ID : MRU_ 434909 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

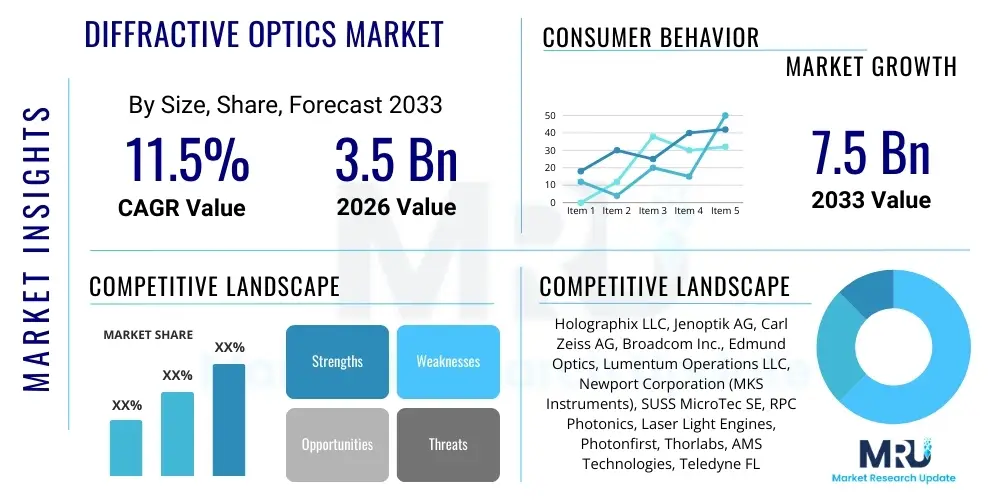

The Diffractive Optics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at $3.5 Billion in 2026 and is projected to reach $7.5 Billion by the end of the forecast period in 2033.

The Diffractive Optics Market encompasses the technology and products utilizing micro-structured surfaces or volume variations to manipulate light through diffraction, offering superior performance characteristics compared to traditional refractive optics. Diffractive Optical Elements (DOEs) are crucial for shaping laser beams, splitting optical power, and correcting chromatic aberrations, enabling miniaturization and enhanced functionality across diverse systems. Key products include diffractive gratings, beam shapers, and homogenizers, fabricated using advanced techniques like photolithography, nanoimprinting, and diamond turning, tailored for specific wavelength ranges and power handling capabilities.

Major applications driving this market expansion include advanced 3D sensing in consumer electronics (smartphones and AR/VR devices), sophisticated medical imaging (OCT, endoscopy), high-speed fiber optic telecommunications, and industrial laser processing systems. The inherent advantages of DOEs, such as reduced component thickness, lower weight, and the capacity to integrate multiple functions onto a single surface, position them as indispensable components in the next generation of compact optical systems. Furthermore, the rising demand for high-efficiency beam delivery systems in high-power industrial lasers significantly contributes to market growth.

The market benefits from several strong driving factors, predominantly the escalating investment in augmented reality (AR) and virtual reality (VR) technologies, which rely heavily on lightweight, high-performance diffractive wave guides for display elements. Additionally, the proliferation of Light Detection and Ranging (LiDAR) systems in autonomous vehicles and robotics necessitates custom DOEs for precise beam steering and pattern generation. Continuous advancements in manufacturing processes, particularly the shift toward mass production techniques for polymer-based DOEs, are further lowering costs and broadening the accessibility of this technology across various volume-sensitive industries.

The Diffractive Optics Market is experiencing rapid expansion, fueled by robust business trends centered on miniaturization and the integration of smart optical functionalities into consumer devices. Key business growth vectors include the development of wafer-level optics (WLO) manufacturing processes, enabling high-volume, cost-effective production of DOEs for 3D sensing modules. Strategic collaborations between material science firms and semiconductor foundries are accelerating innovation, particularly in high-refractive-index materials necessary for efficient deep UV and near-infrared applications. Furthermore, the trend toward customizing beam profiles for specific industrial and medical laser applications ensures sustained high-value revenue streams for specialized manufacturers.

Regionally, the market exhibits strong dynamism, with Asia Pacific (APAC) dominating both in terms of manufacturing capacity and consumption, primarily driven by the colossal consumer electronics manufacturing base located in China, South Korea, and Taiwan. North America and Europe maintain significant market share, largely due to high adoption rates in advanced medical devices, defense, and aerospace sectors, focusing on research and development of highly specialized and expensive DOEs made from materials like fused silica. Emerging markets in Latin America and MEA are showing promising growth, albeit from a smaller base, driven by increasing investment in telecommunications infrastructure and industrial automation projects.

Segment trends highlight the dominance of Surface Relief Gratings due to their versatility and ease of mass production, especially in the consumer electronics segment. However, Volume Holographic Gratings are gaining traction in demanding high-fidelity applications like holographic displays and complex spectroscopy. In terms of material, Fused Silica remains critical for high-power laser applications requiring extreme thermal stability, while polymers and plastics are revolutionizing the consumer segment by offering low-cost, disposable, or high-volume solutions. Application-wise, Consumer Electronics, particularly 3D sensing components, represent the fastest-growing segment, closely followed by the high-precision demands of the Healthcare sector.

Common user inquiries regarding the intersection of Artificial Intelligence (AI) and the Diffractive Optics Market often revolve around how AI can optimize DOE design, enhance manufacturing efficiency, and enable new applications in sensing and imaging. Users frequently ask if AI-driven simulation tools can replace traditional iterative design processes, the potential for machine learning algorithms to detect and correct manufacturing defects in real-time, and the role of DOEs as key hardware enablers for next-generation AI vision systems. Key concerns center on the computational complexity required for optimizing nanoscale optical structures and the potential disruption to traditional optical engineering roles.

The analysis reveals that AI is fundamentally transforming the R&D cycle for diffractive optics. Generative design algorithms, powered by deep learning, are enabling engineers to explore vast parameter spaces far beyond human capability, leading to the rapid creation of ultra-compact and highly efficient DOEs (such as metalenses) tailored for specific spectral responses or beam shaping requirements. This shift reduces the time-to-market for complex optical components, making customized DOEs more accessible. Furthermore, machine learning models are being deployed in manufacturing facilities to monitor lithography processes, predicting yield failures based on subtle variations in etching or coating, thereby significantly improving overall production throughput and quality control.

In application domains, Diffractive Optics are essential components for AI-enabled hardware. For instance, in edge computing vision systems and autonomous vehicles, DOEs are used for structured illumination and efficient light collection, providing the necessary high-fidelity data input for complex AI processing algorithms (e.g., depth estimation, object recognition). AI optimization of the optical system itself, leveraging DOEs to pre-process light signals (e.g., optical computing) before they hit the sensor, can reduce the computational load downstream, making real-time AI processing faster and more energy-efficient, particularly critical for battery-operated devices like AR/VR headsets.

The Diffractive Optics Market is significantly influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), which collectively shape the competitive landscape and technological trajectory. The primary drivers include the exponential demand for compact optical modules in consumer electronics, the widespread adoption of 3D sensing technologies (LiDAR, structured light) across various sectors, and the inherent advantages of DOEs in reducing system complexity and weight. However, the market faces notable restraints, chiefly the high initial investment cost associated with advanced nano-fabrication equipment (e.g., E-beam lithography) and the complexity involved in achieving high-volume production with consistently tight tolerance levels for certain materials.

Opportunities for growth are abundant, particularly in the emerging fields of holographic displays, advanced biomedical diagnostics, and the ongoing development of meta-surfaces which represent an evolutionary step beyond traditional diffractive optics. Furthermore, increasing governmental investment in defense and aerospace applications, particularly for advanced tracking and surveillance systems, provides a high-margin opportunity segment. The key impact forces dictating the market's direction are technological innovation, driven by R&D in new materials and scalable manufacturing methods, and intense competition among key players focused on achieving economies of scale and intellectual property dominance in critical application areas like AR/VR wave guides.

The market also faces external impact forces related to supply chain resilience, especially concerning specialized raw materials and processing chemicals. Regulatory standards, particularly in the medical and defense sectors, impose stringent quality and reliability requirements, acting as both a barrier to entry for new players and a quality benchmark for established manufacturers. Ultimately, the rapid pace of technological obsolescence in related fields, such as smartphone camera technology and display development, compels continuous innovation in DOE design to maintain market relevance and competitive advantage.

The Diffractive Optics Market is segmented based on critical technical and application criteria, offering a granular view of market dynamics and growth pockets. The segmentation highlights the diversity in fabrication methods, materials utilized, and the vast range of end-user industries benefiting from these specialized components. Understanding these segments is crucial for strategic planning, resource allocation, and identifying specific high-growth niches, especially as manufacturing capabilities for novel materials and complex geometries evolve.

The value chain for the Diffractive Optics Market is complex, beginning with upstream analysis focused on the provision of highly specialized raw materials such as ultra-pure fused silica, high-index glasses, and photopolymer resins. Key upstream activities involve advanced material synthesis and substrate preparation, which are critical as the quality and defect rate of the substrate directly impact the performance and yield of the final DOE. Suppliers in this segment require stringent quality control and substantial R&D capability to meet the optical purity and homogeneity demands of the downstream fabrication process. Competition upstream is relatively concentrated among specialized chemical and glass manufacturers.

Midstream activities encompass the sophisticated manufacturing and processing stages, including mask design, lithography (e.g., DUV, E-beam), etching, coating, and quality inspection. This stage is capital-intensive, dominated by highly specialized manufacturers who possess the necessary cleanroom infrastructure and proprietary processing know-how. Direct distribution channels are often preferred for high-value, custom DOEs destined for defense or scientific research, involving direct sales teams and application engineers working closely with the end-users. Conversely, indirect channels, utilizing distributors and value-added resellers (VARs), are more prevalent for standardized or high-volume polymer-based DOEs sold into the consumer electronics supply chain.

Downstream analysis centers on integration and end-use application. System integrators and Original Equipment Manufacturers (OEMs) purchase DOEs to incorporate them into finished products like LiDAR modules, medical diagnostic devices, or smartphone camera arrays. The close integration required necessitates strong technical support and long-term contracts between DOE manufacturers and Tier 1 OEMs. The growth of the market is strongly dictated by the purchasing power and design cycles of major downstream players in the consumer electronics and automotive industries. This structure emphasizes the need for speed, scalability, and precise alignment throughout the entire value chain to minimize losses and maximize efficiency.

The primary end-users and buyers of Diffractive Optics are diverse, spanning major industrial sectors that require precise light manipulation and advanced sensing capabilities. Key customers include large Consumer Electronics OEMs, such as smartphone and wearable technology manufacturers (Apple, Samsung, Huawei), who integrate DOEs for vertical-cavity surface-emitting laser (VCSEL) beam shaping in 3D facial recognition systems and proximity sensors. The rapid adoption of augmented and virtual reality devices means headset manufacturers (Meta, HTC, Sony) are also major consumers, relying on DOEs for compact and highly efficient display projection.

The Healthcare sector represents a high-value customer base, including manufacturers of advanced medical imaging equipment (e.g., Carl Zeiss Meditec, Bausch & Lomb) utilizing DOEs in Optical Coherence Tomography (OCT) systems and high-precision laser surgical devices. Furthermore, the Industrial sector, encompassing providers of laser material processing equipment (e.g., Trumpf, Coherent) and inspection systems, relies on beam homogenizers and splitters to ensure uniform power distribution and high throughput. Finally, governmental and defense contractors procure specialized, high-reliability DOEs for secure communications, targeting systems, and advanced satellite imaging applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $3.5 Billion |

| Market Forecast in 2033 | $7.5 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Holographix LLC, Jenoptik AG, Carl Zeiss AG, Broadcom Inc., Edmund Optics, Lumentum Operations LLC, Newport Corporation (MKS Instruments), SUSS MicroTec SE, RPC Photonics, Laser Light Engines, Photonfirst, Thorlabs, AMS Technologies, Teledyne FLIR, Tinsley Laboratories, OptoSigma Corporation, Headwall Photonics, II-VI Incorporated (Coherent), Horiba, Wasatch Photonics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Diffractive Optics Market is underpinned by several cutting-edge fabrication and design technologies crucial for producing high-quality, complex optical structures. Photolithography remains a foundational technology, particularly deep UV (DUV) lithography, used extensively for defining the micro-patterns in high-volume production, especially for semiconductor-grade diffractive elements. Complementing this is Electron Beam (E-beam) Lithography, which offers superior resolution for features down to the sub-100 nanometer scale, essential for prototyping and producing master elements with exceptionally tight tolerances and complex, non-periodic structures required by advanced applications like holographic displays and meta-surfaces.

The rising focus on cost efficiency and scalability has popularized replication technologies, primarily Nanoimprint Lithography (NIL) and injection molding, especially for plastic and polymer DOEs targeted at consumer electronics. NIL allows for the cost-effective mass production of intricate surface relief structures by pressing a rigid master mold into a curable material, drastically reducing the cost per unit compared to lithography and etching. Furthermore, diamond turning is employed for manufacturing high-quality, continuous surface profile DOEs, suitable for large-aperture optics and specialized industrial systems where material constraints are less flexible.

A significant technological advancement shaping the market landscape is the shift towards metasurfaces and metalenses. These components leverage subwavelength periodic structures to manipulate light in ways traditional optics cannot, offering ultra-thin form factors. Research in this area focuses on developing new high-index dielectric materials (e.g., titanium dioxide, gallium nitride) and optimizing their architecture using inverse design techniques. This technological evolution promises to further shrink optical modules, which is the primary enabler for future AR/VR integration and high-resolution compact cameras, indicating a strong future trend toward merging diffractive and refractive principles at the nanoscale.

The Diffractive Optics Market exhibits distinct regional dynamics driven by unique technological adoption rates, industrial infrastructure, and governmental policies. North America is characterized by robust investment in research and development, particularly in defense, aerospace, and advanced medical diagnostics. The region hosts numerous cutting-edge startups and established firms focusing on high-precision, low-volume DOEs made from fused silica and exotic materials. Demand in the US is strongly tied to the development of sophisticated LiDAR systems for autonomous driving and advanced optical payload systems for space applications, sustaining a market focused on performance over absolute cost.

Europe demonstrates significant strength in the industrial and telecommunications sectors. Countries like Germany and the UK lead in the deployment of high-power industrial laser systems for cutting and welding, where efficient beam homogenization provided by DOEs is critical. Furthermore, Europe is a hub for high-quality optical component manufacturing, emphasizing standardized, reliable components for machine vision and metrology applications. The market growth here is steady, supported by strong institutional frameworks and established industrial automation industries that demand consistent optical reliability.

Asia Pacific (APAC) dominates the market share, propelled by massive manufacturing capabilities and consumer electronics demand, primarily stemming from China, Japan, and South Korea. This region specializes in high-volume, cost-sensitive production of polymer and plastic DOEs utilized extensively in smartphone 3D sensing modules, cameras, and emerging mass-market AR devices. Investment in APAC is heavily skewed toward scaling up Nanoimprint Lithography and wafer-level optics technologies to achieve unprecedented levels of efficiency and miniaturization. The competitive environment in APAC is intense, focused on rapid innovation cycles and low unit costs.

Latin America (LATAM) and the Middle East and Africa (MEA) currently hold smaller market shares but are projected to experience accelerated growth. Growth in LATAM is linked to expanding telecommunications infrastructure and localized industrial automation initiatives. In MEA, particularly the GCC countries, increasing governmental expenditure on defense modernization, security surveillance systems, and diversified industrial base development is driving the demand for specialized diffractive components, albeit through imports from established global players.

The primary factor driving market growth is the explosive adoption of 3D sensing technology, particularly in consumer electronics (facial recognition, depth sensing) and automotive LiDAR systems. Diffractive Optical Elements enable the compact, efficient beam shaping necessary for these mass-market applications.

DOEs are crucial in AR waveguides, allowing for the efficient injection and extraction of light into the thin display glass. They enable the creation of compact, lightweight, and high-fidelity display systems that are essential for comfortable and unobtrusive AR glasses and headsets.

Nanoimprint Lithography (NIL) and associated replication techniques (like injection molding for polymers) are the most critical manufacturing technologies for high-volume, low-cost production, especially for consumer electronics applications requiring millions of units quickly and affordably.

Surface Relief Gratings (SRGs) manipulate light via patterns etched onto a surface and are favored for high-volume production. Volume Holographic Gratings (VHGs) utilize refractive index variations within the bulk material, offering high diffraction efficiency and often preferred for complex holographic displays and specialized spectral filtering.

Metasurfaces, or Metalenses, represent the next generation of diffractive optics. They use subwavelength structures to achieve optical functions (like focusing or spectral filtering) in an extremely thin layer, promising significant further miniaturization and enhanced performance crucial for mobile devices and advanced imaging systems.

Yes, the military and defense sector is a significant, high-value end-user. DOEs are used in critical applications such as secure free-space communication, advanced target illumination, thermal imaging systems, and sophisticated airborne and satellite surveillance optics where reliability and performance in harsh environments are paramount.

For high-power laser applications, materials with high damage thresholds and excellent thermal stability are essential, primarily fused silica and specialized glass substrates. These materials prevent thermal distortion and ensure operational longevity under intense optical flux.

In telecommunications, DOEs are utilized for wavelength division multiplexing (WDM) systems, fiber coupling efficiency improvement, and beam expansion/collimation in data centers and long-haul networks, enabling higher bandwidth and better signal integrity.

Yes, due to the incredibly small feature sizes (nanometers), manufacturing defects such as line edge roughness, pattern distortions, and etching variations are common challenges. This necessitates advanced cleanroom environments and stringent AI-assisted quality control measures to maintain high yields.

Hybrid DOEs combine both diffractive and refractive optical functions within a single component or system. This integration allows engineers to leverage the chromatic aberration correction of DOEs with the power of refractive lenses, leading to superior overall optical system performance, often in a more compact form.

Wafer-Level Optics (WLO) is a manufacturing process that enables the parallel fabrication of thousands of optical elements (including DOEs) simultaneously on a single wafer. This method drastically reduces manufacturing costs and component size, making it transformative for the high-volume consumer electronics sector.

Autonomous vehicles rely heavily on LiDAR systems for environmental mapping. DOEs are essential in these systems for complex beam shaping, steering, and pattern projection, directly linking the growth of the autonomous vehicle market to increased demand for high-performance, robust diffractive optics.

E-beam lithography provides the highest resolution capability for defining complex, non-periodic nanoscale structures. It is primarily used for rapid prototyping, developing master molds for replication techniques, and fabricating cutting-edge metasurface components where feature precision is paramount.

The Asia Pacific (APAC) region holds the largest consumption share, overwhelmingly driven by the massive electronics manufacturing and assembly base, particularly in China and South Korea, which integrates DOEs into billions of consumer devices annually.

Restraints include the high cost of highly specialized custom DOEs, challenges related to managing stray light or zero-order light in certain designs, and the inherent difficulty in maintaining performance consistency across very broad spectral bands compared to some traditional refractive systems.

In Optical Coherence Tomography (OCT), DOEs are used to precisely split the light beam into reference and sample arms or to shape the probe beam profile. This improves the efficiency and resolution of the imaging process, enabling better non-invasive diagnostic capabilities for ophthalmology and dermatology.

Upstream challenges involve securing a reliable supply of highly pure, defect-free optical substrates (like fused silica) and specialized photoresists and chemicals. Material inconsistencies at the substrate level can lead to significant yield losses further down the manufacturing line.

While DOEs offer significant advantages in size and weight, a complete replacement is uncommon. The prevailing trend is towards hybrid optical systems, where DOEs are used synergistically with refractive elements to correct specific aberrations (like chromaticity) and reduce the overall component count and thickness.

For applications requiring high-temperature or extreme environment stability (e.g., aerospace, certain industrial lasers), DOEs are typically fabricated using robust materials such as fused silica or silicon, which offer low coefficients of thermal expansion and high laser damage thresholds.

The main advantage is the ability of DOEs to precisely redistribute a laser beam's energy into a defined, uniform spot (top-hat profile) with high efficiency. This is crucial for consistent material processing and micro-machining, where highly uniform irradiance is required.

The Consumer Electronics segment, driven specifically by the integration of 3D sensing in mobile devices and the proliferation of AR/VR headsets utilizing compact display wave guides, is anticipated to record the fastest Compound Annual Growth Rate.

Patents and intellectual property (IP) are crucial competitive assets, especially concerning complex metasurface designs and high-throughput replication techniques. Companies with strong IP portfolios in specific beam shaping or AR waveguide technologies hold significant leverage and market dominance.

Customers prioritize diffraction efficiency, feature size tolerance, laser damage threshold, spectral bandwidth of operation, and overall cost per unit, depending on whether the application is high-performance scientific or high-volume consumer.

Plastic/polymer DOEs are forecast to experience the highest volume growth due to their low cost and suitability for consumer applications. However, glass/silica DOEs will maintain strong revenue growth in high-value, high-performance niches like defense, industrial processing, and scientific instrumentation.

AI, specifically machine learning and computer vision, is used to analyze high-resolution images of manufactured DOEs in real-time to detect minute nanoscale defects, classify them, and adjust fabrication parameters automatically, drastically improving quality control and production yields.

Hybrid DOEs pose significant design challenges due to the need for optimization across both refractive and diffractive parameters, often requiring specialized inverse design algorithms and extensive electromagnetic simulations to ensure the complex structure performs correctly across the required fields of view and wavelengths.

The medical imaging sector is high-value because it demands ultra-precision, high resolution, and strict regulatory compliance. DOEs enable compact, superior image quality in devices like surgical microscopes and advanced diagnostics, justifying the higher cost associated with specialized, low-volume components.

Zero-order light refers to the portion of the incident light that passes straight through the DOE without being diffracted. Minimizing zero-order light is crucial for maximizing diffraction efficiency and maintaining high contrast in the intended diffracted pattern, especially in display and sensing applications.

Manufacturing large-area DOEs (e.g., for large astronomical telescopes or display screens) is technically feasible but challenging and costly, requiring large-format lithography tools and highly stable environments. Specialized manufacturing techniques like diamond turning or mosaic assembly are often employed for these applications.

The semiconductor industry plays a vital role as it supplies the necessary advanced lithography equipment (e.g., DUV scanners), etching processes, and cleanroom protocols that are adapted and essential for the nanoscale fabrication of high-performance diffractive elements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.