ID : MRU_ 432956 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

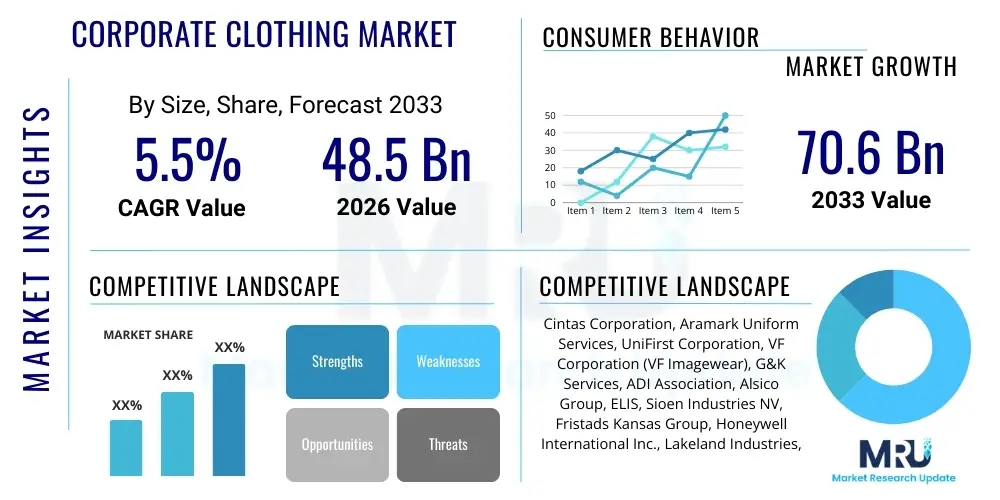

The Corporate Clothing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2026 and 2033. The market is estimated at $48.5 Billion in 2026 and is projected to reach $70.6 Billion by the end of the forecast period in 2033.

The Corporate Clothing Market encompasses the design, manufacture, and distribution of professional garments, including uniforms, workwear, protective apparel, and business attire tailored specifically for organizational employees. This product category is crucial for establishing corporate identity, ensuring brand cohesion, and, most importantly, providing necessary safety and functionality in various work environments, ranging from heavy industrial settings to client-facing service sectors. The primary goal of corporate clothing is multifaceted: to comply with regulatory safety standards, enhance professional appearance, and foster a sense of belonging and uniformity among staff, thereby indirectly improving productivity and customer perception.

Major applications for corporate clothing span a vast array of industries. The service sector, including hospitality, retail, and healthcare, relies heavily on uniforms for identification and hygiene. The industrial sector, including construction, manufacturing, and energy, mandates specialized protective workwear (Personal Protective Equipment or PPE) to mitigate workplace hazards. Furthermore, increasing corporate focus on sustainability and ethical sourcing has driven significant product evolution, leading to the integration of eco-friendly materials and smart textile technologies into professional attire. This shift ensures that modern corporate clothing is not merely functional but also aligned with organizational Environmental, Social, and Governance (ESG) mandates.

Key benefits driving market adoption include enhanced workplace safety compliance, improved brand recognition, and standardization of employee appearance. Driving factors fueling sustained growth involve stringent governmental regulations regarding worker safety, particularly in emerging economies undergoing rapid industrialization, and the sustained growth of the service and retail sectors globally. Technological advancements in fabric science, such as moisture-wicking, antimicrobial finishes, and integrated monitoring sensors, further accelerate the replacement cycle and drive demand for high-performance corporate apparel. The psychological impact of professional attire on employee confidence and team morale also serves as a subtle yet powerful market driver.

The global Corporate Clothing Market is characterized by robust resilience and steady growth, underpinned by non-discretionary safety and compliance requirements across industrial and service sectors. Current business trends indicate a strong move toward customization and personalization, leveraging digital design tools and on-demand manufacturing to meet specific corporate branding needs while minimizing inventory risk. Furthermore, there is a pronounced convergence between traditional corporate fashion and technical textile innovation, pushing manufacturers to integrate performance features—like enhanced durability, temperature regulation, and high visibility—into standard corporate uniforms. Strategic mergers and acquisitions among regional specialized manufacturers and large global players are reshaping the competitive landscape, aiming to consolidate supply chains and expand geographic footprints, particularly into fast-growing Asian markets.

Regional trends highlight Asia Pacific (APAC) as the fastest-growing market, driven by massive infrastructure development, manufacturing expansion, and burgeoning organized retail and healthcare sectors requiring large volumes of compliant uniforms and PPE. North America and Europe, while mature, remain dominant in terms of value, characterized by high adoption rates of premium, technologically advanced workwear and strict adherence to specific Occupational Safety and Health Administration (OSHA) and European Union (EU) directives. The maturity in these Western markets necessitates innovation in service delivery, such as managed uniform programs, rental services, and laundry services, shifting focus from pure product sales to comprehensive uniform solutions. Additionally, political and economic stability directly influences purchasing cycles, with large corporations opting for multi-year managed service contracts to ensure cost predictability and quality consistency.

Segmentation trends reveal significant growth in the Protective Clothing segment, driven by regulatory mandates in high-risk industries (Oil & Gas, Chemical). The segment covering Managed Uniform Programs is also witnessing accelerated uptake, particularly among large multinational corporations seeking centralized management of procurement, distribution, and maintenance across diverse operational locations. By product type, outerwear and specialized technical garments are gaining prominence due to increasing complexities in environmental and operational hazards. The distribution channel analysis shows a continued shift toward B2B e-commerce platforms and direct manufacturer sales, enabling greater transparency and efficient inventory management for corporate buyers, though specialized distributors remain critical for localized fitting and service delivery for smaller enterprises.

Common user inquiries regarding AI in the Corporate Clothing Market typically revolve around four core themes: supply chain optimization, customized sizing accuracy, predictive demand forecasting, and design automation. Users are particularly concerned with how AI can minimize waste in inventory management—a critical issue given the often-large, non-standardized order volumes of corporate attire. There is also significant interest in AI-driven personalized fit solutions, aimed at reducing costly returns and ensuring employee comfort and safety, especially for complex protective gear. Furthermore, corporations are seeking clarity on how machine learning algorithms can analyze macro-economic indicators and internal utilization data to accurately forecast demand for seasonal uniform changes or staffing fluctuations, thereby ensuring timely procurement and cost efficiencies. The general expectation is that AI will transition the market from reactive procurement cycles to highly personalized, predictive manufacturing models.

The implementation of AI is expected to revolutionize production workflows, particularly in the realm of pattern making and material cutting. Computer Vision and deep learning models can analyze detailed 3D body scans to create hyper-accurate sizing profiles, replacing traditional manual measurements and ensuring ergonomic suitability of complex garments, such as fire-resistant suits or medical scrubs. This precision is vital for compliance where a poor fit can compromise the protective capabilities of the clothing. In terms of inventory, AI-powered systems can integrate sales data, staff turnover rates, and operational scheduling to generate highly accurate demand forecasts, resulting in reduced warehousing costs and minimizing obsolescence risk associated with custom-branded apparel. This predictive capability directly supports sustainability goals by avoiding overproduction.

Furthermore, AI algorithms are becoming instrumental in textile innovation and quality control. Machine learning can analyze material performance under various stress conditions (e.g., abrasion, chemical exposure) to optimize fabric selection for specific roles, improving longevity and cost-effectiveness. On the consumer interaction front (B2B buyer experience), AI chatbots and virtual stylists can guide procurement managers through complex regulatory compliance requirements, recommending compliant garments based on industry, region, and specific job roles. This enhanced advisory capacity simplifies the purchasing process for non-expert buyers, positioning manufacturers who adopt these tools as essential solution providers rather than just product vendors. Ultimately, AI fosters a more efficient, responsive, and data-driven corporate clothing supply ecosystem.

The Corporate Clothing Market is fundamentally shaped by a dynamic interplay of Drivers (D), Restraints (R), and Opportunities (O), which collectively define the Impact Forces influencing long-term market trajectories. The primary driver is the stringent, non-negotiable regulatory environment concerning occupational health and safety (OHS), particularly in high-risk sectors globally. This mandates the continuous purchase and replacement of specialized protective clothing, creating a consistent baseline demand regardless of economic cycles. Restraints include the significant fragmentation of the market, where numerous small and medium-sized local players complicate supply chain standardization, alongside the volatility of raw material prices (e.g., cotton, synthetic fibers) which directly impacts manufacturing costs and profit margins. However, emerging opportunities lie in the accelerating demand for high-tech, multifunctional textiles (smart clothing) and the expansion of managed uniform services, which provide recurring revenue streams and deeper integration with corporate clients. These forces exert considerable pressure on manufacturers to innovate structurally, financially, and technologically to maintain competitiveness.

Key drivers include the global expansion of organized service industries, such as retail chains, fast food franchises, and healthcare providers, which require unified branding across multiple international locations, driving bulk procurement of consistent corporate wear. Furthermore, the growing awareness among employers regarding the importance of employee well-being and corporate social responsibility (CSR) has spurred investment in higher quality, ergonomically designed, and sustainably sourced garments, moving beyond basic low-cost uniforms. Technological advancements, such as textiles offering enhanced protection against biological or chemical agents, also drive cyclical replacement demand as older, less effective gear is phased out. Economic indicators, such as stable employment growth in industrial and service sectors, directly translate into expanded demand for new uniforms and replacement stock.

Restraints are notably complex, including the high initial investment required for establishing efficient, scalable uniform management systems, particularly for companies operating globally. The challenge of achieving perfect fit and comfort across a diverse workforce often leads to logistical complexities and high return rates, inflating operational costs. Moreover, the long product lifespan of certain high-quality uniforms can occasionally slow down replacement cycles compared to fast fashion sectors. Opportunities are robust, centering on market penetration in developing regions where formal regulatory frameworks are solidifying, creating massive, previously untapped demand for compliant workwear. The trend toward adopting sustainable and circular economy models in textile manufacturing presents a substantial avenue for differentiation and premium pricing, appealing to environmentally conscious corporate buyers. Leveraging digital platforms for customized design and direct-to-business sales also offers an opportunity to bypass traditional, often inefficient, distribution channels, improving efficiency and time-to-market.

The Corporate Clothing Market is highly segmented based on product type, end-user industry, fabric type, and distribution channel, reflecting the diverse functional and aesthetic requirements of the global workforce. This intricate segmentation allows manufacturers to specialize in highly profitable niches, such as flame-resistant protective wear for the energy sector or antimicrobial scrubs for the healthcare industry. The primary axes of differentiation are functionality (e.g., safety, hygiene, aesthetics) and material composition (e.g., natural fibers, synthetic blends, technical textiles). Understanding the consumption patterns across these segments is critical for strategic resource allocation, particularly in targeting high-growth sectors like healthcare and logistics, which have shown inelastic demand for specialized, high-performance apparel due to critical operational needs.

The Corporate Clothing Market value chain is a complex, vertically integrated structure beginning with raw material sourcing and culminating in final uniform distribution and often, recycling or disposal. The upstream segment involves the production of textiles and technical fibers, where specialized knowledge regarding protective properties (flame resistance, chemical inertness) is critical. Key upstream activities include spinning, weaving, and applying specialized finishes (e.g., antimicrobial, stain-resistant). Fluctuations in the cost of raw materials, such as petroleum derivatives for synthetic fibers or agricultural conditions for cotton, heavily influence the pricing power and stability of the entire chain. Strategic sourcing partnerships and vertical integration are essential strategies employed by major players to mitigate supply chain risk and maintain quality control from the fiber stage onward.

The core manufacturing and distribution stage involves pattern design, cutting, assembly, embroidery, and customization. This stage is increasingly driven by technology, including 3D modeling for accurate fit and automated cutting systems. The downstream segment is highly critical in corporate clothing due to the need for localized service, fitting, maintenance, and logistics. Distribution channels are highly fragmented, relying on a mix of direct sales to large corporations, specialized regional distributors handling niche segments (like medical PPE), and comprehensive managed uniform service providers who offer rental, cleaning, repair, and inventory tracking as a complete package. The dominance of managed services reflects the trend among corporate buyers to outsource non-core functions, prioritizing reliable, consistent uniform supply over direct ownership and maintenance responsibilities.

Direct channels are preferred by very large corporations that possess strong procurement teams and require highly customized or highly specialized technical garments, allowing for closer communication with the manufacturer regarding specifications and testing. Indirect channels, particularly distributors, play a crucial role in serving small and medium-sized enterprises (SMEs) that require lower volume orders, immediate stock availability, and regional fitting services. The overall value proposition is shifting from merely supplying a garment to providing a comprehensive, regulatory-compliant, end-to-end uniform lifecycle management solution. Therefore, successful companies are those that invest equally in advanced logistics, fitting expertise, and robust inventory management systems alongside core manufacturing capabilities, thus maximizing value capture in the downstream service phase.

Potential customers for the Corporate Clothing Market are predominantly large enterprises and institutions whose operations require standardized appearance, regulatory compliance, or mandatory employee protection. The end-user base is extremely diverse but can be broadly categorized into highly regulated sectors and high-volume customer-facing sectors. Highly regulated sectors, such as Oil & Gas, Chemicals, Mining, and specialized Manufacturing, are characterized by high-value, low-volume purchases of complex Protective Clothing (PPE), where safety specifications dictate material choice and procurement decisions are made by Health, Safety, and Environment (HSE) departments. These buyers prioritize product certification, compliance documentation, and demonstrable material performance over initial cost.

Conversely, high-volume service sectors like Hospitality (major hotel chains, restaurant franchises), Retail (department stores, supermarkets), and Transportation (airlines, logistics firms) drive demand for standard Uniforms and General Workwear. In these segments, the purchasing criteria are balanced between corporate branding aesthetics, durability, comfort, and cost-effectiveness, with procurement often managed by HR or Marketing departments. The sheer size and constant employee turnover in these industries ensure consistently high demand for replacement and new uniforms. Emerging customer groups include the rapidly expanding e-commerce logistics and fulfillment industry, which requires high-visibility and lightweight protective gear for warehouse and delivery staff.

Healthcare facilities, including large hospital networks and clinics, represent a distinct and rapidly growing customer segment, driven by strict hygiene protocols requiring specialized antimicrobial and reusable surgical textiles. These customers value managed inventory and laundry services to ensure sterile circulation of garments. Government agencies, including military, police forces, and municipal service departments (fire, waste management), also represent significant, long-term contractual customers requiring highly durable and specific functional clothing, often sourced through complex, large-scale public tenders. Success in serving any potential customer base hinges on the provider's ability to offer a complete solution that addresses not just the product need, but also the logistical and regulatory complexities inherent in managing a large institutional uniform inventory.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $48.5 Billion |

| Market Forecast in 2033 | $70.6 Billion |

| Growth Rate | 5.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cintas Corporation, Aramark Uniform Services, UniFirst Corporation, VF Corporation (VF Imagewear), G&K Services, ADI Association, Alsico Group, ELIS, Sioen Industries NV, Fristads Kansas Group, Honeywell International Inc., Lakeland Industries, 3M Company, Hultafors Group, William & Russell Ltd., Red Kap (VF Corp), Dickies (VF Corp), Superior Uniform Group, Workwear Group, W. L. Gore & Associates |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Corporate Clothing Market is rapidly evolving, driven by the need for enhanced functionality, improved sustainability, and efficient supply chain management. The foundational technological advancements center on smart textiles and integrated technology. Smart clothing incorporates sensors and microelectronics directly into the fabric to monitor physiological data (e.g., heart rate, temperature), track employee location, and detect environmental hazards (e.g., gas leaks, extreme heat). This integration elevates the function of corporate clothing from mere protection to preventative safety monitoring, particularly critical in industrial environments. Furthermore, advancements in specialized finishes, such as permanent flame resistance, hydrophobic coatings for liquid repellency, and highly durable antimicrobial treatments, ensure that garments maintain their protective features throughout their extensive lifespan and demanding wash cycles, directly improving the return on investment for corporate buyers.

Manufacturing technologies are also undergoing transformation through digitization. The adoption of 3D virtual prototyping and digital design tools significantly reduces the time and cost associated with developing new uniform ranges and customized client orders. These tools allow for iterative design changes and accurate fit testing without physical sampling, streamlining the procurement process. On the supply chain side, technologies like RFID tagging and Near-Field Communication (NFC) are becoming standard, enabling highly efficient tracking of individual garments throughout the uniform management lifecycle—from issuance and laundry cycles to mandatory replacement dates. This tracking capability is paramount for regulatory compliance, especially in sectors where PPE replacement schedules must be strictly documented and adhered to.

The push toward sustainable manufacturing necessitates the integration of technologies related to circular economy practices. This includes chemical recycling processes that allow high-performance synthetic fabrics to be broken down and reconstituted into new textile fibers, minimizing dependence on virgin materials. Additionally, advanced textile blending techniques and the utilization of recycled materials (like recycled polyester) are becoming essential competitive differentiators. From an end-user perspective, the adoption of digital platforms for managed services, featuring predictive inventory algorithms and user-friendly portals for employee uniform ordering and fitting appointments, constitutes a major technological shift. These platforms enhance transparency and efficiency, moving the market away from cumbersome paper-based systems toward seamless, data-driven uniform provision. The continuous evolution of these technologies ensures that corporate clothing remains a high-tech segment focused equally on material science and logistical innovation.

The primary driver is the increasing stringency and enforcement of occupational health and safety (OHS) regulations globally, particularly regarding mandatory Personal Protective Equipment (PPE) in high-risk industries such as manufacturing, construction, and energy, ensuring consistent demand for compliant, high-specification technical clothing.

Sustainability is now a critical factor; corporate buyers increasingly prioritize suppliers who offer garments made from recycled or organic materials, utilize ethical labor practices, and provide end-of-life recycling programs, aligning procurement with organizational Environmental, Social, and Governance (ESG) commitments.

The Protective Clothing segment is seeing the fastest technological integration, primarily through the adoption of smart textiles embedded with sensors for biometric monitoring and environmental hazard detection, moving beyond static protection to real-time preventive safety solutions.

Managed uniform service providers (e.g., rental and laundry services) are crucial as they offer comprehensive lifecycle management, including cleaning, repair, inventory tracking, and replacement, allowing large corporations to outsource uniform logistics and ensure continuous compliance and supply efficiency.

The Asia Pacific (APAC) region represents the largest potential for expansion, driven by accelerating industrialization, massive infrastructure development projects, and the maturation of regulatory frameworks in populous economies like China, India, and Indonesia, fueling significant demand for both general uniforms and specialized workwear.

General workwear focuses on standardization, branding, and comfort for environments with low risk (e.g., retail, office). Protective clothing (PPE) is designed and certified to specific international standards (e.g., ANSI, EN) to mitigate serious physical, chemical, or thermal hazards, making compliance and material science the priority.

B2B e-commerce platforms offer corporate buyers greater transparency, streamlined ordering processes, and better inventory visualization, facilitating direct manufacturer engagement and reducing reliance on traditional intermediary distributors for non-specialized or high-volume repeat orders, thereby improving procurement efficiency.

Key challenges include volatile pricing and supply chain instability for specialized technical fibers (like aramid) and fluctuations in raw commodity markets (like cotton). Additionally, manufacturers face the complexity of tracing material origins to meet stringent ethical sourcing and sustainability mandates required by corporate clients.

AI utilizes 3D body scanning data and predictive algorithms to generate highly accurate, personalized sizing recommendations. This minimizes the historically high rate of returns associated with poorly fitting corporate clothing and ensures that safety-critical gear fits correctly, maintaining protective function.

In the healthcare sector, the primary functional requirements are strict hygiene, durability to withstand rigorous industrial laundering, comfort for long shifts, and often, specialized features like antimicrobial treatments or fluid repellency to maintain a sterile environment and protect staff from biological hazards.

Circularity refers to designing uniforms for longevity, repairability, and eventual closed-loop recycling. It involves processes where retired garments are chemically or mechanically recycled back into new textile fibers, minimizing waste sent to landfill and reducing the overall environmental footprint of corporate procurement.

The Oil & Gas industry is high-value because it mandates extremely specialized, fire-resistant (FR) and antistatic protective clothing for all field personnel. These garments utilize expensive technical fibers (e.g., Nomex, Kevlar), leading to high per-unit cost and non-negotiable compliance requirements.

The typical lifespan varies based on use intensity, but specialized industrial workwear often has a mandatory replacement cycle dictated by regulatory bodies or manufacturer warranty, usually ranging from 12 to 36 months, particularly for high-visibility or chemical-resistant materials whose efficacy degrades over time and washing.

Economic slowdowns have a limited dampening effect compared to discretionary consumer goods. While aesthetic uniform upgrades might be postponed, demand for regulatory-mandated protective clothing remains inelastic and essential, providing the market with strong fundamental stability rooted in safety compliance.

Specialized finishes significantly enhance performance, including antimicrobial finishes (for hygiene in healthcare/food service), stain-release finishes (for durability and cleanliness), and permanent press or wrinkle-resistant treatments (for professional aesthetics with minimal maintenance), thereby increasing the value proposition of the garment.

Customization (e.g., corporate colors, specific logos, personalized nametags) necessitates a highly flexible and technologically advanced downstream supply chain capable of handling small-batch personalization and accurate order consolidation, often relying on automated embroidery and digitally integrated ordering systems.

The shift to rental or managed service models transfers the burden of uniform maintenance, inventory tracking, cleaning, and disposal from the corporation to the supplier. This offers corporations predictable operating expenses (OpEx) versus capital expenditure (CapEx) and ensures professional laundering maintains regulatory compliance.

The Logistics and E-commerce Fulfillment sector is emerging rapidly. The massive workforce growth in warehousing and last-mile delivery requires functional, durable, often high-visibility workwear that balances safety compliance with lightweight comfort for extended periods of physical activity.

High-visibility clothing must meet strict photoluminescent standards and use specific colors (typically fluorescent yellow-green or orange) as defined by international standards (e.g., ANSI/ISEA 107 or EN ISO 20471). These color requirements severely limit branding flexibility but are non-negotiable for worker safety in low-light or traffic environments.

Manufacturers ensure consistent quality through standardized operating procedures (SOPs), rigorous supplier qualification protocols, implementation of certified quality management systems (e.g., ISO 9001), and increasingly, the use of automated inspection technologies like Computer Vision systems on production lines globally.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.