ID : MRU_ 434854 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

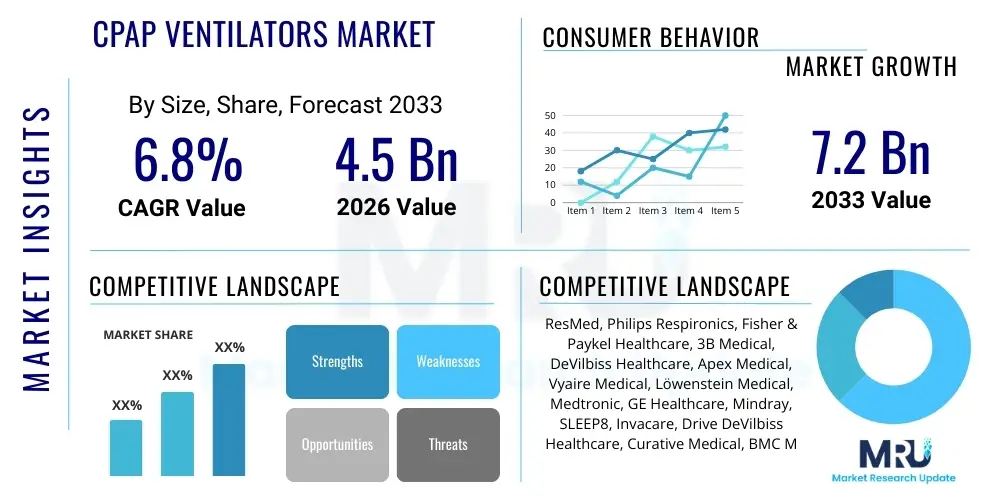

The CPAP Ventilators Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $4.5 Billion in 2026 and is projected to reach $7.2 Billion by the end of the forecast period in 2033.

The Continuous Positive Airway Pressure (CPAP) Ventilators Market encompasses devices crucial for treating Obstructive Sleep Apnea (OSA) and related respiratory conditions. CPAP devices function by delivering pressurized air through a mask to the user’s airway, preventing collapse of the soft tissues and ensuring continuous, unobstructed breathing during sleep. Initially conceptualized as bulky hospital equipment, modern CPAP technology has evolved significantly, focusing on miniaturization, enhanced comfort, and sophisticated algorithms for pressure optimization. The primary product category includes standard CPAP, automatic CPAP (APAP), and bi-level positive airway pressure (BiPAP) devices, each catering to specific patient needs regarding pressure delivery variability and severity of apnea. The pervasive increase in lifestyle diseases, such as obesity and cardiovascular issues, directly contributes to the rising incidence of OSA, thereby cementing the essential nature of CPAP technology in global healthcare infrastructure.

Major applications for CPAP ventilators center heavily around chronic respiratory disorders, predominantly OSA, which affects a substantial portion of the adult population globally. Beyond OSA, these devices are increasingly utilized in specific instances of respiratory insufficiency, though their core strength remains in long-term home care for sleep-disordered breathing. The inherent benefits provided by CPAP therapy are significant, including drastic improvements in sleep quality, reduction in daytime fatigue, lower risk of cardiovascular complications associated with nocturnal hypoxia, and an overall enhancement in patient quality of life. Effective CPAP use mitigates the risks associated with untreated apnea, such as hypertension, stroke, and diabetes, positioning these devices as preventive healthcare tools as much as therapeutic ones.

The market is predominantly driven by several interconnected factors, including demographic shifts, technological innovation, and heightened medical awareness. The aging global population, which is more susceptible to sleep disorders, forms a foundational driver. Simultaneously, continuous advancements in sensor technology, mask design (improving patient adherence), and the integration of humidification systems have made therapy far more tolerable and effective. Furthermore, robust public health campaigns and improved diagnostic screening capabilities in primary care settings are increasing the diagnosis rate of sleep apnea, converting previously undiagnosed patients into active market consumers. The growing preference for home healthcare settings over institutional care also accelerates the demand for portable, user-friendly CPAP systems.

The CPAP Ventilators Market is experiencing robust growth fueled by favorable demographic trends and significant product innovation focused on connectivity and comfort. Business trends indicate a strong competitive emphasis on differentiating products through noise reduction technology, integrated data connectivity (telemonitoring), and lightweight designs suitable for travel and home use. Key market players are investing heavily in research and development to address the persistent challenge of patient compliance, often by developing automated algorithms (APAP) that dynamically adjust pressure, thus maximizing comfort and efficacy. Mergers and acquisitions remain a strategic tool, allowing larger entities to integrate niche technological expertise, especially in sensor technology and cloud-based patient management platforms, driving vertical integration across the value chain. The shift toward subscription models for accessories and consumables (masks, tubing, filters) is becoming a noticeable trend, ensuring recurring revenue streams for manufacturers.

Regionally, North America maintains market dominance due to high OSA prevalence, sophisticated healthcare reimbursement structures, and early adoption of advanced medical devices. However, the Asia Pacific (APAC) region is poised for the fastest expansion, driven by rapidly improving healthcare infrastructure, a burgeoning middle class, and increasing public health awareness regarding sleep disorders in populous countries like China and India. European markets exhibit mature demand characterized by strict regulatory standards and emphasis on clinically proven long-term efficacy. Governments and healthcare providers globally are increasingly recognizing the cost-effectiveness of treating OSA, supporting market growth through favorable insurance coverage policies, which particularly impacts regional market performance based on local healthcare spending priorities.

Segment trends highlight the growing preference for Automatic Positive Airway Pressure (APAP) devices over standard fixed CPAP devices, as APAP offers tailored therapy resulting in better user experience and adherence. Within the application segment, Obstructive Sleep Apnea (OSA) remains the overwhelming revenue generator, although specialized use cases in treating complex respiratory failure are also contributing marginal, high-value growth. The end-user segment is dominated by homecare settings, reflecting the core nature of CPAP therapy as a chronic, nightly intervention. Hospitals and sleep centers primarily serve as diagnostic and initial prescription points, with the subsequent sale and long-term use occurring within the patient's residence. This trend necessitates robust distribution networks focused on direct-to-consumer and durable medical equipment (DME) providers, influencing market strategies across all product segments.

Common user questions regarding AI's impact on CPAP ventilators frequently revolve around improved therapy personalization, remote monitoring capabilities, and the potential for predictive maintenance to enhance device reliability. Users are keen to understand how AI algorithms can move beyond simple pressure adjustments to proactively manage complex breathing patterns, identify subtle signs of non-compliance, and offer real-time coaching via integrated digital interfaces. There is also significant consumer interest concerning data privacy and the security protocols employed when sophisticated AI models process sensitive sleep and biometric data transmitted from connected CPAP devices. Furthermore, clinicians and users alike question whether AI can accurately predict adverse health events, such as impending cardiovascular episodes linked to sleep disturbances, transforming CPAP devices from reactive treatment tools into proactive health management platforms. These expectations underscore a desire for CPAP technology to evolve into a highly intuitive, self-optimizing, and fully integrated component of personal chronic health management.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming the CPAP market, shifting the focus from standardized therapy toward hyper-personalized patient care. AI algorithms are now deployed to analyze vast amounts of nightly sleep data, including apnea-hypopnea index (AHI), mask leak rates, and patient movement, allowing devices to optimize pressure delivery second by second far more efficiently than traditional APAP systems. This advanced analytical capability significantly improves comfort and compliance, addressing one of the most critical restraints facing the market. By recognizing complex flow limitations and proprietary breathing cycles unique to each patient, AI-driven devices can predict respiratory events before they occur, offering a smoother and more effective therapeutic experience, which subsequently reduces the burden on prescribing physicians for routine adjustments.

Beyond direct therapeutic application, AI plays a pivotal role in operational efficiency and patient management ecosystems. AI powers sophisticated telemonitoring platforms that allow healthcare providers to remotely track compliance and therapeutic effectiveness across entire patient populations, identifying those who require intervention swiftly. This proactive approach to adherence management improves outcomes and reduces healthcare costs associated with untreated OSA complications. Furthermore, AI contributes to supply chain optimization by predicting the replacement cycle for high-wear consumables (masks, humidifiers) based on individual usage patterns. While this shift enhances patient care, it simultaneously raises the technical complexity and data requirements for regulatory compliance, pushing manufacturers toward becoming technology and software companies as much as medical device providers.

The CPAP Ventilators Market is powerfully shaped by a dynamic interaction between rising public health crises (OSA prevalence), technological breakthroughs that improve user comfort, and persistent challenges related to patient adherence and affordability. The primary driving force is the escalating global prevalence of Obstructive Sleep Apnea, directly correlated with rising obesity rates and an aging demographic. Simultaneously, relentless innovation in noise reduction, ergonomic design, and integrated data analytics significantly reduces friction points for users, thereby boosting market acceptance. However, these positive drivers are constantly counteracted by significant restraints, particularly the typically high initial cost of advanced CPAP units and the ongoing expense of consumables. The critical restraint remains low long-term patient compliance, as up to 50% of users discontinue therapy within the first year, demanding continuous market efforts dedicated to device usability and educational support. Despite these hurdles, the substantial opportunity lies in penetrating high-growth emerging economies where diagnosis rates are currently low but populations are rapidly urbanizing and adopting Western lifestyles associated with higher OSA risk. The shift towards portable, travel-friendly units and the exploration of novel treatment modalities (like positional therapy or mandibular advancement devices) serve as adjacent opportunities that stabilize the market landscape.

Impact forces within the CPAP Ventilators market are highly concentrated in technological and regulatory domains. The bargaining power of buyers, particularly large hospital systems and Durable Medical Equipment (DME) providers, is moderate, as CPAP devices are essential for therapy but price sensitivity exists, especially in highly competitive reimbursement environments. The bargaining power of suppliers is relatively low to moderate, driven by standardized components in some areas (e.g., electronic sensors, microprocessors) but increasing for specialized, patented materials crucial for mask comfort and noise dampening. The threat of new entrants is low due to the stringent regulatory requirements (FDA, CE Mark) necessary for medical device certification, high R&D costs, and the established brand loyalty commanded by dominant market leaders. However, the threat of substitutes is significant and growing; alternatives such as surgical interventions (e.g., bariatric or palatal surgeries), hypoglossal nerve stimulation devices (HGNS), and pharmaceutical treatments for daytime sleepiness provide competitive pressure, pushing CPAP manufacturers to continually justify their non-invasive treatment efficacy.

The confluence of these forces dictates market trajectory: high prevalence drives volume, technological drivers dictate market premium and adherence rates, while the threat of substitutes mandates continuous product evolution. Specifically, the regulatory landscape is becoming stricter, particularly following notable device recalls, increasing the costs of compliance and acting as a barrier to entry. The increasing demand for connected health solutions means that manufacturers must navigate not only traditional medical device regulations but also complex data security and privacy laws (like HIPAA and GDPR), adding another layer of operational complexity. Successful companies in this environment are those that master the balance between aggressive technological advancement (minimizing discomfort/noise) and robust compliance programs, ensuring the long-term trust of both patients and clinicians.

The CPAP Ventilators Market segmentation provides a granular view of specific product preferences, clinical applications, and the points of care where these devices are utilized. Analysis by Product Type reveals a strong market shift away from basic, fixed-pressure CPAP devices toward more intelligent variants like Automatic Positive Airway Pressure (APAP) machines, which dynamically adjust pressure throughout the night, significantly improving user comfort and adherence. Bi-level PAP (BiPAP or BPAP) machines, offering separate inspiratory and expiratory pressures, cater to patients with complex needs, such as central sleep apnea or neuromuscular diseases, commanding a premium price point due to their specialized therapeutic capabilities. The ongoing trend favors mobility and discretion, leading to the rapid proliferation and increasing demand for specialized travel CPAP devices, which are compact, lightweight, and often battery-powered, catering to a highly mobile demographic.

When examined by Application, Obstructive Sleep Apnea (OSA) overwhelmingly dominates the market revenue share, constituting the core clinical use case for CPAP therapy worldwide. However, the application segment also includes smaller but clinically vital areas such as the management of COPD-related respiratory insufficiency and other forms of sleep-disordered breathing where non-invasive ventilation (NIV) is necessary. This dominant application focus means that marketing strategies and product development are intrinsically tied to addressing the specific physiological and lifestyle challenges faced by OSA patients. Moreover, the increasing recognition of CPAP's role in mitigating comorbid conditions, such as reducing the risk of cardiovascular events, subtly broadens its perceived application value among prescribing physicians.

Segmentation by End User confirms the central role of homecare settings as the largest revenue generator. Once a patient is diagnosed and prescribed a device, the majority of the therapeutic duration occurs at home, facilitating direct-to-consumer distribution models via Durable Medical Equipment (DME) providers. Hospitals and specialized sleep centers remain critical for initial diagnosis (using polysomnography), titration studies, and the first prescription process. However, the long-term economic model depends heavily on the replacement market for consumables sold to homecare users. This distribution structure emphasizes the necessity for user-friendly interfaces, robust patient support services, and strong logistical chains capable of handling repeat orders for masks, filters, and other accessories, dictating segment-specific marketing and sales strategies across the geographical spectrum.

The value chain for the CPAP Ventilators Market begins with rigorous Upstream Analysis, which involves the sourcing of critical high-quality components. These inputs include advanced microprocessors and sensors for dynamic pressure adjustment, noise reduction materials (acoustic baffling), and specialized medical-grade polymers and silicone for mask manufacturing. Procurement and manufacturing efficiency are critical at this stage, as intellectual property surrounding proprietary algorithms and noise reduction technology forms a key competitive differentiator. High R&D investment is centered upstream to develop lighter, more ergonomic designs and integrate sophisticated connectivity features (e.g., Bluetooth, Wi-Fi modules). The quality and consistency of mask components are paramount, as mask comfort is directly linked to patient adherence, dictating strong relationships with specialized material suppliers.

Moving through the midstream, the core activities include final device assembly, rigorous quality control, and regulatory clearance processes, which are significantly complex given the device's life-sustaining role. The Distribution Channel forms the most crucial link between manufacturing and the patient. Distribution is bifurcated into direct and indirect channels. Direct channels involve manufacturers selling directly to large hospital networks or national defense agencies. Indirect channels, which dominate the market for home use, rely heavily on Durable Medical Equipment (DME) providers, who manage insurance verification, initial patient setup, and subsequent sales of necessary consumables. E-commerce platforms are rapidly gaining traction, particularly for replacement parts and travel units, bypassing traditional DME limitations and offering greater pricing transparency to consumers.

Downstream Analysis focuses on the post-sale customer relationship, encompassing installation, ongoing technical support, and the critical recurring revenue stream derived from consumables. This stage is pivotal for compliance management; manufacturers increasingly use connected health platforms and telemonitoring to track usage data, which informs the patient, physician, and DME provider regarding therapy effectiveness. The long-term success of a CPAP device manufacturer is therefore heavily reliant not just on the initial sale, but on the robustness of their support network and the consistent ability to supply masks and filters, tying the overall value proposition tightly to patient-centric services. The efficiency and reach of the DME network directly impact market share penetration in most regional markets.

The primary End-Users and Buyers of CPAP ventilators are individuals diagnosed with Obstructive Sleep Apnea (OSA), ranging across all adult demographics, though concentrated heavily in the 40+ age bracket. These patients, often categorized by comorbidities such as obesity, hypertension, and diabetes, represent the vast majority of direct consumers. These individuals make purchasing decisions heavily influenced by recommendations from sleep specialists and pulmonologists, but the final choice is often driven by factors like device comfort, noise levels (crucial for bed partners), and portability. Since the purchase is usually mediated by health insurance or government programs in developed markets, DME providers act as essential financial intermediaries guiding the patient through product selection and coverage.

Secondary but critical customers include institutional buyers such as specialized Sleep Laboratories and Diagnostic Centers. These centers require CPAP and BiPAP devices for titration studies—a process where the necessary therapeutic pressure is determined—and for temporary patient use. Although these institutions purchase devices in bulk, their demand is generally lower than the continuous, widespread demand from home users. Similarly, Hospitals and Acute Care Facilities utilize CPAP and BiPAP devices for Non-Invasive Ventilation (NIV) in various acute respiratory distress scenarios, requiring devices that are robust, versatile, and compatible with hospital monitoring systems, often favoring premium-priced, multi-functional units.

The evolving healthcare landscape is broadening the customer base to include large corporate wellness programs and military organizations that prioritize addressing sleep disorders due to their direct impact on productivity, safety, and operational readiness. These organizations often engage in direct procurement or centralized supply agreements for large quantities of connected CPAP devices. Ultimately, manufacturers must tailor their sales strategies to address three distinct purchasing motivations: the individual patient focused on comfort and usability, the institutional buyer focused on clinical reliability and fleet management, and the intermediary (DME/insurance) focused on cost-effectiveness and compliance data.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $4.5 Billion |

| Market Forecast in 2033 | $7.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ResMed, Philips Respironics, Fisher & Paykel Healthcare, 3B Medical, DeVilbiss Healthcare, Apex Medical, Vyaire Medical, Löwenstein Medical, Medtronic, GE Healthcare, Mindray, SLEEP8, Invacare, Drive DeVilbiss Healthcare, Curative Medical, BMC Medical, Nidek Medical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the CPAP Ventilators Market is defined by a strong emphasis on acoustic engineering, connectivity, and algorithmic intelligence designed to maximize therapy efficiency and user comfort. Noise reduction technology, utilizing sophisticated motor design and acoustic baffling materials, is a non-negotiable feature for modern devices, as noise is a primary deterrent to long-term compliance for both the user and their partner. Miniaturization technology allows for the creation of high-power, yet extremely portable components, driving the success of the travel CPAP segment. The mechanical innovation focuses on improved humidification systems, which are essential to prevent airway drying and irritation, often featuring heated tubes and integrated water chambers that are easier to clean and maintain.

The most significant technological shift is the transition from purely mechanical devices to sophisticated connected health platforms. Almost all premium CPAP devices now incorporate wireless communication capabilities (Wi-Fi or cellular) to transmit usage data to secure cloud platforms, enabling Remote Patient Monitoring (RPM). This data connectivity facilitates compliance tracking, remote troubleshooting, and allows physicians to remotely adjust pressure settings or identify necessary equipment replacement. This ecosystem creates value beyond the hardware itself, cementing the importance of proprietary data analysis software and user-friendly patient applications that integrate coaching and usage feedback.

Furthermore, the development of advanced proprietary algorithms, such as those used in APAP and BiPAP devices, relies heavily on sensor technology (flow sensors, pressure transducers) to accurately detect complex flow limitations and determine the precise pressure required at any given moment. These algorithms are continuously refined using machine learning to predict breathing patterns and deliver proactive pressure support, thereby smoothing the transition between breaths and vastly improving the sensation of natural breathing during therapy. Future technological advancements are expected to focus heavily on mask-free delivery systems and further integration with broader digital health records and wearable fitness trackers.

The global CPAP Ventilators Market exhibits diverse maturity levels and growth trajectories across different geographical regions, largely influenced by healthcare expenditure, disease awareness levels, and regulatory frameworks. North America, encompassing the United States and Canada, currently holds the largest market share. This dominance is attributed to several critical factors: the exceptionally high prevalence of OSA (driven by lifestyle and demographic factors), highly developed and widely accessible diagnostic infrastructure (numerous sleep labs), high awareness among the general public and physicians, and robust reimbursement coverage provided by both private and public health insurance systems. The U.S. acts as a global leader in early adoption of the latest connected and AI-enhanced CPAP devices, maintaining a mature yet high-value market.

Europe represents the second-largest market, characterized by a fragmented regulatory environment and differing national healthcare systems (e.g., centralized NHS in the UK versus insurance-based models in Germany). Growth in Europe is stable, driven primarily by favorable demographic aging trends and centralized national guidelines that promote CPAP therapy as a primary, cost-effective treatment for OSA. Countries such as Germany, France, and the UK are key contributors, demonstrating high penetration rates and strong demand for premium features like humidification and integrated telemonitoring capabilities. Regulatory standards within the EU, particularly concerning medical device safety and data protection (GDPR), significantly influence market entry and product deployment strategies.

The Asia Pacific (APAC) region is projected to experience the fastest growth rate during the forecast period. This rapid expansion is fundamentally driven by a massive, largely undiagnosed patient population, rapid improvements in healthcare infrastructure, increasing disposable incomes, and greater exposure to Western lifestyle factors associated with OSA risk. While pricing sensitivity remains a factor in developing nations within APAC, increasing medical tourism and government initiatives focused on chronic disease management (especially in China, India, and Japan) are accelerating the adoption of CPAP technology. This region represents the largest untapped potential, requiring manufacturers to adapt their products to localized distribution challenges and often focusing on entry-level, reliable devices before scaling up premium offerings.

The primary factor driving market growth is the escalating global prevalence of Obstructive Sleep Apnea (OSA), which is highly correlated with rising rates of obesity and the aging population demographic worldwide. Technological advancements improving patient comfort and adherence further accelerate adoption.

Standard Fixed CPAP delivers a constant, set air pressure throughout the night. APAP devices automatically adjust the pressure delivery dynamically based on the user's real-time breathing requirements. APAP devices are currently dominating segment growth due to superior patient comfort and enhanced compliance rates.

The biggest restraint is the issue of patient adherence, often linked to discomfort associated with the mask interface, noise from the device, and side effects like dry throat. High costs of the equipment and recurring replacement accessories also contribute significantly to poor compliance.

The Asia Pacific (APAC) region is forecast to demonstrate the highest growth rate. This is due to rapidly improving healthcare infrastructure, rising awareness of sleep disorders, and a vast, largely undiagnosed patient pool in populous nations like China and India.

AI transforms CPAP by analyzing complex sleep data to personalize therapy (dynamic pressure optimization) and enabling robust remote patient monitoring (RPM). This data-driven approach enhances therapeutic effectiveness, improves patient adherence, and facilitates predictive clinical intervention.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.