloy compositions, drastically reducing the traditional time-to-market for specialized ribbons targeting specific high-frequency or high-temperature environments.

The implementation of AI and machine learning (ML) models is poised to revolutionize the material science behind amorphous metal production. AI-driven predictive modeling can simulate the thermodynamic stability and ultimate magnetic properties (like coercive force and saturation induction) of thousands of potential cobalt-iron-silicon-boron combinations before physical synthesis is attempted. This capability streamlines the R&D pipeline, moving material innovation from costly, iterative trial-and-error experimentation to targeted, data-informed development. For manufacturers, integrating AI into manufacturing execution systems (MES) allows for real-time process adjustments, which is crucial for the highly sensitive melt spinning process, leading to substantial improvements in production efficiency and uniformity across large batches of thin ribbons.

Beyond material composition and processing, AI also plays a transformative role in supply chain management and application optimization. Machine learning algorithms can accurately forecast demand fluctuations from key end-user segments, allowing ribbon producers to optimize cobalt inventory levels, thereby mitigating financial risk associated with price volatility. In application engineering, AI assists end-users (e.g., transformer manufacturers) in optimizing core geometry design, predicting the lifespan of the amorphous core under various load cycles, and ensuring the final product meets exacting efficiency standards, ultimately enhancing product reliability and accelerating the adoption of these advanced materials in critical infrastructure projects.

The market dynamics for Cobalt Based Amorphous Metal Ribbons are governed by a robust interplay of Drivers, Restraints, and Opportunities, shaping the overall impact forces on industry growth. Key drivers include the global push for energy efficiency standards, notably in power distribution and data center infrastructure, necessitating the adoption of high-performance soft magnetic materials. The rapid expansion of electric vehicles (EVs) and hybrid electric vehicles (HEVs) significantly boosts demand, as these ribbons are crucial components in onboard chargers, high-frequency DC-DC converters, and precise current sensors required for battery management systems. These powerful demand-side forces ensure continuous technological investment and capacity expansion within the amorphous metal industry.

However, significant restraints temper this expansion. Foremost among these is the high and often volatile cost of raw cobalt, which directly impacts the profitability and competitive pricing of the final ribbon product compared to lower-cost ferrite or silicon steel alternatives. Furthermore, the specialized and capital-intensive nature of the manufacturing process (melt spinning) requires high technical expertise and substantial initial investment, creating high barriers to entry for new market participants. Challenges also exist in scaling up production while maintaining stringent quality control, especially concerning the mechanical fragility and handling requirements of extremely thin amorphous ribbons during post-processing and core winding operations by end-users.

Opportunities for market growth primarily lie in technological advancements and strategic diversification. Developing next-generation ribbons with partial or complete substitution of cobalt (e.g., utilizing nickel or increased iron content) while retaining critical magnetic properties offers a pathway to mitigate raw material cost risks. The emergence of IoT, smart infrastructure, and 5G telecommunications is creating entirely new application spaces for high-frequency magnetic components and advanced sensors, particularly in applications where electromagnetic interference (EMI) shielding is paramount. The successful commercialization of wider ribbon widths and ultra-thin gauges also presents a compelling opportunity for manufacturers to optimize efficiency gains in large-scale power applications and precision magnetic heads, respectively, driving substantial value capture in niche markets. The cumulative impact force matrix favors continued moderate-to-high growth, provided the industry successfully navigates raw material constraints and further optimizes manufacturing costs.

The Cobalt Based Amorphous Metal Ribbons Market is comprehensively segmented across several dimensions crucial for understanding market dynamics and targeted strategic investment. Primary segmentation is defined by Type (based on magnetic properties and composition), Application (based on functional use in electronic and electrical systems), and End-Use Industry (based on the primary sector utilizing the final product). The Type segmentation often differentiates between Ultra-Low Magnetostriction Ribbons (ideal for precision sensors and noise-sensitive devices) and High Permeability Ribbons (used extensively in choke coils and common mode filters). This structural delineation allows stakeholders to accurately gauge demand pockets and align production capabilities with specific market needs, focusing on high-growth areas such as advanced magnetic shielding materials for sensitive electronic devices and components used in high-frequency power transfer systems.

The value chain for Cobalt Based Amorphous Metal Ribbons is relatively complex, beginning with highly specialized upstream raw material procurement and culminating in highly technical downstream integration into advanced electrical systems. Upstream analysis focuses heavily on the sourcing and processing of high-purity raw materials, primarily cobalt, iron, silicon, and boron. Given cobalt’s high cost and geopolitical supply risks, secure sourcing and effective inventory management are critical functions performed by specialized metal suppliers and refiners. Manufacturers of the amorphous ribbons must maintain strong relationships with these suppliers to ensure material quality and mitigate price volatility, as the quality of the starting melt profoundly influences the magnetic performance of the final ribbon.

The core manufacturing stage involves the capital-intensive and proprietary rapid solidification process (melt spinning). Ribbon manufacturers invest heavily in R&D to refine alloy compositions and optimize process parameters for specific market requirements, resulting in a differentiated final product based on width, thickness, and inherent magnetic properties. The distribution channel structure varies based on the end application. For high-volume, standardized applications (like consumer electronics power supplies), indirect distribution through specialized industrial distributors and component houses is common. Conversely, for highly customized and specialized applications, such as high-precision aerospace sensors or custom magnetic shielding, direct sales channels and technical collaboration with the end-user are preferred, ensuring exact specifications are met.

Downstream analysis involves the integration of the ribbons, often processed into toroidal cores or laminated stacks, into final products by Original Equipment Manufacturers (OEMs). Key downstream players include manufacturers of power transformers, specialized industrial sensors, automotive electronics suppliers, and producers of advanced telecommunications hardware. The success of the downstream market relies heavily on the performance guarantees provided by the amorphous core, such as documented core loss reduction and reliability under extreme operating conditions. This strong reliance on technical specifications fosters a tight feedback loop between ribbon producers and downstream integrators, pushing continuous innovation in core winding techniques and thermal management solutions to fully exploit the superior properties of the cobalt based amorphous materials.

The primary end-users and buyers of Cobalt Based Amorphous Metal Ribbons are sophisticated manufacturers across sectors demanding exceptionally high performance in magnetic components, energy efficiency, and operational reliability. These potential customers include major players in the automotive industry, specifically suppliers specializing in components for electric and hybrid vehicles, requiring highly efficient power inductors and precise current sensors for traction motor control and battery state-of-charge monitoring. The transition away from traditional combustion engines towards electrified powertrains ensures that the automotive sector remains a rapidly growing and high-value customer base for these advanced materials, prioritizing low core loss and compact component size for optimized packaging within confined vehicle spaces.

Another major segment comprises manufacturers within the power electronics and industrial automation sectors. Companies producing high-frequency switch-mode power supplies (SMPS), uninterruptible power supplies (UPS), and industrial automation equipment rely on the superior magnetic properties of cobalt ribbons to achieve high power density and minimal heat generation. The low magnetostriction variants are particularly attractive to manufacturers of specialized electromagnetic shielding required for sensitive medical imaging equipment and high-bandwidth data center servers, where minimizing external electromagnetic interference is critical for operational integrity and data security. These industrial buyers value performance stability and long-term reliability in harsh operational environments.

Furthermore, telecommunications infrastructure developers, particularly those building out 5G networks, represent a crucial and expanding customer base. The high-frequency nature of 5G components necessitates materials that maintain efficiency and low loss at higher operating frequencies than traditional ferrites, positioning cobalt amorphous ribbons as essential components in high-speed data filters, common mode chokes, and specialized high-frequency transformers used in base stations and network equipment. The aerospace and defense sector also procures these ribbons for high-reliability magnetic sensors, lightweight power distribution systems, and specialized shielding applications where weight reduction and guaranteed performance in extreme conditions are non-negotiable purchasing criteria, cementing their role as key buyers of premium, specialized ribbon products.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 698 Million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hitachi Metals Ltd., Advanced Technology & Materials Co., Ltd. (AT&M), Qingdao Yunlu Advanced Material Technology Co., Ltd., Metglas Inc., Zhejiang Dongmu Electronics Co., Ltd., China Steel Sumikin Joint Co., Ltd. (CSM), VACUUMSCHMELZE GmbH & Co. KG (VAC), Lamination Specialties Inc. (LSI), Shenyang Amorphous Technology Co., Ltd., MK Magnetic, SAMWHA ELC., TDK Corporation, Fuji Electric Co., Ltd., Magnetec GmbH, Advanced Metalic Technology (AMT). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Cobalt Based Amorphous Metal Ribbons market is defined by continuous innovation in the rapid solidification process and material science to achieve superior magnetic and mechanical properties. The foundational technology remains planar flow casting, commonly known as melt spinning, which involves ejecting a stream of molten alloy onto a high-speed, chilled rotating copper wheel, forming a thin, rapidly cooled ribbon. Key technological advancements center on optimizing the nozzle design, ejection pressure control, and wheel surface finish to improve ribbon width uniformity, minimize thickness variations (typically ranging from 20 to 30 micrometers), and reduce internal stresses that can negatively affect magnetic performance. Manufacturers are increasingly utilizing sophisticated sensor arrays and closed-loop control systems, often leveraging AI, to ensure precise control over the cooling rate, which is the singular most critical determinant of the resulting amorphous structure and soft magnetic behavior.

Furthermore, significant focus is placed on enhancing the intrinsic material properties through precise alloy formulation and post-processing treatments. Achieving near-zero magnetostriction—a property highly valued in sensors and electromagnetic shielding—requires extremely precise control over the cobalt-to-iron ratio and the inclusion of metalloids like boron and silicon. Annealing technologies are also crucial, involving controlled heat treatments applied below the crystallization temperature of the amorphous alloy. These treatments relax internal atomic stresses and induce desirable short-range ordering, dramatically improving magnetic permeability and reducing core losses. Vacuum or controlled atmosphere annealing is employed to prevent oxidation and ensure the final ribbon achieves its peak soft magnetic performance, allowing it to function reliably in high-frequency applications exceeding 100 kHz.

Current research and development efforts are concentrated on several cutting-edge areas, including the production of ultra-thin ribbons (below 15 micrometers) to minimize eddy current losses at very high frequencies, essential for advanced telecommunications and high-speed data transmission systems. Another key technological frontier is the development of advanced coating and lamination techniques to enhance the mechanical robustness of the ribbons and ensure high dielectric strength between layers in wound cores, preventing short circuits and improving overall component longevity. Lastly, research into novel, high-saturation amorphous or nanocrystalline materials derived from cobalt ribbons—such as Finemet-type materials—is driving innovation toward higher operating temperature capabilities and superior performance characteristics that bridge the gap between traditional amorphous metals and highly specialized nanocrystalline alternatives, ensuring the technology remains competitive across evolving electrical demands.

The Cobalt Based Amorphous Metal Ribbons market exhibits distinct geographical patterns driven by regional manufacturing concentration, technological adoption rates, and regulatory environments.

The primary advantage is their unique non-crystalline structure, which results in exceptionally low core loss, high magnetic permeability, and near-zero magnetostriction. This makes them highly efficient for high-frequency applications, reducing energy waste and heat generation in components like transformers and sensors.

The market is primarily segmented by application into magnetic shielding, high-precision sensors (current and magnetic field), and cores for power devices such as high-frequency transformers and inductors. Growing segments include electromagnetic compatibility (EMC) components for 5G infrastructure and automotive electronics.

High and fluctuating cobalt prices represent a significant restraint, increasing the overall manufacturing cost of the ribbons compared to iron-based alternatives. This volatility incentivizes manufacturers to research alloy substitutions and improve production yields to mitigate raw material cost dependence.

The Asia Pacific (APAC) region, driven by major electronics and EV manufacturing hubs in countries like China, Japan, and South Korea, currently leads the global consumption and production capacity for Cobalt Based Amorphous Metal Ribbons.

Future growth is driven by advancements in ultra-thin ribbon production (below 15 micrometers) for high-frequency efficiency, the use of AI for rapid alloy discovery, and improved annealing techniques to achieve enhanced magnetic performance suitable for high-temperature and high-power density applications, particularly in electric vehicles.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.