ID : MRU_ 437314 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

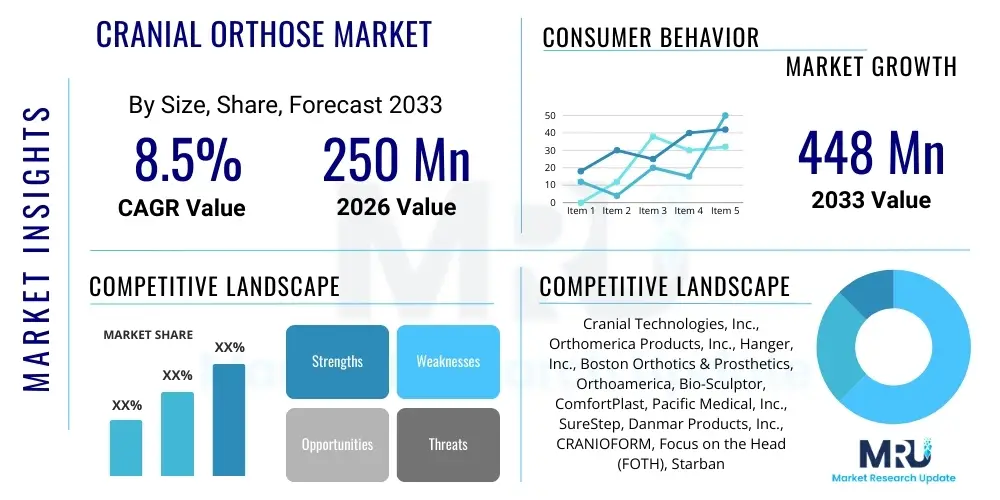

The Cranial Orthose Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 250 million in 2026 and is projected to reach USD 448 million by the end of the forecast period in 2033.

The Cranial Orthose market encompasses the products and services dedicated to treating positional plagiocephaly, brachycephaly, and other forms of cranial asymmetry in infants, primarily through the use of custom-fabricated helmets or bands. These therapeutic devices, often referred to as cranial remolding orthoses, function by applying gentle, corrective pressures to specific areas of the rapidly growing infant skull while providing relief to the flattened areas, thereby guiding symmetrical growth. The necessity for these orthoses is primarily driven by an increased awareness among pediatricians and parents regarding the prevalence of positional head deformities, which have seen a rise corresponding to the implementation of the "Back to Sleep" campaign aimed at reducing Sudden Infant Death Syndrome (SIDS). While highly effective when initiated during the optimal treatment window (typically between 4 and 8 months of age), these devices require frequent clinical adjustments and precise fitting, emphasizing the complexity of the service delivery component within this specialized medical device sector.

Product development within the Cranial Orthose sector is heavily focused on optimizing patient compliance and comfort, leveraging materials that are lightweight, durable, and biocompatible, such as high-density polyethylene shells lined with foam or proprietary padding materials. The application spectrum is primarily pediatric, centered on mitigating moderate to severe forms of deformational plagiocephaly (DP) which, if left untreated, can lead to potential long-term issues such as facial asymmetry, mandibular misalignment, and vision problems, though clinical evidence on the necessity for treatment of mild cases remains a subject of ongoing debate. Major applications include corrective molding post-birth trauma, treatment of torticollis-related head shape issues, and addressing asymmetries resulting from prolonged supine positioning. The efficacy of cranial orthoses is intrinsically linked to early diagnosis and rapid intervention, driving significant effort into improving screening protocols in neonatal and pediatric care settings.

The core benefits derived from cranial orthotic treatment involve achieving aesthetic symmetry, which positively impacts psychosocial development, and correcting functional asymmetries that might interfere with occlusal relationships or visual tracking later in life. Key driving factors accelerating market expansion include significant advancements in 3D scanning technology, which has dramatically reduced the time and invasiveness of the measurement process, leading to more precise and faster fitting of custom devices. Furthermore, rising disposable income in developing regions and robust insurance coverage for orthotic devices in established markets contribute significantly to the high adoption rates. Increased professional education programs aimed at pediatricians and family practitioners further solidify the referral pipeline, ensuring that infants who qualify for treatment are identified within the critical time frame necessary for successful outcomes.

The Cranial Orthose Market is experiencing dynamic business trends characterized by a shift toward highly personalized, technology-driven manufacturing processes, emphasizing rapid prototyping and advanced clinical management software. Current market dynamics reveal intense competition focused on service excellence and clinical efficacy, rather than purely product hardware cost, given the bundled nature of the treatment (device plus mandatory clinical visits and adjustments). Key stakeholders, including orthotic manufacturers and specialist clinics, are heavily investing in proprietary digital platforms that integrate initial 3D scans, design modifications, and long-term patient monitoring data, creating significant barriers to entry for new entrants. Furthermore, global business strategies increasingly incorporate aggressive expansion into emerging Asian Pacific markets where rising birth rates and improving pediatric healthcare infrastructure present untapped commercial opportunities, moving beyond the traditionally saturated North American and Western European landscapes.

From a regional perspective, North America remains the dominant market segment, primarily due to high healthcare expenditure, widespread insurance coverage for orthotic treatment, and established clinical guidelines that facilitate early intervention referrals. However, the Asia Pacific (APAC) region is poised to exhibit the highest Compound Annual Growth Rate (CAGR) over the forecast period, driven by increasing affluence, greater penetration of Western medical practices, and growing urbanization leading to higher awareness levels among parents. Europe maintains a steady growth trajectory, characterized by fragmented national healthcare systems where reimbursement policies significantly dictate market access and device adoption rates. Regional trends are also influenced by localized regulatory environments; for instance, certain European countries favor passive repositioning methods for mild cases, while North America more aggressively utilizes orthotic intervention for moderate classifications, creating nuanced demand patterns across continents.

Segmentation trends indicate that positional plagiocephaly remains the largest application segment due to its higher prevalence compared to brachycephaly and other complex conditions. Device technology is increasingly segmenting based on manufacturing technique, with 3D-printed orthoses gaining traction rapidly over traditionally molded or thermoformed shells. While thermoforming remains the cost-effective standard, 3D printing allows for superior ventilation, decreased weight, and faster turnaround times, appealing particularly to affluent consumers seeking optimal customization and comfort for their infants. The market is also seeing segmentation based on age group, though the 4-8 month window is critically important; there is growing interest in identifying and treating infants outside this traditional window, requiring adaptive designs and expanded clinical protocols. The overarching trend across all segments is the increasing convergence of clinical service and advanced digital manufacturing, underscoring the shift from a pure device sale model to a comprehensive therapeutic service offering.

Analysis of common user questions regarding AI's influence reveals core themes centered around efficiency, personalization, and diagnostic accuracy in the cranial orthose domain. Users frequently inquire about how AI can expedite the design process (currently reliant on skilled technician input), if AI algorithms can predict optimal growth correction pathways, and whether automation will reduce the cost barrier associated with custom-fitted devices. Concerns also revolve around data privacy related to sensitive 3D infant scans and the reliability of AI-driven recommendations compared to experienced clinician judgment. The prevailing expectation is that AI will primarily serve as a powerful clinical assistant, enhancing the speed and precision of diagnosis and customization, particularly through analyzing complex morphological data derived from 3D scans, thereby improving therapeutic predictability and potentially broadening access to timely treatment.

The Cranial Orthose market is propelled by key drivers, most notably the growing incidence rates of deformational plagiocephaly and brachycephaly, directly linked to prevailing safe sleep recommendations that encourage supine positioning. This demographic factor provides a steady and growing patient pool. Furthermore, intensive parental education campaigns and improved screening mechanisms implemented in maternity wards and early pediatric check-ups have significantly boosted the early diagnosis and referral rates necessary for effective orthotic treatment. The technological leap afforded by non-invasive 3D digital scanning technologies (Structured light scanning, Photogrammetry) drastically improves the patient experience by eliminating the need for plaster casting, thereby increasing compliance and streamlining the entire workflow from assessment to final device fitting, solidifying these drivers as continuous forces.

However, significant restraints temper the market’s aggressive growth potential. The most pronounced restraint is the high cost associated with the complete orthotic treatment protocol, which includes the custom device, multiple follow-up adjustments, and specialist consultation fees. While coverage is improving, inconsistencies in insurance and reimbursement policies across various geographical regions remain a substantial financial barrier for many families. Furthermore, the limited availability of highly specialized orthotists and clinicians trained specifically in cranial remolding techniques, especially in rural or underdeveloped areas, restricts market penetration and timely access to care. The necessity for the device to be fitted within a narrow, critical age window (typically before 12 months) means that delayed diagnosis often renders the treatment ineffective or unnecessary, creating a logistical bottleneck in the patient journey.

Opportunities for expansion are primarily concentrated around adopting advanced manufacturing technologies and expanding into underserved regions. The advent of high-resolution 3D printing (Additive Manufacturing) offers the potential for lighter, more breathable, and highly customized orthoses, potentially reducing material waste and production lead times, thereby enhancing overall service efficiency and profitability. Moreover, the opportunity exists in developing predictive modeling and telehealth solutions. Integrating remote monitoring tools and AI-driven analysis allows clinicians to manage patient progression remotely, especially for follow-up adjustments, decreasing the burden on clinic infrastructure and extending clinical expertise to geographically distant populations. The market also presents an opportunity for developing standardized global training curricula to increase the number of qualified practitioners and harmonize clinical outcomes, addressing the current skills gap restraint.

The Cranial Orthose Market is comprehensively segmented across several key dimensions, primarily delineated by application type, material utilized, technology implemented in manufacturing, and end-user profile. This structured categorization allows for a granular understanding of demand variations and innovation hotspots within the industry. The primary driver for segmentation is the specific morphological presentation of the cranial asymmetry, dictating the type of orthosis required. Given the necessity for bespoke fitting and continuous clinical monitoring, the market leans heavily toward high-value, service-intensive segments rather than mass-produced commoditized devices. Analyzing these segments is crucial for manufacturers to tailor their product offerings and strategic distribution efforts, ensuring they effectively address the diverse clinical needs presented by the pediatric population requiring corrective cranial molding.

Application-based segmentation clearly highlights positional plagiocephaly as the dominant segment, attributing to its statistically higher incidence rate compared to brachycephaly and the relatively rare scaphocephaly. However, segments defined by manufacturing technology are undergoing the most significant transformation. While traditional thermoforming techniques based on plaster casts or block-outs still represent a substantial volume due to lower initial setup costs and familiarity, the future growth is firmly anchored in the Additive Manufacturing (3D Printing) segment. 3D printing offers unparalleled geometric complexity, allowing for optimized internal venting structures, reduced weight, and superior fit accuracy derived directly from high-resolution digital scans. This technological segmentation directly impacts the cost structure and time-to-delivery, factors critical to parent satisfaction and clinic efficiency.

Further segmentation includes the material used, typically differentiating between high-density polyethylene (HDPE) and proprietary thermoplastic polymers, chosen for their blend of rigidity and lightweight properties. The end-user segment is almost universally defined as pediatric specialty clinics and hospitals, which often house the necessary diagnostic imaging equipment and specialized orthotic personnel required for treatment initiation and long-up follow-up. Geographically, the market is broadly segmented into five major regions, each presenting unique challenges related to insurance penetration, public health awareness, and the existing density of specialized pediatric care facilities, necessitating localized marketing and regulatory adherence strategies to maximize penetration and profitability.

The Cranial Orthose value chain is highly specialized, beginning with the upstream analysis dominated by advanced material science and digital technology providers. Upstream involves the procurement of highly specific, medical-grade thermoplastics (like HDPE or biocompatible polyesters) and the development of sophisticated 3D scanning hardware and CAD/CAM software essential for design input. Key upstream activities focus on material formulation to achieve optimal strength-to-weight ratios and ensuring that 3D scanning systems provide micron-level accuracy necessary for effective orthotic molding. Partnerships and supply reliability at this stage are crucial, as fluctuations in material costs or availability of specialized digital imaging components directly impact final product pricing and lead times, subsequently affecting patient access and clinic scheduling efficiency.

The core manufacturing and midstream processes involve the sophisticated conversion of digital scan data into a physical, customized helmet. This stage includes the critical steps of digital modeling, virtual blocking and sculpting, and the final production via thermoforming or 3D printing. The downstream segment is defined by the rigorous distribution channel, which is inherently indirect due to the clinical nature of the product. Cranial orthoses cannot be sold directly to the consumer; they require clinical prescription, professional fitting by a certified orthotist, and ongoing clinical adjustments over several months. Distribution typically flows from the manufacturer to specialized orthotic and prosthetic (O&P) clinics or hospital-affiliated pediatric centers, where the high-touch clinical service is provided.

The dominant distribution model is highly personalized and service-driven, necessitating robust training and support networks maintained by the manufacturers for their clinical partners. Direct distribution, although limited, primarily occurs when large manufacturers own and operate their own chains of specialized clinics to maintain tight control over quality and clinical outcomes. Indirect channels—involving independent O&P providers, distributors specializing in pediatric medical devices, and institutional contracts with major hospital systems—form the bulk of the market throughput. The success of the downstream operation relies heavily on efficient supply logistics to minimize the waiting period for the infant, as time is a crucial clinical factor, reinforcing the necessity for localized or distributed manufacturing hubs in key regional markets to optimize turnaround times.

The primary end-users and buyers of cranial orthoses are inherently the parents or legal guardians of infants diagnosed with moderate to severe positional cranial deformities, such as plagiocephaly or brachycephaly. However, the purchase decision and procurement process are mediated almost entirely by specialized healthcare providers and institutional payers. Therefore, the core customer base functionally includes pediatric specialists, neurosurgeons, and, most critically, Certified Orthotists (C.O.) operating within dedicated Pediatric Specialty Clinics and Orthotic and Prosthetic (O&P) Centers. These clinical entities act as gatekeepers, diagnosing the condition, prescribing the device, and managing the lengthy treatment cycle, making them the direct purchasing influencers and often the contractual buyers from manufacturers.

Hospitals, particularly those with strong maternal and neonatal care units, represent a crucial institutional customer segment. These facilities often establish contracts with orthose manufacturers to ensure immediate access to scanning equipment and custom fitting services for referred patients. The procurement process in this setting is driven by clinical effectiveness, ease of integration with existing hospital systems (e.g., electronic health records), and favorable contract pricing negotiated on behalf of payer systems or government entities. Furthermore, the payer ecosystem, including private health insurance companies and governmental healthcare schemes (like Medicare/Medicaid in the US or national health services in Europe), fundamentally dictates market uptake by establishing coverage criteria and reimbursement rates, positioning them as powerful indirect customers whose policies shape patient accessibility.

Geographical variance introduces segmentation within potential customers. In North America, the customer interaction is highly consumer-driven, where parents actively seek out specialists, often guided by insurance networks, making patient outreach and awareness vital marketing tools. Conversely, in many European countries, the customer flow is centrally managed through the national health system, where procurement relies on tenders and adherence to standardized clinical pathways defined by public health authorities. Ultimately, maximizing market reach requires comprehensive engagement with all three customer levels: the end-user (parents, focused on comfort and aesthetics), the prescriber (clinician/orthotist, focused on efficacy and ease of use), and the payer (focused on cost-effectiveness and outcome data).

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 250 million |

| Market Forecast in 2033 | USD 448 million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cranial Technologies, Inc., Orthomerica Products, Inc., Hanger, Inc., Boston Orthotics & Prosthetics, Orthoamerica, Bio-Sculptor, ComfortPlast, Pacific Medical, Inc., SureStep, Danmar Products, Inc., CRANIOFORM, Focus on the Head (FOTH), Starband, SureScan, Molds for Change, Clarity Orthoses, Freedom Prosthetics and Orthotics, NextStep Bionics & Prosthetics, Inc., The Orthotic & Prosthetic Center, Becker Orthopedic. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution of the Cranial Orthose market is heavily reliant on advanced digital imaging and computer-aided design, fundamentally transforming a historically artisanal process into a highly standardized, engineering-driven workflow. The cornerstone of this transformation is the ubiquitous adoption of high-resolution 3D scanning technologies, including structured light scanning and photogrammetry. These systems capture the precise geometry of the infant’s head non-invasively, replacing older, messy, and potentially distressing plaster casting methods. The accuracy provided by these digital scans is paramount, as subtle variations in cranial vault shape dictate the success of the differential pressure application mechanisms inherent in the orthosis design. Furthermore, this digital capture allows for secure, long-term data storage and precise comparison of pre-treatment, mid-treatment, and post-treatment morphologies, significantly enhancing clinical data management and objective outcome assessment, which is vital for clinical validation and payer justification.

Following the digital capture, Computer-Aided Design and Manufacturing (CAD/CAM) software plays the critical role of translating raw geometric data into a functional orthotic design. Specialized CAD platforms allow certified orthotists to virtually "block out" or sculpt the digital model, defining the exact areas where contact pressure must be applied to inhibit further growth and the relief areas where growth must be encouraged. Modern CAD/CAM systems are increasingly incorporating predictive modeling tools and AI-assisted design features, which suggest optimal orthotic parameters based on established clinical patterns, reducing the design cycle time and minimizing human error. The integration of 3D printing technology represents the pinnacle of current manufacturing capability, allowing for the direct fabrication of the orthosis from the digital model using Additive Manufacturing techniques. This bypasses the need for intermediary molds required in thermoforming, leading to decreased material usage, higher fidelity to the design, and the ability to create complex internal features, such as ventilation ports, that enhance patient comfort and compliance.

Material science innovation also forms a key part of the technology landscape, focusing on developing lighter, more durable, and hypoallergenic thermoplastic polymers. These advanced materials must withstand continuous wear (up to 23 hours a day) while maintaining the structural integrity necessary to exert consistent corrective forces. Research is ongoing into smart materials or embedded sensor technologies that could potentially monitor skin temperature, humidity levels, and pressure distribution in real-time. Although currently niche, such advancements promise a future where clinicians receive constant telemetry data, allowing for immediate, highly targeted micro-adjustments to the treatment protocol, moving towards a truly data-driven, closed-loop orthotic system. The collective impact of 3D scanning, sophisticated CAD/CAM, and advanced additive manufacturing cements the market's high technology orientation, driving quality improvements and enhanced patient outcomes.

North America, particularly the United States, holds the largest market share in the Cranial Orthose sector, driven by several compounding factors that establish high market maturity and penetration. The region benefits from exceptionally high public and professional awareness regarding positional cranial deformities, partially resulting from robust marketing efforts by major market players and well-established pediatric guidelines that endorse early orthotic intervention. Furthermore, the healthcare reimbursement landscape, characterized by generally strong private insurance coverage for cranial orthoses, significantly reduces the financial barrier for patients, leading to higher rates of treatment uptake compared to other regions. Clinical infrastructure is also highly developed, featuring a dense network of specialized pediatric clinics, dedicated orthotic and prosthetic centers, and highly trained certified orthotists capable of managing complex cranial remolding protocols, securing its position as the primary revenue generator.

The U.S. market is characterized by intense competition among well-established domestic manufacturers who continuously innovate in service delivery models, often integrating technology such as proprietary 3D scanning devices and unique helmet designs. Regulatory pathways, managed by the FDA, are well-defined, providing a clear framework for product introduction and safety validation, fostering confidence among healthcare providers. Canada, while smaller in volume, follows similar clinical and technological trends, albeit with variations in provincial healthcare funding models influencing access. The high average cost per treatment cycle in North America, combined with the high volume of diagnosed cases, firmly anchors this region as the global leader in terms of market valuation.

Key strategic focus areas in North America include expanding clinical capacity to meet demand surges, especially in metropolitan areas, and investing in AEO-optimized digital outreach programs targeting new parents searching for information on plagiocephaly treatment. Ongoing clinical studies aimed at quantifying long-term functional and aesthetic outcomes further strengthen the evidence base required for continued robust reimbursement. The market here is highly receptive to technological upgrades, positioning it as the primary testing ground for next-generation 3D-printed devices and remote monitoring capabilities, seeking efficiencies within the high-cost healthcare system.

The European market presents a complex picture, defined by significant heterogeneity in healthcare financing, clinical consensus, and regulatory approaches across different countries. Western European nations, including Germany, the UK, and France, exhibit high per-capita spending on healthcare and moderate market penetration, supported by national health service provisions or state-subsidized schemes that often cover necessary orthotic intervention, though criteria for coverage can be stringent. Germany, in particular, showcases strong adoption rates supported by a highly respected network of orthotic technical centers and a strong emphasis on clinical documentation and quality control. Conversely, Eastern European countries represent emerging growth areas where market penetration is lower due to fragmented healthcare budgets and lower public awareness of the condition and available treatment options.

Market growth in Europe is steady, buoyed by incremental improvements in early diagnosis protocols and the harmonization of clinical practice standards under European Union guidelines. However, a major limiting factor is the prevailing clinical controversy in some locales regarding the necessity of orthotic treatment versus conservative management (e.g., repositioning) for mild to moderate cases, which can slow referral rates. Manufacturers operating in this region must navigate complex tender processes and demonstrate cost-effectiveness rigorously to secure contracts within public healthcare systems. Success requires tailored market entry strategies, adapting to local reimbursement rules and clinical preferences, which often prioritize national or regionally sourced medical devices.

Technological adoption lags slightly behind North America in terms of immediate 3D printing saturation, with thermoforming still dominating many segments due to its cost-efficiency, a primary consideration for many national health services. Future growth will be catalyzed by increasing physician education, particularly in Southern and Eastern Europe, and leveraging high-quality clinical data to overcome skepticism regarding the necessity of treatment. The focus is increasingly shifting toward demonstrating the long-term cost savings associated with preventing potential secondary complications linked to untreated cranial asymmetry.

The Asia Pacific region is projected to register the highest CAGR during the forecast period, transitioning rapidly from an underdeveloped market to a major growth engine for cranial orthoses. This acceleration is attributed to rapid economic growth, rising disposable incomes, significant improvements in pediatric healthcare infrastructure, and the increasing westernization of medical practices, which promotes higher acceptance of specialized corrective therapies. Countries like China, India, South Korea, and Japan are leading this surge. Japan and South Korea, with sophisticated medical systems and a high appreciation for aesthetic outcomes, already show solid market penetration, though constrained by smaller populations compared to the vast markets of China and India.

The vast population base of China and India represents an immense untapped patient pool. While overall awareness levels are still developing compared to Western nations, urbanization and the proliferation of digital health information are rapidly educating urban populations about positional deformities. The challenge remains the stark disparity between high-quality, specialty care available in major metropolitan centers and the limited access in rural areas. Manufacturers face the need to establish efficient supply chains and educational programs to train local orthotists and clinicians in best practices for diagnosis and fitting, a critical element given the region's diverse clinical skill landscape.

Investment in localized manufacturing, including the establishment of regional 3D printing facilities, is a critical strategic imperative for companies targeting APAC. The market is highly price-sensitive in many sub-regions, necessitating the development of cost-effective distribution models and potentially lower-cost, high-volume product variants. The long-term trajectory is extremely positive, driven by high birth rates and increasing parental willingness to invest in specialized pediatric care, making APAC the key focus area for market penetration strategies over the next decade. Success hinges on navigating complex regulatory environments and achieving cultural acceptance of orthotic devices.

The Latin American market is characterized by moderate market maturity, with penetration concentrated in economically stable countries such as Brazil, Mexico, and Chile. Demand for cranial orthoses is present, driven by an expanding middle class and improving private healthcare access. However, market growth is often constrained by significant economic volatility, inconsistent public healthcare funding for specialized devices, and low levels of insurance penetration compared to North America. The market generally operates on a cash-pay or limited reimbursement model, making affordability a major determinant of patient uptake, restricting treatment access primarily to affluent urban centers.

Clinical infrastructure development is progressing, but the availability of highly specialized pediatric orthotists is limited, particularly outside major capital cities. This scarcity necessitates significant investment by manufacturers in clinical training and professional development programs to build a sustainable network of skilled practitioners. Imported devices dominate the high-end segment, while local manufacturers often compete on price with simpler, thermoformed solutions, suggesting a bifurcation in market quality and accessibility based on socioeconomic standing.

Future growth will rely on establishing stronger partnerships with local distributors and advocating for the inclusion of cranial orthosis treatment in national health programs. Digital technologies, particularly telehealth for initial consultations and follow-up checks, offer a strong opportunity to overcome geographical barriers inherent in LATAM’s expansive territories. Successful market entry demands strategies that balance high-quality products with price points sensitive to regional economic realities.

The Middle East and Africa represent the smallest segment but offer localized high-potential niches, particularly within the affluent Gulf Cooperation Council (GCC) countries (Saudi Arabia, UAE, Qatar). These nations boast high per-capita healthcare spending, modern clinical infrastructure, and a reliance on advanced Western medical technologies. The demand for cranial orthoses in these regions is driven by high-quality standards and readily available specialized pediatric care, often catering to expatriate and wealthy local populations who prioritize access to best-in-class treatments.

Conversely, the African continent, excluding South Africa, faces significant challenges, including extremely low awareness, limited healthcare budgets, and infrastructural deficits. Cranial orthoses are often considered non-essential specialized care, prioritizing management of infectious diseases and basic healthcare needs. The market penetration is minimal, limited to isolated humanitarian efforts or specialized university teaching hospitals that handle complex craniofacial cases.

Strategic focus in MEA involves targeting the GCC nations with premium products and service models, leveraging medical tourism trends, and engaging with governmental health initiatives that emphasize maternal and child health. For the broader African market, penetration requires sustainable, low-cost solutions and collaborative efforts with NGOs and public health bodies to address the underlying lack of infrastructure and basic clinical training, representing a long-term developmental opportunity rather than an immediate revenue driver.

The optimal treatment window is generally between 4 and 8 months of age. Intervention during this period maximizes the effect of the orthosis because the infant's skull is growing rapidly, allowing for quicker and more effective guidance of symmetrical growth.

Coverage varies significantly by region and specific insurance plan. In North America, many private insurers cover the treatment, but high deductibles or inconsistent policies remain a barrier. The total cost of the device and associated clinical services (which can range from $2,000 to over $4,500) heavily impacts market adoption, particularly in regions with limited public funding.

3D printing (Additive Manufacturing) allows for superior customization, reduced weight, and the creation of highly breathable designs directly from digital scans. This technology shortens production time, minimizes material waste, and significantly enhances patient comfort and clinical efficiency compared to traditional thermoforming methods.

Plagiocephaly involves asymmetrical flattening (oblique shape, often affecting one side of the head and face), while brachycephaly involves symmetrical flattening across the back of the head, resulting in a widened, short skull shape. Cranial orthoses are customized to address the specific growth inhibition pattern dictated by either diagnosis.

Market growth is primarily driven by heightened parental awareness stemming from safe sleep campaigns (increasing incidence), continuous technological advancements like non-invasive 3D scanning, and improved professional screening and referral protocols in pediatric healthcare settings globally.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.