ID : MRU_ 432518 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

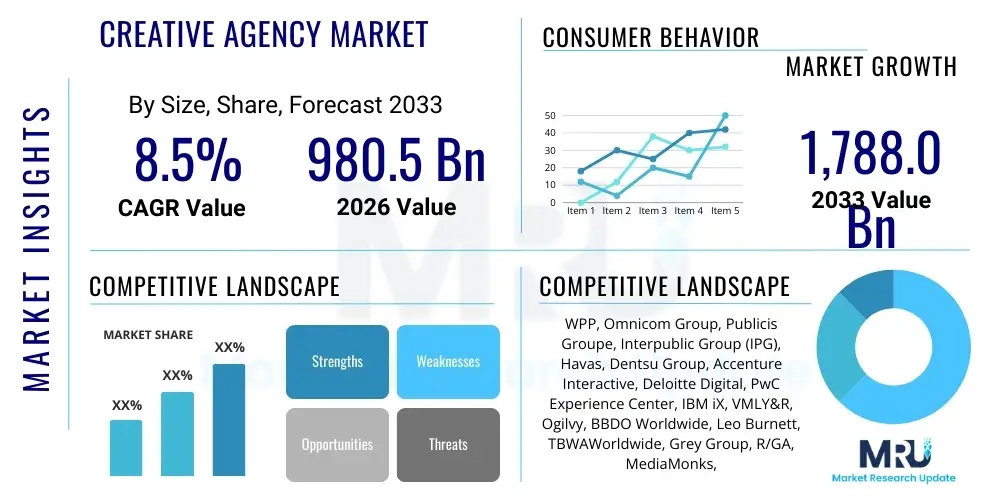

The Creative Agency Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $980.5 Billion USD in 2026 and is projected to reach $1,788.0 Billion USD by the end of the forecast period in 2033.

The Creative Agency Market encompasses firms specializing in developing strategic advertising campaigns, brand identity, marketing communications, and digital content creation for clients across diverse industries. These agencies serve as pivotal partners in navigating the complex modern media landscape, offering expertise in areas ranging from traditional media (print, television) to highly sophisticated digital platforms, data-driven personalization, and emerging technologies like augmented reality (AR) and virtual reality (VR). The core service offering revolves around translating client business objectives into compelling, executable creative strategies that resonate with target audiences and drive measurable commercial outcomes. This market is characterized by intense competition, rapid technological evolution, and a constant need for innovation in storytelling and audience engagement techniques. Agencies are increasingly shifting towards integrated models that combine creative execution with media planning and data analytics to provide holistic solutions.

Product descriptions within this market are multifaceted, primarily involving services such as full-service advertising, brand consulting, digital strategy, social media management, content production, experiential marketing, and public relations. Digital transformation remains the single most significant driver, pushing enterprises to invest heavily in robust online presences and personalized customer journeys, thereby increasing reliance on specialized digital creative agencies. Major applications span almost every consumer and B2B sector, including fast-moving consumer goods (FMCG), banking, financial services, and insurance (BFSI), retail, healthcare, technology, and automotive industries. The diversity of applications necessitates agencies possessing deep sector-specific knowledge and the ability to scale creative outputs globally while maintaining local cultural relevance.

The primary benefits derived from engaging creative agencies include enhanced brand equity, improved customer loyalty, accelerated market penetration, and optimized marketing spend through data-informed decisions. Key driving factors fueling market expansion involve the exponential growth of digital platforms, particularly mobile and video consumption; the necessity for brands to establish purpose-driven identities; and the proliferation of MarTech stacks requiring expert management and creative integration. Furthermore, the rising adoption of programmatic advertising and the constant evolution of search and social algorithms mandate continuous creative adaptation and professional agency support, positioning creative services as essential operational expenditures rather than discretionary marketing costs.

The global Creative Agency Market is undergoing a fundamental transformation driven by the confluence of digital media saturation and advancements in artificial intelligence. Business trends indicate a marked shift away from traditional retainer models toward project-based, specialized consulting, particularly focused on performance marketing and customer experience (CX) design. Large holding companies are actively restructuring and consolidating digital and data capabilities to compete effectively with technology consulting firms, which are aggressively entering the creative space. The emphasis is now placed on integrated offerings, where creativity is seamlessly blended with commerce, data science, and technology implementation. Sustainability and ethical branding have also emerged as crucial strategic components, influencing procurement decisions and agency selection criteria among major global clients, demanding transparency and accountability in creative execution.

Regionally, North America maintains its dominance due to high digital ad spending, the presence of major technological innovation hubs, and significant expenditure by key consumer goods and technology giants. However, the Asia Pacific (APAC) region is demonstrating the highest growth velocity, propelled by rapid internet penetration, rising middle-class consumerism, and the proliferation of localized social commerce platforms, notably in China and India. European markets are characterized by strong regulatory frameworks, such as GDPR, which necessitates sophisticated data-handling and personalized creative solutions. The Middle East and Africa (MEA) and Latin America (LATAM) are dynamic, emerging markets showing strong affinity for mobile-first creative content, driven by younger, digitally native populations.

Segment trends reveal that the Digital Agency segment is expanding fastest, largely overshadowing traditional media expenditures. Within services, content creation and management, particularly video and short-form content optimized for mobile devices, are the fastest-growing sub-segments. Programmatic creative optimization services are gaining prominence as brands seek to deliver dynamic, personalized messaging at scale. Furthermore, the end-user segmentation shows that the Technology and Telecommunications sectors remain primary revenue drivers, followed closely by the highly competitive Retail and E-commerce segments, which rely heavily on creative agencies for differentiation and transactional engagement strategies. Small and Medium Enterprises (SMEs) are increasingly utilizing smaller, boutique digital agencies due to cost-effectiveness and specialized expertise in niche digital channels, democratizing access to high-quality creative services.

Common user inquiries concerning the impact of Artificial Intelligence on the Creative Agency Market typically revolve around automation risk, data privacy implications, efficiency gains, and the future role of human creativity. Users frequently ask if AI will replace copywriters and designers, how agencies can leverage AI tools for personalization at scale, and what skills are necessary for creative professionals in an AI-dominated landscape. The consensus shows a dual perception: excitement over AI’s potential to automate repetitive tasks like basic content generation and media optimization, coupled with concern regarding intellectual property rights, algorithmic bias, and the potential devaluation of truly innovative human creative output. Users are keenly interested in understanding how AI-driven insights can improve campaign performance and client ROI, shifting the focus from manual execution to strategic oversight and ethical deployment of intelligent tools. This analytical demand underscores a critical need for agencies to pivot towards AI proficiency to maintain competitive edge.

The integration of AI technologies, including generative AI models (such as LLMs and image generators), predictive analytics, and sophisticated machine learning algorithms for audience targeting, is fundamentally reshaping the operational landscape of creative agencies. AI automates the mundane aspects of creative production, such as resizing images for multiple platforms, optimizing programmatic ad copy variations, and performing initial market research synthesis. This automation allows human creative professionals to concentrate on high-level strategic thinking, complex problem-solving, and the development of breakthrough concepts that require nuanced emotional intelligence and cultural understanding. AI tools are becoming indispensable for real-time campaign monitoring and optimization, providing agencies with unprecedented speed and accuracy in making mid-campaign adjustments based on granular performance data, thereby maximizing client value.

However, the widespread adoption of AI also introduces significant ethical and legal challenges, particularly concerning data ownership, copyright infringement stemming from generative models trained on proprietary data, and ensuring fairness in targeting algorithms. Agencies must establish robust internal governance frameworks for AI usage, focusing on transparency and accountability to mitigate risks associated with bias amplification and misinformation. Ultimately, AI is not viewed as a replacement for human creativity but rather as a powerful co-pilot and catalyst, transforming the creative process into a highly iterative, data-informed partnership between human strategists and machine intelligence. The agencies that successfully integrate AI into their workflow, emphasizing ethical creativity and data security, are poised to capture substantial market share in the coming decade.

The Creative Agency Market is shaped by a powerful interplay of Driving forces (D), Restraints (R), Opportunities (O), and structural Impact Forces. The primary driver is the accelerating pace of global digital transformation, necessitating sophisticated content strategies across fragmented media landscapes. Brands must maintain continuous communication, which mandates constant creative output, fueling demand for agency services. Conversely, major restraints include intensifying pricing pressure and margin compression, largely due to the commoditization of basic digital services and increased in-housing of creative teams by large corporations. Opportunities abound in specialized areas such as Web3 marketing, metaverse activations, and highly regulated industries like pharmaceutical and financial services, which require niche compliance expertise coupled with advanced creative strategy. The structural impact forces include the consolidation of traditional agencies, the rapid ascension of technology consultancies into the creative domain, and profound shifts in data privacy regulations globally, notably the deprecation of third-party cookies, compelling agencies to reinvent measurement and personalization methods.

Driving forces specifically related to technology are compelling. The explosion of video content (short-form and long-form), the dominance of mobile platforms, and the mandatory shift towards first-party data strategies require complex integration of MarTech stacks, a task agencies are uniquely positioned to manage. Client demand for measurable Return on Investment (ROI) further drives the need for analytical rigor alongside creative flair, favoring agencies capable of demonstrating direct business impact. However, constraints related to talent acquisition and retention present a persistent challenge. The competitive market for skilled data scientists, creative technologists, and specialized UI/UX designers often leads to escalating operational costs for agencies. Additionally, economic uncertainties and marketing budget volatility during geopolitical instability can cause immediate project halts or significant expenditure cuts, acting as unpredictable restraints on sustained growth.

Opportunities for expansion are particularly concentrated in cross-border digital campaigns and the integration of e-commerce capabilities directly into creative content (Creative Commerce). As consumers expect frictionless transactions embedded within their discovery journey, agencies that master the integration of platforms like Shopify, Amazon, and social commerce tools into brand narratives gain significant competitive advantage. The long-term impact forces necessitate a pivot towards full-funnel thinking, where creative output is designed not just for awareness, but explicitly for conversion and long-term customer relationship management. Agencies must evolve from pure creative providers to strategic business consultants, addressing complex supply chain visibility, sustainability claims, and internal digital culture transformation, reflecting a profound structural change in the scope of agency responsibility.

The Creative Agency Market is comprehensively segmented based on Service Type, End-User Industry, and Agency Size, allowing for granular analysis of market dynamics and competitive positioning. Service type segmentation differentiates between foundational traditional advertising services and highly specialized digital offerings, reflecting the ongoing migration of budgets towards performance-driven digital channels. The rapid growth of integrated services signifies client preference for single-source agencies that can manage strategy, media planning, and creative execution holistically. End-user segmentation highlights the uneven distribution of marketing expenditure across major industries, with technology, retail, and finance consistently representing the largest segments due to their high marketing intensity and continuous need for innovation to navigate competitive landscapes and maintain relevance. Understanding these segments is crucial for agencies seeking to identify lucrative niches and tailor their service portfolios accordingly.

Segmentation by Service Type reveals that specialized digital services, including search engine optimization (SEO), performance marketing, social media marketing, and content creation optimized for programmatic distribution, command premium pricing and exhibit the highest growth rates. The integrated segment, combining traditional brand building with robust digital execution and data analytics, is highly valued by global corporations seeking consistency across all consumer touchpoints. Conversely, traditional creative services, while still relevant for mass-market reach (e.g., large-scale TV campaigns), are experiencing slower growth and often face margin pressure. This trend underscores the necessity for traditional agencies to rapidly upskill and acquire specialized digital capabilities, often through mergers and acquisitions, to remain competitive in the evolving market structure.

The End-User structure dictates the level of regulatory compliance and technological sophistication required from agencies. For instance, agencies serving the Healthcare and BFSI sectors must possess deep expertise in regulatory advertising compliance (e.g., FDA, financial disclosure rules), whereas those serving the Media and Entertainment industries prioritize cutting-edge content production and rapid campaign turnaround times. Segmentation by Agency Size reflects market polarization: large, multinational holding companies leverage scale and global reach, while smaller, boutique agencies thrive by offering highly specialized, agile, and cost-effective services, often focused on specific technological niches like blockchain or AR/VR development, catering efficiently to the unique needs of Small and Medium Enterprises (SMEs).

The value chain of the Creative Agency Market starts with Upstream Analysis, which focuses on the primary inputs essential for creative production. These inputs primarily consist of talent (creative directors, strategists, data scientists, technologists), research and data platforms (consumer insight tools, competitive intelligence software, audience data providers), and technology infrastructure (cloud services, specialized production software, generative AI platforms). The efficiency and quality of these upstream inputs directly determine the agency's ability to deliver innovative and effective campaigns. Agencies prioritize strategic partnerships with leading data providers and investment in continuous training to secure premium talent, recognizing that intellectual capital is the most critical asset in this knowledge-intensive industry. Procurement strategies often center on licensing high-fidelity data feeds and specialized MarTech components necessary for modern programmatic and personalized advertising campaigns.

The core activities involve Strategy Development, Creative Execution, Media Planning and Buying, and Performance Measurement. Strategy development transforms client briefs into actionable creative roadmaps, informed heavily by upstream data analysis. Creative Execution involves the actual production of assets (copy, visual, video), demanding sophisticated production facilities or outsourcing relationships. Media planning and buying are critical functions, increasingly relying on automated, programmatic platforms to ensure optimal placement and price efficiency across complex distribution channels. The Downstream Analysis focuses on the delivery of the final campaign to the end-client and the target consumer. Distribution channels are highly diverse, encompassing direct digital channels (social media, search engines, owned websites), traditional broadcast media, and emerging experiential platforms. Effective downstream management requires real-time monitoring and reporting to demonstrate campaign effectiveness and client ROI.

Distribution channels are categorized into direct and indirect methods. Direct channels involve the client engaging the agency directly for services, which is common for large, retained accounts and specialized projects. Indirect channels include agencies operating within large holding company networks, leveraging shared resources, and receiving mandates through corporate procurement processes or via technology platform partnerships (e.g., agencies recommended by Google or Meta). The integration of Direct and Indirect capabilities, particularly through robust digital dashboards and client service portals, enhances transparency and accountability, strengthening client-agency relationships. Ultimately, the successful delivery of value is measured by the campaign's impact on the client’s brand equity and sales performance, driving repeat business and sustained market presence for the agency.

The potential customers, or end-users/buyers, of creative agency services are exceptionally diverse, spanning nearly every economic sector where brand visibility, customer acquisition, and retention are strategic priorities. Large multinational corporations (MNCs), particularly those in highly competitive consumer-facing industries like FMCG, Automotive, and Retail, constitute the largest segment of high-value, long-term clientele, often utilizing integrated, global agency networks. These corporations require extensive services covering global brand strategy, localized campaigns across numerous markets, and complex media buying services. Their purchasing decisions are highly influenced by an agency’s track record in delivering measurable commercial outcomes, technological integration capabilities, and expertise in ethical and sustainable branding practices.

Mid-sized enterprises (MSEs) represent a high-growth segment, seeking cost-effective, specialized agency support, particularly in the digital realm. These clients often prioritize boutique agencies with proven expertise in areas such as performance marketing, advanced SEO, or platform-specific social media strategy, aiming for rapid market traction without the budget commitment required by global holding companies. Technology start-ups and Scale-ups are another crucial customer group, demanding agile, results-oriented branding and marketing services to achieve rapid user adoption and secure venture capital funding. For this group, the speed of execution and the ability to pivot creative strategy based on real-time data are paramount, often preferring agencies that act as extensions of their internal growth teams.

Furthermore, government and non-profit organizations are increasingly engaging creative agencies for public awareness campaigns, digital transformation initiatives, and behavioral change communications. These entities require agencies skilled in complex stakeholder management, public policy communication, and culturally sensitive messaging, often operating under strict budgetary and transparency requirements. The financial viability and long-term stability of the Creative Agency Market are intrinsically linked to the sustained marketing expenditure across these varied customer segments, with digital budgets consistently driving the overall expenditure growth irrespective of the end-user industry.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $980.5 Billion USD |

| Market Forecast in 2033 | $1,788.0 Billion USD |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | WPP, Omnicom Group, Publicis Groupe, Interpublic Group (IPG), Havas, Dentsu Group, Accenture Interactive, Deloitte Digital, PwC Experience Center, IBM iX, VMLY&R, Ogilvy, BBDO Worldwide, Leo Burnett, TBWAWorldwide, Grey Group, R/GA, MediaMonks, Mother, Anomaly |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Creative Agency Market is defined by its deep reliance on advanced technological platforms that enable targeted, data-driven, and scalable creative execution. MarTech stacks form the foundation, incorporating Customer Relationship Management (CRM) systems, Data Management Platforms (DMPs), and Customer Data Platforms (CDPs) which aggregate and synthesize consumer data critical for personalized messaging. Agencies are increasingly becoming experts in integrating and managing these disparate systems for clients, transforming raw data into actionable creative insights. Specialized tools for production, such as cloud-based collaborative editing suites and high-fidelity rendering software, are essential for speeding up content creation cycles, particularly for video and 3D assets required for AR/VR experiences. The adoption of headless CMS solutions is also critical, allowing content to be created once and deployed seamlessly across multiple front-end digital interfaces.

Artificial Intelligence and Machine Learning represent the most disruptive technological force. Generative AI tools are used not just for generating preliminary creative assets (copy, images, mockups) but also for testing hundreds of ad variations simultaneously through dynamic creative optimization (DCO). Machine learning algorithms power predictive analytics, enabling agencies to forecast campaign performance metrics and optimize media spend in real-time, moving beyond retrospective reporting. Furthermore, agencies are investing heavily in technologies related to the emerging Web3 environment, including decentralized marketing platforms, non-fungible tokens (NFTs) for loyalty programs, and developing immersive experiences in virtual worlds (Metaverse), positioning themselves at the forefront of digital innovation for future-proofing client brands.

The technology landscape mandates high proficiency in security and compliance. Given the sensitive nature of first-party data handling, agencies must utilize robust cloud security protocols and demonstrate adherence to global privacy standards like GDPR and CCPA. The move towards cookieless identification methods necessitates expertise in privacy-preserving techniques such as contextual advertising and unified ID solutions. The successful creative agency of the future is fundamentally a technology company that embeds creative thinking, prioritizing tech infrastructure investments—particularly in data platforms and AI research—as central to their core offering, rather than merely relying on creative intuition alone to solve complex client business challenges.

North America, led by the United States, holds the largest market share in the Creative Agency sector globally. This dominance is primarily attributed to the presence of the world's largest holding companies, the highest per capita spending on advertising and marketing, and the early adoption of disruptive marketing technologies. The region benefits from a highly sophisticated and mature digital ecosystem, characterized by massive investment from technology giants in areas like programmatic advertising, video streaming, and data analytics. Major trends in this region include the aggressive competition between traditional creative agencies and technology consultancies (e.g., Accenture Interactive, Deloitte Digital) vying for large-scale digital transformation contracts. Agencies here are highly focused on demonstrating measurable ROI, leading to a strong emphasis on performance marketing, customer experience design, and complex MarTech integration projects. The demand for highly specialized talent in data science and ethical AI application is exceptionally high, driving operational costs but also fostering rapid innovation in creative delivery.

The North American market is highly fragmented yet dominated by a few major holding companies who continuously acquire niche digital and specialized firms to expand their service capabilities. The stringent regulatory environment, particularly regarding consumer data privacy (CCPA in California), forces agencies to develop sophisticated first-party data strategies for clients. The shift toward in-housing creative services among major brands presents a continuous challenge, compelling agencies to offer higher value, strategic consulting services beyond standard production work. Furthermore, the region remains the global benchmark for creative excellence and technological integration, often setting the precedent for global campaign strategies, especially concerning social media monetization and influencer marketing frameworks. Investment remains strong in emerging areas such as connected television (CTV) advertising and augmented reality experiences.

The European Creative Agency Market is characterized by a high degree of digital maturity coupled with a complex, localized regulatory landscape, notably the General Data Protection Regulation (GDPR). This regulatory environment necessitates that agencies prioritize data privacy compliance and ethical marketing practices, fundamentally shaping how data is collected, processed, and utilized for personalized advertising. Western European countries, particularly the UK, Germany, and France, represent major revenue centers, known for their strong emphasis on brand heritage, high-quality production values, and a growing focus on sustainability and corporate social responsibility (CSR) in creative messaging. Agencies operating in this region must master multilingual and multicultural campaign execution, navigating diverse consumer preferences across different member states while maintaining a unified brand voice.

Growth in Europe is concentrated in the digital and integrated segments, driven by businesses transitioning from traditional channels to e-commerce platforms and performance-based marketing. There is a notable trend towards specialization, with boutique agencies gaining prominence for their niche expertise in areas like health tech, fintech marketing, and luxury branding. The economic stability of the Eurozone often dictates advertising expenditure, making the market slightly sensitive to macroeconomic fluctuations. Eastern European nations are emerging as strong hubs for technical and creative production outsourcing due to competitive labor costs and high skill levels, further influencing the overall market structure. European clients are increasingly demanding transparency in media buying and programmatic supply chains, pushing agencies towards robust verification and auditing processes.

The Asia Pacific region exhibits the highest growth potential globally, driven by massive population scales, rapidly increasing internet and mobile penetration, and the emergence of highly sophisticated digital ecosystems, particularly in China, India, Southeast Asia, and Australia. This market is profoundly mobile-first, necessitating agency creative strategies optimized for small screens and local social commerce platforms (e.g., WeChat, TikTok equivalents). The vast cultural diversity and linguistic fragmentation across APAC demand exceptional localization capabilities, making market entry complex but highly rewarding for agencies that master regional nuance. Digital ad spend is skyrocketing, fueled by a booming middle class and aggressive investment in direct-to-consumer (D2C) models across retail and FMCG sectors.

Key drivers include the dominance of short-form video content and live commerce, requiring agencies to blend entertainment seamlessly with transactional capabilities (Creative Commerce). Unlike Western markets, APAC often relies on powerful super-apps, demanding integrated creative solutions that function within closed digital ecosystems. India and Southeast Asia are experiencing exponential growth due to young, digitally native populations adopting new platforms rapidly. Agencies in this region often operate in a high-speed, iterative environment, utilizing real-time data to swiftly adjust campaigns based on immediate consumer feedback. Competition is fierce, involving global holding companies, major Japanese and Chinese networks (like Dentsu and Publicis in China), and strong local independent agencies specializing in regional market penetration strategies.

The LATAM Creative Agency Market, spearheaded by Brazil and Mexico, is characterized by high mobile consumption rates, a strong affinity for social media platforms, and persistent economic volatility that often impacts marketing budgets. Agencies must be highly adaptable to rapid economic shifts and currency fluctuations, leading to a strong focus on cost-efficient digital solutions and measurable performance marketing. The consumer base is digitally savvy, demanding highly engaging, culturally relevant content. Creative output often leans heavily towards emotional storytelling and leveraging local celebrity and influencer endorsements due to high media trust in these figures.

The primary growth areas include digital transformation projects within the financial services and retail sectors, aiming to capture the unbanked and leverage the rapidly expanding e-commerce landscape. Challenges include infrastructure limitations in certain areas and a complex patchwork of regional regulations. Agencies successfully navigating LATAM often specialize in hyper-localizing global campaigns and building strong, transparent client partnerships to mitigate economic risk. There is growing interest in utilizing data analytics to improve targeting efficiency and counter the effects of marketing budget constraints, positioning data-driven creative as a key differentiator.

The MEA region presents a diverse market, with the GCC countries (UAE, Saudi Arabia) being major centers for high-value creative spend, particularly in the luxury, tourism, and real estate sectors. This segment is undergoing rapid digitization, fueled by government initiatives aimed at economic diversification and technological modernization. Creative agencies in the GCC often handle large-scale, high-budget campaigns tailored for high-net-worth individuals and major international events. Mobile usage and social media penetration are exceptionally high, driving demand for innovative digital and experiential marketing.

The African continent, particularly South Africa and Nigeria, represents a dynamic, rapidly emerging market characterized by leapfrogging technological adoption (mobile money, digital payments). Creative agencies here focus on building brand trust and relevance in diverse, often informal economies, prioritizing mobile-first content delivery. Across MEA, regulatory differences and sensitivities necessitate careful cultural calibration of creative messaging. The market is witnessing increased investment from global holding companies seeking to capitalize on the region's demographic growth and accelerating shift towards digital consumerism and personalized content experiences.

Digital transformation is fundamentally shifting agency revenue models from traditional fixed retainers, based on hours worked, to performance-based fees and project-specific contracts tied directly to measurable business outcomes, such as conversion rates or customer lifetime value. This emphasizes accountability and data-driven results over mere creative output.

The increase in in-house creative teams forces global agencies to pivot towards high-value strategic consulting, complex MarTech integration, and specialized production services (e.g., AR/VR). Agencies are moving away from routine production tasks, positioning themselves as expert partners for innovation, scale, and high-level brand strategy that in-house teams often lack the breadth to handle.

The Digital Agency service segment, particularly services related to performance marketing, programmatic creative optimization, and short-form video content creation optimized for mobile and social platforms, is projected to exhibit the highest Compound Annual Growth Rate (CAGR) due to sustained high digital ad expenditure globally.

Data privacy regulations compel creative agencies to abandon reliance on third-party data for targeting. Strategies are shifting towards first-party data activation, contextual advertising, and privacy-preserving creative personalization techniques, emphasizing transparency in data usage and prioritizing consumer trust in brand communications.

Generative AI acts as an efficiency accelerator, automating the drafting and production of diverse creative variations, allowing human creatives to focus on complex strategy, ideation, and defining the ethical guardrails for AI deployment. The future structure integrates AI as a strategic tool for rapid prototyping and maximizing campaign scalability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.