ID : MRU_ 435384 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

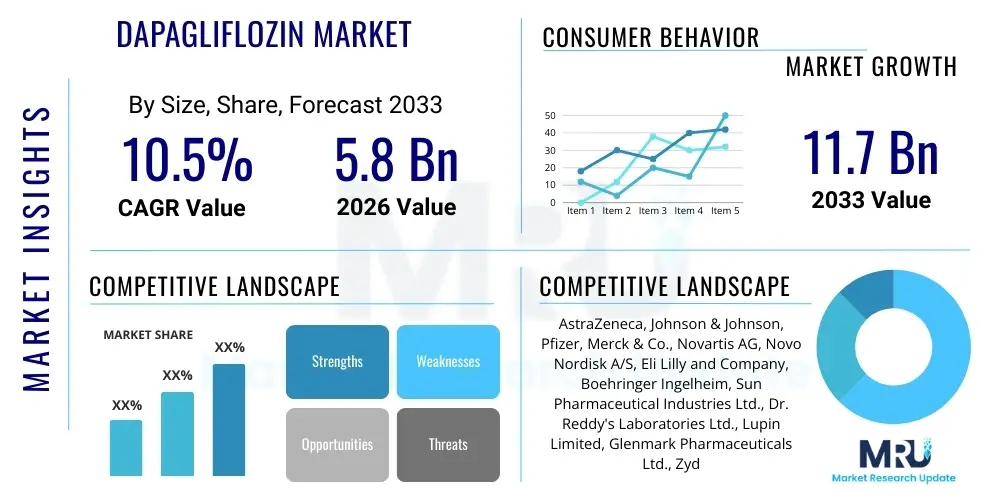

The Dapagliflozin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2026 and 2033. The market is estimated at USD 5.8 Billion in 2026 and is projected to reach USD 11.7 Billion by the end of the forecast period in 2033. This substantial growth trajectory is underpinned by the increasing global prevalence of Type 2 Diabetes Mellitus (T2DM) and the expanded clinical indications for Dapagliflozin, including heart failure (HF) and chronic kidney disease (CKD).

Dapagliflozin, a potent and selective sodium-glucose co-transporter 2 (SGLT2) inhibitor, represents a cornerstone therapy in the modern management of metabolic and cardiovascular diseases. Initially approved primarily for the control of blood glucose in adults with Type 2 Diabetes, its clinical utility has dramatically broadened following pivotal trial data demonstrating significant cardiorenal protective effects. This expansion into non-diabetic indications, particularly in heart failure with reduced ejection fraction (HFrEF) and chronic kidney disease, has fundamentally reshaped the competitive landscape of the pharmaceutical industry, positioning Dapagliflozin as a multi-indication blockbuster drug.

The primary mechanism of action involves the inhibition of SGLT2 in the renal tubules, reducing glucose reabsorption and promoting glycosuria, thereby lowering blood glucose levels independently of insulin. Beyond its antihyperglycemic effect, the drug confers substantial benefits related to reduced intraglomerular pressure, improved kidney oxygenation, and optimized cardiac volume status, making it a critical asset in managing complex comorbidities. Major applications span endocrinology, cardiology, and nephrology, reflecting its comprehensive therapeutic profile. Key benefits include superior glycemic control, weight loss, blood pressure reduction, and demonstrable reduction in hospitalization rates for heart failure and progression of kidney failure.

Market growth is predominantly driven by the escalating global burden of non-communicable diseases (NCDs), particularly T2DM and related cardiovascular complications. The robust evidence supporting Dapagliflozin's mortality and morbidity reduction across diverse patient populations accelerates its integration into international treatment guidelines, ensuring rapid adoption by healthcare providers. Furthermore, aggressive marketing strategies, favorable reimbursement policies in developed economies, and continuous lifecycle management through the investigation of new combination therapies and extended indications further fuel the drug's dominant market position.

The Dapagliflozin market is characterized by robust commercial growth driven by expanded clinical applicability and increasing physician confidence in SGLT2 inhibitors. Current business trends indicate a significant shift in prescription habits, moving Dapagliflozin from a second-line anti-diabetic agent to a foundational therapy recommended early in the treatment paradigms for diabetes, heart failure, and chronic kidney disease. Strategic collaborations between originator companies and generic manufacturers approaching patent expiry are anticipated, although core market stability remains strong due to intellectual property protection in key markets. Pricing strategies are nuanced, balancing premium positioning for novel indications with managed entry schemes in high-volume, developing regions.

Regionally, North America and Europe currently dominate the revenue landscape, attributed to high healthcare expenditure, established guidelines favoring SGLT2 inhibitors, and high prevalence rates of target diseases. However, the Asia Pacific (APAC) region is poised for the fastest expansion, fueled by burgeoning populations diagnosed with T2DM, improved access to specialized care, and rising awareness regarding the long-term benefits of cardiorenal protection. Latin America and the Middle East & Africa (MEA) are also exhibiting accelerated uptake, contingent on the successful navigation of regulatory hurdles and the implementation of governmental health initiatives focused on NCD management.

Segmentation trends highlight the increasing significance of the Chronic Kidney Disease (CKD) application segment, which is expected to register a disproportionately high growth rate compared to the traditional Type 2 Diabetes segment. By route of administration, the oral solid dosage form maintains near-total market share, reflecting its patient convenience and proven bioavailability. The formulation segment sees growth driven by fixed-dose combinations (FDCs) pairing Dapagliflozin with other established anti-diabetic agents, enhancing adherence and therapeutic efficacy for patients managing multiple pathologies.

User queries regarding the impact of Artificial Intelligence (AI) on the Dapagliflozin market frequently center on three critical themes: efficiency in drug discovery/repurposing, optimization of patient stratification for trial recruitment and clinical use, and personalization of dosing regimens. Users are particularly keen to understand if AI can accelerate the identification of novel, synergistic combination therapies involving Dapagliflozin, or if machine learning algorithms can predict which subsets of heart failure or CKD patients will derive the maximum cardiorenal benefit. Concerns also revolve around the integration of real-world data (RWD) collected via AI-driven patient monitoring systems to refine prescribing practices and detect rare adverse events more effectively than traditional pharmacovigilance.

The application of AI is primarily focused on enhancing clinical trial design and optimizing real-world evidence generation. AI algorithms are now routinely employed to analyze vast genomic and phenotypic datasets to better understand the mechanistic pathways modulated by Dapagliflozin, potentially uncovering new biomarkers for response and non-response. This allows pharmaceutical companies to target specific patient subpopulations in marketing and clinical education efforts, thereby maximizing the therapeutic index and commercial penetration. Furthermore, AI-powered predictive modeling is assisting in supply chain management and forecasting demand based on evolving treatment guidelines and regional epidemic trends.

The market dynamics for Dapagliflozin are dictated by a powerful combination of clinical necessity, rigorous regulatory affirmation, and competitive maneuvering. Key drivers include the overwhelming positive clinical trial evidence (such as the DAPA-HF and DECLARE-TIMI 58 trials) supporting multi-organ protection, which has led to rapid guideline inclusion by major medical societies globally. This is compounded by the rising incidence of co-morbidities where Dapagliflozin provides holistic management—a crucial selling point in integrated care systems. Market restraints, conversely, involve impending patent expirations in certain territories, requiring strategic planning for lifecycle management, and the persistent challenge of patient adherence due to potential adverse effects like genital mycotic infections or diabetic ketoacidosis, albeit rare.

Opportunities for sustained growth are substantial, primarily through the pursuit of further indications, particularly in pediatric diabetes or other inflammatory kidney diseases where SGLT2 inhibitors show promise. Developing fixed-dose combinations (FDCs) that integrate Dapagliflozin with metformin, DPP-4 inhibitors, or GLP-1 receptor agonists presents a significant opportunity to simplify complex therapeutic regimens and enhance patient compliance. Furthermore, penetrating underserved markets in emerging economies through differential pricing and public-private partnerships offers vast untapped revenue streams, provided local regulatory approval and affordability hurdles can be overcome efficiently.

The impact forces within this therapeutic class are intense. The competitive landscape is shaped by rivalry from other leading SGLT2 inhibitors (e.g., Empagliflozin and Canagliflozin), which similarly boast strong cardiorenal data. Regulatory policies, particularly the decisions of the FDA and EMA regarding label expansion and safety updates, act as powerful external forces instantly influencing prescribing behaviors. Internally, the research and development pipeline focused on next-generation SGLT2 derivatives or superior combination products represents an ongoing force, ensuring continuous innovation and competitive pressure to maintain therapeutic superiority and market share.

The Dapagliflozin market is comprehensively segmented based on its clinical applications, distribution channels, and formulation types, providing granular insights into market dynamics and growth potential across various therapeutic areas. The application segmentation, which includes Type 2 Diabetes Mellitus (T2DM), Heart Failure (HF), and Chronic Kidney Disease (CKD), is the most critical determinant of future growth, given the significant expansion driven by the latter two indications. Formulation segmentation primarily involves monotherapy and fixed-dose combinations, reflecting evolving treatment protocols aimed at optimizing patient adherence and clinical outcomes. Understanding these segments is vital for stakeholders to allocate resources effectively and tailor commercial strategies to specific patient populations and healthcare systems.

The value chain for Dapagliflozin starts with complex upstream activities, primarily encompassing active pharmaceutical ingredient (API) synthesis and rigorous quality assurance processes. The synthesis of Dapagliflozin involves specialized chemical manufacturing requiring high purity standards and adherence to Good Manufacturing Practices (GMP). Key upstream stakeholders include specialized chemical suppliers and contract manufacturing organizations (CMOs) focused on complex molecule production. Efficient management of these initial stages is crucial as API cost and quality directly impact the final product's profitability and regulatory compliance. Companies invest heavily in securing reliable, high-volume sourcing of raw materials to mitigate supply chain disruption risks, especially given the global demand for this widely prescribed drug.

The midstream phase involves the formulation, dosage manufacturing (primarily tablets), packaging, and inventory management. This stage is dominated by large pharmaceutical companies (like the originator, AstraZeneca) and their licensed manufacturing partners. Significant capital expenditure is allocated to sophisticated tablet presses and packaging lines necessary to meet stringent regulatory requirements across different geographic regions. Quality control is paramount during formulation to ensure dosage accuracy and stability, essential for patient safety and efficacy. Inventory systems must be finely tuned to manage short shelf-life constraints and fluctuating regional demand based on public health crises or seasonal changes in disease incidence.

Downstream activities focus on distribution and final dispensing, utilizing both direct and indirect channels. The direct channel involves distribution straight to major hospital systems and governmental tenders, often facilitated by the manufacturer's own sales force and logistic infrastructure for large-volume purchases. The indirect channel relies heavily on national and regional wholesalers and third-party logistics (3PL) providers, who handle storage and delivery to retail pharmacies, online platforms, and smaller clinics. The strength of the indirect network, coupled with effective market access strategies (including payer negotiations and reimbursement schemes), ultimately determines the drug's penetration and availability to the end-user. Pharmacists play a vital role in educating patients, particularly regarding the specific dosing requirements and potential adverse effects of SGLT2 inhibitors.

The potential customer base for Dapagliflozin is exceptionally broad and multidisciplinary, extending far beyond the traditional endocrinology domain. Primary end-users include adult patients suffering from Type 2 Diabetes Mellitus who require improved glycemic control, often in combination with agents like metformin. A rapidly growing segment comprises patients diagnosed with chronic heart failure, irrespective of their diabetic status (HFrEF and HFpEF are emerging), seeking therapies proven to reduce hospitalizations and cardiovascular mortality. Furthermore, individuals with Chronic Kidney Disease (CKD), particularly those at risk of progression to end-stage renal disease (ESRD), form a critical, high-value customer group due to the demonstrated nephroprotective effects of Dapagliflozin, as evidenced by the DAPA-CKD trial outcomes.

The professional buyers and prescribers are highly specialized and diverse. Endocrinologists remain fundamental in initiating therapy for diabetic patients. However, cardiologists are now significant prescribers, adopting Dapagliflozin as a standard-of- care intervention following heart failure guidelines updates. Nephrologists are also becoming key influencers and prescribers, leveraging the drug's demonstrated ability to slow kidney function decline. This necessitates targeted educational and marketing strategies customized to the distinct informational needs and clinical guidelines governing each specialty, emphasizing the drug's multi-system benefits rather than solely its glucose-lowering properties.

Beyond individual patients and specialist physicians, institutional buyers represent high-volume potential customers. These include integrated healthcare networks, governmental health insurance providers (e.g., NHS in the UK, Medicare/Medicaid in the US), large academic medical centers, and pharmacy benefit managers (PBMs). These entities are focused on pharmacoeconomic value, seeking therapies that reduce long-term costs associated with major cardiovascular and renal events. Therefore, demonstrating cost-effectiveness and favorable quality-adjusted life years (QALYs) data is crucial for securing preferred formulary placement and national tender contracts, which significantly boost overall market penetration and revenue volume.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 11.7 Billion |

| Growth Rate | 10.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AstraZeneca, Johnson & Johnson, Pfizer, Merck & Co., Novartis AG, Novo Nordisk A/S, Eli Lilly and Company, Boehringer Ingelheim, Sun Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories Ltd., Lupin Limited, Glenmark Pharmaceuticals Ltd., Zydus Cadila, Takeda Pharmaceutical Company Limited, Sanofi S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology driving the Dapagliflozin market centers on the pharmaceutical synthesis and specialized formulation technologies required for SGLT2 inhibitors. The chemical synthesis pathway involves complex organic chemistry to produce the highly selective Dapagliflozin molecule (a C-glucoside). Protecting the proprietary synthetic routes and ensuring enantiomeric purity are critical technological aspects. Furthermore, the development of robust, stable, and bioavailable oral solid dosage forms necessitates advanced tableting and coating technologies. These formulation technologies must guarantee drug stability under various environmental conditions and ensure consistent dissolution profiles crucial for predictable patient absorption and efficacy, particularly in combination products.

Beyond the fundamental drug manufacturing process, the technological landscape is increasingly shaped by advancements in drug delivery and combination product development. Fixed-dose combination (FDC) technology requires precise control over API compatibility and release profiles when pairing Dapagliflozin with other agents (e.g., DPP-4 inhibitors). Specialized matrix systems or dual-layer tablets are often employed to manage distinct pharmacokinetic requirements within a single pill, improving patient adherence by reducing pill burden. Technological licensing and cross-company collaboration are essential components of FDC development, leveraging shared expertise in formulation science to rapidly bring complex therapeutic options to market.

The peripheral technology landscape includes significant investment in digital health platforms and patient monitoring solutions that indirectly support Dapagliflozin uptake. Telemedicine and AI-driven remote monitoring systems are critical for managing patients with chronic conditions like HF and CKD, allowing physicians to track efficacy and side effects in real-time. Smart packaging and digital adherence tools (e.g., sensor-enabled pill bottles) represent emerging technologies aimed at enhancing therapeutic compliance, ensuring patients consistently take their Dapagliflozin doses, thereby maximizing clinical outcomes and reinforcing its value proposition to payers and healthcare providers.

The primary driver is the expansion of Dapagliflozin's clinical indications beyond Type 2 Diabetes to include treatment for Chronic Kidney Disease (CKD) and Heart Failure (HF) regardless of diabetic status. This significant broadening of the addressable patient population, supported by robust evidence from major cardiorenal outcome trials, mandates its incorporation into global clinical guidelines.

Dapagliflozin is one of the leading SGLT2 inhibitors, maintaining a significant share alongside Empagliflozin (Jardiance). Competition is fierce, with market share often fluctuating based on regional prescribing habits, specific guideline recommendations (especially for non-diabetic indications), and successful formulation strategies, such as fixed-dose combinations.

Key constraints include the anticipated generic erosion following major patent expiry dates in certain high-volume territories post-2027. Furthermore, mitigating patient non-adherence due to known, though manageable, adverse effects like genital mycotic infections and educating prescribers on the correct management of these risks remain challenges.

The Asia Pacific (APAC) region is projected to exhibit the highest CAGR during the forecast period. This acceleration is driven by the vast, underserved patient population in countries like China and India experiencing rapid increases in diabetes and associated cardiovascular diseases, coupled with improved access to advanced therapies.

Fixed-dose combinations (FDCs), pairing Dapagliflozin with established anti-diabetic agents like metformin, are crucial for future market strategy. FDCs improve patient compliance, simplify complex treatment regimens, and act as a lifecycle management tool to sustain market presence and revenue streams as monotherapy patents approach expiration.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.