ID : MRU_ 432192 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

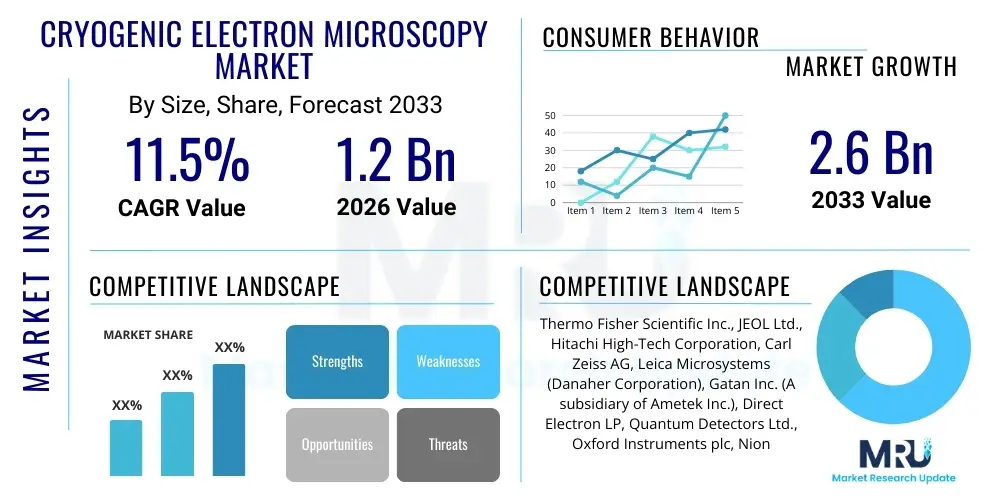

The Cryogenic Electron Microscopy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 1.2 Billion in 2026 and is projected to reach USD 2.6 Billion by the end of the forecast period in 2033.

Cryogenic Electron Microscopy (Cryo-EM) represents a paradigm shift in structural biology, offering unprecedented capabilities for determining the three-dimensional structures of biological macromolecules, complexes, and cellular components at near-atomic resolution. This sophisticated technology involves freezing biological samples rapidly (vitrification) in a thin layer of amorphous ice, stabilizing them without the need for crystallizing or chemical fixation, which preserves their native state. The vitrified sample is then examined using a powerful transmission electron microscope (TEM) equipped with specialized detectors, allowing researchers to capture thousands of projection images necessary for computational reconstruction.

The core product offerings in this market encompass high-end transmission electron microscopes specifically configured for cryogenic temperatures, advanced direct electron detectors (DEDs), automated sample preparation instruments (like plungers and cryo-FIB systems), and specialized computational software packages for image processing and 3D reconstruction. Major applications span critical areas such as structural biology research, where Cryo-EM is essential for understanding protein function; drug discovery and development, by providing high-resolution targets for therapeutic intervention; and virology and vaccine development, through the visualization of viral structures. Key benefits include the ability to study dynamic processes, handle challenging samples that resist crystallization, and significantly accelerate the pace of structural determination compared to traditional X-ray crystallography or Nuclear Magnetic Resonance (NMR).

Market growth is predominantly driven by massive funding increases from government and private organizations globally into life sciences research and personalized medicine initiatives. The ongoing technical advancements in electron microscope performance, particularly higher-brightness electron sources and improved aberration correction, coupled with the introduction of highly sensitive direct electron detectors, have dramatically improved image quality and throughput. Furthermore, the rising adoption of single particle analysis (SPA) and cryo-electron tomography (CET) techniques across pharmaceutical and biotechnology companies fuels the commercial demand, as these firms seek faster, more accurate methods for target validation and understanding mechanism of action (MOA).

The Cryogenic Electron Microscopy market is undergoing rapid expansion characterized by intense innovation in detector technology and sophisticated computational methods that streamline data processing and structure validation. Business trends indicate a strong shift toward consolidation and strategic partnerships between equipment manufacturers and specialized software providers to offer integrated, high-throughput solutions that cater to both institutional core facilities and commercial drug discovery pipelines. Capital investment in high-end Cryo-EM systems remains substantial, but accessibility is improving through shared resource models and the emergence of contract research organizations (CROs) specializing in Cryo-EM services. Geographically, North America currently holds the largest market share due to established academic leadership and heavy investment by pharmaceutical giants, while the Asia Pacific region is rapidly emerging as the fastest-growing market, driven by governmental investment in advanced scientific infrastructure, particularly in China and South Korea, aiming to become global leaders in structural biology.

Segment trends reveal that the Single Particle Analysis (SPA) technique continues to dominate the market due to its proven success in determining high-resolution structures of isolated macromolecules, making it indispensable for foundational biology and drug target identification. However, the Cryo-Electron Tomography (CET) segment is poised for significant growth as researchers increasingly focus on understanding cellular context and visualization of complex, heterogeneous samples in situ. Component-wise, the demand for direct electron detectors (DEDs) is experiencing explosive growth, as these detectors are fundamental to achieving the necessary resolution for modern Cryo-EM applications, offering superior signal-to-noise ratio and fast readout speeds compared to older CCD technologies. End-user adoption is increasingly tilting towards pharmaceutical and biotechnology companies, moving beyond traditional academic settings, indicating the maturation of Cryo-EM as a routine tool in industrial R&D processes, thus shifting the revenue streams from public grants to commercial budgets.

The overarching strategic objective for market participants focuses on miniaturization, automation, and accessibility. Manufacturers are developing fully automated sample preparation workflows, including robotic loading and grid vitrification systems, to reduce human error and boost throughput, which is crucial for pharmaceutical screening efforts. Furthermore, addressing the critical need for skilled operators is becoming a core challenge, prompting companies to invest in comprehensive training programs and user-friendly software interfaces. The shift towards higher-energy microscopes (e.g., 300kV systems) is prevalent for achieving the highest possible resolution, yet there is also a niche but growing market for more accessible 200kV systems suitable for initial screening and smaller laboratories. These technological and business dynamics confirm Cryo-EM's transition from a specialized technique to a fundamental, high-impact tool across the life sciences industry.

User inquiries regarding the influence of Artificial Intelligence (AI) and Machine Learning (ML) on the Cryogenic Electron Microscopy market center around themes of data processing efficiency, automation of complex workflows, and enhanced resolution capabilities. Common questions explore how AI algorithms can accelerate the notoriously time-consuming stages of image alignment, particle picking, and 3D reconstruction, and whether AI can help overcome inherent limitations like sample heterogeneity and low signal-to-noise ratios. Users are highly interested in the potential for AI to automate the decision-making processes required during data collection, thereby optimizing microscope usage and reducing the need for continuous expert oversight. There is also significant concern regarding the validation and interpretability of structures generated partially or wholly through sophisticated ML models, and the integration of AI tools within existing proprietary software platforms.

The Cryogenic Electron Microscopy market is fundamentally shaped by powerful drivers, strict regulatory and technical restraints, and significant emerging opportunities, all mediated by several impactful forces. The primary driver is the accelerating demand for high-resolution structural information in drug discovery, particularly in pharmaceutical companies shifting away from traditional methods to understand complex membrane proteins and dynamic assemblies. However, market adoption is restrained by the exceptionally high initial capital investment required for purchasing and installing 300kV Cryo-EM systems and the specialized peripheral equipment, coupled with the critical shortage of highly skilled technicians and bio-informaticians capable of operating these advanced systems and analyzing the resulting massive datasets. The major opportunity lies in expanding the applications of Cryo-EM beyond structural biology into fields like materials science (studying nanoparticles and polymers) and clinical diagnostics, along with developing more accessible, lower-cost benchtop Cryo-EM systems designed for screening and quality control, thereby broadening the potential user base beyond premier research institutions. These internal factors are heavily influenced by external impact forces such as stringent government funding policies for scientific infrastructure, increasing global academic competition, and the rapid pace of technological obsolescence necessitating continuous equipment upgrades.

A detailed examination of market drivers emphasizes the pivotal role of technological improvements. Innovations in direct electron detection technology, such as the introduction of next-generation detectors with even faster frame rates and lower noise characteristics, have been instrumental in pushing the achievable resolution limit towards the theoretical maximum. Furthermore, increased government and philanthropic investment in large-scale structural genomics and proteomic initiatives across North America and Europe guarantees a steady demand stream for new Cryo-EM instruments and services. The clinical relevance of Cryo-EM is also a growing driver; by visualizing virus structures and key disease targets like amyloid plaques and specific cancer biomarkers, Cryo-EM provides essential foundational data for developing highly targeted therapies and vaccines. The pharmaceutical sector's adoption of Cryo-EM to resolve challenging drug targets, such as G protein-coupled receptors (GPCRs), has firmly established the technology as a standard tool in preclinical development, cementing its commercial viability.

Conversely, market restraints are multifaceted, extending beyond cost. The complex workflow, from sample preparation to final structure validation, remains a technical bottleneck; achieving high-quality vitrified grids is often described as an art, highly dependent on user expertise and ambient conditions. Moreover, the massive computational demands for processing terabytes of raw image data require substantial investment in high-performance computing clusters, which adds significantly to the total cost of ownership (TCO) and operational complexity. Opportunities, however, present pathways for mitigating these restraints; the integration of AI/ML tools is progressively automating and simplifying complex image processing steps, reducing the reliance on human experts and speeding up turnaround times. Furthermore, the development of integrated, fully automated Cryo-EM platforms, featuring robotic sample handling and real-time feedback loops, is expected to democratize the technology, making it accessible to a wider array of research institutions and commercial laboratories globally, particularly as manufacturers strive to reduce the system footprint and operational overhead.

The Cryogenic Electron Microscopy market is comprehensively segmented based on technology, component, application, and end-user, reflecting the diverse requirements of the global research and commercial communities. Analyzing these segments provides a clear understanding of market dynamics, growth trajectories, and areas of high investment. The segmentation highlights the continued dominance of established techniques like Single Particle Analysis (SPA) due to its high-resolution output for isolated proteins, contrasting with the high-growth potential of Cryo-Electron Tomography (CET) driven by the demand for in situ visualization of cellular components. Crucially, the component segmentation underscores the ongoing technological competition and innovation within the detector and software markets, which are key determinants of system performance and operational efficiency. The end-user segmentation clearly indicates the increasing commercialization of Cryo-EM services, moving from purely academic research towards robust industrial application in drug discovery and biotechnology.

The Cryogenic Electron Microscopy value chain is highly specialized, beginning with complex upstream manufacturing and culminating in the provision of high-value structural data to downstream users. Upstream activities involve the highly technical design, precision engineering, and fabrication of core components, specifically the electron optics column, high-vacuum systems, and cryogenic stages. This stage requires specialized expertise in physics, materials science, and high-precision manufacturing, dominated by a few key global players who control the supply of high-end TEMs. The midstream involves the integration of proprietary components, such as state-of-the-art direct electron detectors (DEDs) sourced from specialized suppliers, along with sophisticated computing hardware and the bundled image processing software essential for operating the full system. This integration stage defines the performance characteristics and final cost structure of the Cryo-EM system.

Downstream activities center around the distribution, installation, service, and application support provided to end-users. Distribution typically occurs through direct sales channels due to the high cost and complexity of the equipment, necessitating extensive on-site technical support and training. For academic and corporate research institutions, the primary value generated downstream is the structural data itself, which is often leveraged for publications, intellectual property generation, or drug development milestones. Furthermore, the specialized nature of the technique has fostered a robust ecosystem of specialized Cryo-EM service bureaus and Contract Research Organizations (CROs), which offer access to high-end instrumentation and expert analysis on a fee-for-service basis. These indirect channels help lower the barrier to entry for smaller labs or companies that cannot afford the capital investment.

Direct distribution involves manufacturers selling and installing the complete microscope system directly to major academic core facilities or large pharmaceutical R&D centers, providing comprehensive maintenance contracts and long-term application consulting. Indirect distribution is primarily facilitated by the increasing network of CROs and centralized shared resource facilities (SRFs) that acquire and maintain the expensive instruments. These entities serve a wide client base, providing access to Cryo-EM services, including sample preparation, data collection, and image processing, thereby democratizing access to the technology and expanding the market footprint by serving clients globally who require structural insights but lack the internal infrastructure. This dual distribution strategy ensures that both high-volume core users and smaller, project-based clients are effectively served.

The primary end-users and buyers of Cryogenic Electron Microscopy technology are institutions heavily invested in fundamental biomedical research, applied pharmaceutical development, and high-end materials science. Academic and governmental research institutions represent the historical and still foundational customer segment, utilizing Cryo-EM core facilities to drive basic structural biology discoveries, secure research grants, and publish high-impact scientific findings. These customers typically prioritize resolution, reliability, and robust software ecosystems, demanding the most powerful 300kV systems capable of achieving sub-2 Ångström resolution, often purchased via large capital expenditure grants or centralized university funds.

Pharmaceutical and biotechnology companies constitute the fastest-growing and commercially most lucrative customer segment. These buyers leverage Cryo-EM primarily for target validation, hit-to-lead optimization, and understanding the precise mechanism of action (MOA) of drug candidates, especially those targeting difficult membrane proteins, large protein complexes, or viral capsids. Their purchasing decisions are heavily influenced by high throughput, automation capabilities, and compatibility with industrial-scale screening workflows. This segment increasingly utilizes external specialized CROs as a tactical purchasing decision, allowing them to rapidly scale their structural biology efforts without undertaking massive, long-term capital commitments, thereby accelerating time-to-market for novel therapeutic agents.

A smaller but rapidly emerging customer base includes specialized Contract Research Organizations (CROs) and clinical laboratories. CROs act as intermediaries, providing expert Cryo-EM services to pharmaceutical clients, thus requiring multiple high-end systems and robust automation protocols to manage high-volume commercial projects efficiently. Clinical laboratories are beginning to explore Cryo-EM for high-resolution diagnostic applications, such as analyzing pathological aggregates or identifying subtle structural variations in pathogens, marking a nascent but potentially transformative expansion of the technology’s application beyond traditional research boundaries. These customers require streamlined workflows and rigorous validation protocols.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.6 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Thermo Fisher Scientific Inc., JEOL Ltd., Hitachi High-Tech Corporation, Carl Zeiss AG, Leica Microsystems (Danaher Corporation), Gatan Inc. (A subsidiary of Ametek Inc.), Direct Electron LP, Quantum Detectors Ltd., Oxford Instruments plc, Nion Co., Delong Instruments, National Instruments Corporation, FEI (now part of Thermo Fisher Scientific), Scion Instruments, Hamamatsu Photonics K.K., Agilent Technologies Inc., TTP Labtech, SPT Labtech, Bio-Rad Laboratories Inc., NanoImaging Services Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Cryogenic Electron Microscopy technology landscape is rapidly evolving, driven primarily by innovations aimed at improving resolution, increasing throughput, and enhancing ease of use. At the core of the technology are the ultra-high voltage Transmission Electron Microscopes (TEMs), often operating at 200kV or 300kV. The latest advancements in these microscopes involve integrating highly stable electron sources, such as field emission guns (FEGs), and aberration correctors that minimize spherical and chromatic aberrations, crucial for achieving sub-atomic resolution. Furthermore, improvements in cryogenic stage stability are vital; these stages must maintain samples at liquid nitrogen temperatures (around -170°C) with minimal drift during lengthy data acquisition sessions, demanding extremely precise mechanical engineering and temperature control systems.

The single most impactful technological advancement has been the advent of Direct Electron Detectors (DEDs). Unlike traditional charge-coupled device (CCD) cameras, DEDs directly detect electrons, offering significantly higher sensitivity, faster readout speeds, and superior detective quantum efficiency (DQE). This high performance allows researchers to image samples using much lower electron doses, mitigating radiation damage—a major limitation in Cryo-EM—and facilitating motion correction algorithms that account for slight sample movement during exposure. Leading DED manufacturers continually compete to reduce noise and increase frame rates, directly enabling the high-throughput capabilities now essential for commercial applications and large-scale academic projects. The integration of DED technology is fundamental to nearly all high-resolution Cryo-EM breakthroughs reported in recent years.

Beyond hardware, the technological landscape is defined by sophisticated computational and automation technologies. Software packages for image processing, such as RELION and cryoSPARC, utilize complex statistical and machine learning methodologies to handle particle picking, 2D classification, and 3D reconstruction from vast datasets. Ongoing innovation focuses on streamlining these computational pipelines and incorporating artificial intelligence for automated quality assessment and parameter optimization, which is key to making Cryo-EM accessible to non-expert users. Furthermore, specialized ancillary equipment, particularly automated vitrification robots and focused ion beam (FIB) milling systems integrated with cryo capabilities (Cryo-FIB), are critical. Cryo-FIB is essential for preparing uniformly thin lamellae from thicker biological specimens, enabling in situ Cryo-Electron Tomography (CET) studies of cellular components, representing a major leap forward in visualizing molecules within their native cellular context.

The extremely high cost is primarily driven by the complex, ultra-high precision engineering required for the Transmission Electron Microscope (TEM) column, the high-vacuum systems, the sophisticated cryogenic stages, and the high-performance Direct Electron Detectors (DEDs) which require highly specialized manufacturing processes and materials.

SPA is utilized to determine the high-resolution structure of isolated, purified macromolecules and proteins by analyzing thousands of individual 2D images, whereas CET is used to visualize complex, larger structures and organelles in situ (within their native cellular context) by capturing a series of tilted 2D projections to reconstruct a 3D volume.

The Pharmaceutical and Biotechnology Companies segment is currently the fastest-growing end-user, rapidly adopting Cryo-EM as a routine tool for structural validation, target identification, and lead optimization during the preclinical phases of drug discovery and development.

AI, particularly Deep Learning, accelerates critical, labor-intensive stages such as automated particle picking, classification of conformational states, and optimized image alignment, significantly reducing processing time and maximizing the effective utilization of expensive microscope time.

The market is highly consolidated, dominated by a few major integrated microscope manufacturers (e.g., Thermo Fisher Scientific, JEOL, Hitachi) who compete on system resolution and integration, while a separate segment of specialized companies focuses on high-performance ancillary components like Direct Electron Detectors and advanced software solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.