ID : MRU_ 437630 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

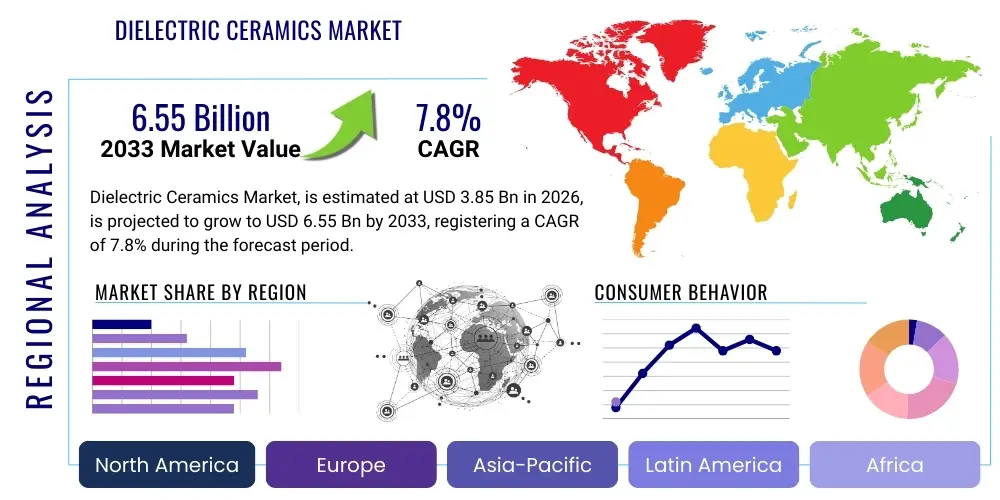

The Dielectric Ceramics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 3.85 Billion in 2026 and is projected to reach USD 6.55 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the relentless miniaturization trend across the electronics industry, particularly in high-frequency and high-power applications where traditional materials fail to meet stringent performance requirements regarding low dielectric loss, high dielectric constant, and thermal stability. The rapid proliferation of 5G infrastructure deployment globally, requiring massive numbers of passive components like multilayer ceramic capacitors (MLCCs) and specialized filters, is the primary accelerator of market valuation during this projection window.

Dielectric ceramics are advanced inorganic, non-metallic materials characterized by their ability to store electrical energy efficiently while exhibiting high resistance to the flow of electric current. These materials possess specific electrical properties, such as a high dielectric constant (K) and low dielectric loss (tan $\delta$), making them indispensable in the manufacturing of various electronic components. They form the core functional element in passive devices like capacitors, resonators, inductors, and filters. The market encompasses a broad range of material compositions, including titanates (like Barium Titanate, BaTiO3), complex perovskites, alumina, and zirconia, each tailored for specific operational frequencies and temperature stability requirements, ranging from standard consumer electronics to specialized aerospace systems.

Major applications of dielectric ceramics span several high-growth sectors, including telecommunications (5G base stations, satellite communication equipment), automotive electronics (ADAS, EV charging infrastructure, battery management systems), and industrial machinery (high-power switching, energy storage). The primary benefit derived from using these specialized ceramics is their superior performance under harsh operating conditions, including high temperatures and high electrical fields, coupled with their ability to enable significant device miniaturization. This capability is critical for optimizing space utilization and improving overall efficiency in modern electronic designs. Key driving factors propelling market growth include the explosive demand for MLCCs in high-density printed circuit boards, the technological shift towards higher operating frequencies (above 10 GHz), and significant governmental investments in smart infrastructure and renewable energy storage solutions.

The Dielectric Ceramics Market is currently experiencing a robust uptrend characterized by significant capital investment in capacity expansion, particularly within the Asia Pacific region, which serves as the global manufacturing hub for electronic passive components. Business trends indicate a strong focus on developing Ultra Low Loss (ULL) and High K dielectric materials suitable for millimeter-wave frequency applications, which are integral to 5G and emerging 6G technologies. Mergers and acquisitions focusing on vertical integration—securing raw material supply chains and advanced synthesis technologies—are common strategies employed by market leaders to maintain a competitive edge and optimize production costs. Furthermore, there is an increasing shift toward automated manufacturing processes utilizing artificial intelligence and machine learning to ensure material consistency and reduce defects in complex multilayer structures like high-capacitance MLCCs.

Regionally, Asia Pacific maintains undisputed dominance, driven by massive manufacturing capacities in China, South Korea, and Japan, coupled with intense domestic demand from consumer electronics and automotive sectors. North America and Europe are distinguished by their high-value, specialized demand, focusing primarily on high-reliability applications such as military radar systems, space technology, and advanced medical imaging devices, favoring highly engineered, customized ceramic formulations. Segment-wise, Barium Titanate and its derivatives remain the largest segment by material type due to their widespread use in MLCCs, although emerging materials like high-purity alumina and complex metal oxides are rapidly gaining traction in high-power and high-frequency filtering applications, reflecting the continuous pursuit of optimized material performance characteristics tailored for extreme environments.

User queries regarding the impact of Artificial Intelligence (AI) on the Dielectric Ceramics Market frequently center on AI's ability to accelerate material discovery, optimize complex sintering and firing processes, and enhance quality control during high-volume manufacturing of components like MLCCs. Users are keen to understand how AI-driven simulation and machine learning models can predict the electrical performance (dielectric constant, Q factor) of novel ceramic compositions before costly physical synthesis, thereby reducing R&D cycles. There is also significant interest in AI's role in predictive maintenance for ceramic processing equipment and minimizing energy consumption during the extremely energy-intensive thermal treatment phases of ceramic fabrication.

The application of AI and machine learning (ML) is fundamentally transforming the R&D and manufacturing landscape of dielectric ceramics, moving the industry away from traditional, trial-and-error methodologies towards data-driven material engineering. AI algorithms are adept at processing vast datasets related to crystal structure, composition, processing parameters, and resulting electrical properties, enabling the rapid identification of optimal material candidates for specific high-frequency or high-power applications. This predictive capability is crucial for meeting the stringent requirements imposed by next-generation electronic systems, where performance margins are extremely tight and new functional materials are constantly needed.

In manufacturing, AI significantly improves yield rates and consistency, which are paramount in the production of sub-millimeter scale components like MLCCs. Machine vision systems coupled with deep learning algorithms perform real-time defect detection during layering and stacking processes, identifying microscopic flaws invisible to human inspectors. Furthermore, ML models optimize kiln profiles and sintering temperatures, ensuring uniform density and grain size distribution, which directly translates to superior and reliable dielectric performance. This integration of intelligent automation is pivotal for scaling production efficiently to meet the skyrocketing global demand for passive components.

The Dielectric Ceramics Market is shaped by a confluence of powerful drivers related to technological advancement in electronics, balanced against strict material performance constraints and complex geopolitical trade dynamics. The primary drivers include the exponential growth in demand for connected devices (IoT, smart homes), the rapid rollout of 5G/6G communication infrastructure, and the massive shift toward vehicle electrification, which necessitates robust, high-performance ceramic components for power management and filtering systems. Conversely, market restraints largely revolve around the high initial capital investment required for cleanroom facilities and specialized processing equipment (e.g., thin film deposition apparatus), the volatility in pricing and supply chain stability of key raw materials (e.g., precious metals like Palladium and Silver used in electrode inks), and the highly complex regulatory landscape surrounding material purity and component reliability in mission-critical applications.

Opportunities in this sector are concentrated in the development of next-generation materials, particularly Low-Temperature Co-fired Ceramics (LTCC) and Ultra-Low Loss ceramics designed specifically for operation in the millimeter-wave spectrum (28 GHz and above), enabling smaller, higher-performing modules for aerospace and defense electronics. Furthermore, the push towards sustainable manufacturing practices and the development of lead-free and conflict-mineral-free dielectric formulations present significant avenues for market differentiation and growth, particularly as environmental regulations tighten globally. The ability of companies to innovate in areas such as ceramic-polymer composites that combine the strengths of both material classes also represents a high-potential market opportunity.

The impact forces influencing the market trajectory are fundamentally technological and economic. The force of technological evolution, specifically the shift toward higher data rates and higher integration density (Moore’s Law applied to passive components), compels continuous material innovation. Economically, the intense pricing pressure exerted by mass-market applications, particularly from large consumer electronics manufacturers, mandates ongoing efficiency improvements and cost reduction in high-volume production. Geopolitical factors related to international trade agreements and tariffs affecting the flow of critical rare earth elements and specialized ceramic powders also represent a strong, pervasive impact force that shapes investment decisions and supply chain resilience strategies across the major manufacturing hubs.

The Dielectric Ceramics Market is primarily segmented based on material type, application, and end-use industry, reflecting the diverse performance requirements and utilization patterns globally. Material segmentation is critical, as different chemical compositions offer distinct dielectric constants and temperature characteristics; for instance, materials like Barium Titanate dominate the capacitor segment due to their high K value, while specialized alumina and silica are preferred for low-loss substrates and microwave applications. Understanding the distribution across these segments is essential for strategic planning, as R&D investment must align with the material properties demanded by high-growth application areas such as high-frequency filtering and power switching in electric vehicles.

Segmentation by application highlights the key functional roles these ceramics play, including energy storage (capacitors), signal processing (resonators, filters), and insulation (substrates). The capacitor segment, particularly MLCCs, holds the largest market share due to their ubiquity across nearly all electronic devices, but the filters and resonators segment is exhibiting the fastest growth due driven by 5G proliferation and the need for precision frequency selection. End-use segmentation clearly indicates that the Electronics & Telecommunications sector is the largest consumer, but the Automotive segment, fueled by the accelerating trend toward electrification and autonomous driving systems, presents the most significant long-term growth opportunity, demanding components that can withstand extreme thermal cycling and mechanical stress.

The value chain for the Dielectric Ceramics Market is intricate, starting from the rigorous sourcing and refining of highly pure raw materials, extending through complex manufacturing processes, and concluding with global distribution to major electronics assemblers. The upstream segment involves the mining and processing of high-purity metal oxides, carbonates, and rare earth elements (e.g., Titanium dioxide, Barium Carbonate). The quality and consistency of these input materials are non-negotiable, as even minor impurities can drastically impair the final dielectric performance. Suppliers must adhere to strict chemical specifications, often involving specialized purification techniques, establishing a strong barrier to entry at this foundational stage.

The midstream process is dominated by specialized ceramic manufacturers who undertake sophisticated tasks such as powder synthesis, green sheet preparation, multilayer stacking, and controlled high-temperature sintering (firing). This stage requires enormous capital investment in precision machinery (tape casting, screen printing, high-temperature kilns) and proprietary know-how to manage shrinkage and minimize internal defects. Key manufacturers often focus on differentiating their products through unique material modifications (doping) and process optimization, moving from standard ceramic processing to highly engineered microelectronic component fabrication. This integration of material science and microelectronics is where the highest value addition occurs.

Downstream activities include the integration of dielectric ceramic components into final electronic products. The distribution channel is bifurcated: direct sales are common for large, specialized components sold to tier-one defense or automotive suppliers, involving long qualification cycles and customized specifications. In contrast, high-volume MLCCs are typically distributed indirectly through a global network of specialized electronic component distributors (e.g., Avnet, Arrow Electronics), who manage complex inventory and logistics for thousands of OEM customers worldwide. The ultimate buyers are system integrators and device manufacturers in sectors like automotive, consumer electronics, and telecommunications, who drive demand based on their product design cycles and market forecasts for end-user devices.

The potential customers for the Dielectric Ceramics Market are highly segmented across industries characterized by high technological complexity and stringent performance requirements for passive electronic components. The primary customer base consists of Original Equipment Manufacturers (OEMs) and Electronic Manufacturing Services (EMS) providers that integrate these ceramics into their final products. The largest volume buyers are those involved in mass production of consumer electronics, such as smartphone and laptop manufacturers, who require billions of MLCCs annually. These customers prioritize cost-efficiency and supply scalability.

A second, highly valuable customer group resides within the Automotive and Aerospace & Defense industries. Automotive electronics suppliers (Tier 1 like Bosch, Continental) purchase ceramics for critical systems such as power inverters, DC-DC converters, battery management units in EVs, and radar modules in ADAS, demanding components that meet rigorous environmental standards (AEC-Q200). Aerospace and Defense contractors (e.g., Lockheed Martin, Raytheon) are niche buyers focused exclusively on high-reliability, radiation-hardened, and hermetically sealed components for satellite communications, avionics, and advanced radar systems, prioritizing performance and longevity over cost.

A third crucial segment includes manufacturers of telecommunications infrastructure, specifically those building 5G base stations, fiber optic networks, and data center equipment. These customers require high-Q dielectric ceramics for filters, resonators, and specialized substrates to ensure minimal signal loss and high bandwidth capacity in demanding operational environments. Furthermore, industrial and medical device manufacturers, producing high-frequency power supplies, MRI machines, and specialized sensors, constitute a growing customer segment requiring ceramics with unique electrical stability and biocompatibility properties.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.85 Billion |

| Market Forecast in 2033 | USD 6.55 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Murata Manufacturing Co., Ltd., TDK Corporation, Samsung Electro-Mechanics (SEMCO), Taiyo Yuden Co., Ltd., Kyocera Corporation, CeramTec GmbH, KEMET (Yageo Corporation), Vishay Intertechnology, Inc., CoorsTek, Inc., Morgan Advanced Materials plc, RAKO Industrial Co., Ltd., CUI Devices, NGK Insulators, Ltd., Rubicon Technology, Inc., APC International, Ltd., Skyworks Solutions, Inc., Knowles Corporation, Littelfuse, Inc., Dielectric Laboratories (Knowles), Materion Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the Dielectric Ceramics Market is characterized by a drive toward higher component density, improved thermal management, and lower overall system costs. A fundamental technological pillar is the Low-Temperature Co-fired Ceramics (LTCC) process, which allows for the integration of multiple passive components, including capacitors, inductors, and resistors, onto a single ceramic substrate. This technology utilizes specialized glass-ceramic materials that can be sintered at relatively low temperatures (around 850°C to 950°C), enabling the co-firing of high-conductivity metal pastes like silver or gold. LTCC is vital for creating compact, highly integrated radio frequency (RF) modules used in wireless communication and radar systems, where low insertion loss and excellent thermal stability are paramount.

Conversely, High-Temperature Co-fired Ceramics (HTCC) technology remains essential for high-power, high-reliability applications where operating temperatures exceed 1000°C. HTCC materials, typically based on alumina or zirconia, are co-fired with high-melting-point metals like tungsten or molybdenum. While offering superior mechanical strength and thermal conductivity, HTCC is more challenging and costly to process. Ongoing research is heavily focused on optimizing ceramic powder synthesis—specifically chemical precipitation and sol-gel methods—to achieve nano-scale particle sizes and highly uniform crystal structures, which directly enhances the dielectric constant and breakdown voltage of the final component while improving yield rates during manufacturing.

Another rapidly advancing area is the application of thin-film deposition techniques and atomic layer deposition (ALD) onto ceramic substrates. These techniques enable the creation of highly precise, ultra-thin dielectric layers (down to a few nanometers thick) for advanced capacitors and integrated passives, pushing the boundaries of capacitance density and operational frequency limits. The continuous evolution of additive manufacturing (3D printing) is also beginning to impact the market, offering potential pathways for producing complex ceramic structures and custom dielectric components without the need for traditional tooling, particularly beneficial for small-volume, highly specialized military or medical applications where customization is crucial.

The global Dielectric Ceramics Market exhibits distinct regional consumption and manufacturing profiles, heavily skewed towards Asia Pacific due to its entrenched position as the world's primary manufacturing base for electronic hardware. APAC, led by nations such as China, Japan, South Korea, and Taiwan, dominates the market both in terms of production volume and component consumption, driven by colossal domestic consumer electronics markets and the presence of major global MLCC and component suppliers. Government initiatives supporting semiconductor manufacturing and 5G network expansion further solidify the region's pivotal role, characterized by high-volume, cost-competitive manufacturing capabilities. Investments in raw material processing and advanced material R&D are intensely focused in this region to meet the surging demand for passive components in both high-end server equipment and mass-market mobile devices.

North America represents a high-value, technology-intensive market, focusing less on mass-market volume and more on specialized, high-reliability applications. Demand here is strongly driven by the stringent requirements of the aerospace and defense sectors, advanced telecommunications infrastructure development, and sophisticated medical technology manufacturing. Companies in this region prioritize innovation in novel ceramic compositions tailored for extreme operating environments and the millimeter-wave spectrum, ensuring performance metrics critical for military radar and satellite communication systems. The emphasis is on quality assurance, component qualification, and research partnerships with academic institutions to maintain technological superiority in high-margin, low-volume segments.

Europe constitutes a mature market with a significant focus on the automotive sector, particularly in Germany and France, due to early adoption and robust manufacturing of Electric Vehicles (EVs) and advanced driver-assistance systems (ADAS). European demand centers on high-power dielectric ceramics for efficient power electronics (inverters and converters) and sensor applications that require excellent thermal stability and reliable operation under harsh road conditions. Furthermore, Europe is a key area for industrial electronics and renewable energy infrastructure, driving demand for high-voltage ceramic insulators and components used in efficient energy transmission and distribution systems. Market growth is increasingly influenced by strict EU directives regarding material safety and sustainability, favoring companies that innovate in lead-free and eco-friendly ceramic formulations.

The primary driver for Barium Titanate (BaTiO3) demand is its high dielectric constant (high K), making it the essential material for manufacturing Multilayer Ceramic Capacitors (MLCCs). MLCCs are ubiquitous in electronic devices due to their ability to store significant energy in minimal physical space, critical for device miniaturization in smartphones, automotive systems, and IoT devices.

The 5G rollout mandates components that can operate efficiently at higher frequencies (millimeter-wave range) with minimal signal loss. This drives demand for Ultra-Low Loss (ULL) dielectric ceramics, such as specialized alumina and complex titanates, which are crucial for constructing high-Q filters, resonators, and LTCC substrates used in 5G base stations and advanced antenna systems to maintain signal integrity.

Crucial technological advancements include the development of nano-sized ceramic powders for enhanced material uniformity, the integration of AI/ML for accelerating material discovery and optimizing complex sintering processes, and the implementation of thin-film deposition techniques to achieve extremely high capacitance density and component integration on substrates.

The Automotive sector, specifically the Electric Vehicle (EV) and Hybrid Electric Vehicle (HEV) segments, is projected to exhibit the fastest growth. EVs require high-power density ceramic components for critical applications such as power inverters, DC-DC converters, and battery management systems, demanding materials with exceptional thermal stability and high breakdown voltage capabilities.

The main challenge is maintaining stringent quality control and consistency at the micro-level across billions of components, particularly regarding controlling the thickness and uniformity of ultra-thin ceramic layers and preventing microscopic defects (voids or cracks) during the complex co-firing process, which directly impacts the component’s reliability and yield rate.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.