ID : MRU_ 436903 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

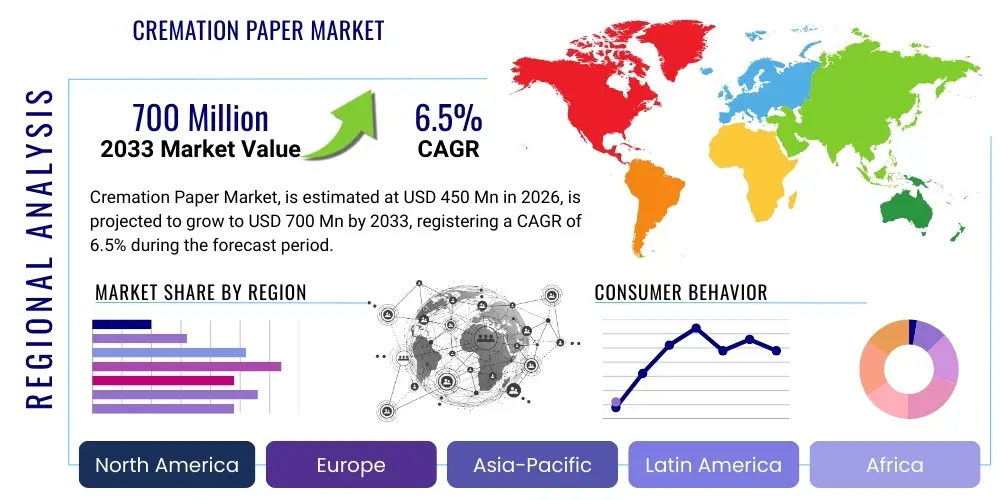

The Cremation Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 700 Million by the end of the forecast period in 2033. This growth trajectory is significantly influenced by increasing global cremation rates, evolving regulatory standards mandating the use of biodegradable materials in cremation processes, and heightened consumer demand for eco-friendly and personalized funeral solutions. The market size reflects the global adoption of cremation over traditional burial practices, particularly in densely populated regions across Asia Pacific and Europe.

The Cremation Paper Market encompasses the production and distribution of specialized, often biodegradable paper products designed for use in the cremation process. These papers serve multiple critical functions, including lining cremation containers, providing identification tags that remain intact during the high heat process, and facilitating the transfer of personal messages, notes, or tributes intended to be cremated alongside the deceased. The market growth is fundamentally linked to the global shift towards cremation, driven by factors such as cost-effectiveness, environmental considerations, and space constraints associated with traditional burial methods. This specialized paper is formulated to combust cleanly, leaving minimal ash residue and ensuring compliance with stringent environmental regulations.

Products within this sector are characterized by their material composition, often utilizing rice paper, bamboo fiber, or highly refined plant-based cellulose to ensure complete and clean incineration. The material selection is paramount, as the paper must withstand handling yet break down completely during the cremation cycle without contaminating the remains or the cremation chamber. Major applications span across professional settings like licensed crematories and funeral homes, where the paper ensures dignity and regulatory adherence, particularly concerning the use of temporary identification measures and the lining of alternative containers.

Key driving factors propelling market expansion include rising public awareness regarding the ecological impact of funeral practices, leading to increased adoption of sustainable cremation paper options. Furthermore, product innovation focusing on enhanced fire resistance for identification purposes while maintaining complete biodegradability post-cremation is attracting investments. The benefit of using specialized cremation paper lies in operational efficiency for funeral service providers, enabling seamless management of remains, reducing cleanup time, and offering personalized memorial options for grieving families, thereby enhancing the overall service quality offered by the funeral industry globally.

The Cremation Paper Market is experiencing robust expansion, primarily fueled by shifting global demographics and cultural acceptance of cremation. Current business trends indicate a strong focus on sustainability, compelling manufacturers to invest heavily in producing 100% biodegradable and zero-emission cremation paper, meeting the rigorous standards set by environmental agencies in North America and Western Europe. Furthermore, the personalization of funeral services is a significant trend, driving the demand for custom-printed cremation papers that allow families to include handwritten notes, drawings, or digital tributes that are then cremated with the loved one, adding a profound emotional value to the service.

Regionally, Asia Pacific dominates the market, largely due to high population density, historically high cremation rates in countries like India, China, and Japan, and favorable regulatory frameworks supporting efficient funeral practices. However, North America and Europe demonstrate the highest per-capita spending and demand for premium, high-density, and specialty-printed cremation papers. These regions are also setting the pace for regulatory changes concerning material transparency and end-of-life cycle management for funeral products, forcing suppliers to innovate rapidly and secure robust traceability within their supply chains. Latin America and MEA are emerging markets, showing accelerated adoption rates as cremation becomes more culturally accepted and infrastructure improves.

Segmentation trends highlight the increasing preference for plant-based cellulose and rice paper materials over synthetic alternatives, reinforcing the eco-conscious market shift. By application, the temporary casket lining segment accounts for the largest market share, ensuring respectful handling and transfer of remains. However, the identification tags and regulatory documentation segment is projected to exhibit the fastest growth, driven by tightening legal requirements for precise tracking throughout the cremation process to prevent commingling or misidentification of remains. Manufacturers are increasingly focusing on developing papers that are designed not only for clean burning but also for advanced digital printing technologies used by funeral homes.

User inquiries regarding the impact of Artificial Intelligence on the Cremation Paper Market generally revolve around logistical efficiency, supply chain optimization, predictive inventory management for funeral homes, and the role of AI in personalizing funeral documentation. Users often question if AI can predict regional demand fluctuations for specific paper types (e.g., eco-friendly versus standard) based on demographic shifts and public health data, thereby minimizing waste and optimizing production cycles. Additionally, there is interest in how AI-powered design tools could enhance the personalization aspect, enabling funeral directors to quickly generate complex, personalized digital content (tributes, photo collages) that can be seamlessly printed onto high-quality cremation paper for the service, ensuring consistency, high resolution, and regulatory compliance regarding size and material usage.

The primary influence of AI lies in refining the operational aspects of both manufacturers and end-users. For manufacturers, AI models can analyze raw material costs, transportation logistics, and real-time inventory levels across various global distribution centers, leading to significant cost savings and reduced lead times for niche products. For crematories and funeral homes, AI is integrated into enterprise resource planning (ERP) systems to forecast demand for identification tags and cremation liners based on historical volumes and seasonal fluctuations, ensuring just-in-time inventory and preventing costly shortages or excess stock, which is critical in maintaining the dignified flow of services. Furthermore, advanced computer vision systems powered by AI could potentially be utilized in quality control during the paper manufacturing process, identifying minute imperfections in the paper material that might compromise its clean-burning properties.

The market dynamics of the Cremation Paper sector are defined by a complex interaction between regulatory pressure, consumer preference for sustainability, and operational requirements of funeral services. The principal driver is the globally increasing rate of cremation, underpinned by economic factors and environmental consciousness, necessitating a reliable supply of compliant, high-quality paper materials. Restraints include the volatility in raw material prices, particularly specialized plant fibers, and the conservative nature of the funeral industry in some regions, which can slow the adoption of newer, more expensive sustainable paper technologies. Opportunities exist in emerging markets, technological advancements in material science creating superior biodegradable options, and the expansion of customization services for families, offering higher profit margins.

Drivers include stringent environmental regulations in developed economies that favor non-toxic, ash-free cremation materials, compelling funeral homes to shift away from traditional, less sustainable alternatives. Furthermore, cultural normalization and increasing acceptance of cremation across diverse populations globally substantially boost the baseline demand for essential cremation supplies, including specialized papers for identification and containment. The demand for product traceability and compliance documentation also necessitates high-quality, specialized paper that can withstand the pre-cremation environment and adhere to strict regulatory standards regarding material composition. This regulatory oversight acts as a major catalyst for market standardization and quality improvement.

However, the market faces significant restraints. The highly localized and fragmented nature of the funeral service industry often results in varied purchasing power and preferences, making large-scale standardization challenging. Another restraint is the potential for substitution by non-paper, biodegradable alternatives, such as certain plant-based fabrics or dissolvable materials, though paper maintains advantages in printability and cost. Impact forces include strong bargaining power from large funeral service chains consolidating purchases, and the intense competitive rivalry among paper manufacturers focusing on achieving the delicate balance between maximum biodegradability, sufficient tensile strength for handling, and clean-burning characteristics required by regulatory bodies, thus maintaining a competitive pricing structure.

The Cremation Paper Market is intricately segmented based on material type, density, application, and end-user, reflecting the diverse operational needs within the global funeral industry. Material segmentation is perhaps the most critical, driven by environmental mandates, distinguishing between conventional materials and the increasingly dominant eco-friendly options. Application segmentation highlights the primary uses, ranging from essential regulatory compliance (identification) to value-added services (personal tributes). The geographic segmentation reveals major consumption hubs, where regulatory frameworks and cultural norms dictate the preferred product specifications and overall market volume.

The value chain for the Cremation Paper Market begins with the upstream sourcing of raw materials, primarily specialized cellulose fibers, rice straw, or bamboo pulp. Key upstream activities involve sustainable forestry management and specialized processing techniques to ensure the pulp produced is free of chemicals or treatments that could release toxic emissions during cremation. Manufacturers must secure reliable, certified suppliers capable of meeting stringent quality control standards regarding fiber purity and structure. Efficiency at this stage directly impacts the final product’s environmental compliance and cost-effectiveness. Technological investments focus on optimizing pulp treatment to enhance both tensile strength for handling and complete combustibility.

The core manufacturing process involves paper production, specific treatment for heat tolerance and printability, cutting, and packaging. Distribution channels form the crucial midstream and downstream linkages. Direct channels involve large paper manufacturers supplying directly to major regional funeral service conglomerates or government-run crematory bodies under long-term contracts. Indirect channels utilize specialized medical and funeral supply distributors who manage inventory, logistics, and sales to numerous independent funeral homes and small-to-medium crematories. Distributors play a critical role in providing localized inventory management and ensuring compliance with varied regional regulations concerning cremation materials.

Downstream activities center on the end-user application within the funeral service workflow, encompassing inventory management at the crematory, application (e.g., lining containers, attaching identification), and the final cremation process. The interaction between manufacturers and distributors is often highly regulated due to the sensitive nature of the product, requiring robust traceability systems. The rising demand for customized paper products is increasing the importance of digital printing service providers integrating into the value chain, acting as converters or specialized service bureaus that personalize the paper before it reaches the funeral home, thereby adding significant value and differentiating offerings in a highly competitive market environment.

The primary customers and end-users of cremation paper products are professional entities operating within the death care industry, mandated by regulatory bodies to utilize appropriate materials during the cremation process. Licensed Crematories form the core demand segment, relying on cremation paper for all internal processes, from temporary holding linings to essential identification tags that must accompany the remains throughout the entire cycle. These facilities prioritize quality, compliance with emission standards, and bulk pricing, given their high volume usage. The operational efficiency and regulatory adherence offered by specialized cremation paper are non-negotiable requirements for this customer segment, making product reliability paramount.

Funeral Homes and Mortuaries represent another major customer base. While some have integrated crematory facilities, many utilize cremation paper for services rendered prior to the remains being transported to a dedicated crematory. This includes using paper linings for alternative containers and facilitating the personalization element, such as collecting and handling family tributes written on special paper designed for cremation. Funeral homes often prioritize ease of use, aesthetic quality (especially for personalized tributes), and logistical convenience, frequently relying on specialized distributors for just-in-time supplies. Their purchasing decisions are often influenced by the ability of the paper supplier to integrate customization services.

A smaller, but growing segment includes Religious Organizations and direct consumers utilizing specialized memorial services. Religious requirements sometimes dictate specific materials or practices for handling remains, driving demand for culturally sensitive and specifically certified cremation paper. Furthermore, the increasing trend of direct-to-consumer sales, often through online memorial product platforms, allows individuals to purchase personalized cremation paper (for letters, drawings, etc.) for inclusion during the service, emphasizing the growing importance of the personalization application segment and broadening the traditional customer base beyond solely institutional buyers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 700 Million |

| Growth Rate | CAGR 6.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Ecologic Paper Solutions, Memorial Products Group, Green Legacy Corp, Biodegradable Paper Mills, FiberTech Innovations, CleanBurn Supplies, Global Cremation Resource, Custom Tribute Papers, Sustainable Fiber Solutions, Cremation Supplies International, Environmental Deathcare Products, Bio-Process Paper Systems, Harmony Funeral Products, Eternal Rest Papers, TerraFibres, Phoenix Cremation Products, Zenith Paper & Pulp, Eco-Sense Materials, The Identification Tag Co., Serenity Supplies. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Cremation Paper Market is primarily centered on material science innovation and specialized manufacturing techniques designed to ensure optimum combustion characteristics. A core technology involves the development of Hydrocarbon-Free and Chlorine-Free (HFCF) pulping processes, which ensure that the final paper product releases minimal volatile organic compounds (VOCs) or toxic residues when subjected to the high temperatures within a cremation chamber. This technological imperative is driven by stringent environmental protection agency (EPA) standards globally, pushing manufacturers towards purer cellulose and non-synthetic binding agents, necessitating advanced filtering and refining technologies in the upstream production process. The implementation of nano-cellulose technology is emerging as a critical differentiator, offering enhanced strength at reduced thickness, thereby minimizing overall material mass requiring combustion.

Another crucial technological area is advanced digital printing compatibility. Funeral homes require the ability to print complex graphics, barcodes, and detailed regulatory information onto cremation paper, often using high-speed digital inkjet or laser printers. Manufacturers must engineer the paper surface to accept various ink types without smudging or compromising the clean-burning properties. This involves specialized surface treatments and coatings that are themselves biodegradable and combust cleanly. Furthermore, technology related to traceability, such as integrating subtle, heat-resistant digital markers or RFID tags (often removed before cremation, but used for inventory tracking), is becoming standard for high-security identification papers, ensuring precise handling throughout the funeral chain of custody.

The technology deployed by end-users, such as licensed crematories, also indirectly influences paper demand. Modern crematory retort technology often features highly optimized airflow and temperature control systems. Manufacturers are developing papers specifically engineered to complement these efficient retorts, ensuring papers burn at specific rates that do not interfere with the retort’s operational parameters. This synergy between paper material science and cremation machine engineering represents a vital technological advancement, ensuring not only environmental compliance but also maximizing energy efficiency and minimizing operational downtime for the crematory operator, thereby solidifying the necessity for specialized, technologically advanced cremation paper products.

The Cremation Paper Market exhibits significant regional variations in terms of adoption rates, product specifications, and regulatory environments, influencing consumption patterns and market potential across the globe.

Cremation paper is primarily manufactured from specialized, unbleached, and untreated natural fibers such as rice paper, bamboo pulp, or pure plant-based cellulose. These materials are selected because they combust completely at high temperatures, leaving minimal ash and ensuring they do not release toxic chemicals or heavy metals into the environment, complying with strict air quality standards.

Standard paper often contains inks, glues, bleaches, and mineral fillers that can produce harmful toxins (like dioxins or volatile organic compounds) when burned at cremation temperatures, contaminating the remains and the environment. Specialized cremation paper is chemically pure and engineered for clean, complete combustion, critical for both regulatory compliance and maintaining the purity of the cremated remains.

The central driver is the consistent and increasing global acceptance and adoption rate of cremation over traditional burial methods, fueled by rising urban density, high costs of burial plots, and growing environmental awareness. This increased volume directly correlates with higher demand for regulatory-compliant and eco-friendly cremation accessories, including specialized paper liners and identification tags.

Cremation paper facilitates personalization by allowing families to include handwritten notes, drawings, or printed tributes that are cremated alongside the deceased. Manufacturers offer specific high-grade, printable paper designed solely for this purpose, adding profound emotional value to the service while ensuring the included materials comply with crematory operational requirements and clean-burning standards.

The Asia Pacific (APAC) region currently dominates the consumption volume of cremation paper. This is due to the consistently high historical and current cremation rates in densely populated countries such as Japan, China, and India, where cremation is a culturally established and necessary practice due to land scarcity.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.