ID : MRU_ 438641 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

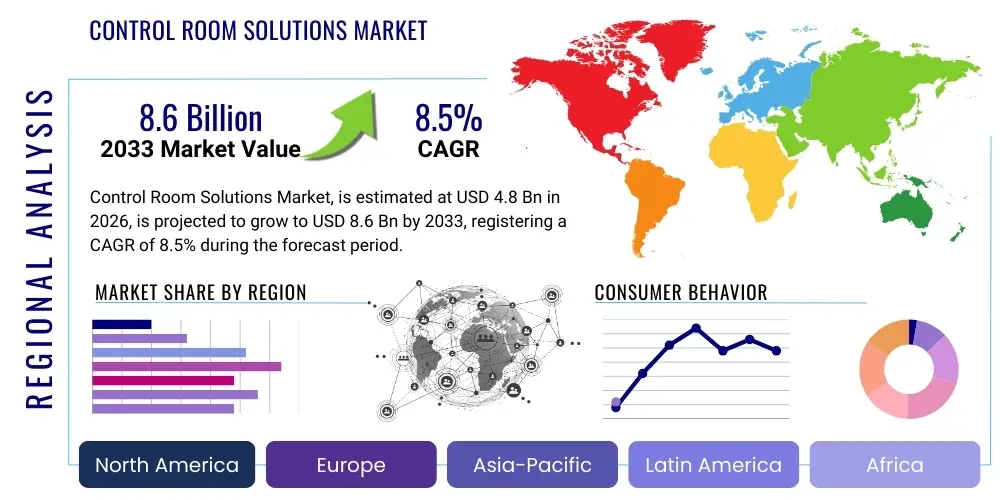

The Control Room Solutions Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 8.6 Billion by the end of the forecast period in 2033.

The Control Room Solutions Market encompasses a highly sophisticated and technologically critical segment of the enterprise and governmental infrastructure domain, focusing on the integration of disparate systems to achieve unified operational oversight, command, and control within mission-critical environments. These solutions are not merely collections of display technologies but represent comprehensive ecosystems comprising specialized hardware, robust software platforms, and professional services, all designed to facilitate efficient data aggregation, real-time visualization, and accelerated collaborative decision-making. The core purpose of control room solutions is to transform vast streams of operational data—originating from industrial sensors, surveillance cameras, network traffic logs, and geopolitical intelligence feeds—into actionable intelligence displayed through ergonomic consoles and high-resolution video walls. This unified operational picture is essential for maintaining situational awareness, particularly in environments where operational continuity, public safety, and infrastructure resilience are paramount, such as in national defense, power grid management, and emergency services.

The product portfolio within this market is diverse and complex, spanning hardware components like ultra-narrow bezel display panels, high-performance video wall controllers utilizing advanced graphics processing units, specialized KVM (Keyboard Video Mouse) extension and switching systems designed for zero-latency performance, and ergonomically engineered operator consoles optimized for 24/7 use. On the software side, the offerings include sophisticated visualization platforms, Command and Control (C2) software suites that enable dynamic workflow automation and incident management, and data management tools capable of normalizing and correlating real-time information from multiple proprietary sources, including SCADA, DCS, and enterprise resource planning (ERP) systems. Major applications are concentrated across sectors defined by high complexity and stringent reliability requirements, including Network Operations Centers (NOCs) for telecommunications, Security Operations Centers (SOCs) for cybersecurity monitoring, Process Control Rooms in manufacturing and energy, and Traffic Management Centers (TMCs) for urban mobility oversight. The robust functionality offered by these integrated solutions provides immense benefits, substantially reducing operational downtime, minimizing human error through centralized monitoring, accelerating critical incident response times, and ensuring overall adherence to safety and compliance mandates.

Market expansion is fundamentally driven by several powerful macro-trends. Firstly, the global shift towards digitalization and the resulting explosion in operational data volume and velocity, often termed Big Data in operational contexts, necessitates advanced real-time visualization capabilities that only modern control rooms can provide. Secondly, governmental focus on modernizing critical national infrastructure, including smart grid deployment and advanced public safety networks (e.g., Next-Generation 911), creates sustained demand for state-of-the-art C2 capabilities. Thirdly, the increasing interconnectedness of industrial control systems (ICS) and IT networks exposes operational environments to sophisticated cyber and physical threats, compelling organizations across finance, energy, and defense to upgrade to integrated control room solutions that offer converged security and operational monitoring capabilities. Finally, technological advancements, such as the maturation of 4K and 8K display technologies, IP-based KVM systems offering superior flexibility, and the integration of AI-powered analytics for predictive insights, are constantly refreshing the demand cycle, prompting organizations to replace outdated or fragmented control room infrastructure with unified, future-proof platforms, thereby ensuring sustained market momentum.

The Control Room Solutions Market trajectory is characterized by key technological convergences and strong regional growth disparities. A dominant business trend is the transition from hardware-centric systems to flexible, software-defined control room architectures, facilitating greater scalability, interoperability, and virtualization of core functions like video processing and KVM switching. Organizations are prioritizing modularity, allowing them to scale display elements and operational capacity without undergoing full infrastructure overhauls. Furthermore, there is a pronounced shift towards incorporating human factors engineering principles into control room design, optimizing console layouts, lighting, acoustics, and software interfaces to minimize cognitive load on 24/7 operators, thereby maximizing accuracy and efficiency. Strategic alliances between display manufacturers, software developers, and specialized systems integrators are essential in delivering complex, customized solutions that meet the highly specific needs of mission-critical environments, promoting a business model focused on total lifecycle support rather than single product sales.

Regionally, the market exhibits a clear bifurcation between mature adoption and high-growth potential. North America maintains its leadership position, underpinned by high spending in national defense, homeland security, and sophisticated corporate sectors, ensuring continuous upgrades and investment in cutting-edge technologies like advanced visualization software and secure command platforms. Europe follows, characterized by steady demand driven by environmental regulations, infrastructure modernization, and a strong emphasis on industrial automation and process control rooms that adhere to stringent safety standards. Conversely, the Asia Pacific (APAC) region is forecasted to achieve the highest CAGR, propelled by unprecedented levels of urbanization and governmental investment in smart city infrastructure, transportation networks, and new energy projects, particularly in rapidly industrializing nations. This growth is largely concentrated in greenfield deployments, where opportunities for deploying fully IP-integrated solutions are maximized, contrasting with the brownfield integration challenges often faced in Western markets.

Segmentation analysis reveals the critical role of software and services in driving value creation. While hardware remains essential, the integrated Command and Control (C2) software segment is rapidly gaining market share, as end-users seek platforms that offer advanced features such as incident correlation, automated standard operating procedure (SOP) execution, and seamless integration with cyber security tools. Within the application vertical, the Utilities and Energy sector continues to represent the largest segment of demand, reflecting the critical necessity of real-time monitoring for power generation, transmission, and distribution assets to prevent widespread outages. Services, specifically system integration, specialized consulting, and long-term managed maintenance, are showing accelerating growth, driven by the complexity of advanced installations and the need for guaranteed system uptime. The shift towards hybrid and cloud-enabled control room components, particularly for non-mission-critical functions like remote access and data backup, suggests future market segmentation will increasingly differentiate based on deployment flexibility and cloud interoperability, allowing for greater geographical distribution of operational oversight and sustained profitability across the services lifecycle.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally reshaping the functional capabilities and strategic role of modern Control Room Solutions, shifting their operational paradigm from purely responsive to proactively predictive. User analysis reveals intense interest centered on AI’s capacity to handle the deluge of data generated by modern IoT, SCADA, and surveillance systems, seeking solutions that automatically filter out noise and highlight critical anomalies that human operators might miss due to cognitive overload. Specific questions frequently address the reliability and ethical governance of AI in high-stakes decisions, particularly concerning automated response initiation, and the training requirements necessary for operators to effectively interact with AI-augmented interfaces. The overarching expectation is that AI will dramatically enhance efficiency by automating routine data analysis, enabling far faster detection of emerging threats, whether they are network intrusions, equipment faults, or public safety incidents, thereby transforming the operator’s role into one focused on high-level decision review and strategic planning rather than continuous, minute-by-minute monitoring.

AI's primary influence manifests in the enhanced cognitive support it provides to operators and the automation it brings to data processing workflows. By leveraging advanced deep learning models, control room software can perform sophisticated pattern recognition on highly granular data, identifying subtle deviations indicative of potential system failure long before conventional threshold-based alarms are triggered. This capability, known as predictive operational intelligence, is vital in industrial control rooms for asset management and in utility control rooms for grid stability forecasting. Furthermore, AI tools are improving the efficiency of resource allocation; for instance, in traffic management centers, ML algorithms optimize signal timings based on real-time traffic flow analysis, or in emergency response centers, AI helps dispatchers prioritize and route response teams based on multi-source data fusion, optimizing speed and effectiveness during critical events. The implementation of AI is therefore not aimed at replacement, but rather at augmenting human capabilities, providing a level of foresight and analytical capacity previously unattainable within the confines of traditional control room technologies.

The technological adoption curve for AI within this market is steep, requiring significant investment in high-performance computing (HPC) infrastructure capable of executing ML models in real-time. Key market players are embedding AI directly into visualization software and video processors, creating 'intelligent endpoints' that preprocess data at the edge before it reaches the core control room display. This distributed intelligence architecture is crucial for managing network bandwidth and ensuring ultra-low latency necessary for mission-critical feedback loops. The successful integration of AI is contingent upon developing secure, transparent, and auditable algorithms, addressing user concerns regarding "black box" decision-making, especially in sensitive government and defense applications. As industry standards evolve to govern the use of operational AI, its pervasive integration will make predictive anomaly detection and automated incident workflow generation standard features, transforming control rooms into adaptive, self-optimizing operational hubs.

The Control Room Solutions market is inherently influenced by a powerful combination of driving forces rooted in technological necessity and operational resilience, balanced against significant cost and integration hurdles. The core drivers are unequivocally centered on the global necessity for increased operational security and efficiency across critical infrastructure domains. As industrial processes and national services become more digitized and interconnected, the vulnerability to catastrophic failure, either through cyberattacks or physical incidents, mandates the establishment of highly resilient, centralized control and monitoring capabilities. This imperative is amplified by the sheer scale of data generated by modern operational environments (IoT, sensors, smart devices), requiring sophisticated control room platforms capable of real-time processing and visualization that simple IT dashboards cannot manage. Opportunities, therefore, emerge in developing highly specialized software that can seamlessly fuse disparate data types, offering a competitive edge to vendors providing truly integrated operational intelligence platforms.

Specific drivers include the global phenomenon of smart city development, where municipal governments are consolidating services—from traffic management to public safety and utility control—into unified command centers, requiring massive investment in integrated video walls and common operational picture (COP) software platforms. Technological advancements further propel the market; the ongoing transition to IP-based infrastructure enables greater geographical flexibility and scalability in control room deployment, while the maturation of 4K/8K display technology necessitates upgrades to video processing hardware to handle ultra-high-resolution content. The increasing global regulatory scrutiny over critical infrastructure reliability and safety (e.g., pipeline monitoring regulations, power grid security mandates) compels sustained investment, often prioritizing redundancy, failover capabilities, and compliance features, reinforcing the necessity of high-reliability control room environments.

Restraints are primarily economic and logistical. The capital expenditure required for designing, procuring, and installing a state-of-the-art control room, including specialized furniture, high-performance display controllers, and proprietary software licenses, is substantial, often leading smaller organizations or entities in emerging markets to defer investments. The complexity of integration poses a significant barrier; integrating modern, IP-based solutions with diverse legacy operational technology (OT) systems—which often utilize older, proprietary communication protocols—requires highly specialized and expensive systems integration expertise. Furthermore, the specialized nature of control room operations requires continuous training and certification for technical support and operational staff, contributing to high operational expenditure (OpEx). Opportunities lie primarily in AI integration for predictive monitoring, the proliferation of managed services models, and expansion into high-growth APAC smart city initiatives. These forces combine to create a market characterized by high-value, long-lifecycle projects where reliability and integration complexity dictate vendor selection and project success.

The Control Room Solutions Market segmentation is highly intricate, reflecting the diversity of technological components, deployment methodologies, and specialized end-user requirements across numerous critical operational domains. The fundamental breakdown by Component is critical, clearly delineating between physical infrastructure (Hardware), the intellectual property driving functionality (Software), and the expertise required for deployment and sustainment (Services). Hardware segmentation includes highly specialized equipment such as large-format visualization systems (e.g., rear-projection cubes, LED walls), complex I/O modules, robust KVM matrices designed for extended performance, and ergonomic consoles optimized for human-centered design principles. Software segmentation encompasses the sophisticated C2 platforms that manage data flow, incident response protocols, and overall visualization layout, which are increasingly crucial as control rooms shift from simple monitoring to active command execution centers. Understanding these component layers is essential for vendors seeking to position themselves strategically, either as specialized hardware providers or comprehensive software platform providers.

Segmentation by Application focuses on the specific operational environment, revealing distinct feature requirements across verticals. For instance, Process Control Rooms (PCRs) in energy and manufacturing demand extreme reliability, deep integration with SCADA/DCS systems, and strict adherence to industrial communication standards, often favoring highly redundant on-premise solutions. Conversely, Network Operations Centers (NOCs) and Security Operations Centers (SOCs) require dynamic scalability, support for complex IP video streams, rapid data correlation capabilities, and seamless integration with IT service management (ITSM) platforms, increasingly leveraging hybrid or cloud-enabled visualization layers. Emergency Response Centers (ERCs) and Traffic Management Centers (TMCs) require robust GIS integration, collaborative incident mapping tools, and resilient communication links. This functional differentiation drives specific requirements for latency performance, data density handling, and the level of automation embedded within the solution, ensuring that specialized solutions cater precisely to the unique operational pressures of each application domain.

The segmentation by Vertical reinforces the differentiated demand patterns across major industries. The Oil and Gas sector requires solutions capable of managing highly distributed assets, often in harsh environments, necessitating ruggedized KVM and visualization systems for remote monitoring of pipelines and refineries. Government and Defense entities demand solutions with the highest levels of security accreditation, favoring customized, often proprietary, C4I (Command, Control, Communications, Computers, and Intelligence) software integrations and requiring physical separation (air gaps) or highly secure KVM solutions. The Services segment, comprising consulting, integration, and managed services, is witnessing transformative growth as end-users increasingly prefer outsourcing the complexity of system lifecycle management, including routine maintenance, rapid software patching, and future capacity planning, to specialized third-party providers. This trend signifies a recognition that the core competence of organizations lies in operating their critical assets, not necessarily in managing the intricate technology ecosystem of the control room itself, creating sustained, high-margin revenue opportunities for service providers.

The upstream segment of the Control Room Solutions value chain is dedicated to the complex manufacturing and supply of highly specialized core components that dictate the performance and longevity of the final system. This includes manufacturers of high-fidelity, high-brightness LCD, LED, and DLP display panels optimized for 24/7 operation without degradation or burn-in, often requiring specialized cooling and calibration systems. Suppliers of critical computing hardware—such as specialized GPUs and capture cards for video wall controllers, along with advanced chipsets for low-latency KVM extension—form the technological foundation. Material sourcing for ergonomic technical furniture, which must be durable, modular, and capable of integrating complex cable management and power systems, is also integral to this stage. The quality, reliability, and guaranteed availability of these upstream components are paramount, as failure in any single part can compromise the functionality of the entire mission-critical control room, necessitating rigorous quality control and specialized supply chain partnerships.

The midstream is the most value-intensive stage, defined by systems integration and software development. Core technology providers develop proprietary C2 software, visualization middleware, and patented KVM protocols. System Integrators (SIs) and Value-Added Resellers (VARs) then take these components, along with third-party products (e.g., communication systems, access control), and design a bespoke control room environment tailored to the client's operational workflow, regulatory compliance needs, and physical space constraints. This stage involves sophisticated project management, architectural design consultation (including adherence to ISO 11064 standards for ergonomic control center design), custom fabrication of consoles, and complex networking configuration to ensure all data sources—from SCADA to IP cameras—are seamlessly aggregated and displayed in a unified operational picture. The expertise of the SI is critical here, as success depends on managing interoperability and redundancy across dozens of hardware and software interfaces under strict performance mandates.

The downstream segment encompasses the distribution, installation, and ongoing support phases. Distribution occurs via a dual structure: direct sales channels are employed for large government contracts and critical infrastructure projects where security and complexity demand direct vendor engagement, while specialized regional VARs handle smaller industrial or regional public safety installations. Crucially, the long-term profitability of this market relies heavily on the quality and responsiveness of the post-sales service structure. Control rooms require continuous technical support, rapid incident response, guaranteed Service Level Agreements (SLAs) for system uptime, and periodic hardware and software refreshes. Therefore, the downstream value chain generates substantial recurring revenue through long-term maintenance contracts, training services for new operators, and consulting on future capacity expansion. Reliable service delivery ensures customer loyalty and minimizes the high risk associated with system failure in mission-critical environments.

Potential customers for Control Room Solutions are organizations operating critical, complex, and high-stakes infrastructure that require centralized, real-time command, monitoring, and decision-making capabilities to ensure safety, security, and operational efficiency. The primary buyers fall into sectors categorized by high asset value, strict regulatory requirements, and the catastrophic potential impact of operational failure. This includes national and regional utilities, such as electricity transmission system operators and water purification plants, which must constantly monitor SCADA systems and distributed network assets. Government entities, particularly defense ministries, intelligence agencies, and public safety organizations (police, fire, emergency medical services), require sophisticated command centers for disaster coordination and security oversight, acting as major consumers of advanced C2 (Command and Control) software and video wall technology.

In the private sector, major end-users include large-scale industrial operators in the oil and gas sector, particularly for pipeline monitoring and offshore platform control; petrochemical processing facilities; and large-scale discrete and process manufacturing plants that rely on centralized control rooms for continuous operation and quality management. Telecommunications companies (Telcos) and major IT service providers are significant buyers, utilizing these solutions for Network Operations Centers (NOCs) to manage network traffic, capacity, and incident response across their global infrastructure. Furthermore, the transportation sector, encompassing air traffic control, rail network management, and metropolitan traffic control centers, consistently invests in control room technology to optimize flow, enhance security, and mitigate congestion, representing a continuous demand driver for systems capable of real-time multi-modal data integration and visualization.

Emerging customers include hyperscale data center operators who require highly resilient and centralized monitoring centers for power, cooling, and security management; and the rapidly expanding smart city initiatives globally, which integrate multiple operational domains—traffic, public safety, utilities—into unified municipal command centers. These new customer segments often demand highly scalable, cloud-integrated, and software-centric control room solutions that can adapt quickly to evolving technological standards and urban planning requirements. The complexity and mission-critical nature of these operations ensure that the procurement process is often high-value, long-term, and focuses heavily on vendor reliability, system redundancy, and proven integration capabilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.6 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Barco, Christie Digital Systems USA Inc., Datapath Limited, Mitsubishi Electric Corporation, EIZO Corporation, Black Box Corporation, VuWall Technology Inc., Eyevis GmbH (Leyard), RGB Spectrum, Planar Systems (Leyard), ABB Ltd., Siemens AG, Honeywell International Inc., Motorola Solutions Inc., General Dynamics Corporation, KVM-TEC GmbH, Winsted Corporation, Control Room Consoles, Matrox Graphics Inc., Guntermann & Drunck GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution defining the Control Room Solutions Market is primarily centered on achieving ubiquitous IP connectivity, ultra-high resolution visualization, and enhanced computational efficiency. The display technology landscape is dominated by the maturity of narrow-bezel LCD and fine-pitch LED video walls, which offer superior brightness, lifespan, and seamless visuals compared to legacy rear-projection cubes, although RPVs maintain a presence in specific high-security or large-scale control environments. Crucially, the underlying infrastructure relies on advanced video wall controllers and display processors, which are increasingly migrating from traditional proprietary bus architectures to highly scalable, software-defined IP streaming and decoding platforms. This technological transition allows control rooms to ingest massive amounts of data from distributed sources (e.g., thousands of IP cameras, geographically dispersed sensors) and render them synchronously onto large visualization surfaces with imperceptible latency, supporting distributed operational models across vast geographical areas.

A second pivotal technology is the widespread adoption of high-performance, secure IP-based KVM (Keyboard Video Mouse) extension and switching systems. Traditional matrix KVM systems, while reliable, lacked scalability and flexibility. Modern IP-KVM solutions overcome these limitations by allowing operators to instantaneously access and control any number of physical or virtual machines located potentially hundreds of miles away via standard network infrastructure, all while maintaining a near-local user experience (zero compression, zero latency 4K video transmission). This capability dramatically improves physical control room ergonomics by allowing all noisy, heat-generating computing assets to be centralized in a secure data center, reducing operator fatigue and increasing the physical security of sensitive computing hardware. Furthermore, advanced KVM solutions now incorporate robust cybersecurity features, including encrypted transmission and multi-factor authentication, essential for protecting access to mission-critical systems in defense and utility control rooms.

The software layer is becoming the primary differentiator, with Command and Control (C2) software platforms integrating sophisticated operational intelligence capabilities. These platforms utilize advanced data connectors (e.g., REST APIs, proprietary industrial protocols) to achieve true OT/IT convergence, normalizing data from disparate systems (SCADA, BIM, ERP, physical security). Key features include dynamic visualization generation based on the nature of the incoming alert, AI-driven correlation of incident data to identify root causes faster, and automated scripting tools for standardized, compliant response execution. The emergence of virtualization technology, allowing the control room’s functional displays and core applications to run on virtual machines, further enhances system redundancy and simplifies disaster recovery, ensuring that even if physical control room hardware fails, the operational functionality can be rapidly transferred or replicated, maintaining maximum operational resilience and supporting the critical move toward remote and hybrid operational models for future control center design.

The Control Room Solutions Market is projected to exhibit a steady Compound Annual Growth Rate (CAGR) of 8.5% between the forecast years of 2026 and 2033, driven primarily by ongoing critical infrastructure digitization and escalating operational security requirements across vital sectors.

The highest market demand, outside of basic display components, is concentrated in advanced Visualization Software and high-performance, flexible IP-based KVM systems, which are essential for seamless data aggregation, secure remote access, and real-time visualization of complex, multi-source operational data streams with minimal latency.

AI is transforming the operator role by automating routine data analysis, enabling predictive maintenance, and facilitating automated incident triage. This augmentation shifts the operator's focus from continuous monitoring to high-level strategic decision review and complex problem-solving based on AI-generated insights and recommendations.

North America's demand is driven by regulatory compliance and upgrades in existing high-security infrastructure, whereas the Asia Pacific region's exceptional growth is fueled by massive greenfield development, state-led smart city projects, and rapid industrialization requiring entirely new, scalable control centers.

Primary operational restraints include the substantial complexity and high cost associated with integrating modern IP solutions with diverse legacy proprietary Operational Technology (OT) systems, coupled with a persistent global shortage of highly specialized technical personnel required for 24/7 system maintenance and advanced operation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.