ID : MRU_ 434827 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

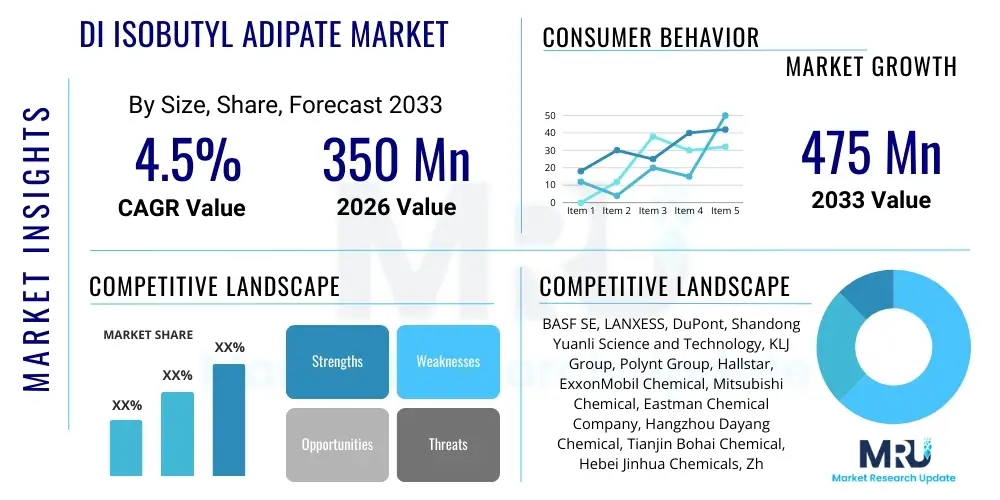

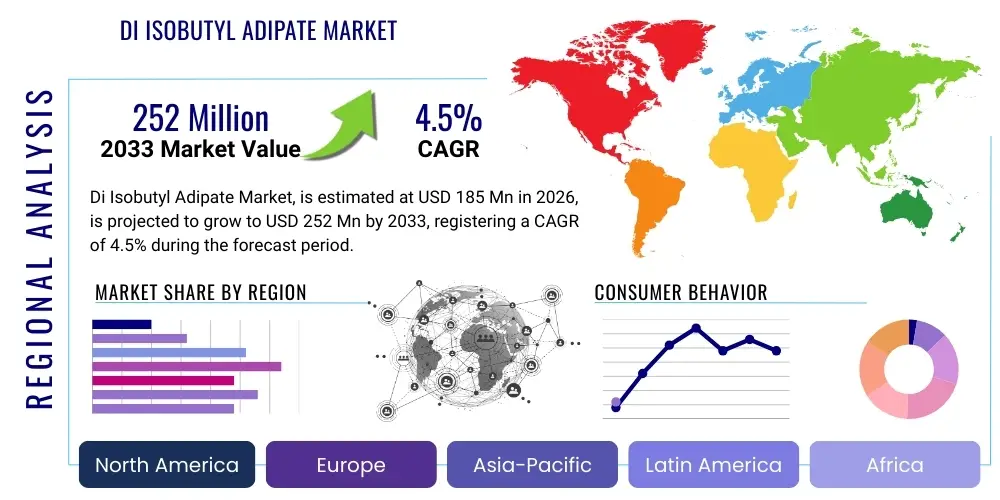

The Di Isobutyl Adipate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2026 and 2033. The market is estimated at USD 350 Million in 2026 and is projected to reach USD 475 Million by the end of the forecast period in 2033.

The Di Isobutyl Adipate (DIBA) market encompasses the production, distribution, and utilization of this crucial organic compound, primarily valued for its properties as an effective plasticizer, emollient, and solvent. DIBA is a diester of isobutanol and adipic acid, characterized by its low viscosity, excellent solvency, and compatibility with various resins and polymers, including polyvinyl chloride (PVC), cellulose esters, and nitrocellulose. Historically, its primary application has been in the plastics industry, where it imparts flexibility, low-temperature performance, and ease of processing to PVC products, contributing significantly to sectors like automotive and construction.

Beyond traditional plasticizer uses, the demand for DIBA is strongly driven by the rapid expansion of the personal care and cosmetics industry. Its emollient properties, non-greasy feel, and ability to improve the spreadability of formulations make it highly sought after in sunscreens, lotions, and makeup products. Furthermore, its role as a high-performance solvent is expanding into specialty applications, including inks and agricultural formulations, where purity and stability are paramount. The versatility of DIBA across multiple high-growth end-user sectors solidifies its position as a critical intermediate chemical.

Key driving factors propelling market expansion include stringent environmental regulations promoting the shift toward safer, phthalate-free plasticizers in sensitive applications such as medical devices and food contact materials. DIBA, being a non-phthalate plasticizer, benefits directly from this regulatory landscape. Additionally, increasing consumer spending on premium cosmetic products, particularly in emerging economies, fuels the demand for high-quality emollients. Continuous technological advancements in DIBA synthesis methods aimed at reducing production costs and enhancing product purity further contribute to its market acceptance and growth.

The Di Isobutyl Adipate market is experiencing steady expansion, underpinned by robust business trends emphasizing sustainability and high-performance chemical intermediates. Major chemical manufacturers are focusing on backward integration to secure raw material supply (isobutanol and adipic acid) and optimize operational efficiencies, leading to competitive pricing structures. Strategic acquisitions and collaborations among regional players are prevalent, aiming to strengthen distribution networks, particularly in the highly fragmented Asia Pacific market. The shift towards bio-based alternatives for DIBA is gaining traction, although conventional synthesis remains dominant, reflecting the industry’s gradual pivot toward environmentally conscious manufacturing practices to meet increasing corporate social responsibility goals and consumer demand for green chemistry.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine, driven by burgeoning manufacturing industries in China and India, coupled with rapid urbanization boosting demand for PVC-based construction materials and automotive components. North America and Europe, while representing mature markets, exhibit steady growth primarily due to stringent regulatory environments phasing out traditional plasticizers, thereby creating substantial opportunities for DIBA as a compliant alternative. These regions are also leading in the adoption of advanced personal care formulations, further cementing DIBA’s use as a high-quality emollient. Market maturity in the West is countered by innovation focus, particularly in high-specification cosmetic and medical grades of DIBA.

Segment trends highlight the dominance of the plasticizers application segment, although the cosmetics and personal care segment is projected to register the fastest CAGR during the forecast period due to shifting consumer preferences towards specialized skincare products. Within end-use industries, the automotive sector remains a critical consumer, using DIBA-plasticized materials for interiors, wires, and cables requiring flexibility and resistance to low temperatures. There is a noticeable trend towards premiumization in product formulation, demanding high-purity DIBA grades, which commands higher profit margins and encourages manufacturers to invest in purification technologies.

Users frequently inquire about how Artificial Intelligence (AI) and Machine Learning (ML) can optimize the complex chemical synthesis process of DIBA, specifically focusing on reaction condition optimization, catalyst selection, and yield enhancement. There is significant concern regarding the integration costs of smart manufacturing systems and the potential disruption to established supply chain logistics. Key expectations revolve around AI’s ability to predict raw material price volatility, optimize inventory management for highly perishable or sensitive components, and ensure regulatory compliance by instantly analyzing changes in global chemical standards. Users are also keen on understanding AI’s role in accelerated formulation development, particularly in cosmetics, where fine-tuning emollient concentrations requires extensive testing.

The DIBA market is primarily driven by the strong push for phthalate alternatives in plasticization, especially in health-sensitive applications, coupled with burgeoning demand from the cosmetic industry where DIBA serves as a preferred emollient and spreading agent. However, the market faces constraints due to the fluctuating prices and limited availability of primary feedstocks, namely isobutanol and adipic acid, which are derivatives of crude oil and petrochemical processes, making them susceptible to geopolitical and economic instability. Opportunities arise from technological advancements leading to the development of bio-based DIBA, capitalizing on sustainability trends and offering enhanced market differentiation. The overall market dynamics are significantly shaped by the increasing regulatory pressure favoring non-toxic plasticizers, exerting a major impact force on substitution rates.

Drivers include the widespread adoption of DIBA in specialty PVC applications, such as medical tubing and food wraps, due to its low toxicity profile compared to traditional plasticizers. Furthermore, the sustained growth in the global automotive and construction industries necessitates flexible, durable plastic components that benefit from DIBA’s low-temperature flexibility properties. Restraints mainly revolve around intense competition from other non-phthalate plasticizers, such as citrate esters and benzoate esters, which might offer comparable performance at different price points or possess unique formulation advantages in specific niche applications. Additionally, the complex and capital-intensive nature of DIBA manufacturing poses a high barrier to entry for new players.

The primary opportunities lie in penetrating emerging markets in Southeast Asia and Latin America, where industrialization and consumer spending are escalating rapidly. Furthermore, the ongoing research into utilizing DIBA in high-performance lubricant formulations and specialized solvent mixtures for advanced materials offers new avenues for market expansion beyond its traditional applications. Impact forces are overwhelmingly driven by regulatory policies; the European Union’s continuous evaluation and restriction of toxic chemicals necessitate constant reformulation, benefiting compliant alternatives like DIBA. Moreover, the increasing consumer preference for natural and organic cosmetics acts as a powerful downstream force influencing DIBA manufacturers to explore sustainable sourcing.

The Di Isobutyl Adipate market is comprehensively segmented based on its primary application, the end-use industry utilizing the compound, and the grade of DIBA offered (standard vs. high purity). This multi-faceted segmentation allows for precise market analysis, identifying high-growth pockets and underlying demand dynamics. The application segmentation provides insight into the diverse roles DIBA plays, ranging from modifying polymer properties to enhancing cosmetic formulations. Analyzing end-use industries reveals key consumption patterns, linking DIBA demand directly to macroeconomic drivers in sectors like construction, automotive, and consumer goods.

Segmentation by grade is becoming increasingly critical, differentiating commodity DIBA used in industrial solvents from high-purity, low-odor grades essential for sensitive applications like cosmetics, pharmaceuticals, and medical devices. The premiumization of cosmetic formulations, particularly those marketed as clean-label or hypoallergenic, necessitates stringent quality control and high purity, commanding higher prices and driving innovation in purification technologies. Manufacturers are increasingly tailoring production processes to meet these specific purity requirements, thereby segmenting the competitive landscape based on technological capability and quality assurance.

Geographic segmentation remains vital, showing significant variation in growth rates and regulatory influences. Asia Pacific dominates consumption due to high manufacturing output, whereas regulatory changes primarily drive growth in North America and Europe. Understanding these segment dynamics is crucial for strategic market positioning, allowing companies to allocate resources effectively, optimize production capacities, and focus on segments offering the highest return on investment, such as the rapidly expanding cosmetics sector or the high-value specialty plasticizer market.

The value chain for the Di Isobutyl Adipate market begins with the procurement of key raw materials—namely, adipic acid and isobutanol. Adipic acid is typically derived from cyclohexane through oxidation, while isobutanol is primarily sourced through petrochemical synthesis, although bio-based routes are emerging. Upstream analysis focuses heavily on the petrochemical sector, as raw material price volatility directly impacts the profitability of DIBA manufacturers. Strong relationships with reliable feedstock suppliers are crucial for maintaining stable production costs and ensuring supply continuity, given that these materials are widely used across various chemical industries, leading to intense competition for sourcing.

The manufacturing stage involves the esterification reaction between adipic acid and isobutanol, often catalyzed by strong acids, followed by extensive purification processes, including distillation and filtration, particularly for cosmetic-grade DIBA. Efficiency in this midstream segment is vital, requiring optimized reactor design, energy management, and waste minimization to maintain competitiveness. The output quality, especially purity levels, dictates the end application, with high-purity manufacturers gaining a premium in the personal care and medical sectors. Investment in advanced purification technology is a key differentiator among leading DIBA producers globally.

Downstream analysis covers distribution and end-use. DIBA is distributed through both direct sales (to large chemical consumers, PVC compounders, and major cosmetic houses) and indirect channels utilizing regional chemical distributors and specialized agents. Direct distribution is common for high-volume technical grades, while specialized distributors handle smaller, high-purity cosmetic volumes, often requiring specialized logistics and storage. End-users, encompassing polymer manufacturers, cosmetic formulators, and ink producers, exert significant pull on the market based on their formulation needs and regulatory requirements, driving demand for specific grades and packaging formats.

The primary potential customers for Di Isobutyl Adipate are major manufacturers operating within the plastics and cosmetic industries globally. Plasticizers are bought by PVC compounders and polymer processors who require flexible, durable, and low-toxicity additives for their final products, which range from automotive interior parts (dashboards, seals) to essential construction materials (flooring, cables). These customers are sensitive to product compliance, particularly the move towards non-phthalate solutions, making DIBA an attractive procurement choice. They typically purchase in bulk volumes (drums or tankers) under long-term supply contracts, emphasizing consistency and competitive pricing.

The second largest customer base comprises formulators in the personal care and cosmetic industry. These companies, ranging from multinational giants to specialized niche brands, purchase cosmetic-grade DIBA as an emollient, solvent, and pigment dispersant for sunscreens, foundations, moisturizers, and lipsticks. Their purchasing criteria are extremely stringent, focusing on ultra-high purity, low odor, non-irritant properties, and compliance with global cosmetic safety standards (e.g., EU Cosmetic Regulation). This segment often demands smaller, customized batches but at premium prices, rewarding suppliers capable of delivering guaranteed quality and traceability.

Other significant potential customers include manufacturers of specialty industrial solvents, particularly those creating high-performance inks and coatings requiring excellent solvency and low volatility, and lubricant blenders looking for synthetic ester components to enhance low-temperature performance and stability. Agricultural chemical manufacturers also utilize DIBA as an effective solvent and carrier for active ingredients in pesticide and herbicide formulations. These industrial customers prioritize technical specifications, performance guarantees, and reliable supply chains, often requiring technical support and certification documents from DIBA vendors.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350 Million |

| Market Forecast in 2033 | USD 475 Million |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, LANXESS, DuPont, Shandong Yuanli Science and Technology, KLJ Group, Polynt Group, Hallstar, ExxonMobil Chemical, Mitsubishi Chemical, Eastman Chemical Company, Hangzhou Dayang Chemical, Tianjin Bohai Chemical, Hebei Jinhua Chemicals, Zhejiang Jianye Chemical, Jiangsu Jingting Chemical, TCI Chemicals, Parchem fine & specialty chemicals, Teknor Apex, Emerald Kalama Chemical, New Japan Chemical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing technology for Di Isobutyl Adipate primarily relies on the well-established batch or continuous esterification process. This process involves reacting adipic acid with isobutanol, often in the presence of a strong acid catalyst (such as sulfuric acid or p-toluenesulfonic acid). The critical technological advancements in this conventional method are centered on optimizing catalyst recovery and minimizing energy usage during the distillation phase. Modern plants increasingly utilize highly selective catalysts and integrated heat exchangers to improve yield efficiency and reduce environmental impact, moving towards continuous flow reactors for larger scale, consistent production, which minimizes variance and operating costs compared to older batch processes.

A key area of technological differentiation lies in the purification and refinement processes, especially for producing cosmetic-grade DIBA. Achieving the necessary high purity (often >99.5%) and minimal odor requires advanced techniques such as multi-stage fractional distillation, carbon treatment, and specialized filtration systems to remove trace impurities, unreacted raw materials, and colored bodies. Companies investing heavily in these purification steps are able to command premium pricing and secure contracts in sensitive sectors like pharmaceuticals and high-end cosmetics. This focus on high-grade synthesis dictates significant capital expenditure in specialized equipment and quality assurance technologies.

The most transformative technology landscape emerging is the development of bio-based DIBA. This involves synthesizing DIBA components using fermentation or enzymatic pathways, deriving adipic acid or isobutanol from renewable biomass (sugars, starches). While currently niche due to higher production costs compared to petrochemical routes, bio-based DIBA aligns perfectly with global sustainability goals and AEO trends related to "green chemistry" and reduced carbon footprint. Successful commercialization of cost-effective bio-based routes, currently a key focus of R&D, represents a disruptive technological shift that could reshape the competitive landscape and significantly influence consumer acceptance in environmentally conscious markets like Europe and North America.

DIBA serves predominantly as a high-performance, non-phthalate plasticizer, crucial for imparting flexibility, durability, and excellent low-temperature resistance to polymers like PVC. It also functions effectively as a solvent in specialty coatings and as an emollient in cosmetic formulations, enhancing texture and spreadability.

Global regulatory bodies, especially in Europe (REACH) and North America, are increasingly restricting the use of traditional phthalate plasticizers due to health concerns. This regulatory pressure strongly drives market demand for compliant, non-phthalate alternatives like DIBA, particularly in sensitive end-uses such as medical, food-contact, and children’s products.

Historically, the building and construction industry, driven by the need for flexible PVC components (flooring, cables, sealants), has been the largest consumer. However, the rapidly expanding cosmetics and personal care sector is projected to be the fastest-growing end-user segment, utilizing DIBA for its superior emollient and spreading characteristics.

The core raw materials are adipic acid and isobutanol, both largely derived from petrochemical processes. The main risks involve feedstock price volatility, as their pricing is directly linked to crude oil markets, potentially impacting DIBA manufacturing costs and overall market profitability.

Asia Pacific is the dominating regional market, characterized by both high production capacity and the highest consumption growth rate. This dominance is fueled by robust manufacturing sectors, rapid infrastructure development, and escalating consumer demand for personal care products across countries like China, India, and South Korea.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.