ID : MRU_ 436438 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

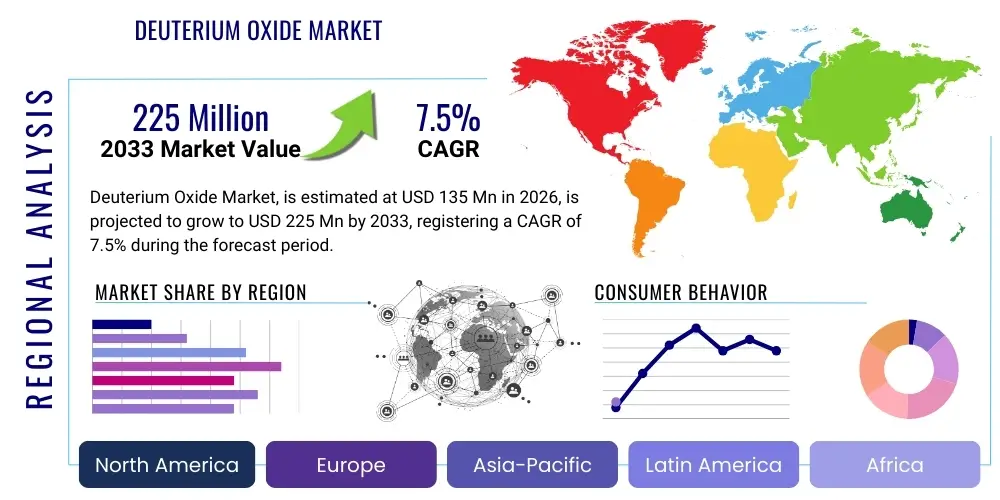

The Deuterium Oxide Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 580 Million in 2026 and is projected to reach USD 910 Million by the end of the forecast period in 2033.

Deuterium oxide, commonly known as heavy water (D2O), is a stable isotope of water where the two hydrogen atoms are replaced by deuterium—an isotope of hydrogen containing one proton and one neutron. This substitution alters the physical and chemical properties significantly compared to normal light water (H2O), making D2O indispensable across highly specialized industrial and scientific applications. Its primary distinguishing characteristics, such as a higher boiling point and slower neutron absorption cross-section, position it uniquely within the global chemical and energy sectors. The market is defined by stringent regulatory requirements due to its strategic importance, particularly in nuclear energy production and high-purity pharmaceutical manufacturing.

The primary applications of Deuterium Oxide center around its exceptional performance as a moderator and coolant in specific types of nuclear reactors, specifically Pressurized Heavy Water Reactors (PHWRs), allowing for the use of natural uranium as fuel. Beyond the energy sector, D2O is critical in life sciences for synthesizing deuterated compounds used in advanced pharmaceutical formulations and metabolic studies, enhancing drug efficacy and stability. Furthermore, its application extends to fiber optics, semiconductor manufacturing, and advanced analytical chemistry techniques such as Nuclear Magnetic Resonance (NMR) spectroscopy, which relies on D2O as a solvent for structural determination.

Key driving factors accelerating the Deuterium Oxide Market include the global emphasis on nuclear power generation as a stable, low-carbon energy source, particularly in developing economies expanding their PHWR capacity. Simultaneously, the rapid growth of the pharmaceutical and biotechnology industries, fueled by increased R&D spending on novel drug development and personalized medicine, necessitates greater supplies of high-purity deuterated solvents. The inherent benefits of D2O, such as its ability to significantly improve the half-life and stability of certain therapeutic drugs and its crucial role in ensuring the safety and efficiency of nuclear processes, continue to underpin sustained market expansion and technological innovation across diverse end-use verticals.

The Deuterium Oxide Market is characterized by robust growth, driven primarily by the resurgence in nuclear energy investment globally and the escalating demand for deuterated solvents within the highly regulated pharmaceutical sector. Current business trends indicate a strategic push towards enhancing production efficiency using advanced separation techniques, such as laser separation and improved catalytic exchange methods, aimed at reducing the substantial energy footprint associated with traditional heavy water manufacturing processes. Market competition remains concentrated, dominated by government-controlled entities and a few specialized private manufacturers capable of achieving the necessary isotopic purity levels, leading to high barriers to entry and necessitating long-term supply agreements within key industries.

Regionally, the market exhibits strong dichotomy. Asia Pacific (APAC) dominates demand, propelled by significant capacity expansion in nuclear power programs in countries like India, China, and South Korea, which heavily rely on PHWR technology. North America and Europe, while having mature nuclear infrastructure, are seeing moderate growth centered predominantly on high-value applications in pharmaceuticals, advanced materials, and scientific research. Regulatory trends across these regions emphasize safety, purity standards, and non-proliferation policies, directly influencing sourcing strategies and limiting the free trade of D2O, especially large volumes necessary for nuclear applications, thereby shaping localized supply chains and pricing dynamics.

Segment trends reveal that the Nuclear Grade segment (typically 99.75% purity or higher) maintains the largest market share by volume due to constant replacement needs in existing reactors and new plant installations. However, the Pharmaceutical Grade segment, demanding ultra-high purity (>99.9% D2O), is witnessing the fastest growth in terms of value, driven by the expanding clinical pipeline for deuterated drugs. Companies are increasingly focusing their R&D efforts on synthesizing specialized, lower-volume deuterated organic compounds for precision medicine, reflecting a shift towards high-margin, specialized applications rather than bulk commodity sales, further fragmenting demand within the overall chemical applications segment.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Deuterium Oxide market typically revolve around optimizing the energy-intensive production processes, enhancing safety and predictive maintenance in nuclear facilities using D2O, and accelerating the discovery and synthesis of new deuterated pharmaceutical compounds. Users frequently inquire whether AI can fundamentally lower the immense energy costs associated with isotopic separation, historically the primary barrier to entry and pricing factor for heavy water. Furthermore, interest focuses on how AI-driven predictive analytics can manage the complex thermal and fluid dynamics within heavy water reactors, ensuring optimal moderation and cooling efficiency while extending the operational lifespan of critical components and minimizing potential leakage risks.

The core theme emerging from these inquiries is the leveraging of AI and Machine Learning (ML) to improve efficiency across the entire D2O lifecycle, from manufacturing optimization to end-use application management. In manufacturing, AI algorithms are being deployed to analyze vast datasets related to temperature, pressure, and flow rates in production facilities (like the Girdler Sulfide process), allowing for real-time adjustments that maximize deuterium extraction yields while minimizing energy consumption and waste. This data-driven approach promises to make D2O production more economically viable and environmentally sustainable, directly addressing market concerns over high operational expenditures and long lead times.

In the end-user sectors, particularly pharmaceuticals, AI is fundamentally transforming how deuterated molecules are designed. Generative AI models are utilized to predict the stability, metabolic pathways, and pharmacological activity of hundreds of novel deuterated drug candidates simultaneously, drastically accelerating the pre-clinical R&D phase. Within nuclear facilities, AI-powered image recognition and sensor fusion are enhancing quality control for D2O purity and detecting minute component failures or corrosion in heavy water circuits before they escalate, providing an enhanced level of operational safety and contributing to regulatory compliance and the reduced reliance on manual, inspection-heavy monitoring systems.

The Deuterium Oxide Market is shaped by a critical balance of powerful drivers (D) related to strategic energy needs and scientific advancements, significant restraints (R) tied to technical complexity and regulation, and key opportunities (O) stemming from emerging technological applications. A primary driver is the accelerating global investment in nuclear energy, especially in Asian countries preferring the indigenous design of Pressurized Heavy Water Reactors (PHWRs), which mandates substantial initial inventories and ongoing replacement volumes of D2O. Concurrently, the robust growth in the pharmaceutical industry and the success of deuterated drugs in clinical trials are driving premium demand for ultra-high purity D2O for solvent and reagent use, solidifying its position as a high-value chemical asset.

However, the market faces significant restraints. The immense capital expenditure and operational complexity associated with constructing and running large-scale heavy water production plants constitute a high barrier to entry, resulting in limited global supply capacity. Furthermore, the strategic nature of D2O, categorized often as a dual-use material, necessitates extremely stringent international trade controls and non-proliferation regulations. These regulatory hurdles impede global commerce, inflate administrative costs, and introduce geopolitical volatility into the supply chain, often creating bottlenecks and long lead times for end-users outside of major producing nations, thereby slowing market liquidity and expansion.

Opportunities for market growth primarily lie in technological innovations that enhance production efficiency and open new application areas. Advancements in non-traditional separation techniques, such as highly selective laser isotope separation (LIS) or advanced membrane technology, promise to potentially lower production costs and decentralize supply, addressing the current restraint of limited global capacity. Moreover, the expanding use of deuterium labeling in advanced diagnostics, fundamental physics research (e.g., fusion research), and niche electronic applications (e.g., optical fibers and displays) presents untapped high-margin opportunities that are less sensitive to bulk commodity pricing pressures, offering market diversification away from the historically dominant nuclear segment and reinforcing overall market resilience against fluctuating energy policies.

The Deuterium Oxide market is meticulously segmented across purity level, application, and end-user industry to reflect the diverse and specific requirements of its consuming sectors. Purity level is arguably the most critical dimension, dictating the feasibility and pricing for various uses, ranging from nuclear-grade (ultra-high purity essential for neutron moderation) to commercial and research grades used in laboratories and less demanding industrial applications. The application segments clearly delineate the distinct functional roles of D2O, such as its bulk use in nuclear systems versus its highly specialized use as a reaction solvent or tracer in medical science, providing a granular view of demand dynamics and growth pockets across the global market landscape.

The value chain for Deuterium Oxide is highly specialized and complex, beginning with the upstream sourcing of feed water, typically natural water, which contains deuterium at a concentration of approximately 150 parts per million (ppm). The upstream phase is dominated by large-scale, highly technical operations involving initial concentration via processes like distillation or catalytic exchange (Girdler Sulfide process), requiring substantial energy input and sophisticated infrastructure management. Success in this phase is critically dependent on access to reliable, low-cost power sources and extensive chemical engineering expertise, defining the high entry barriers seen across the industry and concentrating production capacity within a few global entities, often state-owned or heavily subsidized enterprises.

The midstream phase involves further purification and isotopic separation to achieve the requisite nuclear or pharmaceutical grade purity, often utilizing secondary refinement techniques like vacuum distillation or electrolysis. This stage is focused on quality control, ensuring the final product meets the stringent purity specifications (e.g., 99.9% D2O) demanded by regulated industries. Packaging and storage are also critical, given the high value and strategic nature of D2O, often requiring specialized containment to prevent contamination or leakage. Distribution channels for D2O are predominantly direct, particularly for bulk nuclear-grade quantities, minimizing handling and ensuring secure, regulated transfer from manufacturer to the licensed end-user facility.

The downstream element of the value chain involves the utilization and management of D2O by end-users. In the nuclear sector, this includes commissioning reactors and ongoing heavy water management, demanding continuous monitoring and periodic refurbishment. For the pharmaceutical industry, D2O serves as a critical raw material for synthesizing deuterated active pharmaceutical ingredients (APIs) and as a solvent in advanced analysis. Indirect distribution channels, often involving specialized chemical distributors or brokers, are more common for smaller volumes of research and pharmaceutical-grade D2O, serving a wider array of academic, research, and smaller biotech firms, facilitating access to niche markets while maintaining strict track-and-trace protocols to comply with regulatory oversight.

The potential customer base for Deuterium Oxide is highly segmented, driven by the unique physical properties of D2O, which are essential for specific high-technology applications. The most significant and volume-intensive customers are entities involved in the nuclear energy sector, specifically operators and developers of Pressurized Heavy Water Reactors (PHWRs), such as CANDU reactors. These customers require massive initial fills and substantial annual top-ups to compensate for small losses during operation, making them the anchor customers for nuclear-grade D2O manufacturers, often secured through long-term, government-backed procurement contracts and involving direct sales relationships.

The fastest-growing segment of potential customers includes pharmaceutical and biotechnology companies specializing in drug discovery and development. These customers utilize high-purity D2O as a crucial solvent for Nuclear Magnetic Resonance (NMR) spectroscopy to determine molecular structures, and critically, as a starting material for synthesizing deuterated drugs. By replacing hydrogen with deuterium in specific parts of a drug molecule, these companies aim to improve metabolic stability, enhance bioavailability, and extend the therapeutic half-life of their medications, driving consistent, albeit lower-volume, high-value demand for pharmaceutical-grade D2O for their R&D and manufacturing pipelines.

Furthermore, a diverse set of smaller, but strategically important, potential customers exists across academia, specialized chemical manufacturing, and high-tech industries. Academic and government research institutions are continuous consumers of various grades of D2O for fundamental physics research, isotope tracing studies, and material science experiments. Within the electronics sector, manufacturers of certain specialized fiber optics and advanced displays use D2O components to enhance performance and durability. These customers often procure D2O through specialized chemical suppliers or authorized distributors, emphasizing product purity and rapid, reliable delivery for their specialized and often proprietary manufacturing processes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 580 Million |

| Market Forecast in 2033 | USD 910 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Heavy Water Board (HWB, India), Areva (Orano, France), Russia's Rosatom, China National Nuclear Corporation (CNNC), Ontario Power Generation (OPG, Canada), Korea Hydro & Nuclear Power (KHNP), Linde PLC, Merck KGaA, Cambridge Isotope Laboratories (CIL), ISOTEC (Sigma-Aldrich), Kanto Kagaku, Spectra Gases, Mitsui Chemicals, Ceramatec, Urenco, Atomic Energy of Canada Limited (AECL), Tianjin HuaDeDeuterium Oxide Co., Ltd., Sumitomo Chemical, VWR International, TCI Chemicals. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for Deuterium Oxide production is highly dominated by well-established, energy-intensive isotopic separation processes, which dictate the economic viability and global supply dynamics of the market. Historically, the Girdler Sulfide (GS) process has been the cornerstone of heavy water production globally, relying on the chemical exchange between hydrogen sulfide (H2S) gas and water to concentrate deuterium. While effective for large-scale, high-volume production, the GS process requires massive, complex infrastructure, operates at high pressures and temperatures, and necessitates stringent safety measures due to the toxicity of H2S, contributing significantly to the high capital and operational costs associated with nuclear-grade D2O manufacturing.

A second crucial technological approach is water distillation, which exploits the slight difference in boiling points between light water and heavy water. This method is often utilized as a secondary refinement process to achieve ultra-high purity levels required for pharmaceutical and specialized research applications, or as a standalone process in regions where the feed water has an elevated natural deuterium concentration. Although distillation is cleaner than the GS process, its efficiency is low, requiring immense amounts of energy to process large volumes of water, thus often making it economically suitable only for achieving the final stages of high purification rather than initial bulk concentration, highlighting the inherent technological trade-off between purity, volume, and energy expenditure in the sector.

More advanced or emerging technologies are actively being explored to disrupt this landscape, particularly to reduce the reliance on the energy-intensive and environmentally challenging GS process. Technologies such as catalytic exchange (CE) combined with hydrogen distillation offer a more benign and efficient alternative, utilizing specialized catalysts to facilitate the exchange of deuterium between water and hydrogen gas at lower temperatures. Furthermore, research into laser isotope separation (LIS) promises a future where deuterium separation could be achieved with significantly reduced energy requirements and a smaller physical footprint. While LIS remains largely in the developmental and pilot phases for large-scale production, successful commercialization of these innovative methods could fundamentally shift market dynamics, leading to lower production costs, decentralized supply chains, and enhanced flexibility in meeting the specific purity requirements of the rapidly growing non-nuclear sectors.

The Deuterium Oxide market exhibits pronounced regional variation, primarily driven by governmental policies regarding nuclear energy infrastructure and the concentration of high-end pharmaceutical research and manufacturing capabilities. Asia Pacific (APAC) stands out as the predominant consumer and growth engine, largely attributable to the massive investment in nuclear power expansion in countries such as India and China. These nations have either adopted or developed indigenous PHWR technology, which requires substantial inventories of nuclear-grade D2O for moderation. The long-term energy security strategies, coupled with rapid industrialization and urbanization, ensure sustained, large-volume demand for heavy water, making APAC the cornerstone of the bulk D2O market and a crucial region for market forecasting.

North America (NA), particularly the United States and Canada, holds a mature market position characterized by high demand for specialized, high-ppurity D2O grades. Canada, historically a major producer and developer of the CANDU reactor, maintains a significant operational fleet, ensuring ongoing replacement demand. In the U.S., while the use of D2O in energy is less dominant than in Canada, the concentration of world-leading pharmaceutical companies, biotechnology firms, and advanced research laboratories drives high-value demand for pharmaceutical-grade D2O used in drug synthesis, metabolic studies, and NMR solvents. The North American regional focus is shifting increasingly towards high-margin, specialized applications rather than bulk nuclear consumption, reflecting the advanced nature of its R&D economy.

Europe represents a stable market with mixed dynamics. Countries with active nuclear programs (e.g., Romania, which operates CANDU reactors) contribute to the nuclear demand segment. Crucially, the presence of major global chemical and pharmaceutical hubs, notably in Germany, Switzerland, and the UK, ensures a strong and resilient demand for research and pharmaceutical grades of D2O. European regulations and environmental standards often push manufacturers towards exploring cleaner, more energy-efficient production methods, influencing technological development across the continent. Meanwhile, Latin America (LATAM) and the Middle East and Africa (MEA) currently represent emerging markets, where D2O demand is episodic, tied primarily to sporadic large-scale infrastructure projects, such as new nuclear plant proposals in countries exploring nuclear capabilities for the first time, or limited, localized research activities.

The primary factor driving demand is the global expansion and maintenance of Pressurized Heavy Water Reactors (PHWRs), such as the CANDU reactor design. D2O serves as an essential moderator and coolant in these reactors, allowing them to utilize natural uranium, thus necessitating large-scale, strategic procurement for commissioning and operational top-ups worldwide.

The production of Deuterium Oxide is highly energy-intensive, primarily utilizing the Girdler Sulfide process, which requires significant capital investment and high operational expenditure. This leads to high manufacturing costs, limits the number of global producers, and creates high barriers to entry, resulting in constrained supply capacity and geopolitical sensitivity regarding its trade and inventory management.

In pharmaceuticals, D2O is vital for synthesizing deuterated drugs. By substituting hydrogen with deuterium, pharmaceutical companies can enhance the drug's metabolic stability and extend its half-life in the body, potentially improving patient efficacy and dosing regimens. It is also extensively used as a solvent in advanced Nuclear Magnetic Resonance (NMR) spectroscopy for chemical analysis.

The Asia Pacific (APAC) region, particularly India and China, leads in consumption by volume. This dominance is attributed to their aggressive long-term energy strategies focused on expanding indigenous nuclear power capacity through PHWR technology, which requires sustained, bulk quantities of high-purity heavy water to fuel and moderate their reactor fleets.

Yes, research is actively focusing on non-traditional separation methods to improve sustainability. Technologies such as advanced catalytic exchange combined with hydrogen distillation and highly selective laser isotope separation (LIS) are being developed to reduce the massive energy consumption and environmental footprint associated with the legacy Girdler Sulfide production process.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.