ID : MRU_ 431703 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

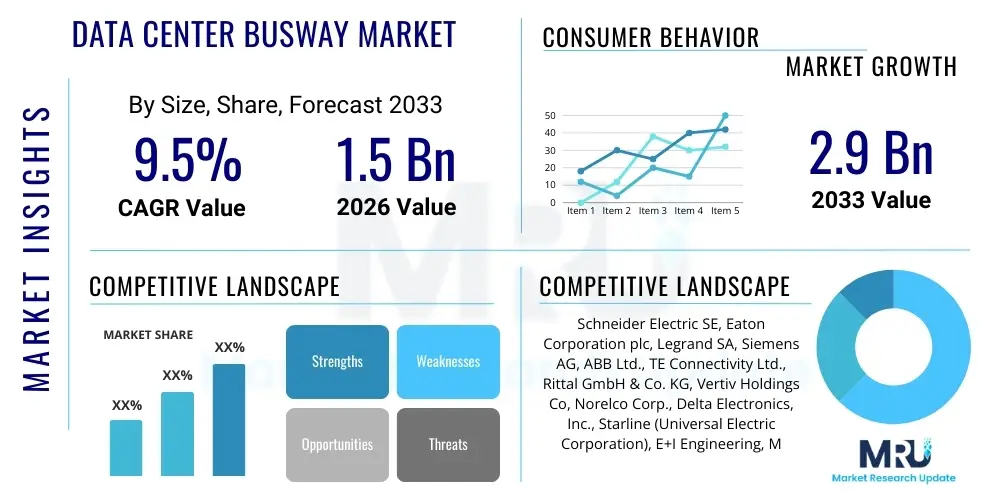

The Data Center Busway Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 2.9 Billion by the end of the forecast period in 2033.

The Data Center Busway Market encompasses high-efficiency, modular power distribution systems designed to replace traditional cabling and conduit solutions within mission-critical facilities. Busway systems, often characterized by their standardized, insulated metallic enclosures containing copper or aluminum conductors, provide flexible and scalable power delivery from the main power source to server racks. This inherent modularity allows data center operators to rapidly scale their infrastructure and manage increasing power densities without significant downtime, making them essential infrastructure for modern, high-performance computing environments.

The primary applications of busway systems within data centers span across hyperscale facilities, large colocation providers, and high-density enterprise data centers, where efficient space utilization and superior electrical performance are paramount. These systems offer significantly lower impedance compared to large cable bundles, reducing energy losses and improving overall Power Usage Effectiveness (PUE). Furthermore, the simplified installation process and reduced physical footprint contribute directly to faster deployment times and optimized floor planning, which are critical factors in competitive data center operations.

Key driving factors accelerating the adoption of busway technology include the unprecedented expansion of cloud services, which necessitates the construction of massive hyperscale facilities, and the consistent upward trend in server rack power density driven by demanding workloads such as artificial intelligence and big data analytics. The need for enhanced safety features, superior thermal performance, and quick reconfigurability in dynamic data center environments further solidifies the busway system's position as the preferred power distribution backbone.

The Data Center Busway Market is undergoing substantial transformation, primarily driven by the imperative for scalable and energy-efficient power distribution systems capable of handling hyper-dense computing environments. Current business trends indicate a strong industry shift towards Low Voltage (LV) and Medium Voltage (MV) busways designed for higher amperage ratings, often exceeding 1,600 Amps, to support 50kW+ racks. This pivot reflects the need to minimize power loss across long distribution runs in massive data center campuses, emphasizing modular plug-and-play features for enhanced operational flexibility and reduced installation time, crucial for minimizing capital expenditure delays.

Regionally, the Asia Pacific (APAC) market is exhibiting the fastest growth, fueled by exponential digitalization, significant government investment in IT infrastructure, and the construction of numerous hyperscale data centers in emerging economies like India, China, and Southeast Asia. While North America remains the dominant revenue generator due to the presence of major cloud providers and high technological maturity, growth in APAC is expected to narrow this gap. European markets are characterized by stringent energy efficiency regulations, driving demand for intelligent, monitoring-enabled busway systems that contribute positively to sustainability metrics.

Segment-wise, the Low Voltage Busway segment maintains the largest market share due to its direct application within the white space for rack-level power delivery, though the Medium Voltage Busway segment is seeing increased adoption for primary distribution feeds in large-scale facilities to minimize transformation losses. Hyperscale data centers represent the highest revenue generating application, requiring standardized, high-volume deployments, while colocation facilities prioritize highly configurable and granularly monitored busway solutions to accurately bill and manage multi-tenant power loads.

The proliferation of Artificial Intelligence (AI) and Machine Learning (ML) workloads is fundamentally reshaping the design requirements for data center power infrastructure, leading to a critical need for high-capacity busway systems. Common user questions revolve around whether existing busway infrastructure can support the extreme power density demanded by AI clusters (often exceeding 50 kW per rack), the effectiveness of busways in mitigating heat generated by high amperage draws, and the necessity of integrating real-time power monitoring to optimize AI resource allocation. The core themes users seek clarification on include thermal management strategies, the feasibility of DC busway adoption for AI efficiency, and the long-term scalability of power systems for continuous AI growth.

The summarized key themes indicate that AI acts as a profound accelerator for the Data Center Busway Market, pushing the boundary of power delivery requirements far beyond traditional enterprise needs. AI necessitates specialized busways with enhanced current carrying capacity, superior thermal dissipation characteristics, and integrated digital intelligence for granular power monitoring and load balancing. Users expect that busway manufacturers must rapidly innovate to produce systems that handle higher fault current levels and maintain operational safety while delivering unprecedented power levels to graphics processing unit (GPU) heavy racks.

The expectation is that future busway designs will incorporate sensor technology for predictive maintenance and instantaneous load shifting, ensuring continuous uptime crucial for intensive training models. This shift demands modularity not just for scaling but also for rapid reconfiguration of power zones as AI cluster sizes fluctuate. Consequently, the average ampere rating and the sophistication of monitoring features within the busway infrastructure are expected to rise exponentially throughout the forecast period due to direct pressure from AI/ML deployment.

The dynamics of the Data Center Busway Market are primarily governed by the continuous global expansion of digitalization and the increasing intensity of cloud and hyperscale deployments (Drivers), balanced against significant initial capital outlay and complex regulatory landscapes (Restraints). Opportunities primarily lie in leveraging emerging market demands such as edge computing infrastructure and integrating power systems with advanced monitoring capabilities (IoT integration). These forces collectively create a high-impact environment where modularity, power efficiency, and scalability are critical competitive differentiators, forcing vendors to prioritize robust product development and simplified deployment models.

Key drivers include the massive build-out of hyperscale data centers by technology giants, coupled with the relentless increase in rack power density driven by AI and high-performance computing (HPC) applications, making efficient power distribution indispensable. Furthermore, the inherent safety advantages of busway systems over traditional cable trays—offering better fire resistance and reduced risk of human error during maintenance—contribute significantly to market momentum. The global push for improved energy efficiency in data centers also favors busway technology due to its superior power transmission efficiency compared to copper cabling, directly impacting the facility’s PUE targets.

Conversely, significant restraints hinder market penetration, notably the substantial initial capital expenditure required for installing high-capacity busway infrastructure compared to conventional cable solutions, posing a barrier for smaller enterprise data centers. Furthermore, the lack of complete standardization across busway manufacturers regarding tap-off boxes and modular components can complicate multi-vendor integration and expansion plans for data center operators. However, opportunities abound in the proliferation of smaller, distributed edge data centers requiring compact, highly reliable busway systems, and the potential integration of busways with advanced cooling solutions like liquid cooling to address extreme power loads effectively.

The Data Center Busway Market is segmented across various dimensions, including voltage type, conductor material, end-user application, and structural configuration, enabling a granular view of market dynamics. Understanding these segments is crucial as design choices directly impact a facility's efficiency, cost, and long-term scalability. The segmentation reflects the diverse needs ranging from massive hyperscale power distribution requirements to highly customized enterprise installations.

By voltage type, the market is distinctly divided into Low Voltage (LV) and Medium Voltage (MV) segments, corresponding to their function in primary versus secondary power distribution within the data center environment. Conductor material segmentation highlights the cost versus performance trade-off between copper (high performance, higher cost) and aluminum (cost-effective, lighter weight) options, influencing deployment choices based on facility size and budget constraints. Application segmentation clearly delineates the demand profiles of hyperscale cloud providers, colocation facilities, and enterprise data centers, each requiring specific levels of modularity and monitoring sophistication.

The analysis of these segments reveals that while the LV segment currently dominates due to direct white space applicability, the MV segment is poised for robust growth as data center campuses expand and seek to minimize transmission losses over long distances. Hyperscale deployment remains the fastest growing application segment, continuously setting the benchmark for required amperage ratings and demanding highly standardized, rapidly deployable busway products.

The value chain for the Data Center Busway Market begins with the upstream procurement of essential raw materials, primarily high-conductivity copper and aluminum conductors, and specialized insulating materials like epoxy resins and plastics. Supply chain resilience in sourcing these base metals is critical, as volatility in commodity prices directly impacts manufacturing costs and, consequently, final market prices. Efficient manufacturing processes, including precision engineering for metallic enclosures and stringent quality control for conductor insulation, are vital to ensure product reliability and compliance with safety standards required for mission-critical data center environments.

The midstream stage involves the highly specialized manufacturing of busway components, including straight lengths, elbows, tap-off units, and joint packs, often customized according to project specifications regarding amperage and configuration. Manufacturers invest heavily in automated production lines to maintain consistency and high volumes required for large data center projects. Following production, the distribution channel plays a pivotal role, relying heavily on a combination of direct sales and indirect channels, utilizing specialized electrical distributors, value-added resellers (VARs), and system integrators who possess deep domain knowledge in data center design and power infrastructure.

Downstream activities are dominated by specialized installation, commissioning, and post-sales maintenance services. Due to the critical nature of data center power, installation is almost always managed by certified contractors with expertise in high-amperage systems. Direct distribution ensures better control over complex project timelines and technical support for hyperscale clients, while indirect channels provide wider geographical reach and cater more effectively to smaller or regional enterprise deployments. Ultimately, the integration of service and maintenance into the offering lifecycle, often including preventative maintenance and smart monitoring services, defines the long-term value delivered to the end-users.

The primary consumers and end-users of Data Center Busway systems are entities that operate power-intensive, mission-critical computing infrastructure requiring high reliability and rapid scalability. Hyperscale cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud represent the largest segment of potential customers. These giants require standardized, massive volumes of high-amperage busway to power their extensive, rapidly expanding global data center campuses, emphasizing total cost of ownership (TCO) and speed of deployment over component customization.

Colocation service providers constitute another significant customer base. Companies like Equinix and Digital Realty rely on busway systems to deliver flexible, reliable power feeds to hundreds of diverse tenants. For colocation customers, the busway's modularity allows for quick reconfigurations and precise power metering capabilities, which are essential for accurate billing and managing multi-tenant power loads and service level agreements (SLAs). The ability to deploy power infrastructure quickly and safely is a major factor driving colocation adoption.

Furthermore, large enterprises within the Banking, Financial Services, and Insurance (BFSI) sector, along with major players in IT and Telecommunication, represent highly sensitive end-users. These organizations often operate proprietary, high-density data centers where uptime is absolutely non-negotiable. They seek busway systems offering enhanced redundancy, superior fault protection, and advanced monitoring capabilities to ensure stringent regulatory compliance and business continuity. The increasing decentralization of IT architecture is also making edge data center operators a rapidly emerging customer segment, requiring compact, robust, and often outdoor-rated busway solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.9 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Schneider Electric SE, Eaton Corporation plc, Legrand SA, Siemens AG, ABB Ltd., TE Connectivity Ltd., Rittal GmbH & Co. KG, Vertiv Holdings Co, Norelco Corp., Delta Electronics, Inc., Starline (Universal Electric Corporation), E+I Engineering, Mersen S.A., Connect Busway, Power Distribution, Inc. (PDI), C&S Electric Limited, DB Power, Elmeasure India Pvt Ltd, Lonsdale Electric, EAE Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Data Center Busway Market is rapidly evolving towards smarter, higher-capacity, and more flexible systems, moving beyond passive power conductors. A dominant trend is the integration of advanced IoT and monitoring capabilities, transforming traditional busways into 'Smart Busways.' These systems incorporate embedded sensors within the enclosure and tap-off units to provide real-time data on current draw, voltage fluctuations, temperature profiles, and fault locations. This granular data is essential for data center infrastructure management (DCIM) platforms, allowing operators to optimize load balancing, enhance capacity planning, and implement predictive maintenance schedules, significantly improving PUE and reliability.

Another crucial technological advancement is the focus on extremely high amperage ratings and robust thermal performance to support 50 kW and greater rack densities driven by AI and HPC clusters. This requires innovations in conductor design—often shifting towards specialized sandwich-style conductors or high-density copper configurations—and improved enclosure materials that facilitate better heat dissipation while maintaining critical electrical separation and safety standards. Furthermore, manufacturers are exploring advanced insulation techniques, such as non-hygroscopic epoxy systems, to enhance dielectric strength and fire resistance within demanding, high-temperature operating environments.

Finally, the growing discussion around energy efficiency is prompting research into DC (Direct Current) Busway systems, primarily for distributing power within the data center, bypassing multiple AC-DC conversion stages. While AC busway currently dominates, DC systems promise reduced power loss, especially in environments supporting high-voltage DC equipment. Parallelly, the rise of modular and prefabricated data centers is driving innovation in quick-connect, tool-less busway systems, drastically reducing installation complexity and time on-site, aligning with the industry's need for rapid global deployment and standardization.

Busway systems offer superior energy efficiency due to lower impedance, enhanced flexibility and modularity for rapid expansion or reconfiguration, reduced physical footprint for better air flow, and improved safety features compared to cumbersome and often fire-prone traditional cabling infrastructure.

AI and HPC workloads dramatically increase rack power density, necessitating busway systems with significantly higher amperage ratings (often 1,600A to 4,000A) and advanced thermal management capabilities to safely and efficiently deliver large amounts of power while minimizing transmission losses within the facility.

Yes, HVDC busway is gaining viability, particularly in specialized power environments, as it eliminates conversion steps, reducing power loss and improving overall PUE. While AC remains standard, DC busway is increasingly explored for integration with specific server architectures and renewable energy sources.

Operators must primarily prioritize current capacity, cost, and weight. Copper offers higher conductivity and lower impedance but is heavier and more costly. Aluminum provides a lighter, more cost-effective solution, making it popular for very long runs or facilities with weight restrictions, though it requires larger cross-sections for equivalent current ratings.

A Smart Busway integrates IoT sensors and monitoring hardware to provide real-time data on power draw, voltage, and temperature at the busway level. This intelligence facilitates proactive maintenance, precise load balancing, accurate capacity planning, and integration with DCIM systems for optimal operational efficiency.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.