ID : MRU_ 431861 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

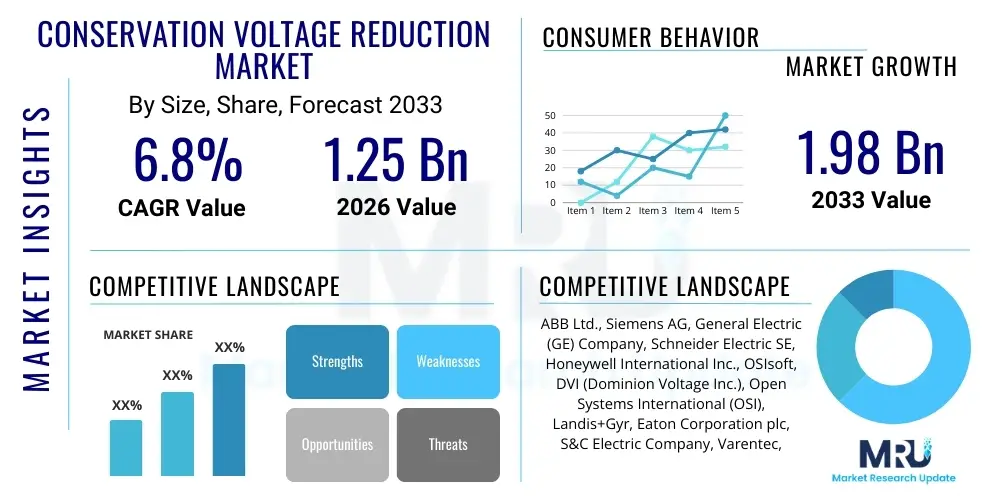

The Conservation Voltage Reduction Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 1.98 Billion by the end of the forecast period in 2033.

The Conservation Voltage Reduction (CVR) market encompasses technologies and strategies deployed by utility companies to systematically manage and optimize distribution voltage levels, thereby reducing energy consumption and peak demand across the grid. CVR leverages advanced smart grid infrastructure, including Supervisory Control and Data Acquisition (SCADA) systems, Advanced Metering Infrastructure (AMI), and specialized voltage regulators and capacitor banks, to ensure that the delivered voltage remains within the lower permissible range established by regulatory standards (e.g., ANSI C84.1), while still satisfying consumer minimum voltage requirements. This reduction in voltage translates directly into proportional savings in energy consumption for end-users, particularly for voltage-dependent loads such as resistive heating, lighting, and certain motor applications. The deployment of CVR is increasingly seen as a cost-effective and immediate means of achieving energy efficiency goals and deferring expensive capital investments in generation capacity or grid expansion.

CVR systems are crucial components of modern Distribution Management Systems (DMS) and are foundational to the concept of Volt/VAR Optimization (VVO). These solutions are deployed across various major applications, including load management, power quality enhancement, and grid reliability improvements. For utilities, the primary benefits derived from CVR adoption include significant reductions in technical line losses, extended equipment lifetime due to lower operational stress, and enhanced grid stability. Furthermore, CVR programs often qualify for governmental incentives and regulatory mandates focused on energy conservation, providing a strong financial impetus for their implementation. The integration of centralized and decentralized control architectures allows utilities to tailor CVR strategies to specific feeder characteristics and rapidly adapt to dynamic load changes and distributed energy resource (DER) penetration.

Key driving factors propelling the Conservation Voltage Reduction market include stringent governmental regulations aimed at improving grid efficiency and reducing carbon footprints, coupled with the rapid global adoption of smart grid technologies. The rising cost of electricity generation and the imperative to maximize the efficiency of existing aging infrastructure further necessitate CVR deployment. Moreover, the increasing integration of intermittent renewable energy sources requires advanced grid controls like CVR to maintain voltage stability and power quality across increasingly complex distribution networks. The demonstrated ability of CVR to deliver measurable and verifiable energy savings positions it as an essential tool for utility decarbonization and operational excellence initiatives.

The Conservation Voltage Reduction market demonstrates robust growth driven by utility investment in grid modernization, specifically the convergence of VVO/CVR solutions with advanced analytics and sensor technologies. Business trends indicate a strong shift towards software-as-a-service (SaaS) models for complex grid management systems, enabling utilities to adopt CVR capabilities without massive upfront capital expenditure on proprietary hardware. Furthermore, there is a distinct trend of integrating CVR protocols with Distributed Energy Resource Management Systems (DERMS), allowing voltage optimization efforts to account for two-way power flow caused by solar PV installations and battery storage systems. The market is increasingly characterized by strategic partnerships between traditional equipment manufacturers (providing regulators and capacitor banks) and specialized software providers (offering optimization algorithms and control platforms), focusing on creating unified, end-to-end grid efficiency solutions.

Regional trends highlight North America and Europe as established leaders in CVR adoption, primarily due to well-defined regulatory frameworks that mandate energy efficiency targets and provide performance-based incentives for utilities implementing CVR. The North American market is highly mature, characterized by ongoing replacement cycles and the integration of CVR with existing robust AMI infrastructures. Conversely, the Asia Pacific (APAC) region is experiencing the highest growth rate, driven by massive urbanization, subsequent rapid expansion of electricity grids, and the necessity to manage high peak loads efficiently, especially in densely populated emerging economies like India and China. Regulatory push for smart city development and grid resilience following extreme weather events is accelerating CVR deployment across APAC.

Segment trends emphasize the escalating importance of the Software component segment, which includes sophisticated optimization engines, data processing platforms, and predictive analytics tools necessary for real-time voltage management. While the Hardware segment (regulators, transformers, capacitors) remains foundational, its growth is steadier, focusing on smart, connected devices compatible with modern communication standards. Utility companies represent the dominant End-User segment, holding substantial market share due to their direct responsibility for distribution network operation and maintenance. The growing complexity of integrating CVR into decentralized deployment models, which allow for localized optimization efforts on smaller distribution feeders, is also a notable trend enhancing system responsiveness and reliability.

User queries regarding the impact of Artificial Intelligence (AI) on Conservation Voltage Reduction predominantly center on AI's ability to enhance the precision, predictability, and real-time adaptability of CVR systems, moving beyond traditional rule-based or static optimization models. Users often question how machine learning can handle the volatility introduced by high penetration of Distributed Energy Resources (DERs), which traditional CVR struggled to manage effectively. Key concerns revolve around data requirements for training reliable AI models, the cybersecurity risks associated with highly autonomous control systems, and the verifiable accuracy of predicted energy savings. Expectations are high regarding AI's potential to provide true predictive VVO, minimize operational voltage violations, and dynamically adjust CVR actions based on granular load forecasts and weather patterns, thereby maximizing energy savings while guaranteeing customer quality of service (CoS).

AI significantly transforms CVR implementation by migrating control schemes from reactive or heuristic methods to proactive, predictive optimization frameworks. Machine learning algorithms, particularly reinforcement learning, are used to train the system based on historical grid data, real-time sensor inputs, and external factors like weather and localized demand forecasts. This allows the CVR system to accurately model the complex relationships between voltage adjustments and resultant load reductions, optimizing control settings across hundreds of nodes simultaneously. This enhanced capability ensures that voltage reduction is maximized without violating the lower voltage constraints for any customer on the feeder, a challenge that manual or simpler optimization techniques often fail to consistently address across dynamic grid conditions.

Furthermore, AI-driven analytics enhance the maintenance and fault detection aspects of CVR implementation. AI can analyze performance data from voltage regulators and capacitor banks to predict potential equipment failures before they occur, shifting maintenance strategies from reactive to predictive maintenance. This improves grid reliability and reduces operational costs. The integration of AI also facilitates the seamless coordination of CVR with other grid functions, such as fault location, isolation, and service restoration (FLISR), and provides superior situational awareness to utility operators. By rapidly processing vast datasets generated by AMI and SCADA, AI ensures that CVR becomes a dynamic tool that adapts instantly to grid topology changes, maximizing energy efficiency across the distribution network hour by hour.

The Conservation Voltage Reduction market is fundamentally influenced by a complex interplay of regulatory drivers, economic restraints, technological opportunities, and critical impact forces shaping utility investment cycles. The primary driver is the global regulatory impetus toward mandated energy efficiency and carbon emissions reduction targets, compelling utilities to adopt proven technologies like CVR to demonstrate measurable savings. The immediate and quantifiable reduction in technical line losses offers a significant financial benefit, providing a substantial operational leverage. However, market adoption is restrained by the high initial capital investment required for deploying advanced sensors, communication infrastructure, and sophisticated control software, particularly in older distribution networks lacking smart grid foundations. Furthermore, ensuring customer confidence regarding consistent power quality and avoiding voltage sags or flickering during peak CVR operations requires stringent testing and validation, acting as a functional restraint on aggressive voltage reduction targets.

Opportunities in the CVR market are strongly linked to the ongoing convergence of IT and Operational Technology (OT) within the utility sector. The exponential increase in data generated by AMI rollout creates vast potential for advanced data analytics and AI integration to refine CVR algorithms, transforming static programs into dynamic, predictive systems. The rise of microgrids and localized energy optimization presents an opportunity for CVR solutions tailored to smaller, localized distribution systems. Moreover, CVR offers a compelling non-wires alternative (NWA) for utilities facing capacity constraints in rapidly growing areas, deferring or eliminating the need for expensive substation upgrades. The market benefits from the standardization of communication protocols, which lowers integration costs and allows for greater interoperability among components from different vendors, opening up opportunities for specialized software vendors.

The impact forces driving the current market dynamics are centered on environmental and technological shifts. The increasing frequency of extreme weather events necessitates grid hardening and resilience improvements; CVR contributes by reducing stress on transmission and distribution equipment. Technologically, the rapid proliferation of solar PV and electric vehicles (EVs) introduces highly dynamic load and generation profiles that fundamentally challenge traditional centralized voltage control. This forces utilities to rapidly invest in advanced CVR/VVO solutions capable of managing bi-directional power flow and localized voltage fluctuations. Economically, the move toward performance-based regulation (PBR) models encourages utilities to invest in efficiency measures like CVR, as their returns are directly tied to achieved savings and reliability metrics, thereby solidifying CVR's position as a critical investment for modern power distribution infrastructure.

The Conservation Voltage Reduction market segmentation provides a comprehensive breakdown based on Component, Deployment Type, and End-User, illustrating the diverse technologies and application areas driving market growth. The Component segmentation distinguishes between the foundational hardware required for physical voltage manipulation (regulators, capacitor banks, sensors), the critical software necessary for optimization, control, and data analytics (DMS/VVO platforms, AI engines), and the requisite services (consulting, integration, maintenance) essential for successful CVR implementation. This segmentation highlights the high growth trajectory within the software and services segments as utilities prioritize advanced analytics and robust support over pure hardware procurement.

Segmentation by Deployment Type examines the architectural approach taken by utilities to implement CVR. Centralized deployment, traditionally utilizing SCADA or DMS systems to manage voltage setpoints across large feeders from a single control center, remains dominant, particularly in established networks. However, the rapidly emerging Decentralized deployment model, often leveraging intelligent electronic devices (IEDs) and localized controllers (such as smart regulators and advanced capacitor bank controls) at the distribution level, is gaining traction. Decentralized approaches offer superior response times and better management of local voltage issues, particularly relevant in grids with high DER penetration.

Finally, the End-User analysis focuses on the entities benefiting from and driving the adoption of CVR technology. Utility companies, including Investor-Owned Utilities (IOUs), Municipal Utilities, and Rural Electric Cooperatives, represent the largest segment due to their direct responsibility for grid operation, loss reduction, and regulatory compliance. While CVR primarily operates at the utility distribution level, the energy savings ultimately benefit Residential, Commercial, and Industrial end-users. Increased efficiency demands and high energy consumption in the Commercial and Industrial sectors, coupled with regulatory incentives, drive the measurable impact and justification for utility CVR investments.

The value chain of the Conservation Voltage Reduction market initiates with the upstream analysis, which is dominated by raw material suppliers and manufacturers of core electrical components. This phase involves the procurement of highly specialized materials for transformers, voltage regulators, and capacitor banks, requiring advanced manufacturing capabilities focused on precision, durability, and integration compatibility with smart grid components. Key upstream players are large electrical equipment conglomerates that invest heavily in R&D to produce intelligent field devices (IFDs) that can communicate effectively with centralized or decentralized control systems. The quality and intellectual property associated with these core components form the foundational layer of CVR system performance and reliability.

Moving downstream, the value chain shifts focus towards system integration, software development, and specialized services. This crucial stage involves integrating disparate hardware components—ranging from legacy SCADA systems to newly installed AMI—with VVO/CVR software platforms. System integrators and utility IT departments play a pivotal role in customizing algorithms to match specific feeder topologies and regulatory requirements. The distribution channel is predominantly direct, where large utilities contract directly with major equipment providers (OEMs) or specialized software vendors. However, there is a growing role for indirect channels, specifically third-party energy consultants and professional service firms that provide feasibility studies, cost-benefit analyses, and post-implementation performance validation, thereby facilitating technology adoption by smaller utility cooperatives and municipal services.

The final stage encompasses the deployment, operationalization, and continuous optimization of the CVR system. Once installed, the system requires ongoing maintenance, software updates, and rigorous performance monitoring to ensure the conservation voltage effect (CVE) is maintained over time. Direct engagement between the utility and the CVR solution provider is paramount for addressing potential operational challenges, managing cybersecurity risks, and refining optimization strategies based on changing load patterns or increased DER penetration. The efficacy of the entire value chain is measured by the verifiable energy savings delivered to the utility, emphasizing the need for robust data acquisition and analytics capabilities at the downstream end.

The primary and most significant customer segment in the Conservation Voltage Reduction market consists of electricity distribution utility companies globally. This includes Investor-Owned Utilities (IOUs), which operate large regional grids and possess the substantial capital necessary for comprehensive smart grid deployments; Municipal Utilities, which are often focused on serving localized city jurisdictions and prioritize localized reliability and cost control; and Rural Electric Cooperatives, which manage extensive distribution networks over vast, often sparsely populated territories where line loss reduction is a critical economic priority. These utility operators are the direct purchasers of CVR hardware, VVO software platforms, and related integration services, driven by the dual goals of regulatory compliance (meeting energy savings mandates) and operational efficiency (reducing technical line losses and deferring infrastructure investments).

Secondary potential customers include large energy consumers in the Commercial and Industrial (C&I) sectors, although their procurement typically focuses on localized voltage optimization equipment rather than full-scale CVR platforms for the distribution network. C&I facilities that generate their own power or operate sophisticated manufacturing processes often utilize localized power conditioning and voltage optimization equipment to ensure operational consistency and energy efficiency within their specific site boundaries. While they are not direct buyers of the utility-scale CVR solutions, their demand for stable and optimized voltage indirectly influences utility adoption, particularly when energy saving regulations target large commercial consumers.

Furthermore, government energy agencies and regulatory bodies act as influential facilitators and indirect customers. While not purchasing the technology themselves, their mandates, incentive structures, and grid modernization programs create the mandatory environment and financial rationale for utilities to adopt CVR technologies. Energy Service Companies (ESCOs) and specialized engineering consulting firms also serve as key intermediaries, often partnering with utilities to implement CVR projects and offering performance-based contracts, thereby effectively acting as agents for the technology deployment and assuring the return on investment for the ultimate utility buyer.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 1.98 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, General Electric (GE) Company, Schneider Electric SE, Honeywell International Inc., OSIsoft, DVI (Dominion Voltage Inc.), Open Systems International (OSI), Landis+Gyr, Eaton Corporation plc, S&C Electric Company, Varentec, Inc., OATI, Utilidata, NovaTech LLC, Advanced Control Systems (ACS), Tesla, Inc. (Powerwall/Grid), Cisco Systems, Inc., Oracle Corporation (Utilities Global Business Unit), Schweitzer Engineering Laboratories (SEL) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Conservation Voltage Reduction market is dominated by the convergence of operational hardware and highly sophisticated software platforms, forming the backbone of Volt/VAR Optimization (VVO) systems. At the core are intelligent field devices (IFDs), including smart distribution transformers, advanced pole-mounted and substation voltage regulators, and switched capacitor banks. These devices are crucial as they perform the physical manipulation of voltage and reactive power. The latest hardware generations feature integrated communication capabilities (often utilizing protocols like DNP3 or IEC 61850) and local intelligence, enabling them to execute commands from centralized control systems and perform localized, autonomous adjustments, which is foundational for decentralized CVR deployment models.

The critical technology differentiator in the CVR market is the VVO software platform, often integrated within a larger Distribution Management System (DMS). These platforms utilize complex mathematical models and optimization algorithms to determine the optimal voltage setpoints for distribution feeders, aiming to maximize energy savings while adhering strictly to statutory voltage limits across all customer service points. Key technological advancements include the incorporation of Advanced Metering Infrastructure (AMI) data for granular, real-time feedback on voltage levels at the customer premise, allowing for highly accurate voltage modeling. Furthermore, the integration of geographical information systems (GIS) data and topological models allows the software to accurately map the impedance and voltage drop characteristics of the entire distribution network, providing the necessary context for precision control.

The emerging frontier in CVR technology involves the application of Artificial Intelligence (AI) and machine learning (ML) to enhance optimization. Traditional CVR uses static rules or pre-calculated settings. Modern systems employ ML to predict load changes, generation fluctuations (from DERs), and transformer tap wear, enabling predictive control. This allows the system to proactively adjust voltage setpoints minutes or hours in advance, maximizing the duration and depth of conservation while mitigating risks of low voltage events. Cloud-based or edge computing solutions are also gaining prominence, facilitating faster data processing and localized decision-making, which is paramount for maintaining grid stability in highly complex, modern distribution environments subject to two-way power flow.

Regional dynamics play a crucial role in shaping the Conservation Voltage Reduction market, largely driven by varying levels of smart grid maturity, regulatory environments, and specific grid modernization objectives. North America, particularly the United States and Canada, represents a leading and mature market. This dominance is attributable to early and sustained utility investment in smart grid infrastructure, extensive AMI coverage, and regulatory frameworks, such as those established by state Public Utility Commissions (PUCs), which often mandate CVR/VVO implementation as part of utility performance targets. Utilities in this region utilize CVR extensively to manage summer peak demands, reduce transmission congestion, and adhere to efficiency portfolio standards. The market here is characterized by sophisticated integration challenges, often focusing on optimizing CVR performance in high DER penetration areas, necessitating continuous algorithm refinement and technology upgrades.

Europe demonstrates steady growth, driven primarily by the European Union's ambitious climate and energy efficiency targets (e.g., the "Fit for 55" package) and the widespread deployment of smart meters across member states. Countries such as Germany, the UK, and France are actively leveraging CVR technologies to minimize network losses, which is a major focus under EU energy mandates. The European market emphasizes interoperability and compliance with stringent cyber security standards, given the high level of grid interconnection. Furthermore, the high density of renewable energy sources in Northern European countries requires CVR solutions that can rapidly mitigate voltage fluctuations caused by solar and wind variability, often integrated into holistic grid flexibility platforms.

Asia Pacific (APAC) is projected to be the fastest-growing region for CVR adoption. Rapid industrialization, explosive urbanization, and the consequent surge in electricity demand necessitate urgent improvements in grid efficiency and reliability across countries like China, India, and South Korea. While the initial smart grid adoption rate varies, governmental initiatives aimed at building resilient and efficient power systems (e.g., India's Smart Grid Mission) are fueling large-scale investment in CVR pilots and deployments. The APAC market presents significant opportunities for centralized CVR due to the high density of traditional distribution networks, but also requires robust decentralized solutions to manage burgeoning distributed generation, particularly in rural and remote electrification projects.

CVR is a smart grid strategy that systematically lowers the operational voltage on distribution feeders to the lowest practical level within regulatory standards (typically ANSI C84.1). Energy savings are achieved because many loads (e.g., lighting, resistive heaters) consume less power at lower voltages, resulting in verifiable system-wide conservation effects and reduced line losses.

CVR is specifically the function of reducing energy consumption by minimizing feeder voltage. VVO is the broader, integrated approach that optimizes both voltage (Volt) and reactive power (VAR) management simultaneously. CVR is often considered a key operational outcome or specific objective within a comprehensive VVO program, aiming for efficiency and loss reduction.

DERs, such as rooftop solar, introduce volatility and bi-directional power flow, making static CVR challenging. Modern CVR systems must integrate advanced VVO software, often leveraging AI/ML, to dynamically manage these fluctuations, ensuring voltage remains stable despite intermittent local generation while maximizing conservation opportunities.

Essential components include intelligent voltage regulators and capacitor banks for physical control; Advanced Metering Infrastructure (AMI) for granular voltage measurement feedback; a robust communications network; and sophisticated VVO/DMS software platforms, increasingly incorporating AI for predictive optimization and real-time control decision-making.

While CVR can be implemented in stages, achieving its full potential (dynamic, real-time control) requires significant investment in foundational smart grid infrastructure, especially smart meters and communications systems. Utilities with legacy systems often start with basic, centralized CVR using existing substations and then incrementally deploy smart sensors and modern software.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.