ID : MRU_ 438933 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

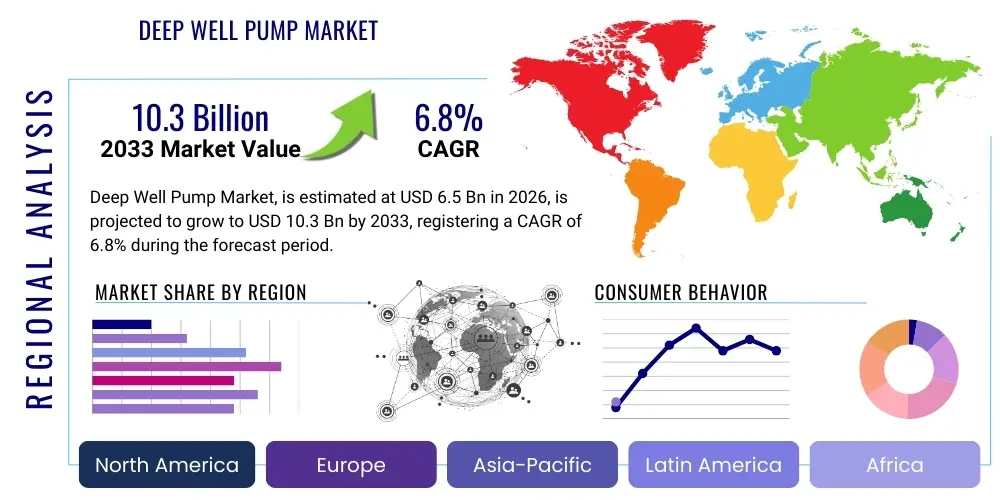

The Deep Well Pump Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 10.3 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global demand for reliable water sources across agricultural, industrial, and municipal sectors, particularly in regions facing acute water stress. Investments in large-scale infrastructure projects, coupled with advancements in submersible and vertical turbine pump technologies, are key factors contributing to this robust market trajectory, ensuring efficient water extraction from deep underground reservoirs to meet increasing consumption needs.

The Deep Well Pump Market encompasses specialized pumping systems designed to lift water or other fluids from significant depths, typically exceeding 50 feet. These pumps are critical components of modern hydrology, engineered for high head and robust operation in diverse environments. Deep well pumps are generally categorized into submersible pumps, which operate fully submerged within the well casing, and vertical turbine pumps, which utilize above-ground motor assemblies. Their core function is to provide reliable, high-pressure fluid transfer necessary for sustaining operations in key sectors globally, ensuring continuity of supply from aquifers and deep boreholes.

Major applications of deep well pumps span across essential economic activities, including large-scale irrigation systems necessary for commercial agriculture, municipal water supply networks, and specialized industrial processes such as mining, oil and gas extraction, and geothermal energy utilization. The primary benefits derived from these sophisticated systems include high energy efficiency, reduced maintenance requirements associated with submerged operation, and unparalleled reliability in delivering consistent flow rates over extended periods. Their robust construction materials, often stainless steel or specialized alloys, ensure longevity even in corrosive or abrasive subterranean environments, making them indispensable for sustainable resource management.

Market growth is predominantly driven by increasing global population density, necessitating expanded municipal water infrastructure, coupled with the critical need for efficient irrigation to bolster food security in developing economies. Furthermore, the accelerating depletion of shallow water tables due to climate change and over-extraction compels users to drill deeper wells, thereby increasing the reliance on high-performance deep well pump systems. Technological driving factors include the integration of Variable Frequency Drives (VFDs) for optimized power consumption and the incorporation of smart monitoring sensors that enhance operational control and predictive maintenance capabilities, significantly improving the Total Cost of Ownership (TCO).

The Deep Well Pump Market is characterized by vigorous business trends focusing on enhancing energy efficiency and integrating advanced monitoring technologies. Key manufacturers are prioritizing the development of pumps compatible with renewable energy sources, notably solar power, to cater to remote agricultural and off-grid municipal installations, particularly prominent in Asia Pacific and Africa. Regional trends show that Asia Pacific dominates the market due to massive investments in agriculture-based water infrastructure and rapid urbanization across nations like China and India, while North America and Europe emphasize replacement cycles utilizing premium, highly efficient pump models adhering to stringent energy standards. Segment trends highlight the increasing prominence of submersible pumps, driven by their operational efficiency and ease of installation in narrow boreholes, and a growing application share in industrial sectors, including sophisticated dewatering processes and mineral extraction, alongside the traditional dominance of agricultural irrigation.

User queries regarding the impact of Artificial Intelligence (AI) on the Deep Well Pump Market primarily revolve around themes of predictive maintenance, optimization of energy usage, and autonomous operation in remote locations. Common concerns address how AI algorithms can analyze vibration data, current draw, and pressure fluctuations in real-time to forecast potential component failures, thereby minimizing costly downtime and extending Mean Time Between Failures (MTBF). Users are also keen on understanding the role of machine learning in adjusting pump speed and operation cycles based on fluctuating water table levels, energy tariffs, and actual demand patterns, moving the industry toward a truly demand-responsive and resource-efficient water extraction model. The consensus expectation is that AI integration will fundamentally shift the industry from reactive servicing to proactive, data-driven asset management, ultimately lowering operational expenditures and improving environmental sustainability.

The Deep Well Pump Market dynamics are fundamentally shaped by a powerful confluence of drivers such as global water scarcity and increasing industrialization, counterbalanced by restraints like high initial investment costs and reliance on consistent electricity supply, while abundant opportunities exist in solar-powered systems and the revitalization of aging municipal infrastructure. These forces, collectively referred to as DRO (Drivers, Restraints, Opportunities), exert significant pressure on market participants, dictating strategic investment areas and product development trajectories. Impact forces derived from these dynamics include the escalating environmental scrutiny on water usage and the rapidly falling costs of renewable energy components, compelling manufacturers to innovate toward more sustainable and cost-effective solutions for deep water extraction.

Drivers: A primary driver is the accelerating decline in global freshwater resources, compelling agricultural and municipal sectors to access deeper aquifers. This is coupled with robust population growth, particularly in emerging economies, demanding massive expansions of urban and rural water supply infrastructure. Furthermore, industrial growth, especially in mining (requiring deep dewatering) and manufacturing (needing high-purity water sources), fuels the demand for high-capacity, durable deep well pumps. Government initiatives aimed at improving irrigation efficiency and ensuring water security also act as significant market catalysts, subsidizing the adoption of modern, high-efficiency pumping equipment.

Restraints: The market faces several critical restraints, notably the relatively high initial capital expenditure required for drilling deep boreholes and procuring specialized submersible equipment, which can deter adoption in smaller agricultural operations. Operational restraints include the susceptibility of pumps to voltage fluctuations and the necessity for robust, reliable electricity access, which remains a challenge in many rural areas. Additionally, the complexity of maintenance for submerged equipment requires specialized labor and tools, contributing to higher servicing costs and potential downtime if not managed efficiently, posing an operational hurdle for end-users.

Opportunities: Significant growth opportunities lie in the proliferation of solar-powered deep well pumping systems, offering a viable, sustainable alternative to grid power in remote locations, massively expanding the market reach, especially in Africa and South Asia. The vast segment of aging municipal water infrastructure in established economies presents a massive replacement and upgrade opportunity, driving demand for modern, smart, and energy-efficient pumping solutions compliant with contemporary environmental standards. Moreover, the integration of Industrial Internet of Things (IIoT) sensors and AI for condition monitoring opens avenues for lucrative service contracts and value-added digital offerings, transforming the business model for key manufacturers.

The Deep Well Pump Market is segmented primarily based on Product Type, Operational Mechanism, Power Rating, and End-User Application. This segmentation allows for a precise understanding of market dynamics specific to different consumer needs, ranging from high-flow municipal water supply systems to low-flow domestic use cases. The dominant segments are Submersible Pumps, favored for their efficiency and reliability in deep settings, and the Agricultural sector, which represents the largest volume consumer globally due to extensive irrigation requirements. Analyzing these segments is crucial for strategic planning, revealing distinct technological requirements and geographical concentrations of demand, guiding product innovation towards high-growth niches such as the solar-powered segment.

Submersible pumps continue to lead the market share due to their superior efficiency, as they require less external priming and eliminate suction lift issues inherent in above-ground systems. Conversely, vertical turbine pumps maintain a specialized but significant share, primarily in large-scale municipal water treatment plants and industrial facilities where high capacity and accessible maintenance are prioritized. Segmentation by power rating is critical, distinguishing between small, single-phase units (used for residential and small farm irrigation) and large, multi-stage, three-phase units essential for municipal and industrial operations, where efficiency standards are stringent and operational demands are continuous. The transition towards more powerful yet compact units demonstrates a key technological advancement across all segments.

Application-based segmentation clearly illustrates the interdependence of market growth with global demographic trends. Agriculture remains the foundational segment, heavily influenced by weather patterns and government subsidies for efficient irrigation. The municipal segment, however, is projected to exhibit the fastest growth, driven by rapid urbanization and the necessity for replacing outdated infrastructure in developed countries, coupled with building new water networks in developing regions. Industrial applications, encompassing mining dewatering, oil and gas field operations, and specific process manufacturing, demand highly customized, ruggedized pump solutions, providing opportunities for high-margin specialized product offerings, driving revenue concentration among major multinational manufacturers.

The value chain for the Deep Well Pump Market is complex, beginning with the upstream supply of specialized raw materials, primarily high-grade stainless steel, cast iron, and specific corrosion-resistant alloys necessary for pump longevity in harsh subterranean environments. Upstream analysis focuses heavily on material sourcing and the manufacturing of precision components like impellers, diffusers, and motor windings, which require specialized fabrication expertise. Suppliers of high-efficiency electric motors and Variable Frequency Drives (VFDs) form another critical upstream component, directly influencing the final product's energy performance rating, a key competitive metric in the downstream market.

Midstream activities involve the core manufacturing, assembly, and rigorous testing of the deep well pump systems. This stage is dominated by major pump companies that invest heavily in research and development to optimize hydraulic efficiency and ensure regulatory compliance (e.g., energy consumption standards). The complexity of integrating sophisticated electronics, such as monitoring sensors and smart controllers, into the mechanical structure necessitates close collaboration between pump manufacturers and technology providers, ensuring seamless interaction between hardware and software components for condition monitoring and predictive maintenance functionalities demanded by modern end-users.

Downstream activities involve distribution, installation, and after-sales servicing. Distribution channels are bifurcated into direct sales for large, customized municipal or industrial projects, and indirect channels relying on an extensive network of specialized dealers, authorized distributors, and water well drilling contractors. These contractors play a vital role, often acting as technical consultants who select and install the appropriate pump system based on borehole specifications and hydrological survey data. After-sales service, including maintenance, repair, and parts supply, is crucial for maintaining customer loyalty and capturing recurring revenue, often managed through certified service centers specializing in submerged equipment retrieval and repair.

The primary consumers and end-users of deep well pumps are diverse, spanning governmental bodies, large private corporations, and millions of individual agricultural producers. Key potential customers include municipal waterworks departments globally, which are responsible for extracting, treating, and distributing potable water to urban populations, necessitating high-volume, reliable pumping stations often utilizing vertical turbine or large submersible pumps. These entities prioritize longevity, energy efficiency, and compliance with strict public health standards, driving demand for premium, highly certified equipment designed for continuous, decades-long operation without failure.

Another major customer segment is the commercial agriculture industry, including large farm holdings, cooperative farms, and governmental irrigation projects. These customers require robust, cost-effective pumps—increasingly solar-powered—capable of handling large volumes of water necessary for field crop irrigation, especially in arid and semi-arid regions. The purchasing decision in this sector is heavily influenced by the pump's power efficiency and reliability during critical peak irrigation seasons, directly impacting crop yields and operational profitability, making VFD integration and low maintenance requirements attractive features.

Furthermore, the industrial sector constitutes a highly lucrative customer base, particularly companies engaged in mining (for dewatering deep pits and tunnels), oil and gas exploration (for managing produced water and water injection), and geothermal energy production. These applications require pumps capable of operating under extreme conditions, including high temperatures, high pressures, and handling chemically aggressive or highly abrasive fluids. Specialized consulting engineers and system integrators often act as intermediaries for these industrial customers, specifying highly customized, engineered-to-order pump solutions that meet stringent safety and environmental regulations specific to their industrial processes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 10.3 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Grundfos, Xylem, KSB Group, Flowserve Corporation, Sulzer, Franklin Electric, Wilo Group, Ebara Corporation, Weir Group, Atlas Copco, SPP Pumps, Ruhrpumpen, Shakti Pumps, LEO Group, Aqua Group, C.R.I. Pumps, Vican Pump, Cornell Pump Company, DWT, Pioneer Pump. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Deep Well Pump Market's technological landscape is rapidly evolving, driven by the imperative for enhanced energy efficiency, durability, and integration with smart digital controls. A cornerstone technology is the widespread adoption of High-Efficiency Motor Standards (such as IE3 and IE4), coupled with advanced hydraulic designs that minimize friction losses within the impellers and diffusers. Furthermore, the integration of Variable Frequency Drives (VFDs) is crucial; VFDs allow the pump motor speed to be precisely adjusted to match the flow requirements, dramatically reducing energy consumption compared to fixed-speed operation, especially in municipal and irrigation applications characterized by fluctuating demand and variable water levels.

Material science innovation also plays a critical role, particularly the development and application of corrosion-resistant and abrasion-resistant materials, such as specialized stainless steels, ceramic coatings, and engineered plastics for internal components. These advancements are essential for extending the operational lifespan of pumps in challenging environments, such as wells containing high mineral content, sand, or corrosive chemicals found in industrial wastewater or geothermal brine. The refinement of sealing technologies, including advanced mechanical seals and stuffing boxes, contributes significantly to reducing maintenance requirements and preventing costly water ingress into the motor housing, a common cause of pump failure in deep installations.

The increasing prominence of the Industrial Internet of Things (IIoT) represents the most impactful technological shift. Modern deep well pumps are frequently equipped with integrated sensors (pressure transducers, temperature probes, vibration monitors) that transmit real-time operational data wirelessly to cloud-based monitoring platforms. This enables sophisticated remote diagnostics, performance benchmarking, and, crucially, the implementation of condition-based monitoring programs. These systems utilize data analytics, sometimes powered by AI, to predict maintenance needs weeks or months in advance, minimizing unscheduled downtime and optimizing the overall efficiency of large-scale water extraction networks, enhancing resource security and operational reliability across all end-user segments.

Market growth is predominantly driven by increasing global water scarcity, compelling reliance on deeper aquifers, coupled with rapid urbanization and the necessity to expand municipal water supply infrastructure globally. Furthermore, the escalating demand for efficient agricultural irrigation systems and stringent energy efficiency regulations contribute significantly to the adoption of advanced pumping technologies.

Solar-powered pumps are crucial market disruptors, providing a sustainable, cost-effective, and grid-independent solution for water access in remote agricultural and rural municipal areas. This technology significantly reduces long-term operational costs associated with electricity or diesel, accelerating market penetration in regions like Africa and South Asia where reliable power infrastructure is often lacking.

Submersible pumps have the motor and the pump housing entirely submerged in the well fluid, offering high efficiency and quiet operation, suitable for narrow boreholes. Vertical turbine pumps utilize a motor mounted above ground, driving the submerged pump bowls via a long shaft, which simplifies motor maintenance and is typically preferred for high-flow, large-capacity municipal or industrial applications.

The Agriculture segment holds the largest volume share due to the massive global requirement for irrigation to support crop production and food security. However, the Municipal water supply segment is projected to show the fastest growth rate, driven by essential infrastructure replacement projects in mature economies and network expansion in developing urban centers.

IIoT sensors and AI algorithms enable real-time condition monitoring, remote performance optimization, and crucial predictive maintenance capabilities. This digital integration maximizes operational uptime, reduces energy consumption through precise VFD control, and drastically lowers the Total Cost of Ownership by anticipating and preventing component failures before they occur.

Material selection, particularly the use of specialized stainless steel, high-grade cast iron, and engineered ceramics, is vital for resisting corrosion and abrasion caused by aggressive subterranean water compositions (high sand, high mineral content, or chemical brine). Using appropriate, durable materials ensures extended Mean Time Between Failures (MTBF) and robust operation over the system's intended lifecycle.

In mature markets like North America and Europe, stringent energy efficiency standards, such as minimum efficiency indices for motors and hydraulic performance mandates (e.g., DOE standards in the U.S.), heavily influence product development. Compliance with these regulations drives manufacturers to invest in highly efficient motors (IE3/IE4) and superior hydraulic designs to minimize energy usage and meet environmental sustainability targets.

The replacement market is extremely significant, especially in developed regions where existing municipal and older industrial infrastructure is reaching the end of its service life (20-30 years). The need to replace aging, inefficient pumps with modern, smart, and energy-compliant models represents a large and continuous revenue stream for market players, driving demand for modern retrofit solutions.

High head capability refers to the pump's ability to lift fluid vertically against significant gravitational pressure and system friction losses over long distances or depths. Deep well pumps are specifically engineered with multiple impellers (stages) to generate the high pressure necessary to overcome the substantial static head presented by deep boreholes, ensuring adequate flow is delivered to the surface or distribution point.

The primary challenge is the requirement for specialized equipment (cranes, specific retrieval rigs) and skilled personnel to pull the entire pump and motor assembly out of the well for diagnosis or repair, which is inherently time-consuming and expensive. This difficulty strongly reinforces the market trend toward highly reliable, low-maintenance designs and remote monitoring systems to minimize the frequency of required retrievals.

The Asia Pacific (APAC) region currently leads the market consumption by volume and value, predominantly driven by massive infrastructure expansion projects in major economies like China and India, coupled with extensive, necessity-driven demand from the agricultural sector for irrigation pumping solutions across the subcontinent.

Variable Frequency Drives (VFDs) are electronic devices that control the speed of the electric motor by varying the frequency and voltage of the electrical supply. They are critical because they allow the pump's output to precisely match the fluid demand, preventing unnecessary energy wastage associated with running the pump at a fixed, maximum speed, thereby optimizing energy efficiency dramatically, especially in variable-load systems.

The mining industry utilizes deep well pump technology primarily for dewatering—removing large volumes of groundwater from deep underground pits, shafts, and tunnels to facilitate safe extraction operations. These applications demand extremely robust, high-capacity, and often abrasion-resistant vertical turbine or heavy-duty submersible pumps designed to handle harsh, sediment-laden water.

Key restraint factors include the high initial capital investment required for drilling and purchasing the specialized, high-capacity pumping systems. Additionally, the operational reliance on a stable and continuous electricity supply, particularly challenging in rural or remote global regions, acts as a significant impediment to widespread adoption without concurrent investment in alternative power sources like solar PV.

The market is primarily segmented by Type into Submersible Pumps and Vertical Turbine Pumps. Submersible pumps are the dominant segment due to their efficiency and ease of installation in deep wells, while Vertical Turbine Pumps are preferred for large flow rates and surface-accessible motor maintenance in municipal and large industrial setups.

Emerging opportunities are concentrated in the provision of comprehensive service contracts centered around IIoT integration, offering customers data-driven maintenance and performance optimization services. Furthermore, expanding the manufacturing base and distribution network for solar-powered pump accessories and complete off-grid solutions represents a major growth opportunity, particularly in high-sunshine developing regions.

Drilling contractors are critical because they often act as the primary interface with the end-user, providing technical consultation on well depth, casing size, and hydrological data. Their expertise is essential for correctly sizing and installing the appropriate deep well pump system, influencing brand loyalty and ensuring successful system operation, thereby integrating sales and service functions.

Climate change exacerbates droughts and increases reliance on irrigation, simultaneously causing the depletion of shallow groundwater tables. This necessitates drilling deeper wells to access sustainable water sources, directly increasing the global demand for high-performance, multi-stage deep well pumps capable of operating reliably at greater depths and higher heads.

Under optimal operating conditions, utilizing high-quality materials and benefiting from efficient motor and VFD controls, a deep well pump system can typically have a service life ranging from 15 to 25 years. This longevity, however, is significantly dependent on the abrasive nature of the pumped fluid, the stability of the power supply, and adherence to regular, proactive maintenance schedules.

The most significant industrial consumers include the mining industry for dewatering purposes, the oil and gas sector for water management (injection and produced water handling), and power generation plants, particularly those utilizing geothermal energy which requires highly specialized, heat- and corrosion-resistant pumping systems for brine circulation.

Geothermal applications involve pumping extremely hot, often chemically aggressive brine containing high concentrations of corrosive salts and minerals. Corrosion-resistant alloys (such as specialized stainless steels or Hastelloy) are mandatory to prevent rapid material degradation, maintain hydraulic integrity, and ensure the operational safety and lifespan of the pumping equipment under these severe temperature and chemical stresses.

Government policies that accelerate adoption include subsidies for agricultural pumping equipment, particularly solar PV systems, along with large-scale public investment programs aimed at expanding rural and urban potable water access (e.g., national water security missions). These policies often incentivize the purchase of highly efficient, certified pump models, aligning resource management with economic development goals.

Advancements in hydraulic design involve optimizing the shape and geometry of impellers, diffusers, and casing components using Computational Fluid Dynamics (CFD) modeling. This optimization minimizes internal friction and turbulence within the pump stages, maximizing the conversion of electrical energy into useful kinetic energy and pressure head, thereby significantly reducing the overall specific energy consumption (SEC) of the unit.

The Latin American market outlook is moderately positive, driven primarily by the sustained demand from large commercial agricultural enterprises (like soybean and sugar cane production) and continued, though often fluctuating, investment in the high-demand mining sector. Future growth hinges on stabilizing regional economies and increasing public spending on water infrastructure modernization.

The precise measurement of the dynamic water table level is critical because it dictates the total head the pump must overcome and prevents the pump from running dry (drawdown), which can cause catastrophic damage to the unit. Continuous monitoring allows VFD systems and smart controls to optimize pump speed dynamically, maximizing efficiency while protecting the equipment from adverse operating conditions.

The Municipal Water Supply and large-scale Industrial segments (such as mining and utilities) are most likely to rapidly adopt AI and IIoT. These sectors have high operational expenditures, large asset bases, and critical needs for uninterrupted supply, making the investment in predictive maintenance and remote operational optimization highly cost-effective and strategically necessary for risk mitigation.

Specific Energy Consumption (SEC) is a critical efficiency metric defined as the amount of energy (in kilowatt-hours, kWh) required to pump a unit volume of water (typically cubic meter or thousand gallons). Lower SEC values indicate higher energy efficiency, which is a key performance indicator favored by municipal authorities and large commercial users seeking to minimize long-term operational costs.

Manufacturers who achieve vertical integration—controlling the production of critical components like motors, VFDs, and hydraulic parts—gain significant competitive advantages. These advantages include tighter quality control over the entire system, reduced reliance on external suppliers, faster time-to-market for new technologies, and ultimately, better control over manufacturing costs and pricing strategies across diverse product lines.

The push for sustainable practices necessitates the design of pumps with superior energy efficiency (minimizing carbon footprint) and the use of environmentally safe, often recyclable, materials. This includes prioritizing non-leaching, corrosion-resistant internal components and engineering pumps optimized for integration with renewable energy sources like solar power, reducing dependence on fossil fuel-derived electricity.

Future advancements are expected to focus heavily on greater autonomy and digitalization, including self-diagnosing pumps that automatically adjust for wear, advanced non-metallic materials (composites) for enhanced durability, and improved battery storage solutions integrated with solar systems, allowing 24/7 operation in remote locations without grid connectivity challenges.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.