ID : MRU_ 432531 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

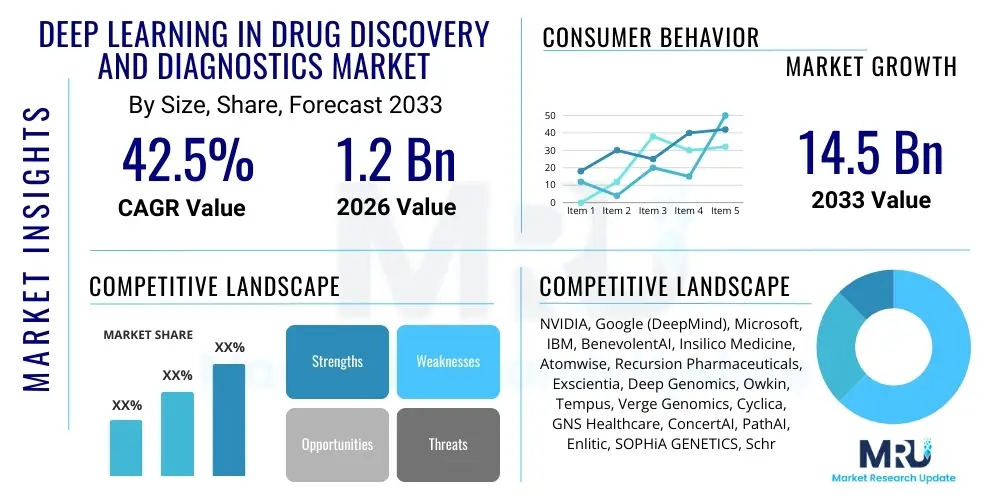

The Deep Learning in Drug Discovery and Diagnostics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 42.5% between 2026 and 2033. The market is estimated at $1.2 Billion in 2026 and is projected to reach $14.5 Billion by the end of the forecast period in 2033.

The Deep Learning (DL) in Drug Discovery and Diagnostics Market encompasses the application of sophisticated neural networks—such as Convolutional Neural Networks (CNNs), Recurrent Neural Networks (RNNs), and Generative Adversarial Networks (GANs)—to revolutionize the pharmaceutical and clinical pathology industries. This technology leverages massive biological, chemical, and patient data sets to accelerate the most complex stages of R&D, significantly reducing the time and cost associated with bringing a new therapeutic agent or diagnostic tool to market. The core product offering includes specialized software platforms, predictive modeling tools, and integrated service solutions designed for high-throughput screening, target identification, compound optimization, and automated medical image analysis.

Major applications driving market expansion include the acceleration of hit-to-lead and lead optimization processes, enabling the design of novel molecules with optimized pharmacokinetic properties (ADME/Tox prediction). In the diagnostic realm, deep learning models are critically utilized for enhancing the accuracy and speed of medical image interpretation (e.g., radiology, pathology slides), personalized risk stratification, and the identification of subtle biomarkers undetectable by traditional methods. These capabilities fundamentally address the current limitations of traditional research, which often suffers from high failure rates and protracted timelines in early-stage development.

The primary benefits driving the rapid adoption of deep learning include unprecedented efficiency gains, enhanced precision in prediction, and the potential to unlock treatments for previously intractable diseases. Key driving factors include the exponential growth in biological data (genomic, proteomic, clinical trial data), substantial investments from pharmaceutical giants and venture capitalists in AI startups, and increasing regulatory acceptance of AI-driven tools, positioning deep learning as a pivotal technology transforming biomedical research globally.

The Deep Learning in Drug Discovery and Diagnostics Market is characterized by intense innovation, significant strategic partnerships, and substantial financial backing, primarily targeting the pharmaceutical research bottleneck and improving clinical decision support. Business trends indicate a shift towards end-to-end integrated platforms that combine data management, model development, and regulatory submission support, moving beyond siloed, task-specific tools. Furthermore, M&A activity is robust, with large established technology firms and pharmaceutical companies acquiring niche AI biotechs to internalize core deep learning capabilities and secure intellectual property related to proprietary algorithms and novel compound libraries generated through AI.

Regionally, North America maintains market dominance due to early adoption, high levels of governmental and private funding for biomedical research, and the presence of leading technological giants and established biotechnology clusters. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth rate, fueled by expanding healthcare infrastructure, vast, diverse patient populations generating large datasets, and increasing governmental initiatives promoting digital transformation in healthcare and life sciences. Europe also represents a significant market, emphasizing explainable AI (XAI) due to stringent regulatory environments like GDPR and focusing on collaborative research between academia and industry.

Segment trends reveal that the Drug Discovery application segment, particularly target identification and lead optimization, holds the largest market share due to the immediate financial incentive of accelerating the drug pipeline and reducing late-stage failures. However, the Diagnostics segment is projected to grow rapidly, driven by the increasing integration of AI in clinical settings for automated pathology, radiological screening, and genomic sequencing interpretation, proving crucial for realizing the promise of personalized medicine. Technology-wise, Convolutional Neural Networks (CNNs) remain predominant, especially within diagnostics and image-based drug screening, while generative models like GANs are rapidly gaining traction in novel molecular design and synthesis planning.

Common user questions surrounding the impact of AI in this sector often center on validation and trust: "How reliable are AI-generated drug candidates compared to traditional methods?", "What are the regulatory pathways for AI-diagnostics?", and "Can AI models truly handle the complexity and diversity of human biological data without introducing bias?" These inquiries reflect a necessary skepticism regarding model explainability, data privacy, and the reproducibility of results derived from black-box algorithms. Users are also highly interested in the economic impact, specifically asking about the projected Return on Investment (ROI) from deep learning integration, the necessary expertise required for deployment, and how AI might shift the fundamental roles of research scientists and clinical pathologists.

The key themes emerging from user expectations revolve around AI’s potential to dramatically lower the cost of Phase I failures by improving preclinical toxicity prediction and enhancing target specificity, thereby de-risking the entire drug development process. In diagnostics, expectations focus on achieving near-perfect diagnostic accuracy for complex diseases like cancer and neurodegenerative disorders, enabling earlier intervention and precision treatment planning. The collective consensus points towards AI being an indispensable tool that augments human expertise, moving the industry away from slow, iterative experimentation towards predictive, hypothesis-driven discovery cycles. Regulatory bodies are increasingly responding to these concerns by issuing guidelines focusing on dataset diversity, model robustness, and transparent documentation, addressing the urgent need for verifiable and trustworthy AI solutions in high-stakes healthcare environments.

The profound integration of deep learning models has shifted the paradigm from empirical screening to computational prediction. This transformation has necessitated new infrastructures capable of handling petabytes of multi-omics data and has spurred the development of specialized talent skilled in both biology/chemistry and machine learning engineering. AI’s influence extends beyond mere efficiency; it is enabling the discovery of entirely new classes of therapeutic targets and diagnostic biomarkers that were previously inaccessible, fundamentally redefining the scientific approach to biological complexity and disease mechanisms. The industry anticipates that within the forecast period, the majority of initial drug targets and diagnostic protocols for novel diseases will be, at least in part, identified or optimized using deep learning frameworks, establishing AI as the central engine of biomedical innovation.

The market expansion is fundamentally shaped by powerful drivers, persistent restraints, and significant long-term opportunities, all interacting to form critical impact forces. The primary drivers include the urgent need for efficient drug development models given the soaring R&D costs and diminishing returns from traditional methods, coupled with the explosion of high-quality, high-volume biological data accessible through high-throughput sequencing and electronic health records (EHRs). These drivers create an immediate demand signal for predictive deep learning solutions capable of mining complex biological relationships. However, progress is tempered by significant restraints, namely the scarcity of interdisciplinary talent skilled in both clinical science and deep learning engineering, the inherent "black box" nature of complex neural networks challenging regulatory approval (the explainability issue), and pervasive concerns regarding data privacy, security, and the fragmentation of clinical data sources across institutions.

Opportunities for exponential growth are concentrated in untapped areas such as the application of deep learning in precision oncology, rare disease therapeutics, and personalized biomarker development for autoimmune disorders. The ability of deep learning to rapidly integrate multi-omics data (genomics, transcriptomics, proteomics, metabolomics) presents an opportunity to move beyond single-target therapies towards complex polypharmacology approaches. Furthermore, the development of robust, federated learning frameworks provides a pathway to leverage decentralized clinical data without compromising patient privacy, thereby overcoming a major data access restraint. These opportunities encourage continuous investment and technological refinement, ensuring the long-term viability and disruptive potential of the market.

The impact forces synthesized from these dynamics are compelling. The positive impact force is the undeniable economic imperative to cut costs and accelerate time-to-market, forcing pharmaceutical companies to integrate deep learning as a core competency rather than a peripheral tool. Conversely, the negative impact force stems from the high initial capital investment required for computational infrastructure and specialized personnel, creating a significant barrier to entry for smaller firms and potentially widening the gap between technology leaders and laggards. Ultimately, the market trajectory will be determined by the speed at which regulatory bodies adapt to and standardize approval pathways for AI-driven discoveries, thereby translating technological potential into widespread clinical and commercial reality.

The Deep Learning in Drug Discovery and Diagnostics Market is meticulously segmented based on Application, Component, Technology, and End-User, reflecting the diverse deployment strategies across the life sciences ecosystem. This structured segmentation allows for focused technological development and precise market targeting. The analysis highlights that while the tools and technologies (Component and Technology segments) are crucial for market enablement, the ultimate growth and value creation are realized through specific clinical and research applications, particularly in oncology diagnostics and novel drug candidate generation, which attract the majority of investment capital and partnership focus.

The Application segment demonstrates the clearest delineation of market value, with Drug Discovery applications commanding dominance due to their direct influence on pipeline profitability. Within Diagnostics, the utilization of deep learning in medical imaging analysis—including MRI, CT, and histological slides—is experiencing exponential growth, driven by the immediate clinical benefits of reduced human error and increased throughput. This segment is characterized by rapid deployment in clinical decision support systems and high demand for software-as-a-service (SaaS) models tailored for hospital networks and large diagnostic centers seeking operational efficiency improvements.

Technologically, the differentiation between models like CNNs, optimized for image and sequence recognition, and generative models, optimized for designing novel outputs (molecules or data), indicates evolving R&D priorities. End-user analysis underscores the pivotal role of Pharmaceutical and Biotechnology companies as the primary revenue generators, driven by large licensing agreements and custom model development contracts. However, the academic and research institutes segment is critical for foundational model development and public validation, often serving as crucial early adopters and providers of foundational, high-quality training datasets that fuel commercial advancements.

The value chain for deep learning in this sector is highly complex, starting with the foundational upstream elements involving data generation and foundational technology supply. Upstream analysis focuses on technology providers such as high-performance computing (HPC) infrastructure developers (e.g., NVIDIA, AWS, Google Cloud) and proprietary biological data generators (genomic sequencing providers, biobanks, EHR vendors). These entities provide the necessary computational power and standardized, high-quality raw materials (data) that are essential for training complex deep learning models. The quality, accessibility, and standardization of these upstream data sources directly dictate the effectiveness and non-biased nature of the resulting predictive models.

The midstream segment involves the core intellectual property and platform development, comprising specialized AI companies (e.g., Insilico Medicine, BenevolentAI) and dedicated data science units within larger pharmaceutical companies. This stage focuses on algorithm design, model training, validation, and the creation of user-friendly platforms and APIs that translate raw data and algorithms into usable scientific predictions. Distribution channels here are primarily direct, involving licensing agreements, strategic partnerships, and enterprise subscriptions for cloud-based software solutions. Indirect channels involve integration through CROs or specialized consulting firms that act as intermediaries, tailoring generic AI platforms for specific client R&D requirements.

Downstream analysis focuses on the final application and adoption of the deep learning output by end-users. This includes pharmaceutical R&D departments utilizing predicted novel targets, clinical trials leveraging AI-optimized patient selection, and diagnostic centers employing automated image analysis tools for patient care. The success at this stage is measured by tangible outcomes: reduced time-to-market for drugs, increased diagnostic accuracy, and improved patient outcomes. Effective collaboration between midstream platform developers and downstream clinical practitioners is paramount for model refinement and ensuring the practical utility and regulatory compliance of AI-driven tools in real-world clinical and research environments, establishing a high-value feedback loop.

The potential customer base for deep learning solutions in drug discovery and diagnostics is diverse yet highly concentrated among entities dealing with large-scale biomedical data processing and R&D acceleration challenges. The most significant end-users are large multinational Pharmaceutical and Biotechnology Companies. These organizations are driven by the urgent need to replenish diminishing drug pipelines and control escalating R&D expenditures, making them prime candidates for investing heavily in predictive models for target identification, lead optimization, and toxicology screening. Their demand is centered around bespoke solutions, large-scale data integration, and secure, on-premise or compliant private cloud deployments, ensuring data exclusivity and regulatory adherence.

Another rapidly expanding customer segment includes Academic and Research Institutes, often leveraging government grants and institutional funding to explore foundational deep learning applications. While their purchasing power may be lower than large pharma, they are critical for validating new model architectures, generating public domain data sets, and developing open-source tools that ultimately push the boundaries of the field. These institutions primarily seek cost-effective, high-performance computing resources and collaborative licensing arrangements to utilize advanced deep learning software platforms for fundamental biological research and disease mechanism elucidation.

Furthermore, Diagnostic Centers and Hospital Networks represent a crucial vertical, especially for applications related to medical imaging, digital pathology, and clinical decision support systems. These customers seek tools that can integrate seamlessly into existing Electronic Health Record (EHR) and Picture Archiving and Communication System (PACS) infrastructure, prioritizing real-time processing capabilities, high throughput, and verifiable clinical accuracy to improve patient triage and reduce clinical labor costs. Finally, Contract Research Organizations (CROs) act as crucial intermediaries, adopting deep learning tools to enhance the efficiency of their services (e.g., clinical trial design, biomarker analysis) offered to pharma and biotech clients, thereby expanding the reach of these AI technologies across the industry supply chain.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.2 Billion |

| Market Forecast in 2033 | $14.5 Billion |

| Growth Rate | CAGR 42.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | NVIDIA, Google (DeepMind), Microsoft, IBM, BenevolentAI, Insilico Medicine, Atomwise, Recursion Pharmaceuticals, Exscientia, Deep Genomics, Owkin, Tempus, Verge Genomics, Cyclica, GNS Healthcare, ConcertAI, PathAI, Enlitic, SOPHiA GENETICS, Schrödinger |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Deep Learning in Drug Discovery and Diagnostics market relies on a specialized technological ecosystem centered around high-performance computing and nuanced neural network architectures tailored for complex biological data. The dominant technological frameworks include TensorFlow, PyTorch, and Keras, which provide the underlying infrastructure for building, training, and deploying large-scale neural networks. Hardware acceleration, predominantly through NVIDIA’s specialized Graphics Processing Units (GPUs) and increasingly Application-Specific Integrated Circuits (ASICs), is indispensable for handling the massive computational load required for molecular dynamics simulations, image segmentation, and deep genomic sequencing analysis, effectively defining the practical scale of research capabilities.

Specific neural network types dictate the effectiveness within different application segments. Convolutional Neural Networks (CNNs) are the foundational technology for diagnostics, excelling in pattern recognition in visual data. They are extensively used in analyzing medical images (CT, MRI), pathological slides (histopathology analysis for cancer staging), and phenotypic screens in drug discovery. Their ability to automatically learn hierarchical spatial features makes them unparalleled for tasks like tumor boundary detection and classification. Similarly, Recurrent Neural Networks (RNNs) and Long Short-Term Memory (LSTM) networks are essential for sequence data analysis, particularly in genomics, where they process linear biological data like DNA, RNA, and protein sequences to predict structure, function, and regulatory elements. The use of Transformer models, initially popularized in natural language processing (NLP), is rapidly expanding into protein structure prediction and molecular interaction modeling, offering superior handling of long-range dependencies in sequence data compared to traditional RNNs.

Furthermore, Generative Models such as Generative Adversarial Networks (GANs) and Variational Autoencoders (VAEs) are critical for the cutting-edge application of De Novo Drug Design. These models are employed not just to screen existing libraries, but to create novel molecular scaffolds with specific desired properties, overcoming the limitations of pre-existing chemical space. The technological landscape is also increasingly focused on developing methods for Explainable AI (XAI), which seeks to provide transparent rationales for the model's predictions. This is achieved through techniques like SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-agnostic Explanations), which are crucial for gaining regulatory approval and clinical trust, particularly in high-risk diagnostic and therapeutic decisions. The synthesis of these hardware, framework, and model innovations drives the market’s capability to automate and optimize traditionally manual and labor-intensive processes.

Deep Learning significantly accelerates R&D by improving the accuracy of target identification, predicting molecular properties (ADME/Tox) early in the pipeline, and enabling the computational design of novel chemical entities (de novo design), thereby drastically reducing the reliance on slow and expensive high-throughput physical screening methods and minimizing late-stage failures.

Convolutional Neural Networks (CNNs) are the most critical architecture for diagnostic imaging, including radiology and digital pathology. CNNs excel at automatically learning complex spatial features and patterns within image data, allowing for precise segmentation, classification of diseases (e.g., cancer grading), and automated quantification of pathological findings.

The primary challenges include the "black box" nature of deep learning models (lack of explainability), which hinders clinical trust and regulatory approval; concerns over data privacy and security (GDPR, HIPAA); and the difficulty in obtaining large, standardized, and unbiased training datasets necessary for robust model generalization across diverse patient populations.

Deep Learning facilitates precision medicine by analyzing vast multi-omics datasets (genomics, proteomics, clinical data) to identify patient subgroups, predict individual responses to specific treatments, and discover personalized biomarkers, allowing clinicians to tailor therapeutic strategies for optimal efficacy and minimized adverse effects.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR), driven by significant government investments in modernizing healthcare IT, the enormous and diverse patient data pools available for training models, and a rapid increase in technological adoption across major economies like China, India, and South Korea.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.