ID : MRU_ 431566 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

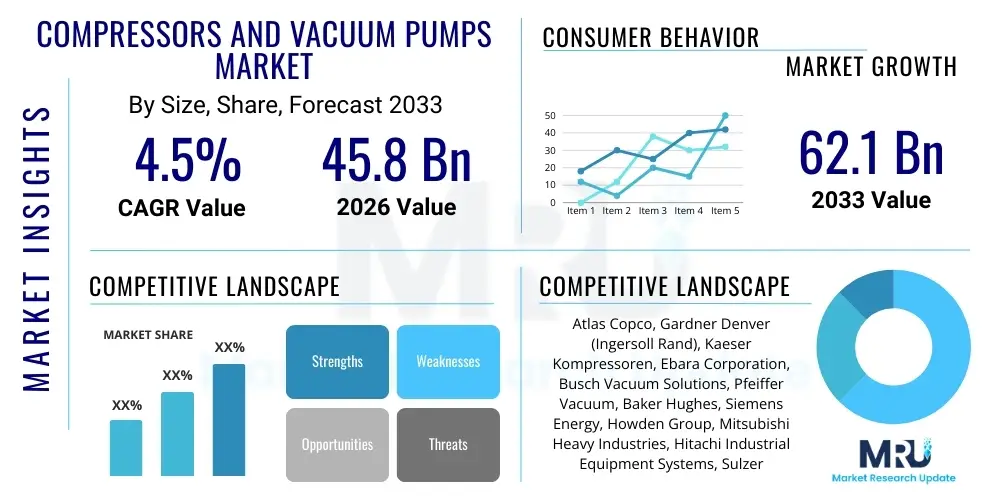

The Compressors and Vacuum Pumps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2026 and 2033. The market is estimated at USD 45.8 Billion in 2026 and is projected to reach USD 62.1 Billion by the end of the forecast period in 2033.

The Compressors and Vacuum Pumps Market encompasses a wide range of mechanical devices essential for numerous industrial processes, including manufacturing, energy generation, chemical processing, and healthcare. Compressors function by increasing the pressure of a gas or air, making them indispensable for pneumatic tools, cooling systems, and powering heavy machinery. Vacuum pumps, conversely, remove gas molecules from a sealed volume to leave behind a partial vacuum, crucial for semiconductor fabrication, lyophilization (freeze-drying) in pharmaceuticals, and specialized coating processes. These devices form the backbone of modern industrial infrastructure, providing the motive power and specialized environmental conditions required for high-precision and large-scale operations across global supply chains.

The core product offerings include positive displacement compressors (such as reciprocating and rotary screw) and dynamic compressors (like centrifugal and axial flow), alongside various types of vacuum pumps, including dry pumps, liquid ring pumps, and turbomolecular pumps. Major applications span petrochemical refineries, automotive assembly lines, HVAC systems, food and beverage processing, and emerging sectors like hydrogen fuel cell production. The critical benefits derived from these technologies include enhanced energy efficiency through optimized designs, improved process control, reduced operational noise, and the ability to handle corrosive or sensitive gases in controlled environments. Furthermore, continuous innovation in materials science and digitalization allows for extended lifecycles and reduced maintenance requirements.

The market is currently being driven by rapid industrialization in developing economies, particularly across Asia Pacific, which necessitates increased investment in manufacturing and infrastructure. Additionally, stringent environmental regulations requiring reduced energy consumption and lower emissions are compelling industries to upgrade to high-efficiency, oil-free compressors and dry vacuum systems. The expansion of high-tech manufacturing, such as the semiconductor industry's surging demand for ultra-high vacuum environments, is also providing significant impetus. Furthermore, the increasing adoption of Industry 4.0 principles, integrating these systems with IoT sensors and predictive maintenance platforms, is optimizing performance and accelerating market expansion.

The global Compressors and Vacuum Pumps Market is undergoing a transformation driven by sustainability mandates and technological advancements focused on energy efficiency and connectivity. Business trends indicate a strong shift towards service-oriented models, where manufacturers offer long-term maintenance contracts and performance monitoring packages enabled by integrated sensor technology. There is intense competition centered on developing oil-free and low-vibration solutions to meet cleanroom standards in sensitive industries like food processing and electronics. Key players are aggressively pursuing mergers and acquisitions to consolidate market share, particularly targeting specialized dry vacuum technology providers to capitalize on the semiconductor boom.

Regionally, the Asia Pacific (APAC) stands out as the primary growth engine, fueled by massive government investments in infrastructure, escalating manufacturing output, and expanding data center construction, all of which require reliable air and vacuum systems. North America and Europe, while mature markets, are experiencing demand driven primarily by replacement cycles and regulatory compliance, favoring premium, energy-efficient rotary screw compressors and advanced magnetic bearing turbo pumps. The Middle East and Africa (MEA) are seeing stable growth linked to petrochemical capacity expansions and water treatment projects, creating demand for heavy-duty, robust industrial compressors.

Segment trends reveal that the rotary screw compressor segment continues to dominate due to its versatility, reliability, and increasingly high efficiency, making it the preferred choice across general manufacturing. Concurrently, the dry vacuum pump segment is exhibiting the highest growth rate, necessitated by the stringent contamination avoidance requirements in semiconductor and pharmaceutical manufacturing. By application, the chemical and petrochemical sector remains a dominant revenue generator, but the electronics and power generation segments are experiencing accelerated adoption rates, especially as renewable energy sources and hydrogen infrastructure development become global priorities, demanding specialized high-pressure compressors and robust process vacuum solutions.

User queries regarding the impact of Artificial Intelligence (AI) on the Compressors and Vacuum Pumps Market typically revolve around three major themes: predictive maintenance efficacy, optimization of energy consumption in real-time, and autonomous operational control within smart factories. Users are keenly interested in how AI algorithms can analyze vast streams of operational data—including vibration, temperature, pressure, and energy draw—to anticipate equipment failure long before traditional monitoring methods, thereby maximizing uptime and minimizing catastrophic breakdowns. A significant concern is the necessary investment in retrofitting older machinery with compatible sensor technology and the development of robust, secure data infrastructure required to feed the AI models effectively. Furthermore, users expect AI integration to move beyond mere monitoring toward truly optimizing complex systems, such as dynamically adjusting compressor loads based on fluctuating production schedules or energy tariffs, thus achieving unprecedented levels of efficiency and operational intelligence.

The implementation of AI and machine learning models fundamentally shifts the service paradigm from reactive maintenance to prescriptive maintenance. By creating digital twins of compressor or pump systems, operators can simulate various operational scenarios and identify the optimal configuration for a given process, reducing energy waste which often accounts for a substantial portion of total operating costs. This AI-driven optimization is crucial in industries where compressed air is treated as a fourth utility, ensuring consistent supply and pressure stability without over-provisioning. The sophistication of AI allows for the recognition of subtle anomalies that human operators or standard threshold alarms might miss, significantly enhancing reliability and safety protocols.

However, the successful adoption of AI requires standardized communication protocols (e.g., OPC UA) and interoperability between different equipment vendors. The market is witnessing a convergence where traditional equipment manufacturers are partnering with or acquiring software analytics firms to embed these capabilities directly into their controllers. This integration not only secures their position in the digital supply chain but also ensures that the proprietary data generated by the machines is used effectively to refine the machine learning algorithms, making future generations of compressors and vacuum pumps inherently smarter and more adaptable to diverse industrial demands. The long-term impact is a reduced total cost of ownership (TCO) for end-users and a competitive edge for manufacturers providing superior data-driven insights.

The Compressors and Vacuum Pumps Market is primarily driven by expanding global manufacturing capacity and rigorous environmental mandates compelling industries to adopt sustainable, energy-efficient machinery. Restraints include the high initial capital expenditure associated with high-efficiency equipment, particularly dry vacuum systems and sophisticated centrifugal compressors, alongside the cyclical nature of end-user industries like construction and automotive, which can lead to fluctuating demand. Opportunities are abundant in the burgeoning hydrogen economy, which requires specialized high-pressure compressors, and the relentless expansion of data centers and electronics manufacturing, creating unprecedented demand for ultra-clean, high-throughput vacuum pumps. These forces collectively shape the market's trajectory, mandating continuous technological innovation to balance performance requirements with cost and regulatory constraints.

The primary driving force remains energy efficiency. Compressed air and vacuum generation are highly energy-intensive processes, often accounting for a significant portion of an industrial facility’s total electricity bill. Regulations such as the European Union’s Ecodesign Directive and similar efficiency standards globally push manufacturers to develop Variable Speed Drive (VSD) compressors and advanced controls that dramatically lower energy consumption during partial load operations. This regulatory environment acts as a continuous market accelerator, forcing the obsolescence of older, less efficient units and driving substantial replacement demand. Furthermore, the global infrastructure push, particularly in developing nations, necessitates large-scale, reliable air compression for construction, power generation, and industrial fabrication.

Key restraints include increasing raw material costs, particularly for steel, copper, and specialized coatings required for corrosion resistance, impacting manufacturing overhead and final product pricing. Additionally, the complexity of integrating advanced IoT and AI features into existing industrial setups poses a technological barrier for smaller enterprises. However, the largest opportunities lie in niche, high-growth applications. The transition towards Industry 4.0 creates an opportunity for comprehensive system providers, not just hardware vendors. Furthermore, the pharmaceutical and biotechnology sectors, driven by stricter quality control and sterilization needs, are massive consumers of specialized, oil-free compressors and sterile vacuum systems, presenting stable and high-value growth potential moving forward.

The Compressors and Vacuum Pumps Market is structurally segmented based on product type, technology, lubrication method, end-user industry, and region. Analyzing these segments provides a clear map of competitive intensity and growth hotspots. Product segmentation differentiates between Compressors (Reciprocating, Rotary, Centrifugal) and Vacuum Pumps (Dry, Liquid Ring, Turbomolecular, etc.). The lubrication segment, categorized into oil-free and oil-lubricated, is crucial as industries increasingly prioritize product purity and environmental compliance, favoring oil-free technologies despite their higher cost.

Technology segmentation focuses on the functional mechanisms, such as positive displacement versus dynamic compression, and further refines the understanding of applications—for instance, centrifugal compressors are favored for high-volume, continuous industrial gas compression, while reciprocating compressors are essential for high-pressure tasks. End-user analysis identifies the largest demand drivers, with manufacturing, oil and gas, and chemical sectors historically dominant. However, the rapid expansion of electronics and semiconductors is shifting market dynamics, demanding highly precise, low-vibration, and contamination-free solutions, which drives intense innovation within the vacuum pump segment.

The market’s future growth is heavily dependent on the performance of specific sub-segments. The Variable Speed Drive (VSD) technology within compressors is projected to see maximum growth due to mandated energy savings, while in vacuum technology, dry pumps are expanding rapidly, displacing older liquid-ring and oil-sealed pumps due to operational efficiency and environmental benefits. Geographic segmentation underscores the concentration of high-growth manufacturing capacity in the Asia Pacific region, making it the focal point for strategic market investment and supply chain establishment.

The value chain for Compressors and Vacuum Pumps is complex, starting with upstream activities involving the sourcing and processing of raw materials such as specialized alloys, castings, motors, and electronic components. Key upstream dependencies include reliable suppliers for high-precision components like air ends, rotors, seals, and advanced motor controls (especially VSD technology). The quality and cost stability of these core components directly influence the final product efficiency and reliability. Manufacturers heavily invest in R&D at this stage to optimize component design for reduced friction, enhanced heat dissipation, and superior corrosion resistance, ensuring the longevity and operational performance required by demanding industrial customers.

The core manufacturing stage involves assembly, quality testing, and the integration of control systems, including proprietary software and IoT connectivity modules. Efficiency in manufacturing relies on lean production techniques and rigorous quality assurance processes, particularly for highly specialized products like turbomolecular pumps where tolerances are extremely tight. Downstream activities involve distribution, sales, installation, and, critically, after-sales service. Direct distribution models are often used for large industrial projects or highly customized process compressors, allowing manufacturers to maintain direct control over installation and commissioning, while indirect channels, utilizing distributors and value-added resellers (VARs), handle standard commercial units and serve regional markets efficiently.

The distribution channel landscape is defined by the need for technical expertise. Unlike commodity products, compressors and vacuum pumps require specialized knowledge for selection, installation, and maintenance. Therefore, distributors often act as technical consultants, providing local support, parts inventory, and rapid repair services. This emphasis on service capabilities means that aftermarket support—including genuine parts supply, remote monitoring, and preventative maintenance contracts—constitutes a significant portion of the total market value and profitability. The shift toward EaaS models further solidifies the role of downstream services as a critical differentiator and revenue stream for market leaders.

Potential customers for compressors and vacuum pumps are diverse, spanning nearly every sector of the industrial economy, defined primarily by their need for controlled air pressure or specific vacuum environments. The largest and most demanding customer segment includes the Oil and Gas and Chemical/Petrochemical industries, which require heavy-duty, customized process gas compressors for synthesis, separation, and transport, often operating under extreme temperature and pressure conditions. These buyers prioritize reliability, compliance with strict safety standards, and long operational lifecycles, leading them to procure large, expensive centrifugal or reciprocating units directly from top-tier original equipment manufacturers (OEMs).

The General Manufacturing and Automotive sectors represent a high-volume market, relying heavily on standard rotary screw and reciprocating air compressors to power pneumatic tools, spray painting booths, and automated machinery. These customers seek energy-efficient solutions (like VSD compressors) to reduce operational costs and benefit significantly from robust local service networks provided by indirect distribution channels. Furthermore, the Food and Beverage sector, which demands oil-free compressors for product contact and packaging, is a rapidly expanding customer base driven by hygiene regulations and increased automation.

A rapidly emerging and high-value customer segment is the Electronics and Semiconductor industry, alongside adjacent high-technology clean processes like advanced battery manufacturing and aerospace component production. These customers are the primary consumers of highly sophisticated dry vacuum pumps and turbomolecular pumps, essential for creating the ultra-clean, high-vacuum environments necessary for deposition, etching, and cleanroom operations. Their purchasing decisions are driven less by price and more by ultra-low contamination risk, vibration control, and process throughput, making them ideal targets for manufacturers specializing in high-end, proprietary vacuum technology.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 45.8 Billion |

| Market Forecast in 2033 | USD 62.1 Billion |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Atlas Copco, Gardner Denver (Ingersoll Rand), Kaeser Kompressoren, Ebara Corporation, Busch Vacuum Solutions, Pfeiffer Vacuum, Baker Hughes, Siemens Energy, Howden Group, Mitsubishi Heavy Industries, Hitachi Industrial Equipment Systems, Sulzer Ltd., ANEST IWATA Corporation, Corken, Inc., Fusheng Group, PMP Industries, Leybold GmbH, Dekker Vacuum Technologies, Becker Pumps, and Aerzen. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for compressors and vacuum pumps is rapidly evolving, driven primarily by the pursuit of enhanced energy efficiency, digitalization, and cleaner operation. A cornerstone of modern compressor technology is the widespread adoption of Variable Speed Drive (VSD) systems, which match the motor speed and power consumption precisely to the fluctuating demand for compressed air, often resulting in energy savings of 20% to 35% compared to fixed-speed units. Alongside VSD, advancements in permanent magnet motor technology are increasing power density and overall efficiency, particularly in rotary screw and scroll compressors. Furthermore, the push for oil-free operation utilizes technologies like water injection, ceramic coatings, and specialized dry screw or scroll air ends, which are essential for quality-sensitive applications like pharmaceuticals and electronics where even minute oil residue is unacceptable.

In the vacuum pump sector, the most significant technological shift is the dominance of dry vacuum technologies, which completely eliminate the need for sealing or lubricating fluids in the pumping chamber, addressing contamination concerns and reducing maintenance complexity. Dry pumps, including multi-stage roots pumps, screw pumps, and scroll pumps, are replacing traditional oil-sealed rotary vane pumps across high-tech industries. For ultra-high vacuum requirements—critical in processes like molecular beam epitaxy or advanced particle accelerators—magnetic levitation turbomolecular pumps represent the cutting edge, offering extremely high pumping speeds and complete mechanical stability with zero vibration and hydrocarbon contamination. The integration of advanced materials, such as specialized ceramics and composites, also plays a crucial role in improving pump reliability and thermal management in challenging process environments.

Digitalization forms the third pillar of technological advancement, consolidating control and monitoring capabilities. Modern systems are increasingly equipped with integrated IoT sensors, communication gateways (supporting protocols like Ethernet/IP and Profibus), and cloud connectivity. This allows for real-time monitoring of operational parameters, facilitating predictive maintenance powered by AI and enabling remote diagnostics. The integration of smart controllers not only manages the individual compressor or pump unit but also coordinates entire networks of machines in a centralized air or vacuum management system, optimizing system-wide performance and ensuring optimal pressure consistency across the manufacturing floor. This technological convergence is shifting equipment from isolated mechanical assets into intelligent, networked components of the broader industrial ecosystem.

The global Compressors and Vacuum Pumps Market exhibits significant regional variations influenced by industrial maturity, regulatory frameworks, and infrastructural investment cycles. North America, characterized by high automation levels and stringent energy efficiency regulations, represents a mature market focused heavily on replacement demand, technological upgrades (VSD, oil-free), and substantial consumption from the large oil and gas, aerospace, and advanced manufacturing sectors. The regional focus is on minimizing lifecycle costs, driving the demand for premium, highly efficient systems and sophisticated aftermarket service contracts. The expanding shale gas operations and significant investment in data centers further stabilize demand for specialized compressors and high-throughput vacuum pumps, respectively.

Europe mirrors North America in its focus on energy efficiency, heavily influenced by the EU’s Ecodesign Directives and Net Zero carbon targets. The market here is defined by high adoption rates of dry vacuum solutions and VSD compressors in the automotive, chemical, and pharmaceutical industries. Furthermore, Europe is rapidly developing its hydrogen infrastructure, which creates immediate demand for specialized hydrogen compression technology. While growth rates are steady, the market is characterized by high technological penetration and strong local manufacturing bases, making it a critical region for innovation and standard setting.

Asia Pacific (APAC) stands out as the undisputed leader in terms of market growth, driven by massive government initiatives supporting manufacturing expansion in China, India, and Southeast Asian nations. The region is undergoing rapid industrialization and urbanization, leading to high greenfield investment across general manufacturing, textiles, infrastructure, and electronics. APAC is the world’s hub for semiconductor production, fueling explosive demand for turbomolecular and dry screw vacuum pumps. While price sensitivity remains a factor in general industry applications, the scale of expansion ensures that APAC remains the epicenter of volume growth for both standard and high-end compression and vacuum equipment through the forecast period.

The shift is driven primarily by increasingly stringent quality control standards in sensitive industries like pharmaceuticals, food and beverage, and electronics manufacturing, where product contamination by oil residue is unacceptable. Furthermore, oil-free systems offer lower maintenance costs and support environmental sustainability goals by eliminating oil disposal requirements.

VSD technology is a major driver of market growth because it allows the compressor’s motor speed to dynamically match the air demand, leading to significant energy savings (often 20-35%). With global mandates emphasizing industrial energy efficiency and rising electricity costs, VSD compressors offer a compelling return on investment, accelerating replacement cycles.

The Electronics and Semiconductor manufacturing sector provides the strongest growth opportunity. The fabrication of microchips and flat-panel displays requires extremely high vacuum levels and ultra-clean environments, necessitating continuous investment in advanced, low-vibration dry screw and turbomolecular pumps.

Industry 4.0 integration, through IoT sensors and cloud connectivity, enables predictive maintenance and real-time operational optimization. This results in reduced unplanned downtime, lower total cost of ownership (TCO), and the development of new revenue streams for manufacturers via service-based models like Equipment-as-a-Service (EaaS).

Yes, the rapidly emerging hydrogen economy significantly influences demand. Hydrogen production, storage, and transportation require specialized high-pressure, multi-stage compressors designed to handle hydrogen's unique molecular properties safely and efficiently, creating a new, high-growth niche market segment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.