ID : MRU_ 438929 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

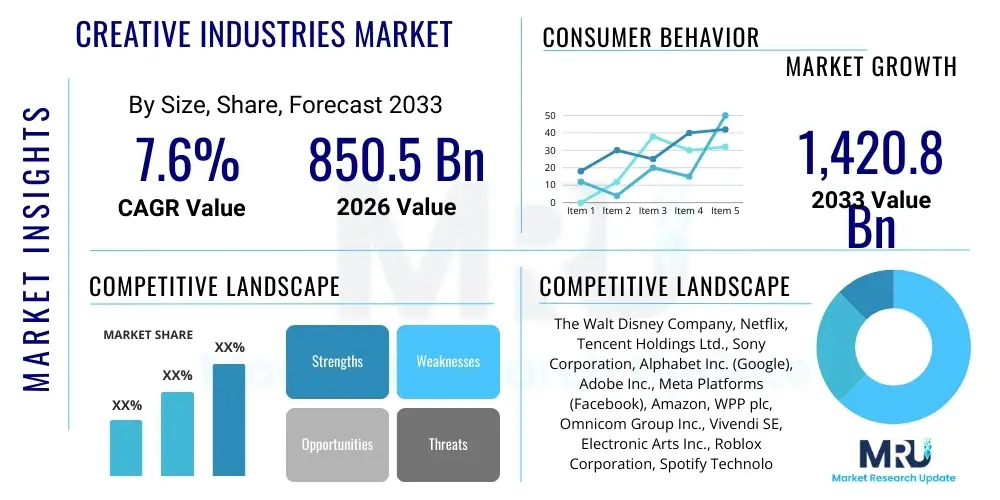

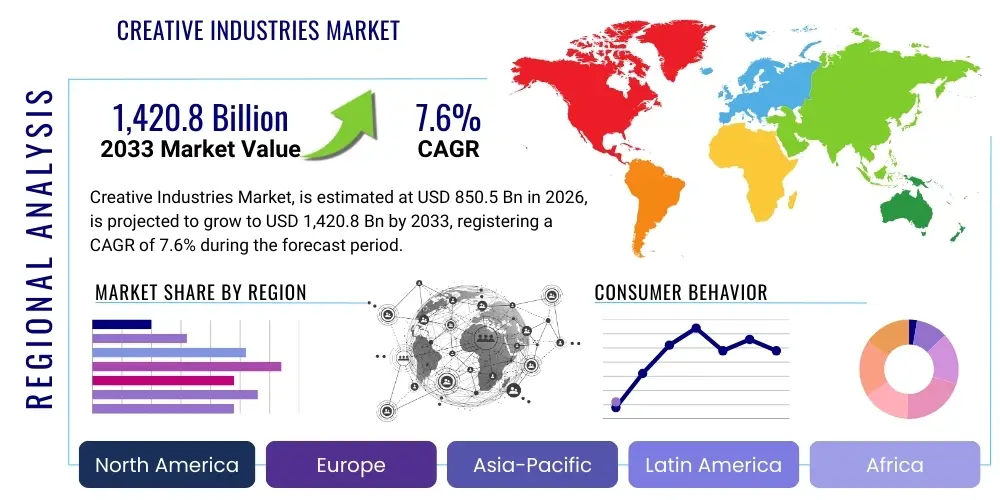

The Creative Industries Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.6% between 2026 and 2033. The market is estimated at $850.5 Billion USD in 2026 and is projected to reach $1,420.8 Billion USD by the end of the forecast period in 2033. This growth trajectory is fueled by increasing digitalization, rising global demand for entertainment content, and the integration of advanced technologies like Artificial Intelligence (AI) and Virtual Reality (VR) across various creative domains, fundamentally transforming production and consumption models.

The Creative Industries Market encompasses a wide spectrum of sectors that generate economic value through the creation or production of intellectual property, artistic expression, and cultural goods and services. Key segments include design, film and television production, advertising, music, publishing, gaming, and digital media. These industries serve as vital engines for cultural exchange and economic diversification, focusing on innovation, creativity, and skill-based expertise. The product offerings range from intangible services, such as brand consulting and architectural design, to tangible goods like printed books and video game software. Major applications span corporate marketing (advertising and branding), entertainment consumption (streaming services and cinema), educational content, and urban development (architecture and heritage management), reflecting the pervasive influence of creativity across global commerce.

The principal benefits derived from a robust Creative Industries Market include enhanced national branding, significant employment generation, and stimulation of cross-sectoral innovation. Furthermore, these industries drive digital transformation, necessitating constant adaptation and adoption of cutting-edge production tools and distribution platforms. The inherent value lies in converting cultural resources and individual talent into marketable economic assets, supporting a diverse ecosystem of freelancers, small enterprises, and multinational corporations. The ability of the creative sector to pivot quickly to technological changes, such as the shift from physical to digital distribution models, underscores its resilience and growth potential in the modern economy.

Driving factors propelling this market forward include substantial growth in internet penetration globally, particularly in emerging economies, which opens up new consumer markets for digital content and services. The proliferation of affordable smartphones and high-speed mobile data facilitates easy access to streaming media, online gaming, and digital publications. Moreover, corporate investment in immersive experiences (AR/VR advertising) and personalized content creation is surging, recognizing creativity as a core differentiator in competitive markets. Government initiatives supporting cultural heritage, intellectual property protection, and investment in creative education further stabilize and accelerate market expansion, ensuring a continuous supply of skilled talent and protected assets.

The Creative Industries Market is currently characterized by rapid digital convergence and technological disruption, particularly through AI integration and the metaverse concept. A primary business trend involves the consolidation of streaming platforms and content aggregators seeking greater market share and cost efficiencies, alongside a parallel rise in decentralized content creation fueled by Web3 technologies. Businesses are increasingly adopting project-based and hybrid work models, relying on global networks of creative talent, which necessitates robust digital infrastructure and secure collaborative tools. Financial metrics show a strong shift in revenue streams from traditional licensing and physical sales towards subscription models, micro-transactions (especially in gaming), and data monetization related to consumer behavior and content preferences.

Regionally, North America and Europe maintain dominance due to established intellectual property frameworks, high consumer disposable income, and the presence of global media conglomerates. However, the Asia Pacific (APAC) region is demonstrating the highest growth velocity, largely driven by massive populations adopting mobile-first entertainment (e.g., K-pop, Bollywood, and extensive mobile gaming markets). Latin America and the Middle East & Africa (MEA) are emerging as high-potential markets, leveraging unique cultural content and increasing governmental investment in digital infrastructure and creative hubs. Regional trends also show significant government support for localized content production to counteract cultural homogenization.

Segmentation trends highlight the increasing importance of the Digital Media and Gaming segments, which collectively command the largest market share and exhibit superior growth rates due to their high scalability and instantaneous distribution capabilities. Within the design sector, UX/UI design is experiencing explosive demand as businesses prioritize user-centric digital interfaces. Furthermore, the convergence of Advertising and Film/Video Production is evident, with brands acting increasingly as content creators. The shift toward bespoke, personalized, and interactive content across all segments ensures that creative services remain indispensable for consumer engagement in a fragmented media landscape.

User inquiries concerning AI's role in the Creative Industries frequently revolve around the dichotomy of displacement versus augmentation. Common questions center on the future of traditional creative jobs (e.g., graphic designers, copywriters, and concept artists) when confronted with sophisticated generative AI models capable of producing content rapidly and cheaply. Users seek clarity on ethical boundaries, particularly regarding copyright ownership of AI-generated content and the use of existing intellectual property in training datasets. Furthermore, there is significant interest in understanding how AI tools can be leveraged to streamline tedious production tasks, personalize consumer experiences, and unlock entirely new forms of creativity, moving beyond simple automation to genuine creative partnership between human and machine.

The consensus emerging from market analysis suggests that AI is primarily an augmentation tool that dramatically shifts the required skill set for creative professionals, emphasizing prompt engineering, curation, and strategic oversight rather than fundamental execution. While initial stages of content generation may be automated (e.g., generating preliminary design drafts or basic musical compositions), human expertise remains crucial for quality control, aesthetic judgment, cultural relevance, and ensuring emotional resonance. This transformation necessitates substantial investment in training programs focused on utilizing AI pipelines effectively, turning potential job displacement into a skill upgrade opportunity.

However, AI also introduces market dynamics that accelerate production cycles and lower the barrier to entry for content creation, leading to an explosion of digital assets. This saturation increases the competitive pressure on high-quality, unique, and culturally significant human-created content. Intellectual property management, traceability of data sources, and establishing clear legal frameworks for AI co-creation are therefore critical areas of market uncertainty and regulatory focus, impacting content licensing and monetization strategies across the entire creative value chain.

The Creative Industries Market is profoundly influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming crucial Impact Forces that dictate strategic decision-making. Key drivers include the exponential growth in digital connectivity, particularly mobile internet access, which democratizes content distribution and expands the global consumer base. Furthermore, the persistent demand from corporations for compelling and differentiated branding, advertising, and user experience (UX) design services ensures continuous investment in creative expertise. The rapid adoption of new technological platforms, specifically virtual and augmented reality (VR/AR), is opening lucrative avenues for immersive content creation and experiential marketing, solidifying technology as the primary positive impact force.

Conversely, significant restraints hinder optimal market growth. The pervasive issue of intellectual property theft and piracy, exacerbated by global digital distribution, continues to erode potential revenue streams and necessitates ongoing legal and technological investment in protection mechanisms. Skills gaps are another constraint; the fast pace of technological evolution, especially in AI and advanced VFX, means that the existing workforce often requires rapid re-skilling, which poses a bottleneck in project execution. Economic volatility, particularly recessions or geopolitical instability, often results in immediate cuts to discretionary spending, disproportionately affecting advertising budgets and high-end creative projects.

Opportunities for expansion are abundant, centered around emerging markets and specialized technologies. The potential for monetizing the metaverse and Web3 platforms offers creative professionals decentralized ownership models and new interaction modalities. Furthermore, the convergence of health, education, and creative content (edutainment/health tech) provides fertile ground for cross-sectoral collaboration and service diversification. Ultimately, the dominant impact force is the accelerating pace of technological innovation; its ability to both drive productivity gains and introduce profound regulatory and ethical challenges means market participants must prioritize agility, IP protection, and continuous technological integration to maintain competitive advantage.

The Creative Industries Market is analyzed across comprehensive segmentation strategies, primarily categorized by Type of Industry, Application, and Revenue Model. This structure allows stakeholders to delineate specific growth pockets, understand competitive landscapes within sub-sectors, and tailor investment strategies to high-yield domains. The Type segmentation isolates sectors like Film & Video, Music & Sound, Advertising & Marketing, and Gaming, each possessing distinct operational characteristics and value chain structures. The dynamism across these segments is high, particularly the continuous blurring of lines between traditional sectors, such as film studios expanding into gaming development, or advertising agencies adopting advanced VR production techniques.

Application-based segmentation divides the market based on the primary end-use of the creative output, such as Entertainment, Corporate Branding, Education, and Heritage/Tourism. This highlights that while entertainment remains the largest consumer of creative services, the corporate sector’s reliance on creative input for digital transformation and UX design is rapidly expanding. Revenue Model analysis reveals the critical transition away from one-off sales towards recurring revenue streams. Subscription models (e.g., SaaS platforms for design tools, streaming services) and micro-transaction models (prevalent in gaming) dominate modern market economics, signifying a shift in consumer behavior toward access over ownership.

Understanding these segments is crucial for strategic alignment and resource allocation. For instance, the Gaming segment demands high-frequency updates and advanced graphics technologies, requiring substantial capital expenditure in R&D, whereas the Publishing segment faces unique challenges related to print decline and the proliferation of digital reading platforms, necessitating strategic partnerships with distribution platforms. The inherent diversity ensures market stability, as different segments exhibit varying degrees of resilience to economic downturns and technological shifts, providing hedging opportunities for diversified creative conglomerates.

The value chain for the Creative Industries Market is intricate and highly specialized, beginning with the Upstream activities centered on idea generation, raw talent acquisition, and foundational intellectual property (IP) development. Upstream participants include individual artists, writers, composers, designers, and specialized talent agencies that scout and manage creative human capital. Investment in education, technology research (e.g., new CGI software), and cultural incubation centers are vital upstream components, ensuring a continuous supply of novel concepts and highly skilled professionals. The primary challenge upstream is protecting intangible assets and securing adequate funding for R&D, as creative concepts are highly susceptible to imitation before formal production.

The core Midstream phase involves the production, manufacturing, and technical execution of creative content. This includes film studios, recording houses, publishing presses, digital game developers, advertising production houses, and architectural firms. This phase is capital-intensive, requiring specialized equipment (e.g., rendering farms, sound stages) and sophisticated management of complex workflows and supply chains. The shift towards digital production has led to increased reliance on cloud-based collaboration tools and outsourced technical services (e.g., VFX rendering), enhancing efficiency but also introducing data security and latency risks.

The Downstream segment focuses on distribution, consumption, and monetization. This involves direct channels such as proprietary streaming platforms (e.g., Netflix, Spotify), direct-to-consumer sales (DTC), and retail outlets (physical books/art). Indirect channels heavily rely on aggregators, distributors, broadcasters, and platform intermediaries (e.g., app stores, social media networks). Successful downstream execution requires sophisticated data analytics to understand audience consumption patterns, enabling highly targeted marketing and personalized distribution strategies. The dominance of a few large digital platforms in the downstream sector presents significant market entry barriers for smaller content creators, making strategic partnerships critical for broad reach.

Potential customers for the Creative Industries Market are broadly segmented into three categories: Commercial Enterprises, Individual Consumers, and the Public Sector/Non-Profits. Commercial Enterprises represent the largest and most varied client base, including multinational corporations, SMEs, and startups across sectors like technology, finance, retail, and manufacturing. These clients require creative services primarily for competitive differentiation, brand building, product design (especially UX/UI design), and extensive marketing campaigns (digital and traditional advertising). Their buying decisions are driven by ROI, measurable impact on customer engagement, and the need for scalable, high-quality creative assets.

Individual Consumers serve as direct purchasers, predominantly within the Entertainment and Cultural segments. This includes subscribers to streaming services (SVoD, music), buyers of video games and in-game content, attendees of performing arts events, and purchasers of books and personalized artwork. This customer segment is highly sensitive to content quality, convenience of access, and price point. The rise of social media and influencer marketing has made individual consumers more informed and discerning, placing higher demands on authenticity and innovation in content offerings.

The Public Sector and Non-Profit organizations constitute a vital, albeit often overlooked, customer base. Governments utilize creative services for public campaigns (health, civic engagement), urban planning (architecture and public space design), and managing national cultural heritage sites (conservation, digital archiving, and tourism promotion). Non-profits rely on creative professionals for fundraising materials, educational programs, and advocacy campaigns. Their procurement processes often emphasize societal impact, transparency, and adherence to regulatory standards, differentiating them from pure commercial engagements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $850.5 Billion USD |

| Market Forecast in 2033 | $1,420.8 Billion USD |

| Growth Rate | 7.6% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | The Walt Disney Company, Netflix, Tencent Holdings Ltd., Sony Corporation, Alphabet Inc. (Google), Adobe Inc., Meta Platforms (Facebook), Amazon, WPP plc, Omnicom Group Inc., Vivendi SE, Electronic Arts Inc., Roblox Corporation, Spotify Technology S.A., Shutterstock, Inc., Autodesk, Inc., Condé Nast, Marvel Entertainment, Epic Games, Inc., Warner Bros. Discovery. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Creative Industries is undergoing a profound transformation, spearheaded by the widespread deployment of cloud computing and sophisticated digital creation suites. Cloud-based infrastructure enables real-time collaboration across geographically dispersed teams, critical for large-scale film production, complex architectural modeling, and global advertising campaigns. Software-as-a-Service (SaaS) models provide subscription access to cutting-edge tools for graphic design, 3D modeling, and video editing, lowering the initial capital expenditure for smaller studios and freelancers while ensuring they always operate with the latest iterations of production technology. This pervasive reliance on the cloud also necessitates robust cybersecurity measures to protect sensitive creative assets and intellectual property during transit and storage.

Artificial Intelligence and Machine Learning (AI/ML) are arguably the most disruptive technologies, influencing everything from concept art generation to personalized content curation. Generative AI tools accelerate the prototyping phase and provide alternatives for routine creative tasks, optimizing efficiency. Furthermore, predictive AI analytics are being utilized extensively in the gaming and media sectors to forecast content performance, inform investment decisions, and optimize platform layout based on deep consumer data analysis. The integration of AI requires significant backend infrastructure investment and specialized data science expertise within creative firms, moving them closer to being technology-driven entities rather than solely artistic ones.

The development of Immersive Technologies, namely Virtual Reality (VR), Augmented Reality (AR), and Mixed Reality (MR), is creating entirely new markets for experiential content. These technologies are crucial in architectural visualization, retail design (virtual showrooms), training simulations, and, most notably, in the burgeoning gaming and metaverse economies. Blockchains and Non-Fungible Tokens (NFTs) are also entering the landscape, offering mechanisms for digital asset verification, secure IP management, and new monetization models for digital artists, particularly in segments related to high-value digital collectibles and virtual real estate. These technologies together demand professionals who can blend traditional creative skills with deep technical proficiency in coding, physics engines, and decentralized systems architecture.

North America: North America, particularly the United States, remains the undisputed global hub for the Creative Industries, distinguished by its dominant position in film production (Hollywood), high-budget gaming development, and world-leading digital advertising and tech platforms (Silicon Valley). This region benefits from mature venture capital ecosystems, strong intellectual property rights protection, and a highly digitized consumer base with high disposable income. The strategic focus here is on cutting-edge technological integration, including AI-driven content pipelines and the commercialization of 5G networks to support high-fidelity streaming and interactive experiences. Growth is largely driven by large media conglomerates expanding their proprietary streaming offerings and significant R&D investment in immersive realities. The market structure is highly competitive, characterized by intense M&A activity aimed at consolidating content libraries and technological expertise.

Asia Pacific (APAC): APAC is projected to experience the fastest growth, fueled by demographic advantages, rapidly increasing internet penetration in China, India, and Southeast Asia, and a strong cultural affinity for mobile entertainment. South Korea and Japan are global leaders in gaming, animation, and unique cultural exports (K-pop, Anime), providing significant regional market drivers. The challenge in APAC lies in the regulatory fragmentation across diverse national markets and the need to cater to multilingual and multicultural audiences. However, high rates of digital adoption and the dominance of mobile gaming platforms ensure robust revenue generation. Investment is heavily concentrated on localized content production and adapting global creative formats to regional consumer preferences, making localized content strategy essential for market penetration.

Europe: Europe is characterized by a fragmented but rich creative landscape, supported by strong public funding for cultural arts and robust government initiatives designed to foster local creative economies (e.g., Creative Europe Programme). Key markets like the UK, France, and Germany excel in high-end design, fashion, publishing, and specialized VFX work. A primary regional trend is the necessity to comply with strict data protection regulations (GDPR), which significantly impacts advertising technology and data-driven creative strategies. The European market focuses heavily on ethical AI development in creative processes and cross-border collaborations, aiming to leverage the continent's diverse linguistic and cultural heritage while resisting the dominance of US-centric content platforms.

The primary growth driver is the exponential increase in global digital consumption, particularly the widespread adoption of mobile internet and high-speed streaming technologies. This expansion democratizes distribution and creates massive global audiences for video, music, and interactive media, fueling demand for continuous content creation and novel monetization strategies.

AI is fundamentally shifting creative roles from manual execution to strategic oversight, focusing on prompt engineering, curation, and quality control. While AI automates routine tasks like preliminary design drafts and data analysis, it enhances productivity and speed, making specialized human judgment in areas like cultural relevance and emotional resonance more valuable than ever.

The Gaming and Interactive Media segment, specifically covering mobile gaming, esports, and metaverse content creation, holds the highest growth potential. This is driven by high user engagement, lucrative micro-transaction revenue models, and the segment's capacity for rapid integration of new immersive technologies like VR/AR.

The main challenges involve combating rampant digital piracy, managing complex licensing requirements across global digital platforms, and establishing clear legal frameworks for ownership and fair usage of IP when generated or co-created using large-scale generative AI models trained on existing content databases.

APAC is critical due to its vast, rapidly digitizing population, high consumer affinity for mobile-first entertainment, and emerging creative powerhouses like China and South Korea. The region offers immense scale and high CAGR, driving global trends in mobile gaming, digital video consumption, and culturally specific content formats, requiring significant investment in localized production.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.