ID : MRU_ 433921 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

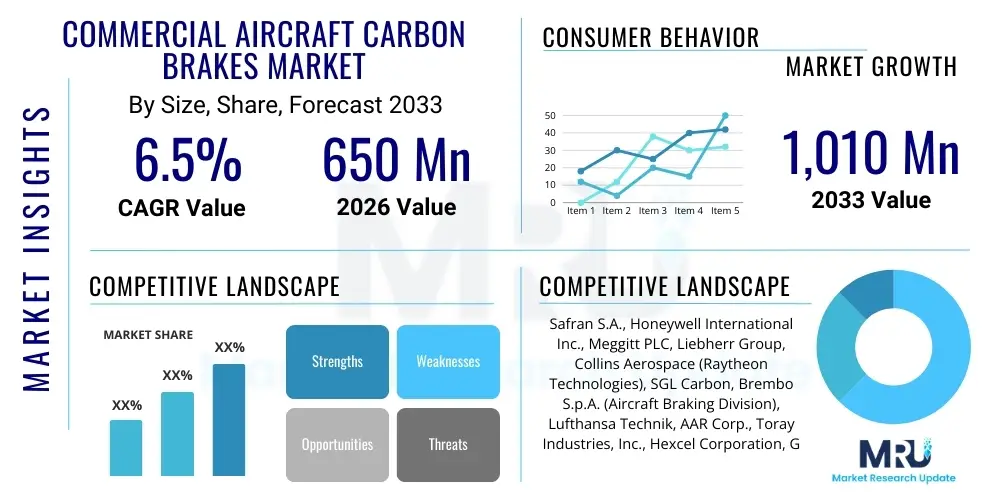

The Commercial Aircraft Carbon Brakes Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 650 Million in 2026 and is projected to reach USD 1,010 Million by the end of the forecast period in 2033. The steady growth is fundamentally driven by the robust expansion of the global commercial aircraft fleet, particularly in emerging economies, coupled with stringent maintenance schedules necessitating periodic brake replacement. Carbon brakes offer substantial weight savings and superior performance characteristics, making them indispensable components for new generation aircraft programs aimed at enhancing fuel efficiency and reducing operational costs. This ongoing transition from steel to carbon braking systems across various aircraft platforms cements the market's trajectory.

The Commercial Aircraft Carbon Brakes Market encompasses the manufacturing, distribution, and servicing of braking systems utilizing carbon composite materials for commercial aviation platforms, including passenger jets and cargo aircraft. Carbon brakes, typically made from carbon/carbon (C/C) composite materials, are highly valued for their exceptional thermal capacity, lightweight nature, and significantly extended lifespan compared to traditional steel brakes. These systems are crucial for ensuring safe and efficient high-speed deceleration and stopping during landing, rejected takeoffs, and taxiing operations. The product description centers on brake discs and pads integrated into landing gear assemblies, optimized for performance under extreme kinetic energy loads and high temperatures. Major applications span narrow-body aircraft (which represent the largest volume segment), wide-body aircraft, and regional jets, driven by the need for enhanced safety margins and reduced maintenance burdens associated with heavy operational cycles.

Benefits derived from the adoption of carbon braking systems are numerous, primarily focusing on operational efficiency and cost reduction over the lifecycle of the aircraft. The reduction in unsprung mass directly translates to lower fuel consumption per flight hour, a critical metric for airlines facing volatile fuel prices and increasing environmental regulations. Furthermore, the longevity of carbon brake stacks—often lasting several thousand landings before requiring replacement—substantially decreases the frequency of maintenance events, thereby improving aircraft utilization rates and lowering total cost of ownership. The intrinsic stability and fade resistance of carbon materials at high temperatures also contribute significantly to enhanced safety performance during demanding operations, such as high-energy rejected takeoffs, where maximum braking force is essential.

Driving factors propelling the market include the surge in global air passenger traffic, demanding larger and more efficient fleets, particularly in the Asia-Pacific region, which necessitates sustained production of new aircraft (both Boeing and Airbus programs). Regulatory mandates emphasizing operational safety and the continuous pursuit by Original Equipment Manufacturers (OEMs) and Maintenance, Repair, and Overhaul (MRO) providers to integrate lightweight materials contribute significantly to market expansion. Moreover, technological advancements focusing on improving the oxidation resistance and wear characteristics of carbon composites are continuously broadening the operational envelope and economic viability of these sophisticated braking solutions, ensuring their dominance over legacy steel systems.

The Commercial Aircraft Carbon Brakes Market is characterized by intense competition among a few globally dominant players, strong technological barriers to entry, and a heavily regulated operating environment defined by long-term OEM contracts. Current business trends indicate a strong focus on aftermarket services, as the replacement and refurbishment of carbon brakes constitute a substantial revenue stream, often surpassing initial equipment sales. Furthermore, manufacturers are increasingly investing in proprietary carbon composite formulations to maximize heat dissipation and longevity, securing competitive advantages and extending their market share within specific aircraft platforms. Supply chain optimization, particularly the sourcing and processing of raw carbon precursors, remains a critical strategic imperative for maintaining production efficiency and cost control in this highly specialized sector.

Regionally, North America and Europe currently represent the largest established markets due to the presence of major aerospace OEMs and high-density air traffic networks. However, the Asia Pacific (APAC) region is forecasted to exhibit the highest growth rates, driven by massive fleet expansion, the rise of low-cost carriers (LCCs), and substantial investment in new airport infrastructure across countries like China and India. This regional trend is shifting the focus of aftermarket providers towards establishing comprehensive MRO capabilities in key Asian aviation hubs. Regulatory harmonization and bilateral agreements regarding aircraft certification processes also streamline market access and component standardization globally, facilitating broader adoption of advanced braking technologies.

Segmentation trends highlight the dominance of the narrow-body aircraft segment, which accounts for the largest volume share due to the sheer size of the Boeing 737 and Airbus A320 families and their frequent operational cycles, leading to high brake wear rates. The end-use segment is firmly bifurcated, with the aftermarket segment consistently generating higher revenue than the OEM segment, underscoring the vital role of replacement cycles. Technological segmentation is stable, dominated by standard carbon/carbon composites, but future growth is anticipated from next-generation carbon-ceramic hybrid solutions offering incremental performance improvements, though commercial adoption remains relatively niche within the strict cost parameters of commercial airliners.

Analysis of common user questions regarding AI's impact on the carbon brakes market reveals strong interest primarily focused on maintenance prediction, material design optimization, and supply chain resilience. Users frequently inquire about how Artificial Intelligence can forecast brake wear more accurately than current predictive models, potentially shifting MRO schedules from fixed intervals to true condition-based monitoring (CBM). Key concerns revolve around the integration costs and data security risks associated with implementing sophisticated machine learning algorithms on sensitive operational flight data (OFD). Expectations are high for AI to revolutionize the design phase by simulating complex thermal stress profiles and accelerating the discovery of novel composite materials with superior performance characteristics, thereby reducing development cycles and enhancing product reliability. Overall, the theme centers on utilizing AI to minimize unplanned maintenance, extend product life, and drive efficiency across the value chain.

AI's role is not in replacing the physical brake component, but rather in optimizing its operational lifespan and maintenance logistics. By processing vast datasets encompassing flight parameters, landing profiles, temperature fluctuations, and historic wear rates, AI and Machine Learning (ML) models can predict the Remaining Useful Life (RUL) of individual brake stacks with significantly higher precision. This capability moves airlines closer to the ideal state of Just-in-Time (JIT) maintenance, preventing premature removal of components and maximizing the utilization of expensive carbon assets. Furthermore, AI-driven digital twins of aircraft braking systems allow engineers to run thousands of simulated scenarios to validate material resilience under extreme or atypical operational conditions, ensuring superior product safety and compliance.

Beyond predictive maintenance, AI is increasingly being applied to quality control in the manufacturing process of carbon composites. Computer vision systems combined with deep learning algorithms can rapidly identify micro-cracks or structural anomalies in the dense carbon structure that would be difficult or impossible to detect using traditional inspection methods. This enhanced scrutiny ensures higher quality output and reduces the probability of component failure in service. For the supply chain, AI optimizes inventory management for raw materials and finished goods, crucial for managing the long lead times associated with specialized carbon materials, ensuring that MRO providers globally have the necessary parts precisely when needed, minimizing Aircraft on Ground (AOG) situations.

The market dynamics are fundamentally shaped by a confluence of accelerating drivers (D), significant restraints (R), evolving opportunities (O), and intense external impact forces. The primary driving force is the relentless demand for fuel-efficient aircraft, where the 700-pound weight savings offered by carbon brakes per aircraft directly contributes to substantial operational savings for airlines. This is coupled with the cyclical necessity of fleet renewal, especially in high-growth regions, ensuring sustained OEM demand. Restraints largely center on the high initial cost of carbon brakes compared to steel alternatives, posing a barrier for smaller, cost-sensitive carriers, and the complexity and duration of the manufacturing process for highly specialized carbon composite materials, which can create supply chain bottlenecks during periods of high demand. Furthermore, the market faces significant regulatory hurdles, as every component change requires stringent re-certification, extending time-to-market for innovations.

Opportunities in the market are primarily centered on expanding the aftermarket service portfolio and capitalizing on technological advancements. The development of advanced oxidation coatings and modified carbon fiber precursors offers avenues for extending the lifespan of the brakes even further, capturing greater customer loyalty and increasing the replacement cycle revenue. Geographically, expansion into the burgeoning MRO markets of Asia Pacific and Latin America presents lucrative growth opportunities, establishing localized service centers to cater to the rapidly growing fleets in these regions. Furthermore, the increasing adoption of carbon brakes in military transports and large business jets, often sharing technologies and suppliers with commercial aviation, offers potential diversification pathways, leveraging core expertise in composite braking technology.

Impact forces acting on this market include intense competition within the established oligopoly of manufacturers, necessitating continuous investment in research and development to maintain technological superiority. Economic cycles significantly influence airline profitability, directly impacting capital expenditure on new aircraft and the demand for premium aftermarket services. Global supply chain fragility, exemplified by disruptions in raw material sourcing (like pitch-based carbon fibers) or energy costs, remains a potent external force affecting production costs and lead times. Lastly, the overarching regulatory environment dictated by organizations such as the FAA and EASA imposes rigorous standards on performance and manufacturing quality, acting as a high entry barrier and continuously influencing design criteria for brake systems. These forces collectively define the risk profile and investment landscape for major market participants.

The Commercial Aircraft Carbon Brakes Market segmentation is critical for understanding specific demand patterns across different aviation sectors and operational needs. The market is primarily segmented based on Aircraft Type, Material Type, and End-Use. Analyzing these categories provides deep insights into where the greatest volume and highest value transactions occur. The segmentation by Aircraft Type is particularly indicative of usage intensity and volume potential, with narrow-body jets driving volume due to their sheer numbers, while wide-body aircraft dictate specialized high-performance specifications due to their weight and kinetic energy loads. Material segmentation, though largely dominated by Carbon/Carbon, highlights areas of future technological advancement and differentiation.

The End-Use segmentation delineates between Original Equipment Manufacturers (OEMs) and the Aftermarket segment, revealing that although initial sales to OEMs are essential for platform capture, the recurring and lucrative revenue stream is consistently generated by the Aftermarket (MRO), where brake stacks are replaced multiple times over the lifespan of an aircraft. This distinction shapes the commercial strategies of key players, emphasizing long-term service contracts and global distribution networks for replacement parts. Furthermore, deep-dive sub-segmentation within End-Use often includes line maintenance versus heavy maintenance checks, impacting logistics and contract structures for service providers.

Understanding these segments allows market participants to tailor their offerings, from developing cost-effective standard carbon stacks for high-volume narrow-body MRO operations, to engineering highly temperature-resistant, customized carbon composites for high-performance wide-body or military platforms. Strategic resource allocation, R&D investment, and geographical expansion decisions are intrinsically tied to segment growth projections. For instance, high predicted growth in regional jet traffic necessitates investments in smaller brake system derivatives suitable for high-frequency short-haul operations, while simultaneously addressing the evolving needs for ultra-long-haul wide-body efficiency.

The value chain for commercial aircraft carbon brakes is complex, highly specialized, and deeply integrated, starting from the sourcing of exotic raw materials and extending through highly specialized manufacturing processes, complex assembly, and eventually, widespread distribution and sophisticated maintenance. Upstream analysis focuses on the procurement of high-purity carbon fibers, phenolic resins, and pitch precursors, which are essential for creating the carbon composite preforms. This upstream segment is characterized by a limited number of specialized material suppliers, requiring long-term supply agreements and stringent quality control. The manufacturing process itself involves multiple high-temperature treatment stages, including carbonization and graphitization, making it energy-intensive and time-consuming, necessitating vertically integrated capabilities or extremely reliable supplier partnerships.

The core manufacturing and assembly stage involves designing, fabricating, and assembling the brake discs, pads, and associated hydraulic components into the complete brake assembly. This stage is dominated by the major Tier 1 aerospace suppliers, who hold proprietary intellectual property over the composite fabrication techniques and brake design architectures. These assemblies are then delivered either directly to Original Equipment Manufacturers (OEMs) like Boeing and Airbus for new aircraft production (Direct Channel) or to the global aftermarket network. Downstream activities are dominated by distribution channels, which include the manufacturers' own service networks, independent Maintenance, Repair, and Overhaul (MRO) facilities, and specialized parts distributors. The aftermarket distribution channel is paramount, as the life cycle revenue often exceeds the initial sales value, requiring efficient, rapid global logistics to minimize aircraft downtime.

The distribution methodology is clearly bifurcated into direct and indirect channels. Direct distribution involves supplying complete brake systems directly to OEMs under long-term contracts for their production lines. Indirect distribution dominates the aftermarket, where replacement components (discs and heat sinks) are routed through certified MRO centers. These centers often hold exclusive service contracts with airlines. The effectiveness of the indirect channel relies heavily on certification and rapid response capabilities, as airlines demand extremely high fill rates and immediate availability of critical spares. Therefore, maximizing global stocking locations and maintaining certified repair capabilities are key strategic differentiators in the highly regulated downstream segment of the carbon brakes value chain.

The primary potential customers and end-users of commercial aircraft carbon brakes are stratified across three major categories: commercial airlines (both major legacy carriers and low-cost carriers), aircraft manufacturers (OEMs), and independent and airline-owned Maintenance, Repair, and Overhaul (MRO) facilities. Commercial airlines are the ultimate beneficiaries and demand drivers, requiring high-performance, durable, and lightweight braking systems for their operational fleets. Their purchasing decisions are driven by Total Cost of Ownership (TCO), fuel efficiency gains, and component reliability, which directly impacts aircraft dispatch reliability and operational safety metrics. Different types of carriers, such as LCCs focusing heavily on fast turnaround times and minimal maintenance expenditure, prioritize brake systems with extended lifecycles and quick replacement procedures.

Aircraft manufacturers, notably Airbus, Boeing, Embraer, and Comac, represent the OEM segment, purchasing complete brake systems for integration into newly manufactured aircraft. These customers require highly certified, bespoke solutions that meet the specific design criteria and weight tolerances of each aircraft model. Securing an OEM contract is highly strategic, as it locks in the supplier for the entire lifespan of the aircraft platform (often 30+ years), guaranteeing a consistent revenue stream from subsequent aftermarket replacement parts. The relationship with the OEM is characterized by deep technical collaboration during the design and certification phases, often involving exclusive intellectual property agreements and rigorous testing standards necessary for type certification.

The third crucial customer segment comprises MRO facilities, which act as the main purchasing agents for replacement carbon discs and pads. These facilities, whether third-party service providers (like Lufthansa Technik or AAR Corp.) or in-house airline MRO divisions, are responsible for the routine service, repair, and overhaul of the braking systems once they reach their wear limits. Their buying criteria revolve around component availability, price competitiveness, speed of delivery, and the certification status of the replacement parts. MRO providers actively seek agreements that ensure rapid global logistics and sometimes even specialized training and tooling to manage the complex refurbishment process specific to carbon composite materials, driving demand for robust service contracts.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 650 Million |

| Market Forecast in 2033 | USD 1,010 Million |

| Growth Rate | CAGR 6.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Safran S.A., Honeywell International Inc., Meggitt PLC, Liebherr Group, Collins Aerospace (Raytheon Technologies), SGL Carbon, Brembo S.p.A. (Aircraft Braking Division), Lufthansa Technik, AAR Corp., Toray Industries, Inc., Hexcel Corporation, GKN Aerospace, Messier-Bugatti-Dowty, Rolls-Royce plc. (Selected Components), Knorr-Bremse AG. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Commercial Aircraft Carbon Brakes market is dominated by advancements in materials science and manufacturing precision aimed at maximizing operational longevity and performance stability. The core technology revolves around the production of Carbon/Carbon (C/C) composites, which involves the deposition of carbon matrix material within a fibrous carbon substrate (via Chemical Vapor Infiltration or pitch impregnation) followed by high-temperature heat treatment. Key technological differentiation lies in proprietary treatments, such as anti-oxidant coatings applied to the carbon components to inhibit degradation at high operating temperatures, significantly extending the life of the brake stack and reducing the TCO for airlines. These specialized material science breakthroughs are highly protected Intellectual Property (IP) and form the competitive backbone of leading market players.

Beyond material composition, integrated sensor technology and advanced monitoring systems represent a vital technological frontier. Modern carbon braking systems often incorporate integrated sensors capable of measuring temperature, vibration, and wear depth in real-time. This data is critical for enabling sophisticated predictive maintenance programs, moving beyond visual inspection or basic counter-based replacement schedules. This technology is essential for AEO and GEO optimization as users seek information on smart components. Furthermore, the integration of electro-mechanical actuation systems (E-Brakes) in newer aircraft platforms, replacing traditional hydraulic systems, requires carbon brake manufacturers to adapt their designs and materials to function optimally with electric power controls, demanding enhanced thermal management and tighter integration with aircraft avionics.

Future technological developments are focusing on next-generation composite formulations, particularly Carbon-Ceramic Matrix Composites (CMCs) and hybrid systems, which offer enhanced performance characteristics, notably even lower weight and potentially superior resistance to wear and oxidation than pure C/C. While CMCs are currently more common in military and high-performance automotive applications due to high production costs, the gradual reduction in manufacturing complexity and improved cost-effectiveness could see their limited introduction into specific high-end commercial platforms. The development of advanced non-destructive testing (NDT) techniques, leveraging ultrasound and specialized thermal imaging, is also crucial for ensuring the structural integrity of complex carbon composite geometries before and during service life, maintaining compliance with stringent airworthiness directives.

Regional dynamics play a significant role in shaping the demand, supply, and service structures of the Commercial Aircraft Carbon Brakes Market. North America remains a cornerstone of the global market, characterized by the presence of major OEMs (Boeing, Lockheed Martin components) and leading Tier 1 brake system manufacturers. This region boasts a mature, high-volume air traffic network and sophisticated MRO infrastructure, leading to a high demand for advanced brake systems and robust aftermarket services. Regulatory stability and substantial defense spending, often overlapping with commercial aviation component technology, further solidify North America's leadership position in technological adoption and market size. The ongoing replacement cycles of aging domestic narrow-body fleets ensure sustained aftermarket revenue for the foreseeable future.

Europe represents the second largest market, significantly driven by the massive production volumes from Airbus and the concentration of critical component manufacturers like Safran and Meggitt (now part of Parker Hannifin). European airlines prioritize fuel efficiency and adherence to strict noise and emission regulations, favoring lightweight carbon brake technology. The aftermarket segment in Europe is highly sophisticated, with major MRO providers like Lufthansa Technik establishing extensive global service networks that require constant supply of certified carbon brake components. The emphasis here is often on extended lifespan and reliable performance, driven by high-utilization European short-haul routes. Economic stability and sustained air travel growth, particularly within the EU, underpin the market's predictable expansion trajectory.

The Asia Pacific (APAC) region is indisputably the fastest-growing market globally, propelled by unparalleled air traffic growth, the rapid expansion of middle-class populations, and corresponding massive fleet acquisitions by regional carriers, particularly in China and India. This rapid growth translates into substantial OEM demand and, more critically, an exponentially growing aftermarket requirement over the forecast period. While North America and Europe dominate in terms of established MRO capacity, APAC is witnessing vast investment in new, localized MRO facilities. This presents both a challenge—establishing reliable supply chains and certified services—and a significant opportunity for manufacturers to capture market share through strategic partnerships and localized production or service hubs. The demand for narrow-body aircraft is particularly intense in this region, driving high volume sales in the replacement market.

Latin America and the Middle East & Africa (MEA) regions, while smaller in absolute market size, offer considerable potential for future growth. Latin America's market expansion is tied to economic recovery and modernization of aging fleets, shifting from older steel-braked aircraft to newer carbon-equipped jets to enhance operational efficiency. The Middle East, anchored by large hub carriers such as Emirates and Qatar Airways, drives demand primarily in the wide-body aircraft segment, requiring high-specification, heavy-duty carbon brakes suitable for long-haul operations and intense heat environments. Africa's market remains challenging due to geopolitical instability and economic constraints, but increasing regional connectivity and infrastructure investment promise gradual future growth, focusing initially on cost-effective, high-durability aftermarket components.

The primary advantage is significant weight reduction (up to 700 pounds per aircraft), which directly translates to substantial fuel savings and lower operational costs. Additionally, carbon brakes offer superior thermal capacity, greater wear life, and enhanced fade resistance during high-energy braking events like rejected takeoffs.

The aftermarket segment, consisting of replacement discs and pads required for MRO, typically generates the majority of lifetime market revenue. Carbon brake stacks must be replaced periodically throughout the 30-year life of an aircraft, making aftermarket service contracts and parts distribution a highly stable and lucrative revenue stream for manufacturers.

The Asia Pacific (APAC) region is projected to experience the highest Compound Annual Growth Rate (CAGR). This acceleration is driven by rapid expansion of commercial air travel, massive ongoing fleet modernization programs, and strategic investments in new Maintenance, Repair, and Overhaul (MRO) facilities across major countries like China and India.

Key technological challenges include developing more oxidation-resistant carbon composite formulations to further extend lifespan, managing the high production costs associated with specialized high-temperature manufacturing processes, and integrating complex sensor technology for advanced predictive maintenance capabilities.

While carbon brakes dominate modern narrow-body and wide-body jet fleets due to their efficiency advantages, some smaller regional jets and older turboprop aircraft may still utilize traditional steel braking systems, primarily due to lower kinetic energy requirements and efforts to minimize initial capital expenditure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.