ID : MRU_ 433323 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

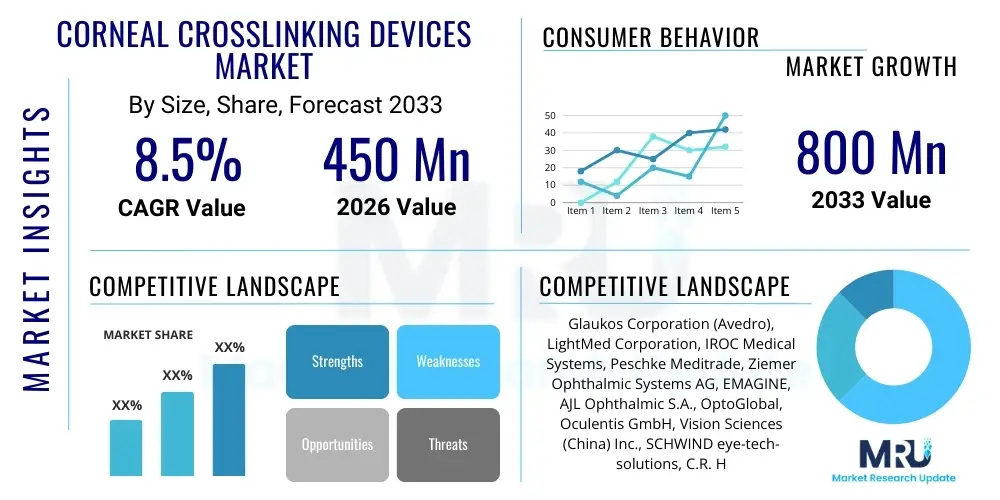

The Corneal Crosslinking Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 800 Million by the end of the forecast period in 2033.

Corneal Crosslinking (CXL) devices are specialized medical systems utilized in an ophthalmic procedure designed to strengthen the corneal tissue. This minimally invasive technique is primarily employed to treat progressive corneal ectatic disorders, most notably keratoconus, by increasing the biomechanical rigidity of the cornea. The procedure involves the application of a photosensitizer, typically Riboflavin (Vitamin B2), followed by exposure to controlled Ultraviolet A (UVA) light. This interaction fosters new chemical bonds (crosslinks) between collagen fibers, halting the progressive thinning and deformation of the cornea which otherwise leads to significant vision impairment.

The core product offering in this market includes the UVA irradiation systems, which provide precise and controlled energy delivery, and the associated consumables, such as specialized Riboflavin formulations (dextran-free, transepithelial, or iontophoretic solutions). Major applications extend beyond keratoconus to include post-LASIK ectasia and certain corneal infections. The primary benefit of CXL is its ability to stabilize corneal shape, thus preventing the need for more invasive procedures like penetrating keratoplasty (corneal transplantation), which carries higher risks and longer recovery times. This shift towards preventative, stabilizing treatments fuels market expansion.

Driving factors for the adoption of CXL devices include the rising global incidence and prevalence of keratoconus, particularly in younger populations, coupled with increasing awareness among ophthalmologists and patients regarding the efficacy and safety profile of CXL. Furthermore, advancements in CXL technology, such as accelerated protocols, topography-guided treatments, and non-invasive transepithelial methods, are broadening the patient pool suitable for treatment. Regulatory approvals in major economies, particularly the United States and Europe, have standardized the procedure and instilled greater clinical confidence, solidifying its position as the standard of care for progressive corneal ectasia.

The Corneal Crosslinking Devices Market is characterized by robust growth driven fundamentally by the increasing global diagnosis rates of keratoconus and continuous technological refinements aimed at improving procedural efficiency and patient comfort. Key business trends include strategic collaborations between device manufacturers and eye care providers, aggressive focus on developing novel Riboflavin formulations that reduce treatment time and enhance penetration, and expansion into emerging markets where keratoconus prevalence is high but infrastructure is still developing. Successful market participants are focusing on systems that offer customization options, suchately topography-guided treatments, to deliver superior visual outcomes compared to standard protocols.

Regionally, North America and Europe currently dominate the market due to high healthcare expenditure, well-established reimbursement policies for CXL procedures, and the early adoption of advanced CXL technologies. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth over the forecast period, fueled by a large patient base, improving healthcare access, and rising medical tourism promoting ophthalmic surgery. Segmentation trends indicate that the Consumables segment, driven by repeat purchases of proprietary Riboflavin solutions and accessories, will maintain a higher growth rate than the Systems segment, which is prone to longer replacement cycles. Furthermore, the Keratoconus application segment remains overwhelmingly dominant, though the application in infectious keratitis is showing promising adoption.

Overall, the market dynamic is shifting from penetration of basic CXL systems to optimization and technological superiority, emphasizing faster treatment protocols (accelerated CXL) and enhanced safety profiles (transepithelial CXL). Investors and stakeholders must prioritize companies that demonstrate strong intellectual property protection around Riboflavin formulations and possess comprehensive training programs to facilitate widespread adoption in geographically diverse clinical settings. The ongoing clinical research into combined CXL procedures, such as pairing CXL with photorefractive keratectomy (PRK), also represents a significant avenue for future market expansion and procedural volume increase.

User inquiries regarding the influence of Artificial Intelligence (AI) on the Corneal Crosslinking Devices Market primarily center on how AI can enhance diagnostic accuracy, optimize treatment planning, and personalize procedural outcomes. Common questions explore AI’s role in automating the detection of subtle early-stage keratoconus from corneal topography data, predicting the progression rate of ectasia, and calculating the optimal parameters (UVA intensity, exposure time, riboflavin saturation) necessary for individualized CXL treatment. Users are keenly interested in predictive modeling capabilities that can minimize the risk of under- or over-treatment and improve long-term stabilization rates, thereby augmenting the efficacy of existing CXL devices and protocols.

The Corneal Crosslinking Devices Market growth trajectory is significantly influenced by a powerful combination of driving forces and inherent restraints, all filtered through the lens of critical opportunities and external impact forces. Primary drivers include the global epidemic increase in diagnosed cases of keratoconus, which affects approximately 1 in 2,000 individuals globally, and substantial clinical evidence supporting CXL as a safe, effective, and cost-effective first-line treatment. The increasing demand for minimally invasive ophthalmic procedures and improvements in regulatory acceptance across highly regulated markets further bolster the market's positive outlook. However, the market faces constraints such as the high initial capital investment required for purchasing UVA illumination systems, the relatively complex procedural training needed for ophthalmologists, and the persistent lack of standardized global protocols for treatment across all patient demographics, particularly concerning pediatric cases.

Opportunities within this specialized segment revolve around the development and commercialization of new, less-invasive transepithelial CXL protocols and devices that eliminate the need for epithelial removal, thereby reducing post-operative discomfort and recovery time. Furthermore, vast untapped potential exists in emerging Asian and Latin American markets where specialized ophthalmic care penetration is growing rapidly. Strategic opportunities also include research into advanced Riboflavin formulations designed for faster penetration and increased efficacy under accelerated UVA exposure, allowing treatment times to be dramatically reduced. The overall impact forces relate primarily to technological obsolescence pressure, regulatory scrutiny over device safety, and reimbursement coverage expansion, which profoundly influences patient access and device adoption rates in key geographical regions.

Specific market dynamics show that the high impact of the driving force concerning rising keratoconus prevalence far outweighs the moderate impact of restraints related to device cost and complexity, particularly as financing and lease options become more common for clinical practices. The immediate impact forces center on competition among manufacturers to achieve the shortest treatment time, moving from standard 30-minute protocols to accelerated 10-minute or even 5-minute protocols. Successful market navigation requires manufacturers to address the cost-benefit ratio effectively, demonstrating that early CXL intervention prevents much higher long-term healthcare costs associated with advanced keratoconus treatment or corneal transplant surgery.

The Corneal Crosslinking Devices Market is comprehensively segmented based on product type, application, and end-user, allowing for detailed market assessment and strategic targeting. The product segmentation differentiates between the long-lifecycle UVA illumination Systems and the recurring revenue generating Consumables, which include Riboflavin formulations, single-use application tools, and specialized corneal shields. Application segmentation highlights the dominance of keratoconus treatment, which accounts for the vast majority of procedural volume, alongside emerging uses in corneal ectasia following refractive surgery and infectious keratitis treatment. End-user segmentation reflects the primary healthcare settings where CXL procedures are performed, ranging from large, comprehensive hospital ophthalmology departments to specialized, high-volume private eye clinics.

The value chain for Corneal Crosslinking Devices is specialized, beginning with sophisticated upstream activities focused on the research and development of both UVA delivery technology and proprietary Riboflavin chemistry. Upstream analysis involves high investment in optical engineering, materials science for UV light sources, and pharmaceutical development to formulate stable, effective Riboflavin solutions that maximize corneal absorption and penetration efficiency. Manufacturers must rigorously manage intellectual property surrounding these formulations, as the proprietary nature of the Riboflavin solution often dictates device compatibility and forms a significant barrier to entry.

Midstream activities encompass the manufacturing, quality control, and assembly of the complex CXL systems, ensuring compliance with stringent medical device regulations (e.g., FDA, CE Mark). The distribution channel represents a critical juncture, typically involving a mix of direct sales teams for key accounts (major hospitals) and specialized indirect distributors who manage sales, training, and technical support across broader geographical territories, particularly in developing regions. Given the technical nature of the devices, distribution often mandates extensive training for sales representatives and clinical application specialists to effectively demonstrate the technology's benefits and procedural nuances to end-users.

Downstream analysis focuses on the end-users—ophthalmologists and clinics—who perform the CXL procedures. The value generated at this stage is tied directly to patient outcomes and subsequent quality of life improvement. The key drivers of downstream value are device reliability, ease of use, and integration capability with existing ophthalmic diagnostic equipment (like topography and pachymetry systems). The direct channel interaction allows manufacturers to gain immediate clinical feedback, whereas indirect channels leverage existing regional networks to ensure timely supply of high-volume consumables, ultimately supporting consistent patient care and driving procedural volume growth.

The primary customers for Corneal Crosslinking Devices are ophthalmic surgeons and specialized eye care facilities treating patients suffering from progressive corneal disorders. These facilities range from large university hospitals and teaching institutions, which often serve as early adopters for new technologies and conduct clinical research, to mid-sized specialized private ophthalmology clinics that focus specifically on refractive surgery and corneal disease management. The decision-makers within these institutions prioritize devices that offer proven clinical safety, efficiency (shorter treatment times), and strong reimbursement potential.

Ambulatory Surgical Centers (ASCs) are rapidly emerging as significant buyers, valuing CXL devices for their profitability potential and efficiency in handling high patient throughput in an outpatient setting. Smaller, regional eye clinics often serve as secondary customers, relying heavily on reliable and cost-effective systems, often acquired through third-party distributors or leasing agreements. The ultimate beneficiaries—the patients suffering from keratoconus—drive the market demand, compelling physicians to invest in the latest stabilizing technology to prevent vision deterioration and dependency on corneal transplants.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 800 Million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Glaukos Corporation (Avedro), LightMed Corporation, IROC Medical Systems, Peschke Meditrade, Ziemer Ophthalmic Systems AG, EMAGINE, AJL Ophthalmic S.A., OptoGlobal, Oculentis GmbH, Vision Sciences (China) Inc., SCHWIND eye-tech-solutions, C.R. Healthcare, Alcon, Bausch + Lomb, CorneaGen, Topcon Corporation, Keragen GmbH, The Eye Company. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Corneal Crosslinking Devices market is undergoing rapid evolution, primarily focused on reducing treatment time, improving Riboflavin delivery, and enhancing procedural customization. The foundational technology relies on calibrated UVA light sources, typically LED or diode-based systems, designed to emit radiation precisely at 365 nm, the optimal wavelength for Riboflavin activation. A major technological shift involves the transition from standard (Dresden protocol) CXL, which uses low-intensity UVA over 30 minutes, to Accelerated CXL (A-CXL). A-CXL utilizes higher intensity irradiance for shorter periods (e.g., 9mW/cm² for 10 minutes), significantly improving clinic efficiency and patient compliance without compromising clinical efficacy, provided the laws of reciprocity are respected concerning total energy delivered.

In terms of Riboflavin delivery, the market is seeing continuous innovation in formulations. Standard epi-off (epithelium removal) CXL requires Dextran-based solutions, but the focus is rapidly shifting towards Transepithelial CXL (Epi-on), utilizing proprietary Riboflavin formulas combined with enhancers (like EDTA or benzalkonium chloride) or delivery methods such as iontophoresis. Iontophoresis CXL devices use a mild electrical current to facilitate the non-invasive penetration of Riboflavin through the intact epithelium, promising faster healing and reduced risk of infection, although its efficacy compared to epi-off remains a subject of ongoing clinical debate. These advancements are crucial for expanding CXL application in pediatric cases and patients with thin corneas where epi-off is riskier.

Furthermore, integration technologies are crucial, encompassing topography-guided and customized CXL systems. These advanced platforms utilize pre-operative corneal mapping data to modulate the UVA intensity spatially across the cornea, theoretically allowing for some degree of refractive improvement alongside stabilization, rather than just halting progression. The increasing adoption of integrated monitoring systems, which provide real-time feedback on corneal temperature and riboflavin saturation during the procedure, is further enhancing safety and standardization. The technological trajectory clearly favors intelligent, rapid, and customizable treatment platforms that minimize patient burden while maximizing long-term stability.

The global Corneal Crosslinking Devices market displays significant regional variation in terms of adoption rates, reimbursement policies, and prevalence of keratoconus. North America, specifically the United States, holds a dominant market share. This leadership is underpinned by high awareness levels, favorable and extensive reimbursement coverage following FDA approval of CXL protocols (especially in-office procedures), and the presence of major industry players like Glaukos (Avedro). The region also benefits from a mature healthcare infrastructure capable of supporting the high capital investment required for specialized CXL systems and associated diagnostic equipment, driving consistent procedural volume.

Europe represents the second-largest market, characterized by high adoption rates in countries like Germany, the UK, and France. Early clinical acceptance of CXL protocols, often predating FDA approval in the US, allowed European manufacturers to establish a strong presence. The market here is fragmented, with significant interest in newer, accelerated, and transepithelial CXL protocols driven by patient demand for reduced recovery times and enhanced comfort. Reimbursement varies significantly among national healthcare systems, influencing the distribution mix between public hospitals and private clinics.

The Asia Pacific (APAC) region is forecasted to be the fastest-growing market segment. This accelerated growth is primarily attributed to a massive and largely undertreated patient population, increasing disposable incomes, and rapidly expanding access to advanced ophthalmic care in economic hubs such as China, India, and South Korea. While historically reliant on older, less standardized CXL protocols, the introduction of proprietary systems from Western manufacturers and rising medical tourism are rapidly driving the adoption of high-end accelerated devices. Growth in Latin America and the Middle East and Africa (MEA) is moderate, constrained by cost sensitivity and less developed reimbursement frameworks, although increasing investment in specialized eye hospitals is slowly improving market access.

The primary factor driving market growth is the globally increasing incidence and diagnosis rates of progressive keratoconus and other corneal ectatic disorders, coupled with strong clinical evidence establishing Corneal Crosslinking (CXL) as the standard of care for halting disease progression.

Accelerated CXL significantly boosts market demand by reducing treatment time from 30 minutes to often 10 minutes or less, improving patient comfort, enhancing clinic throughput, and facilitating wider adoption in both specialized eye clinics and Ambulatory Surgical Centers (ASCs).

The Consumables segment, primarily driven by the recurring purchase of proprietary Riboflavin formulations and single-use accessories, is expected to exhibit a higher growth rate, following the initial placement and subsequent utilization of the CXL Systems.

Future CXL devices will be shaped by the widespread adoption of transepithelial (Epi-on) CXL protocols, integration of Artificial Intelligence for personalized treatment planning, and topography-guided systems that optimize UVA delivery for superior refractive outcomes alongside stabilization.

The Asia Pacific (APAC) region is projected to hold the highest potential for future market expansion due to its vast, underserved patient population, increasing penetration of advanced medical technologies, and rapid development of healthcare infrastructure in major economies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.