ID : MRU_ 435287 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

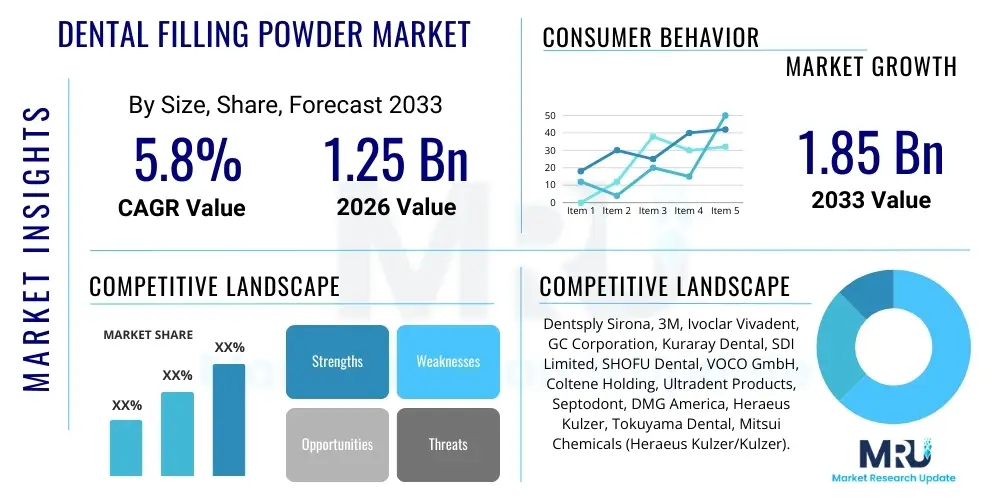

The Dental Filling Powder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 1.85 Billion by the end of the forecast period in 2033.

The Dental Filling Powder Market encompasses materials essential for restorative dentistry, primarily used to treat carious lesions, fractures, and structural defects in teeth. These powders, which form the matrix of dental restorations when mixed with a liquid component, include various advanced formulations such as glass ionomer cements (GIC), resin-based composites, and ceramic-based materials. The shift away from traditional amalgam fillings due to environmental and health concerns has significantly accelerated the adoption of aesthetic, biocompatible, and high-performance powder formulations, driving innovation across the industry. Dental filling powders are crucial for maintaining oral health and providing aesthetic rehabilitation, serving as the cornerstone for direct restorative procedures performed globally.

Major applications of dental filling powders span general restorative dentistry, cosmetic procedures, and minor prosthetic applications. They are indispensable in dental clinics and hospitals for treatments ranging from simple pit and fissure sealing to complex anterior and posterior restorations. The demand for these products is intrinsically linked to the rising global prevalence of dental caries, aging populations requiring extensive dental care, and increasing patient awareness regarding aesthetic dental solutions. The evolution of powder technology focuses on enhancing characteristics such as strength, wear resistance, dimensional stability, and fluoride release capabilities, particularly for materials like GICs which offer therapeutic benefits.

Key driving factors supporting market expansion include continuous advancements in material science, leading to the development of nanofilled composites and bio-active glass materials that mimic natural tooth structure more effectively. Furthermore, increasing dental tourism in developing economies, coupled with growing government investment in oral health infrastructure, provides substantial market momentum. The transition towards minimally invasive dentistry also favors high-quality, flowable, and easily manipulated powder-based systems. Regulatory bodies are increasingly scrutinizing the safety and efficacy of these materials, pushing manufacturers toward superior quality assurance and research into next-generation restorative solutions that promise longevity and minimal post-operative sensitivity.

The global Dental Filling Powder Market is characterized by robust growth, primarily driven by demographic trends such as a rising geriatric population and increasing disposable income leading to higher demand for elective cosmetic dental procedures. Business trends indicate a strong move toward consolidation among major players who are aggressively investing in R&D to launch advanced formulations, particularly in the realm of nanohybrid composites and smart biomaterials capable of active tissue integration. Strategic alliances, mergers, and acquisitions focused on expanding geographical reach, particularly into the high-growth Asia Pacific region, and acquiring specialized material technologies are defining the competitive landscape. Furthermore, heightened focus on supply chain resilience and localized manufacturing is becoming a key differentiator, helping companies navigate geopolitical and logistical challenges and maintain competitive pricing structures.

Regionally, North America and Europe maintain leading positions, primarily due to established healthcare infrastructure, high awareness levels, and rapid adoption of premium, advanced restorative materials. However, the Asia Pacific (APAC) region is poised to exhibit the highest CAGR during the forecast period, fueled by massive untapped populations, expanding dental clinic networks in countries like China and India, and increasing penetration of dental insurance schemes. Regulatory harmonization efforts, particularly within the EU (MDR framework), are influencing product innovation timelines and market entry strategies. Latin America and the Middle East & Africa (MEA) present nascent opportunities, driven by increasing healthcare expenditure and focused initiatives by international organizations to improve access to basic dental care, which favors cost-effective, durable filling materials.

Segment trends reveal that the Resin-based Composites segment dominates the market in terms of value, owing to their superior aesthetics and versatility in various clinical situations. Within composites, bulk-fill technologies, which simplify posterior restorations, are experiencing rapid uptake. Conversely, the Glass Ionomer Cements (GIC) segment is witnessing significant growth in volume, propelled by their utility in pediatric dentistry, temporary restorations, and preventative applications, largely due to their fluoride-releasing properties. End-user analysis shows that independent dental clinics remain the largest consumers, though the consolidation of practices into large dental service organizations (DSOs) is altering purchasing dynamics, favoring bulk contracts and comprehensive supply agreements for powder formulations.

User inquiries regarding the intersection of Artificial Intelligence (AI) and the Dental Filling Powder Market typically center on how AI can optimize material formulation, predict clinical performance, and improve the efficiency of restorative procedures. Users are keenly interested in whether AI algorithms can be used to analyze vast datasets of material properties and patient outcomes to design superior, personalized filling powders with enhanced longevity and reduced failure rates. Key concerns revolve around the ethical implications of using AI in material selection, the required investment in infrastructure for AI-driven manufacturing, and the potential for AI to standardize procedures, thereby influencing the optimal stock levels and required inventory of specific powder types at the clinic level. Expectations include AI-powered diagnostics that precisely determine the required material volume and characteristics for individual patient needs, minimizing material waste and ensuring procedural precision, ultimately impacting demand for specific, high-specification dental filling powders.

The dynamics of the Dental Filling Powder Market are defined by a complex interplay of Drivers, Restraints, and Opportunities, which collectively determine the overall Impact Forces. The primary drivers include the global increase in dental disease burden, particularly caries, the escalating preference for aesthetic dental procedures over traditional metallic restorations, and substantial technological leaps in material science, offering biocompatible and durable solutions. These drivers exert a continuous upward pressure on market demand, necessitating high-volume production and consistent innovation in powder formulations. Simultaneously, the market faces significant restraints, such as the high cost associated with advanced restorative materials, which limits adoption in low-income settings, and stringent regulatory approval processes that increase the time-to-market for novel powder technologies. The lingering presence of amalgam in specific low-cost markets also slightly constrains the universal adoption of composite and GIC powders, though this resistance is steadily diminishing.

Opportunities within the market are predominantly concentrated in the emergence of bio-active and regenerative dental materials that actively interact with the tooth structure to promote healing, such as specialized GICs and calcium silicate-based powders. The massive, untapped potential in emerging economies, driven by expanding middle classes and government initiatives focused on preventative care, represents a crucial avenue for growth and market penetration. Furthermore, the increasing acceptance of teledentistry and digital workflow integration is streamlining the demand process and enabling manufacturers to offer more customized and precise filling solutions, opening avenues for high-value product differentiation and service integration. These opportunities suggest a path toward specialized, premium, and geographically diverse market growth.

The impact forces are substantial, pushing the market toward non-metallic, aesthetically superior solutions. The substitution effect is strong, with modern composites and GICs rapidly displacing older materials. Furthermore, the competitive intensity remains high, compelling manufacturers to invest heavily in intellectual property and clinical validation to establish market trust and justify premium pricing. The societal impact of aesthetic concerns globally has created a powerful market pull force, making tooth-colored restorations the standard of care. Environmental regulations regarding material disposal and biocompatibility further reinforce the direction of innovation, favoring environmentally benign and patient-safe powder formulations, solidifying the trend toward highly specified, advanced material science solutions.

The Dental Filling Powder Market is meticulously segmented based on Material Type, Application, and End-User, reflecting the diverse clinical requirements and preferences across the dental industry. Segmentation by material type is crucial as it dictates the mechanical properties, aesthetic outcomes, and cost structure of the restoration. Resin-based composites, which are polymerized using light, currently hold the largest market share due to their superior aesthetics and adaptability. However, the segmentation also highlights the steady growth in Glass Ionomer Cements (GIC) and their variations, especially in pediatric and geriatric care, due to their unique ability to release fluoride and chemically bond to the tooth structure, positioning them as essential therapeutic materials alongside conventional restorations.

Application-based segmentation divides the market into Restorative Dentistry, Prosthetic Dentistry, and Cosmetic Dentistry, illustrating where the bulk of the demand originates. Restorative dentistry, encompassing the repair of carious and damaged teeth, represents the core application sector, driven by basic oral healthcare needs globally. Cosmetic dentistry, focusing on aesthetic enhancement, utilizes premium, highly aesthetic powder formulations and is strongly influenced by patient disposable income and media exposure. End-user segmentation reveals the dominance of independent dental clinics, yet acknowledges the growing influence of specialized dental hospitals and educational institutions that drive both high-volume consumption and the adoption of cutting-edge, experimental powder technologies.

The value chain for the Dental Filling Powder Market begins with upstream activities, focusing heavily on the sourcing and refinement of specialized raw materials. This includes high-purity glass fillers (silica, barium glass), specialized monomers (for resin composites), and unique metallic salts or acids (for GICs). Suppliers in the chemical and materials science industries play a critical role, as the quality and consistency of these inputs directly determine the final performance characteristics of the dental powder, such as polymerization shrinkage, wear resistance, and radiopacity. Significant investment is placed in intellectual property surrounding the filler technology and coupling agents, which are essential for creating the fine, highly controlled particle sizes necessary for modern aesthetic and strong restorative materials.

Midstream activities involve the complex manufacturing and formulation processes where raw materials are precisely mixed, milled, and packaged. This phase requires rigorous quality control and specialized industrial equipment to maintain sterile conditions and particle uniformity. Manufacturers engage in R&D to develop proprietary mixing ratios and chemical stabilizers that enhance shelf life and clinical handling characteristics. Downstream activities involve distribution channels, encompassing both direct sales forces targeting large Dental Service Organizations (DSOs) and indirect distribution through specialized medical and dental product distributors. The distribution channel is critical, as filling powders require specific storage conditions and timely delivery to maintain efficacy, particularly in geographically widespread markets.

Direct distribution, utilized often by market leaders, allows for closer relationships with key opinion leaders, hospitals, and major dental chains, facilitating faster product adoption and personalized training. Indirect distribution relies on an established network of regional dealers who manage smaller clinics and remote geographical areas, providing necessary market penetration and local logistical support. The selection of the channel is often guided by the product type; highly specialized, premium powders are often sold directly, while standard GICs or bulk-fill composites might utilize extensive indirect networks. Effective channel management, including training distributors on product handling and clinical benefits, is paramount for ensuring market reach and maximizing sales volume in this highly professionalized sector.

The primary customers and end-users of dental filling powders are professional healthcare providers within the oral care domain, encompassing a broad range of clinical settings focused on restorative and preventative treatments. General dentists constitute the largest buyer segment globally, utilizing filling powders for routine procedures such as cavity restorations and minor repairs. Their purchasing decisions are driven by factors including ease of use, handling properties, cost-effectiveness, and the clinical longevity of the material. The increasing demand for aesthetic outcomes means that general practitioners are progressively shifting their preference toward high-quality resin-based composites and advanced GIC formulations that require specialized training and consistent supply.

Specialized dental practitioners, such as orthodontists, prosthodontists, and pediatric dentists, represent another crucial segment. Pediatric dentists are heavy users of Glass Ionomer Cements due to their therapeutic fluoride release and simplified bonding protocols, making the material ideal for treating children. Prosthodontists often require materials suitable for core build-ups prior to crown placement or specific formulations for indirect restorations. Furthermore, large Dental Service Organizations (DSOs) and consolidated clinic chains act as powerful institutional buyers. They often negotiate large-volume procurement contracts, preferring suppliers who can provide a comprehensive portfolio of materials, reliable logistics, and competitive pricing across multiple brands and formulations to standardize clinical practice across their network.

In addition to clinical entities, academic and research institutes are essential end-users, serving both educational and research functions. Dental schools purchase filling powders for student training purposes, often requiring large volumes of diverse, mid-range materials for simulation labs. Research institutes utilize specialized, often experimental, powder formulations for clinical trials, material testing, and the development of next-generation biomaterials. Their procurement decisions are often influenced by the need for cutting-edge technology and materials supported by robust scientific data, making them key partners for manufacturers introducing innovative, high-performance powder products to the market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 1.85 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Dentsply Sirona, 3M, Ivoclar Vivadent, GC Corporation, Kuraray Dental, SDI Limited, SHOFU Dental, VOCO GmbH, Coltene Holding, Ultradent Products, Septodont, DMG America, Heraeus Kulzer, Tokuyama Dental, Mitsui Chemicals (Heraeus Kulzer/Kulzer). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Dental Filling Powder Market is characterized by a rapid evolution toward nanotechnology and bio-active material incorporation, aimed at improving longevity, handling, and therapeutic benefits. Nanotechnology is pivotal, allowing manufacturers to reduce filler particle size significantly (into the nanometer range) in resin composites. This innovation enhances polish retention, surface smoothness, and mechanical strength while minimizing polymerization shrinkage, resulting in restorations that mimic the optical properties and texture of natural enamel more closely. The development of nanohybrid and nanofilled composites addresses the long-standing challenge of balancing high strength with superior aesthetics, solidifying their position as the gold standard for high-performance posterior and aesthetic anterior restorations.

Another crucial technological development involves the continuous refinement of Glass Ionomer Cements (GIC) and their resin-modified counterparts (RMGICs). Modern GIC powders are engineered with optimized polyacrylic acid components and ultrafine glass particles to achieve enhanced initial strength and fluoride release kinetics over extended periods, offering a significant advantage in areas of high caries risk or in situations requiring chemical adhesion without complex bonding agents. Bio-active filling powders, which release beneficial ions (like calcium and phosphate) that encourage remineralization of adjacent tooth structure, represent the leading edge of regenerative dentistry. These materials are transitioning from niche products to mainstream offerings, promising a shift from passive filling to active tooth repair and protection.

Furthermore, bulk-fill technology has significantly impacted the composite segment. Historically, composite restorations required incremental layering (2mm maximum) to manage polymerization stress and ensure adequate curing depth. Bulk-fill powders and corresponding matrices allow dentists to place and cure larger increments (up to 4mm or 5mm) in a single step, drastically reducing chair time and complexity, particularly in posterior restorations. This technological advancement directly addresses clinical efficiency concerns, making restorative procedures faster and less technique-sensitive. Manufacturers are focusing R&D efforts on adjusting the photoinitiator systems and increasing filler translucency to facilitate deeper and more uniform curing, ensuring the sustained clinical performance of these time-saving restorative materials.

The increasing global emphasis on cosmetic appearance and the rising demand for metal-free, tooth-colored restorations, primarily resin-based composites and advanced Glass Ionomer Cements (GICs), are the primary drivers for aesthetic dental filling powders, driven by patient preference and improved material science.

The Resin-based Composites segment currently holds the largest market share by value, attributed to their superior aesthetic qualities, versatility in restorative procedures, and continuous innovation in nanofilled and bulk-fill technologies that enhance efficiency and longevity.

Bio-active dental filling powders, particularly specialized GICs, are shifting restorative dentistry from passive repair to active protection by releasing therapeutic ions like fluoride and calcium, which stimulate remineralization and prevent secondary decay at the margin of the restoration, improving long-term oral health outcomes.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR) due to rapid development in dental infrastructure, significant growth in disposable income, and expanding public awareness of dental health in highly populous countries like China and India.

The main drawbacks include the high material cost, which restricts adoption in low-income markets, and the technique-sensitivity of application, which requires careful moisture control and precise curing protocols to ensure optimal clinical performance and longevity of the restoration.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.