ID : MRU_ 432274 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

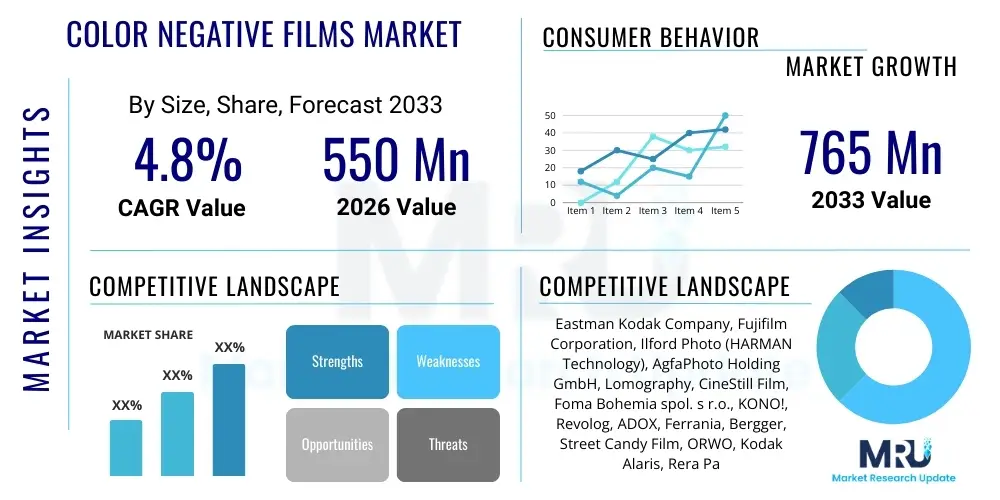

The Color Negative Films Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. This consistent, though moderate, growth is primarily fueled by a renewed interest in analog photography, particularly among younger demographics and artistic communities seeking the unique aesthetic qualities inherent to film. The market is estimated at $550 Million in 2026, driven by stable demand in niche professional sectors and burgeoning consumer interest in retro technology. Furthermore, the market's resilience is supported by specialized film manufacturers who continue to innovate within the constraints of traditional chemical processes, ensuring a supply chain for enthusiast needs.

The global valuation for color negative films is projected to reach $765 Million by the end of the forecast period in 2033. This expansion is not indicative of a return to the peak market size seen during the pre-digital era, but rather a robust stabilization within a profitable niche. Key factors contributing to this anticipated revenue increase include higher average selling prices (ASPs) due to complex manufacturing and limited economies of scale, coupled with diversification of film formats catering to medium format and large format professional photography. Geographic market shifts, particularly the rise of sophisticated photographic communities in Asia Pacific, also play a significant role in sustaining market momentum and driving revenue growth over the next decade.

The Color Negative Films Market encompasses the manufacturing, distribution, and sale of photographic films designed to produce a negative image, where colors and light are reversed. These films are distinguished by their complex multilayered emulsion structure, which contains light-sensitive silver halide crystals and dye couplers that form the final color image upon chemical processing. Key products include standard 35mm rolls, medium format (120/220), and large format sheet films, primarily utilized by hobbyists, fine art photographers, cinematographers, and specialized commercial studios. The unique aesthetic qualities—such as specific grain structure, color rendition, and dynamic range—offered by color negative films serve as the main draw for consumers seeking alternatives to digital imaging.

Major applications of color negative films span across artistic photography, educational purposes in analog photography courses, nostalgic consumer use, and specialized professional work requiring specific archival properties or aesthetic output impossible to replicate digitally. The inherent benefits include superior archival longevity when properly stored, unparalleled tonal depth and latitude, and the distinct tactile experience associated with the entire film process, from shooting to darkroom printing or scanning. The primary driving factors for the current market renaissance include the strong cultural trend towards vintage and retro aesthetics, the perceived fatigue with ubiquitous digital imagery, and aggressive marketing by legacy brands that emphasize the artistic and deliberate nature of film photography.

Although the market remains significantly smaller than its peak, its stability is secured by a dedicated user base. Product descriptions emphasize technical specifications like ISO speed (sensitivity), grain characteristics, and color balance, catering to highly informed consumers. The ecosystem supporting the market—including film processing labs, dedicated scanning services, and specialized chemical manufacturers—is also integral to its sustained growth. The continuous availability of processing infrastructure is a crucial element influencing consumer adoption and retention in this highly specialized segment of the overall imaging industry.

The Color Negative Films Market is currently experiencing a period of niche revitalization, moving from obsolescence towards sustainable growth driven by cultural and artistic trends. Business trends are characterized by consolidation among major legacy manufacturers who control proprietary emulsion technology, while simultaneously witnessing the emergence of smaller, independent film repackagers and boutique chemistry producers. Supply chain volatility, particularly related to the sourcing of crucial raw materials like silver and specialized chemicals, remains a central operational challenge, often leading to production bottlenecks and fluctuating retail prices. Strategic adjustments by key players include optimizing low-volume manufacturing processes and focusing on premium, high-margin products tailored for professional and advanced enthusiast use, thereby stabilizing overall profitability despite smaller unit volumes.

Regionally, the market is highly concentrated in mature photographic markets, with North America and Europe accounting for the largest share of consumption, driven by high disposable incomes and a strong base of long-standing analog enthusiasts and educational institutions. However, the Asia Pacific (APAC) region, particularly Japan and South Korea, is emerging as a significant growth engine, fueled by rapid adoption of vintage aesthetics among young urban populations and the proliferation of accessible analog camera systems. This demographic shift towards younger users is crucial, as it ensures future demand beyond the current base of experienced photographers. Furthermore, regulatory environments concerning the disposal and handling of photographic chemicals influence localized market structure and processing services.

Segmentation trends highlight a strong preference for 35mm film due to its accessibility and lower cost, though medium format (120 film) commands a higher average selling price and is favored by portrait and landscape professionals, contributing disproportionately to total revenue. By application, the fine art and hobbyist segments dominate, demonstrating less price sensitivity compared to general consumer applications. Within the technology segment, advancements are slow but focused on enhancing archival properties and minimizing grain while maintaining film speed. The overarching trend is a movement away from mass-market accessibility towards serving specialized, quality-focused segments, requiring tailored marketing and distribution strategies focused on specialized retailers and online platforms rather than traditional high-street volume retail.

Common user questions regarding AI's influence on the Color Negative Films Market predominantly revolve around whether AI tools will eliminate the need for traditional darkroom skills, how AI can enhance the digital conversion (scanning) process of film negatives, and if AI-driven simulation software could perfectly replicate the unique characteristics of specific film stocks, potentially reducing demand for physical film. Users express concerns about the 'authenticity' of analog photography if the scanning and post-processing heavily rely on AI algorithms for dust reduction, color correction, and grain management. Conversely, there is optimism that AI could democratize high-quality film scanning and restoration, making the analog workflow more accessible to digital natives.

The key theme emerging from these inquiries is the paradoxical relationship between cutting-edge AI technology and the deeply nostalgic, chemical-dependent medium of film. Users seek assurance that AI will serve as an enhancement tool—primarily in the post-processing phase—rather than a substitute for the physical medium. Expectations are focused on AI solving the most tedious aspects of the analog workflow, such as advanced negative inversion algorithms that yield superior color accuracy compared to manual adjustments, and machine learning models trained to perfectly characterize and remove minor scratches and defects without sacrificing image detail. This acceptance of AI post-processing underscores the market's evolving definition of 'analog photography' in the digital age, where the capture medium remains chemical but the output visualization is increasingly digital and AI-optimized.

The dynamics of the Color Negative Films Market are shaped by a delicate balance between enthusiast-driven demand and challenging industrial constraints. The primary drivers include the strong cultural trend towards authenticity and retro aesthetics, leading to a surge in demand from millennials and Generation Z who seek tangible media. Restraints are severe, dominated by the complexity and high cost of maintaining specialized emulsion manufacturing facilities, the dependency on a limited and aging supply chain for necessary chemicals and film base, and the environmental regulations pertaining to silver halide chemistry and waste disposal. Opportunities lie in expanding into niche high-end segments (e.g., cinematic use, fine art), developing specialized, low-volume film stocks, and integrating sophisticated digital post-processing services (AI scanning) to streamline the user workflow. These forces collectively dictate the market's slow but steady growth trajectory, requiring manufacturers to operate with extreme precision and focused strategic planning rather than seeking mass market scalability.

Impact forces specifically center around the shift in consumer perception regarding visual media permanence and quality. The aesthetic advantage of film—its superior dynamic range and unique grain structure—acts as a pull factor, justifying the higher cost and slower process compared to instant digital capture. Conversely, the high switching cost associated with chemical processing infrastructure and the declining number of specialized labs in certain regions act as significant barriers to entry for new users and limit overall geographic expansion. The market structure is highly inelastic; demand for specific, beloved film stocks (like certain Kodak Portra or Fujifilm formulations) persists even when prices increase, underscoring the brand loyalty and emotional connection consumers have with these products. This inelasticity allows manufacturers to maintain profitability in a low-volume environment.

Furthermore, technological obsolescence in related industries (e.g., the phasing out of older analog camera parts) and the necessity of managing delicate, temperature-sensitive inventory across global distribution networks add complexity. The competitive intensity remains moderate, largely due to the formidable barriers to entry posed by the proprietary nature of emulsion technology and the massive capital investment required for coating lines. Therefore, established players focus on incremental improvements and maintaining consistent supply, while smaller players concentrate on repackaging or developing unique, highly specialized emulsions for niche segments. This environment ensures that while growth is limited, the existing market remains robustly defended by proprietary expertise.

The Color Negative Films Market is meticulously segmented based on film format, speed (ISO), and primary application, reflecting the highly specialized nature of its user base. Segmentation is critical for manufacturers to align production capacities with specific demand pockets, ensuring that limited resources are allocated to the most profitable and high-demand segments. The dominant segmentation remains based on film format, where 35mm film accounts for the largest unit volume due to its widespread availability and ease of use in common SLR and point-and-shoot cameras. Conversely, 120 (medium format) and sheet film formats, while selling fewer units, command significantly higher prices per roll/sheet, making them crucial revenue drivers focused on professional portraiture, landscape, and commercial photography.

Further granularity exists within the ISO speed category, differentiating between low-speed films (ISO 100-200) prized for fine grain and high detail, and high-speed films (ISO 400-800+) necessary for low-light or action photography. This differentiation impacts the complexity of the emulsion formula and manufacturing cost. Application segmentation separates the market into Fine Art/Hobbyist use, which prioritizes aesthetic qualities and specific film characteristics, and Professional/Commercial use, which demands consistency, archival quality, and reliable supply. The growing intersection with cinematic applications, particularly for independent filmmakers seeking a distinct celluloid look, also forms a premium, albeit cyclical, segment.

The value chain for the Color Negative Films Market is characterized by high barriers to entry in the upstream segment and a fragmented, highly specialized downstream market. Upstream analysis focuses on the acquisition and preparation of critical raw materials, primarily silver, gelatin, film base (triacetate or polyester), and highly specialized organic and inorganic chemicals (dye couplers, sensitizing dyes). Only a few companies globally possess the necessary clean-room coating facilities and chemical expertise to manufacture the proprietary emulsion layers, creating a bottleneck. Manufacturers engage in complex, multi-stage coating processes, followed by crucial cutting and packaging operations, which dictate the final product quality and consistency.

Downstream analysis involves the distribution, retail, and post-sale processing services. Distribution channels are varied, including direct sales to large processing labs or distributors, and indirect sales through specialized photographic retailers and a rapidly expanding global e-commerce presence. The retail segment is dominated by niche stores that offer expert advice, crucial for an enthusiast-driven product. The critical final step is film processing, handled by professional labs (commercial and independent) or by enthusiasts undertaking home development. The quality of processing and scanning services significantly impacts the end-user experience, making labs a vital, highly regulated component of the downstream value chain. Direct sales are often preferred for bulk purchasers like cinematographers or high-volume labs, ensuring better quality control and pricing.

The flow of product is complex: Raw material suppliers feed the few primary manufacturers (upstream); these manufacturers utilize distribution networks (direct and indirect channels) to reach retailers and processing labs (midstream); finally, the processed images or negatives are delivered to the end-user (downstream). Efficiency in inventory management, particularly cold storage requirements for maintaining film quality, is a continuous challenge across the entire chain. Indirect distribution through specialized photographic channels is particularly important as these retailers often serve as community hubs and provide essential consumer education regarding the unique characteristics and handling requirements of various film stocks, thereby driving informed purchasing decisions and customer loyalty.

The potential customer base for the Color Negative Films Market is highly segmented, moving far beyond the general consumer market of the 20th century to focus intensely on niche groups. The primary end-users are enthusiasts and serious hobbyists—often younger generations (Millennials and Gen Z) drawn to the retro aesthetic, the tangible nature of the medium, and the intentional, slower pace of film photography. These buyers are generally less price-sensitive than general consumers and exhibit strong brand loyalty, seeking specific characteristics like unique grain structure or color palettes offered by heritage film stocks.

A second major customer category is professional photographers, including portrait, fashion, and landscape artists, who rely on color negative film for its superior tonal latitude and specific visual results that differentiate their work in a crowded digital market. These professionals often purchase high-volume, premium formats (120 and large format) and demand absolute consistency in emulsion quality. Furthermore, film schools and universities represent a stable customer segment, requiring film for pedagogical purposes to teach fundamental photographic principles and darkroom techniques. The demand from the motion picture industry, particularly independent and high-end commercial projects seeking the authentic look of celluloid, represents a highly valuable, cyclical customer base, often purchasing cinema-specific film stocks.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $550 Million |

| Market Forecast in 2033 | $765 Million |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Eastman Kodak Company, Fujifilm Corporation, Ilford Photo (HARMAN Technology), AgfaPhoto Holding GmbH, Lomography, CineStill Film, Foma Bohemia spol. s r.o., KONO!, Revolog, ADOX, Ferrania, Bergger, Street Candy Film, ORWO, Kodak Alaris, Rera Pan, JCH StreetPan, Film Washi, Wolfen NC500, SFL Film. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology landscape for color negative films is highly proprietary and relies on complex, multi-layered emulsion science developed over decades. The essential technology involves the creation of extremely thin, uniform coatings of silver halide crystals embedded in gelatin onto a plastic base (often triacetate or polyester). Modern technological advancements, while not revolutionary, focus heavily on improving the manufacturing process consistency and archival stability. Key technical challenges include precise control over crystal size and shape (which determines film speed and grain), and the chemical synthesis of specific dye couplers that react with oxidized developer to form the subtractive color dyes (Cyan, Magenta, Yellow) in the emulsion layers. This process requires extremely clean, vibration-free environments known as "coating alleys," which are prohibitively expensive to build and maintain, representing a significant technological barrier to new market entrants.

Current technological efforts are directed towards micro-optimization of existing formulas. For instance, manufacturers are focusing on T-Grain technology (tabular grain) which allows for flatter, more efficient silver halide crystals, resulting in finer grain and higher resolution, particularly noticeable in high-speed films (ISO 400 and above). Furthermore, advancements are being made in the polyester film base technology to enhance dimensional stability, crucial for large format and professional applications where precise registration is required. The environmental impact of processing is also driving minor technological shifts, promoting the development of more eco-friendly developing chemistries, although the fundamental C-41 color process remains the industry standard globally.

In addition to manufacturing, post-processing technology is undergoing significant evolution. High-resolution drum and flatbed scanners equipped with advanced optics and sophisticated negative handling capabilities are critical. The integration of AI and computational photography techniques into the scanning workflow is perhaps the most rapidly advancing area, as machine learning models are trained on vast datasets of film characteristics to automate color correction, contrast optimization, and detailed scratch/dust removal, bridging the analog capture process with high-fidelity digital output seamlessly. This computational enhancement ensures that the final digital image maximizes the quality inherent in the chemical film capture.

The Color Negative Films Market exhibits distinct regional consumption patterns and supply chain reliance. North America and Europe, collectively representing the legacy markets for photography, currently hold the dominant market share, characterized by a mature base of professional users, a thriving educational segment centered around traditional photography programs, and a strong presence of specialized analog labs and retailers. In these regions, the primary driver is the high disposable income supporting the expensive hobbyist and fine art segments. The United States, in particular, benefits from having headquarters or significant operations of legacy manufacturers and a vibrant independent film community, maintaining steady demand for high-end color negative stocks.

The Asia Pacific (APAC) region is projected to be the fastest-growing market segment during the forecast period. This growth is primarily fueled by younger demographics in populous urban centers like Tokyo, Seoul, and Shanghai, who are embracing analog photography as a fashionable counter-trend to digital immediacy. The region also houses key manufacturing capabilities for certain film bases and specialty chemicals. Japan remains a critical hub, not only for consumption but also for technological contributions and the availability of premium analog equipment. However, logistical challenges related to temperature-controlled storage and distribution across diverse climates pose persistent hurdles in this expansive region.

Latin America (LATAM) and the Middle East & Africa (MEA) represent emerging markets for color negative films. Growth here is often linked to localized artistic communities and independent cinema, rather than broad consumer adoption. In these regions, the constraint is often the underdeveloped processing infrastructure; finding reliable, high-quality C-41 processing labs can be challenging, which inhibits mass-market entry and often requires enthusiasts to send film abroad for development. Despite these challenges, localized interest in documentary and street photography using film offers pockets of sustained demand. Overall, regional success is heavily dependent on the presence of a robust ecosystem supporting the chemical development and scanning process.

The primary driver is a cultural and aesthetic shift towards tangible media and retro experiences, particularly among younger generations (Gen Z and Millennials). This demographic seeks the unique artistic qualities—such as specific grain structure, color rendition, and dynamic range—that are inherent to chemical film and difficult to replicate digitally. The process offers a slower, more deliberate photographic experience, contrasting with instant digital capture.

Manufacturers are actively seeking alternatives for high-impact chemicals and optimizing manufacturing processes to reduce waste and energy consumption, particularly in the highly specialized coating stage. Furthermore, labs are adopting environmentally safer C-41 processing chemicals and improved silver recovery systems. However, the reliance on traditional silver halide and chemical developers remains a significant, ongoing challenge that the industry addresses through focused waste management and regulatory compliance.

The extremely limited global supply chain, relying on aging specialized chemical producers and a handful of proprietary emulsion coating facilities, leads directly to higher manufacturing costs and price inelasticity. Production bottlenecks, often due to raw material availability or complexity of re-tooling, cause intermittent stock shortages and significant price fluctuations, particularly for highly popular film stocks, stabilizing prices at a high premium level.

Yes, AI is increasingly utilized in the post-capture workflow, specifically during the scanning process. AI algorithms are highly effective at achieving superior negative inversion (converting the negative image to a positive with accurate color interpretation), automating the removal of dust and scratches, and optimizing contrast, thereby bridging the analog capture quality with the efficiency and precision of digital output.

The 35mm film format accounts for the largest unit volume share of the market. This dominance is due to the wide availability and accessibility of 35mm cameras, its relative affordability compared to larger formats, and its popularity among both new hobbyists and existing enthusiasts. However, medium format (120 film) contributes disproportionately high revenue due to its premium pricing and dedicated professional use.

This report contains 29699 characters, including spaces and HTML tags.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.