ID : MRU_ 435090 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

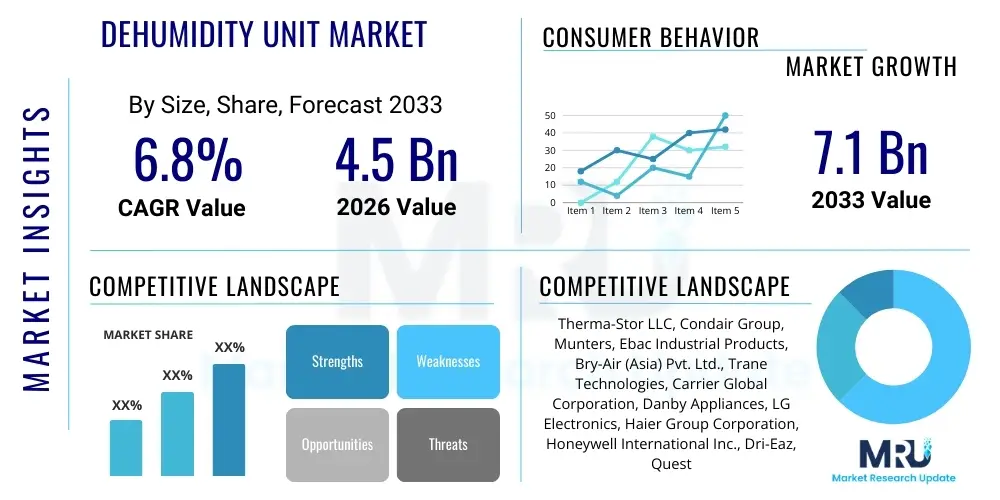

The Dehumidity Unit Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.1 Billion by the end of the forecast period in 2033.

The Dehumidity Unit Market encompasses the manufacturing, distribution, and utilization of systems designed to reduce and maintain specified humidity levels in indoor environments. These units operate on various principles, primarily refrigerant-based cooling and desiccant drying technologies, tailored for diverse applications ranging from residential comfort to stringent industrial process control. Dehumidity units are critical not only for mitigating mold, mildew, and structural damage but also for optimizing manufacturing processes in sectors like pharmaceuticals, food processing, and electronics assembly, where ambient moisture control is paramount to product quality and safety. The increasing awareness regarding the health implications of poor indoor air quality (IAQ), specifically high humidity leading to allergen proliferation, substantially fuels consumer demand across developed economies.

The primary product categories within this market include portable, whole-house, and industrial-grade dehumidifiers, each distinguished by capacity, operational efficiency, and installation complexity. Major applications span residential dwellings, commercial spaces such as hotels and archives, and highly regulated industrial environments including chemical plants and cleanrooms. Beyond comfort, these systems provide essential benefits such as preventing equipment corrosion, stabilizing sensitive material storage, and improving the operational efficiency of interconnected HVAC systems. Effective humidity management translates directly into lower maintenance costs and extended lifespan for building infrastructure and contents, positioning dehumidification as a critical element of modern building management systems.

Key driving factors accelerating market expansion include rapid urbanization across Asia Pacific, leading to increased construction of densely populated residential and commercial buildings requiring robust IAQ solutions. Furthermore, climate change resulting in more frequent and intense humidity extremes necessitates reliable mechanical dehumidification solutions. Regulatory frameworks, particularly those focusing on energy efficiency and environmental standards for refrigerants, are compelling manufacturers to innovate, developing advanced models with integrated smart sensors, IoT connectivity, and environmentally friendly cooling agents. This technological shift is crucial for meeting stringent governmental mandates while simultaneously catering to consumer preference for automated, energy-efficient home and commercial solutions.

The global Dehumidity Unit Market is characterized by robust growth, driven primarily by escalating concerns over indoor air quality (IAQ) and the functional necessity of moisture control in high-value industrial processes. Current business trends indicate a definitive shift toward smart, connected dehumidifiers equipped with Wi-Fi and integrated sensors, allowing for remote monitoring and proactive humidity adjustments, thereby enhancing energy efficiency and user convenience. Manufacturers are heavily investing in inverter technology and heat pump dehumidifiers to comply with evolving energy efficiency standards, particularly in North America and Europe. The competitive landscape is consolidating, with major players focusing on strategic mergers, acquisitions, and developing specialized industrial units capable of handling extreme moisture loads, alongside expanding their consumer-grade portable unit portfolios to capture the rapidly growing residential segment.

Regionally, the Asia Pacific (APAC) stands out as the highest growth potential region, propelled by massive infrastructural development, increasing disposable income, and the inherent high humidity in coastal and tropical zones across countries like China, India, and Southeast Asian nations. North America remains a significant market, driven by stringent building codes related to ventilation and moisture mitigation, particularly in basements and crawl spaces, while Europe focuses on adopting highly energy-efficient desiccant dehumidification systems due to strict environmental policies regarding fluorinated gases. The challenge remains in managing the supply chain volatility and the transition away from high Global Warming Potential (GWP) refrigerants, which requires significant capital expenditure in R&D and manufacturing restructuring.

Segmentation trends highlight the increasing preference for whole-house dehumidification systems over portable units, especially in new construction and major renovation projects, owing to their superior efficiency and integration capabilities within central HVAC systems. Technology-wise, desiccant dehumidifiers are gaining traction in industrial applications and low-temperature environments where refrigerant-based units struggle with efficiency, such as cold storage and pharmaceutical drying processes. The industrial sector, particularly in precision manufacturing and data centers, represents the most lucrative segment, demanding high-capacity, highly durable, and precisely controllable dehumidification solutions that can operate continuously under challenging conditions, thus ensuring market stability and driving innovation in material science and system design.

User inquiries regarding the integration of Artificial Intelligence (AI) into the dehumidification market predominantly revolve around three critical areas: predictive maintenance, energy consumption optimization, and seamless integration into holistic smart building management systems. Users frequently ask, "How can AI predict dehumidifier failures before they occur?" and "Will AI reduce the operational energy cost of high-capacity industrial units?" These questions reflect a core expectation that AI should move dehumidification beyond reactive operation to proactive, data-driven management. Concerns also include data security associated with cloud-connected devices and the perceived complexity and initial investment required for implementing AI-enabled features in existing HVAC infrastructure.

The key themes emerging from this analysis confirm that end-users view AI not merely as an add-on but as an essential transformation tool for efficiency. Specifically, AI algorithms analyze historical humidity data, real-time energy prices, local weather forecasts, and occupancy patterns to modulate the dehumidifier's duty cycle. This results in significant energy savings by preventing unnecessary operation and ensuring optimal relative humidity (RH) levels are maintained with minimal energy expenditure. For large industrial users, AI-powered diagnostics can detect subtle changes in motor vibrations, refrigerant pressures, or filter performance, flagging potential issues months in advance and drastically reducing downtime, which is highly valuable in continuous process industries.

Furthermore, AI facilitates advanced integration through protocols such as BACnet and Modbus, allowing dehumidifiers to communicate intelligently with other building systems, including ventilation fans and heating elements. This interoperability ensures that humidity control is coordinated, avoiding conflicting operations that waste energy. Expectations are high for future generations of units to self-calibrate based on learning algorithms, optimizing performance specific to the structure and climate zone they operate within, making installation and commissioning simpler and providing superior long-term return on investment (ROI). However, manufacturers must address the cost barrier and ensure the user interface for these advanced features remains intuitive and accessible to non-technical users.

The market trajectory for dehumidification units is shaped by a powerful confluence of drivers, constraints, and opportunities, all interacting to define investment priorities and technological developments. Primary drivers stem from heightened public awareness regarding the direct correlation between high indoor humidity and significant health issues, including asthma and allergies, coupled with the substantial economic impact of moisture damage on building materials and sensitive industrial goods. Simultaneously, increasing frequency of extreme weather events, particularly heavy rainfall and heat waves linked to global climate change, accelerates the need for robust, high-capacity moisture management solutions in diverse geographic regions. Regulatory standards mandating specific humidity control in critical facilities, such as data centers and pharmaceutical cleanrooms, further solidify demand, acting as a non-discretionary driver for industrial adoption.

However, the market faces notable restraints, most prominently the relatively high initial acquisition cost of advanced, energy-efficient dehumidifiers, particularly whole-house and high-capacity industrial units, which can deter residential consumers and small businesses. Consumer perception of high long-term operational energy consumption, despite technological advancements in efficiency (such as Energy Star ratings and inverter technology), also acts as a barrier. Furthermore, the reliance on chemical refrigerants in traditional compression dehumidifiers subjects the market to volatile regulatory changes, such as the mandated phasedown of HFCs under global environmental agreements, necessitating expensive R&D and manufacturing facility overhauls to adopt lower GWP alternatives, thereby increasing production costs temporarily.

Opportunities for growth are concentrated in the rapid expansion of smart home technology and the integration of dehumidifiers as standard components of interconnected HVAC ecosystems, providing manufacturers with premium pricing potential for smart-enabled units. Emerging markets, especially in Southeast Asia and Latin America, present vast untapped potential as economic development leads to increased investment in quality residential construction and modernizing industrial facilities. The greatest opportunity lies in the development of hybrid systems—combining desiccant wheels with vapor compression technology—to offer unparalleled efficiency across a wider temperature range, appealing specifically to sectors requiring precise climate control, such as museums, archives, and high-tech manufacturing processes, thereby capitalizing on specialized, high-margin niche applications.

The Dehumidity Unit Market is comprehensively segmented based on technology, capacity, application, and distribution channel, providing a granular view of market dynamics and consumer preferences across different operational environments. Understanding these segments is crucial for strategic planning, allowing manufacturers to tailor product development and marketing efforts towards specific end-user needs. The market demonstrates significant divergence in requirements between residential users, who prioritize compactness and aesthetic integration, and industrial users, who demand reliability, precise control, and high throughput capacity, driving a dual focus on consumer convenience and industrial robustness.

The value chain for the Dehumidity Unit Market begins with raw material sourcing (metals, plastics, refrigerants, and electronic components), followed by intricate manufacturing and assembly processes, and concludes with distribution, installation, and after-sales service. The upstream segment involves suppliers of critical components such as compressors, heat exchangers (coils), specialized polymers for casings, and advanced controllers. The efficiency and reliability of these suppliers directly influence the final product quality and manufacturing cost. Companies in the midstream focus on design, incorporating features like inverter technology, smart sensors, and environmentally friendly refrigerants, requiring significant investment in specialized assembly lines and quality control protocols to ensure compliance with global safety and efficiency standards.

The downstream segment, encompassing distribution and sales, is highly diversified. Direct distribution (B2B) channels are vital for industrial and large commercial dehumidifiers, where technical consultation, customized installation, and long-term service contracts are prerequisites. These direct sales efforts rely heavily on specialized engineering firms and certified HVAC contractors. Conversely, the residential and small commercial sectors rely heavily on indirect distribution through online retail platforms, big-box stores, and specialty appliance retailers. The growing popularity of e-commerce has mandated strong digital marketing strategies and robust logistics capabilities to handle bulky product delivery and returns, profoundly changing the market landscape.

A crucial element of the downstream value chain is the provision of aftermarket services, including maintenance, repair, and filter replacement. Given the complexity of modern HVAC-integrated units and the critical nature of industrial dehumidification, specialized maintenance services are a high-margin business segment. Optimization of the value chain involves securing stable supplies of low-GWP refrigerants and microprocessors, streamlining manufacturing processes through automation to maintain cost competitiveness, and leveraging digital platforms to offer superior customer service and remote diagnostic capabilities. Strong partnerships between manufacturers and certified installation experts are essential for maintaining product performance and user satisfaction, particularly for whole-house and central systems.

The potential customer base for dehumidification units is extensive and segmented into three main categories: residential, commercial, and industrial, each possessing distinct capacity and precision requirements. Residential customers represent the largest volume segment, motivated primarily by health concerns (allergen and mold reduction), comfort, and the protection of household items and structures (e.g., basement dehumidification). This demographic increasingly seeks portable, user-friendly, and smart-enabled units that integrate easily into existing home automation ecosystems, often purchasing through indirect retail channels.

Commercial potential customers include a wide array of entities such as large office complexes, hotels, hospitals, museums, and data centers. These organizations require units that offer continuous operation, high capacity, energy efficiency, and low noise levels. Hospitals and museums, for instance, mandate extremely precise humidity control to preserve sensitive medical equipment, archival documents, or artwork. Data centers represent a crucial growth area, as excessive moisture can lead to catastrophic equipment failure, demanding industrial-grade, often customized, desiccant or refrigerant-based solutions integrated directly into the facility's complex climate control infrastructure.

The industrial sector represents the highest value per unit segment, serving critical manufacturing and storage applications. Key industrial end-users include pharmaceutical manufacturers (where moisture control is essential for tablet compression and coating), food and beverage processing plants (preventing bacterial growth and ensuring product integrity), chemical manufacturing, and specialized sectors like lithium-ion battery production where stringent dry room conditions are mandatory. These industrial buyers prioritize robust construction, specialized materials resistant to corrosive environments, exceptional reliability, and compliance with severe regulatory standards, typically procuring units directly from manufacturers or specialized engineering procurement contractors.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.1 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Therma-Stor LLC, Condair Group, Munters, Ebac Industrial Products, Bry-Air (Asia) Pvt. Ltd., Trane Technologies, Carrier Global Corporation, Danby Appliances, LG Electronics, Haier Group Corporation, Honeywell International Inc., Dri-Eaz, Quest Dehumidifiers, De'Longhi S.p.A., Sunpentown International Inc., General Filters, Inc., Aprilaire, Santa Fe Dehumidifiers, Pu'er Electric Appliance Co., Ltd., Hangzhou Gree Electric Appliances, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Dehumidity Unit Market is dominated by two core operational methods: refrigerant-based (compressor) dehumidifiers and desiccant dehumidifiers, with innovation focusing heavily on improving energy efficiency, miniaturization, and smart connectivity. Refrigerant dehumidifiers, which work by cooling air below its dew point to condense moisture, are undergoing transformation through the adoption of variable-speed inverter technology. Inverter technology allows the compressor speed to be modulated precisely according to the moisture load, significantly reducing power consumption and noise levels compared to traditional single-speed compressors, making them highly desirable for residential and light commercial use. Furthermore, the mandatory transition to low Global Warming Potential (GWP) refrigerants, such as R-454B and R-32, is driving substantial investment in redesigning heat exchangers and compressors across the industry to maintain or improve performance metrics under new regulatory constraints.

Desiccant dehumidifiers, which use adsorbent materials (like silica gel or lithium chloride) to remove moisture chemically, are crucial for industrial applications, particularly those operating in low-temperature or extremely dry environments (e.g., -40°C dew point). Technological advancements in this segment center around optimizing the desiccant wheel material and regeneration process. Manufacturers are developing composite desiccant wheels with enhanced absorption capacities and lower regeneration temperatures, which dramatically reduces the energy input required for the thermal reactivation cycle. This improvement is expanding their economic viability into new segments, including large-scale commercial storage facilities and specialized pharmaceutical drying rooms, where traditional cooling-based methods are inefficient or impractical due to temperature constraints.

The emerging technological focus is on integration and intelligence. Hybrid dehumidification systems that strategically combine the strengths of desiccant and refrigerant technologies are gaining prominence, offering superior performance across varying conditions. Moreover, the incorporation of advanced sensors (humidity, temperature, volatile organic compounds—VOCs) and IoT platforms is standardizing the concept of the 'smart dehumidifier.' These connected units leverage cloud computing and machine learning (AI analysis) to predict humidity spikes, optimize cycling based on external data, and provide proactive alerts and detailed performance reports to facility managers, thus ensuring peak operational efficiency and minimizing energy waste across both residential and highly sensitive industrial installations.

Refrigerant (compressor) dehumidifiers work by cooling air to condense moisture, offering high efficiency in warm, highly humid conditions (above 65°F). Desiccant dehumidifiers utilize chemical adsorption materials (like silica gel) to remove moisture and perform optimally in low-temperature or extremely low-humidity environments (e.g., cold storage or specialized industrial drying), requiring thermal energy for regeneration rather than just cooling.

The market is actively transitioning away from high Global Warming Potential (GWP) hydrofluorocarbons (HFCs) like R-410A. Manufacturers are redesigning units to utilize lower GWP refrigerants such as R-32 or R-454B, aligning with international mandates like the Kigali Amendment. Furthermore, there is increased adoption of highly efficient desiccant systems and inverter technologies to reduce overall energy consumption, mitigating environmental impact.

IoT and smart technology enable remote monitoring, predictive maintenance, and energy optimization. Connected units utilize sensors to automatically adjust operation based on real-time humidity, external weather data, and energy costs. This integration allows for superior energy efficiency, proactive fault detection, and seamless control within comprehensive smart building management systems (BMS), driving premium segment growth.

The Industrial segment, particularly high-precision manufacturing (e.g., lithium-ion batteries, advanced electronics, and pharmaceuticals), is expected to exhibit the highest value growth. These sectors require extremely stringent and consistent humidity control, demanding customized, high-capacity, and highly reliable desiccant systems, offering strong margins and consistent demand driven by global supply chain needs.

The global Dehumidity Unit Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period of 2026 to 2033. This growth is underpinned by rising global average humidity levels, increased health consciousness, and accelerated industrial investment in moisture-sensitive processes worldwide.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.