ID : MRU_ 434445 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

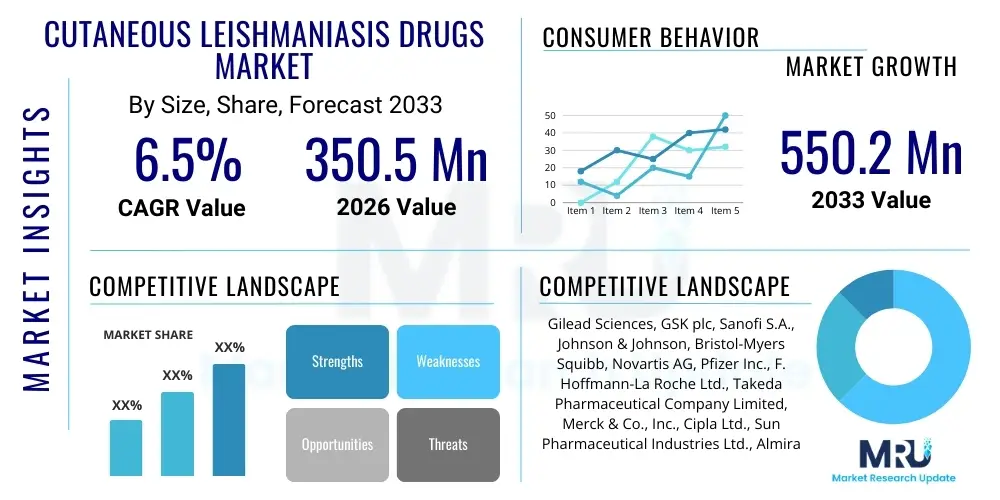

The Cutaneous Leishmaniasis Drugs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 350.5 million in 2026 and is projected to reach USD 550.2 million by the end of the forecast period in 2033.

The Cutaneous Leishmaniasis (CL) Drugs Market encompasses pharmaceuticals specifically utilized for the treatment and management of localized skin lesions caused by protozoan parasites of the genus Leishmania. CL is the most common form of leishmaniasis, a complex neglected tropical disease (NTD) endemic in over 90 countries. Products range from systemic agents, such as pentavalent antimonials (e.g., sodium stibogluconate) and liposomal amphotericin B, which are often associated with toxicity and complex administration, to topical and oral therapies like miltefosine and paromomycin, offering improved patient compliance and safety profiles. The necessity for effective, safer, and cost-efficient drugs is paramount, especially in resource-limited settings where the disease burden is highest, driving significant research and development efforts toward novel drug formulations and therapeutic approaches tailored for specific geographic strains and clinical manifestations.

Major applications of these drugs include treating primary skin ulcers, disseminated forms, and preventing progression to mucosal leishmaniasis, which is debilitating and hard to manage. Key benefits driving market growth include a heightened global awareness through initiatives by organizations such as the WHO, the increasing incidence rates in newly affected non-endemic areas due to climate change and human migration, and the continuous need to combat rising drug resistance observed in standard treatments like antimony derivatives. Furthermore, the push for effective, short-course oral therapies that reduce the reliance on injectable and often toxic compounds is reshaping the landscape, fostering innovation in drug delivery systems and formulation stability to ensure efficacy in challenging environments.

Driving factors for this market are multi-faceted, including sustained funding from philanthropic organizations and governmental bodies focused on NTDs, advancements in diagnostic techniques allowing for earlier and more accurate identification of infections, and critical unmet medical needs, particularly concerning pediatric formulations and treatments for pregnant women. The complexity of CL, stemming from the variability in Leishmania species and patient immune responses, necessitates personalized therapeutic strategies, thereby supporting the development of a diverse product pipeline. Investment in research focused on repurposing existing drugs and exploring host-directed therapies contributes substantially to the overall expansion trajectory of the cutaneous leishmaniasis drugs market through the forecast period.

The Cutaneous Leishmaniasis Drugs Market is poised for robust expansion, driven primarily by the high endemicity in developing nations and continuous efforts to minimize treatment durations and toxicity profiles associated with traditional drugs. Business trends indicate a shift toward public-private partnerships, accelerating the clinical trials and approval pathways for novel drugs, such as topical paromomycin formulations and new-generation oral inhibitors that offer superior efficacy against antimony-resistant strains. Investment in manufacturing capacity for thermostable drug products is also noted, facilitating better distribution logistics in tropical and subtropical regions. Furthermore, competitive strategies emphasize licensing agreements and acquisitions focused on securing intellectual property related to innovative drug targets, positioning specialized pharmaceutical firms for leadership in this niche therapeutic area.

Regional trends highlight Latin America and the Middle East & Africa (MEA) as major revenue contributors and critical growth engines due to the high burden of disease and prevalence of zoonotic reservoirs, necessitating large-scale public health intervention programs. Conversely, North America and Europe, while representing smaller volume markets, contribute significantly in terms of R&D investment and access to premium specialized treatments, including combination therapies and advanced supportive care. The emergence of imported cases in non-endemic regions further influences regulatory bodies in developed markets to streamline approval processes for CL treatments, thereby bolstering global market accessibility and driving rapid uptake of new therapeutic options post-launch.

Segment trends underscore the dominance of the drug class segment, particularly the antileishmanial agents, while observing rapid growth in the topical route of administration segment, preferred for localized, uncomplicated lesions due to enhanced safety and ease of use. Within distribution channels, government purchases and non-governmental organization (NGO) distribution networks remain vital, reflecting the critical role of public sector procurement in ensuring drug affordability and availability in high-incidence zones. The future trajectory suggests increased market share for oral therapies as manufacturers successfully address challenges related to absorption variability and gastrointestinal side effects, fulfilling the clinical demand for fully systemic, non-invasive treatments for complex or multiple lesions.

Common user inquiries concerning the influence of Artificial Intelligence (AI) in the Cutaneous Leishmaniasis Drugs Market center on its capacity to expedite the identification of novel drug targets, optimize existing treatment regimens, and enhance epidemiological surveillance. Users frequently question how machine learning can predict drug resistance patterns in specific geographical isolates of Leishmania and whether AI-driven image analysis can standardize the diagnosis and severity assessment of CL lesions, reducing reliance on invasive procedures. Key themes emerging from these questions involve the accelerated pipeline development, personalized medicine approaches based on genomic profiling of both the host and parasite, and improving the efficiency and success rates of preclinical screening, thereby lowering the substantial R&D costs associated with NTD drug development.

AI's role is transformative, offering powerful tools for high-throughput screening (HTS) of chemical libraries against Leishmania parasites, significantly shortening the lead optimization phase. Deep learning algorithms are being employed to analyze complex biological data, including genomic, proteomic, and metabolomic profiles of the parasites, to pinpoint essential metabolic pathways that can be selectively inhibited. This computational approach allows researchers to identify compounds with favorable pharmacological properties and reduced off-target toxicity earlier in the development cycle. Furthermore, AI models are crucial in simulating clinical trial outcomes, predicting patient responses to combination therapies, and refining dosing schedules, optimizing scarce resources in clinical research settings.

Beyond drug discovery, AI facilitates enhanced public health management and resource allocation within the CL domain. Predictive analytics leverage environmental, climatic, and socio-economic data to forecast outbreak areas and severity, enabling proactive drug stocking and deployment strategies by health organizations. Integrating AI into point-of-care diagnostic devices, especially those using microscopy or digital imaging, can rapidly provide accurate species identification and parasite load quantification, ensuring immediate initiation of the most appropriate treatment protocol. This shift towards data-driven decision-making represents a fundamental improvement in the speed and precision of CL management globally.

The dynamics of the Cutaneous Leishmaniasis Drugs Market are shaped by a complex interplay of systemic drivers, structural restraints, and emerging opportunities, collectively known as DRO & Impact Forces. The primary driver is the increasing global prevalence and geographical spread of CL, coupled with the critical challenge of drug resistance, which necessitates continuous innovation and product refresh. Restraints largely stem from the classification of CL as a neglected tropical disease, resulting in limited commercial profitability expectations, which discourages major pharmaceutical investment in R&D and manufacturing capacity for specific CL therapies. However, philanthropic funding and governmental incentives, alongside advanced technologies for rapid drug screening and formulation, present substantial opportunities for smaller biotech firms and academic institutions to introduce novel, low-cost treatments. These impact forces regulate market growth by balancing the urgent public health need against the economic feasibility of drug development.

A significant force driving market expansion is the growing support from global health initiatives, particularly those focused on eliminating or controlling NTDs. Organizations such as the World Health Organization (WHO), Drugs for Neglected Diseases initiative (DNDi), and the Bill & Melinda Gates Foundation provide crucial funding for preclinical research, clinical trials, and procurement of essential medicines, insulating development efforts from typical market pressures. Furthermore, advancements in drug delivery technologies, such as microencapsulation and liposomal formulations, enhance the efficacy and reduce the toxicity of established drugs like Amphotericin B, thus improving patient compliance and broadening the therapeutic window for systemic treatments, significantly contributing to market utilization and acceptance.

Conversely, major restraints include the high cost, complex administration, and significant side-effect profile of many first-line treatments, such as parenteral antimonials, which require long treatment durations under clinical supervision. The logistical challenges inherent in distributing thermostable, sensitive pharmaceuticals to remote, underserved endemic areas further hinder market penetration. Opportunities reside in developing topical and oral agents, like new formulations of Miltefosine or topical Paromomycin, which simplify treatment and minimize the need for specialized medical infrastructure. The pipeline focusing on entirely new drug targets, utilizing synthetic biology and fragment-based drug design, represents a long-term opportunity to overcome current resistance issues and deliver curative, single-dose regimens.

The Cutaneous Leishmaniasis Drugs Market is comprehensively segmented based on Drug Class, Route of Administration, and Distribution Channel, reflecting the diverse approaches required to manage this heterogeneous disease. Segmentation by Drug Class allows for analysis of the market dominance of traditional systemic agents versus newer, targeted therapies, including pentavalent antimonials, polyenes (Amphotericin B formulations), and alkylphospholipids (Miltefosine). Analyzing the Route of Administration—systemic (oral and parenteral) versus topical application—is critical, as it highlights the ongoing shift toward non-invasive, patient-friendly options for uncomplicated lesions. Furthermore, understanding the Distribution Channel, which is heavily reliant on public procurement and institutional sales, provides insight into the accessibility and pricing structure required for global health impact.

The Drug Class segment is dominated by older, essential medicines, but the fastest growth is anticipated in the newer classes that address drug resistance and patient tolerance issues. Specifically, liposomal formulations of Amphotericin B (such as AmBisome) are gaining traction due to a significantly improved therapeutic index compared to conventional formulations, despite higher initial costs. The Route of Administration segmentation clearly indicates that while systemic treatments remain necessary for severe or complicated infections, the demand for highly effective, locally acting topical drugs, often based on paromomycin or essential oils, is accelerating in primary healthcare settings due to minimal systemic side effects and ease of self-application.

The Distribution Channel segment is unique in that it is not primarily driven by retail pharmacy sales in high-incidence areas. Instead, government procurement programs, large-scale donations, and centralized distribution networks managed by international organizations (like MSF and WHO) account for the majority of volume sales. This institutional structure requires manufacturers to engage in differential pricing strategies and large volume contracts. The market’s segmentation thus provides a roadmap for stakeholders, indicating where innovation in formulation is needed (topical/oral) and how products must be priced and distributed to maximize public health benefit and market reach.

The value chain for the Cutaneous Leishmaniasis Drugs Market begins with intensive upstream research and development, which is characterized by high risk and low immediate commercial reward, necessitating substantial non-profit or public funding. This stage involves target identification, lead optimization, and preclinical testing, often focused on identifying compounds that are active against multiple Leishmania species strains and capable of effective intracellular delivery within macrophages. Manufacturing processes follow, requiring specialized capabilities, particularly for complex formulations such as liposomes (Amphotericin B) or sterile parenteral preparations (Antimonials). Due to low market pricing, efficient, high-volume production is crucial to maintain cost-effectiveness.

Downstream analysis focuses heavily on regulatory approval and extensive clinical trials, which often take place in endemic countries under challenging logistical conditions. The distribution channel is bifurcated: direct distribution involves specialized governmental or global health organizations (like PAHO or WHO regional offices) managing large-scale procurement and dispensing to clinics in rural areas. Indirect distribution involves local pharmaceutical wholesalers and hospital networks, predominantly in areas with better healthcare infrastructure, handling specialized prescriptions for complicated cases or imported infections in non-endemic regions. The complexity lies in ensuring cold chain requirements are met for sensitive biological or liposomal products throughout the supply chain.

Key profit generation points are often focused on the intellectual property associated with novel chemical entities or proprietary formulation technologies rather than high-volume sales margins. For generic or legacy drugs, margin is maintained through scale and cost efficiency in manufacturing. The final crucial element is patient adherence and monitoring, requiring robust educational programs supported by NGOs and public health bodies. This holistic approach, from academic research to last-mile delivery, defines the highly institutionalized and philanthropically supported value chain characteristic of the Cutaneous Leishmaniasis drugs segment.

The primary customers and end-users of Cutaneous Leishmaniasis drugs are highly centralized and institution-based, reflecting the nature of a neglected tropical disease where treatment is often managed by public health systems. The largest customer segment consists of national health ministries and governmental agencies in endemic countries across Latin America, South Asia, the Middle East, and Africa, who purchase drugs in bulk via tenders for national control programs and public clinics. These buyers prioritize low unit costs, high efficacy against local strains, and ease of storage and administration in low-resource settings, heavily influencing procurement decisions toward essential medicines lists.

A secondary, yet crucial, customer base includes international non-governmental organizations (NGOs) such as Médecins Sans Frontières (Doctors Without Borders), Partners in Health, and various charitable foundations dedicated to tropical medicine. These organizations operate in conflict zones and remote communities, often procuring the most recently developed or specialized treatments, including liposomal formulations, through direct agreements or donations. Their purchasing criteria emphasize logistical simplicity, robust clinical evidence, and suitability for field use, making them key early adopters of novel, safer therapies, especially those simplifying the treatment regimen.

Finally, specialized hospitals, infectious disease clinics, and travel medicine centers in developed countries (North America and Europe) constitute the third customer segment. These institutions treat imported cases and require a steady supply of high-quality systemic treatments, including branded and off-patent specialty drugs. These customers are less price-sensitive than governmental buyers but demand strict regulatory compliance and sophisticated diagnostic support, often utilizing the latest generation of combination or targeted treatments based on specific species identification for the visiting patient population.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350.5 million |

| Market Forecast in 2033 | USD 550.2 million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Gilead Sciences, GSK plc, Sanofi S.A., Johnson & Johnson, Bristol-Myers Squibb, Novartis AG, Pfizer Inc., F. Hoffmann-La Roche Ltd., Takeda Pharmaceutical Company Limited, Merck & Co., Inc., Cipla Ltd., Sun Pharmaceutical Industries Ltd., Almirall S.A., DNDi (Drugs for Neglected Diseases initiative), Knight Therapeutics Inc., G&W Laboratories, Inc., ViiV Healthcare, ProfoundBio, MacroGenics. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Cutaneous Leishmaniasis Drugs Market is focused on three main pillars: enhancing drug delivery systems for existing compounds, developing novel chemical entities targeting unique parasite vulnerabilities, and integrating genomic and computational tools for preclinical optimization. Liposomal technology represents a mature and critical delivery system, significantly reducing the nephrotoxicity associated with conventional Amphotericin B. This formulation encapsulates the drug within lipid bilayers, enabling preferential uptake by macrophages—the very cells where Leishmania parasites reside—thereby increasing efficacy and reducing systemic exposure, making it the preferred systemic treatment in many regions, despite its cost.

A second crucial technological area is the development of advanced topical formulations, aiming to deliver sufficient drug concentrations deep into the dermal lesions without systemic absorption, thus minimizing side effects. Technologies such as microemulsions, nanoparticles, and proprietary permeation enhancers are utilized to improve the skin penetration of drugs like Paromomycin or newer chemical entities. This technological focus directly addresses the need for simple, non-invasive treatments for uncomplicated cutaneous leishmaniasis, which accounts for the vast majority of cases, enhancing patient comfort and adherence, especially in pediatric populations, which are highly susceptible to the disease.

The third pillar involves the application of modern drug discovery techniques, leveraging high-throughput screening (HTS) and fragment-based drug design (FBDD) against novel Leishmania targets, such as parasitic kinases or unique proteases crucial for survival. Genomic sequencing technologies allow for rapid identification of strain-specific drug resistance mechanisms, guiding the development of broad-spectrum or tailored compounds. Furthermore, technologies focusing on host-directed therapies—modulating the host immune response to clear the infection—represent a developing frontier, often involving small molecule inhibitors that interfere with the parasite's ability to evade or manipulate the host macrophage environment, offering a fundamentally different treatment strategy.

The geographic analysis of the Cutaneous Leishmaniasis Drugs Market reveals significant heterogeneity in disease prevalence, species distribution, treatment protocols, and market access, strongly correlating with economic development and public health infrastructure maturity. Latin America, particularly Brazil, Colombia, Peru, and Bolivia, represents a critical market segment due to the hyper-endemic nature of the disease, driven by species like Leishmania braziliensis, which often leads to more aggressive mucocutaneous forms requiring intensive systemic treatment (Antimonials or Liposomal Amphotericin B). Institutional procurement programs, often supported by regional bodies like PAHO, dictate market volume and pricing strategies.

The Middle East and Africa (MEA), especially countries like Sudan, Ethiopia, Syria, and Afghanistan, face immense challenges due to ongoing conflicts and displacement, which exacerbates CL outbreaks. The demand here is overwhelming, primarily focused on low-cost, readily available systemic therapies like pentavalent antimonials, though resistance concerns are mounting. Market growth in MEA is highly dependent on large-scale humanitarian aid and donor-funded projects that subsidize drug costs and distribution logistics. The APAC region, concentrated in South Asia (India, Bangladesh), also demands specific therapeutics, although visceral leishmaniasis often receives greater focus; CL treatments are necessary, often driven by government efforts to integrate diagnostics and treatment at the primary health center level.

North America and Europe constitute smaller volume markets for CL treatment, characterized primarily by 'imported' cases related to travel, military deployment, or migration from endemic regions. Treatment in these areas often involves specialized infectious disease centers with access to high-cost, state-of-the-art diagnostics and treatments, particularly liposomal Amphotericin B, often used off-label for certain strains. The market function here is less about mass public health campaigns and more about premium pharmaceutical accessibility and precision medicine tailored to the specific imported species, supporting high per-unit revenue generation compared to endemic zones.

The primary challenges involve increasing drug resistance to traditional pentavalent antimonials, the high toxicity and complex intravenous administration required for first-line systemic treatments like Amphotericin B, and the need for simplified, oral, or topical regimens suitable for remote, resource-limited healthcare settings. Addressing the lack of commercial incentive for R&D in NTDs also remains a structural challenge.

The Alkylphospholipids segment, primarily driven by Miltefosine, and advanced liposomal formulations of Polyenes (Amphotericin B) are expected to show the fastest growth. Miltefosine is gaining prominence as the only available oral systemic treatment, improving patient adherence, while liposomal technology offers superior safety profiles over conventional antifungals, driving specialized hospital usage.

Institutional procurement, led by national governments, WHO, and international NGOs, is extremely significant, accounting for the majority of market volume, especially in high-burden, endemic countries. These entities determine accessibility and pricing through large-volume tenders and prioritize treatments listed as essential medicines, making institutional sales the critical distribution channel.

AI significantly accelerates drug discovery by facilitating high-throughput virtual screening of potential compounds against Leishmania-specific molecular targets. It also enables predictive modeling to forecast drug efficacy, toxicity, and potential resistance development, optimizing the preclinical phase and potentially identifying existing drugs for repurposing, thus speeding up pipeline development for NTDs.

Latin America and the Middle East and Africa (MEA) hold the highest potential for expansion based on the endemic population size and high disease burden. While MEA requires affordable, high-volume products for crisis control, Latin America drives demand for advanced systemic treatments due to the prevalence of species associated with more severe, non-healing forms of cutaneous and mucocutaneous leishmaniasis.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.