ID : MRU_ 432554 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

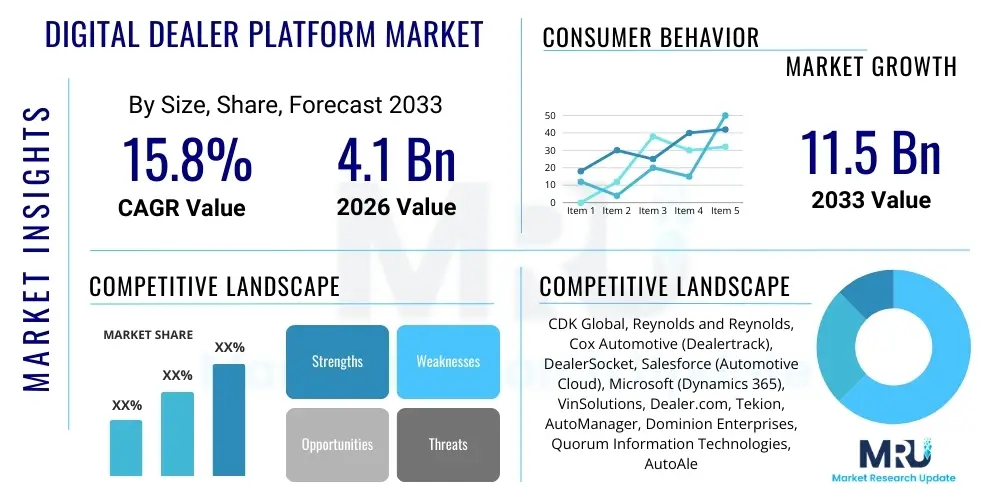

The Digital Dealer Platform Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 4.1 Billion in 2026 and is projected to reach USD 11.5 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the accelerating digitalization of automotive retail processes, consumer demand for seamless omnichannel experiences, and the necessity for dealerships to optimize operational efficiency and manage complex inventory streams in real-time. The shift from traditional sales models to integrated digital ecosystems, encompassing lead management, financing, and service scheduling, fundamentally underpins this expansion.

The valuation reflects a significant investment spike in cloud-based solutions and advanced data analytics capabilities, crucial for transforming how dealers interact with prospective buyers. Market growth is further amplified by small and medium-sized dealerships recognizing the competitive imperative of adopting advanced platform technologies to maintain market relevance and improve Customer Lifetime Value (CLV). Geographically, mature automotive markets in North America and Europe currently dominate the revenue share, though emerging markets in Asia Pacific are expected to witness the highest incremental growth due to rapid urbanization and increasing consumer affluence supporting vehicle purchases.

The Digital Dealer Platform Market encompasses sophisticated software solutions and integrated ecosystems designed specifically for automotive dealerships to manage core business operations across the entire customer journey, from initial inquiry to vehicle maintenance. These platforms serve as the central nervous system for dealerships, consolidating data and functionalities previously spread across disparate systems, including Customer Relationship Management (CRM), Dealer Management Systems (DMS), inventory synchronization tools, digital retailing interfaces, and integrated financing modules. The primary objective of these platforms is to facilitate an end-to-end, seamless, and personalized car buying experience, catering to the modern consumer's preference for researching, initiating, and often concluding vehicle transactions online.

Major applications of Digital Dealer Platforms include streamlined inventory management across multiple physical and digital locations, advanced lead generation and nurturing via digital marketing tools, efficient workflow automation for sales and service departments, and enhanced data analytics for predictive demand forecasting and personalized customer engagement strategies. The integrated nature of these platforms significantly reduces operational friction, improves data accuracy, and ensures compliance with increasingly stringent regional data privacy regulations. Furthermore, they are pivotal in optimizing used car valuation and trade-in processes through rapid, data-driven assessment tools, accelerating the sales cycle and maximizing profitability per transaction.

Key driving factors propelling the market include the irreversible trend towards automotive e-commerce, where consumers expect full transaction transparency and remote capabilities; the necessity for competitive differentiation through superior customer service; and the pressure on dealerships to achieve economies of scale by automating repetitive administrative tasks. The platforms deliver significant benefits such as increased sales conversion rates, reduced operating costs, improved employee productivity, and a quantifiable boost in customer satisfaction scores, making them indispensable investments for modern automotive retail enterprises aiming for sustainable growth and operational resilience in a volatile economic landscape.

The Digital Dealer Platform Market is characterized by intense innovation driven by business trends prioritizing omnichannel integration and hyper-personalization of the automotive purchasing process. Current business trends indicate a strong move toward platform consolidation, where dealerships prefer unified solutions offering modules for marketing, sales, F&I (Finance and Insurance), and after-sales service, rather than managing multiple single-function vendors. This consolidation is pushing solution providers to enhance their API ecosystems and integrate advanced analytics engines capable of deriving actionable insights from vast amounts of consumer behavior and inventory data. Significant investment is being channeled into refining the digital showroom experience, leveraging high-fidelity visuals and virtual reality (VR) tours to bridge the physical and digital retailing gaps effectively. Furthermore, the rising popularity of subscription-based vehicle ownership models is necessitating platform updates to manage recurring revenue streams and complex fleet logistics efficiently.

Regionally, North America maintains its leadership due to high technological readiness, stringent regulatory environments encouraging digital transparency, and significant early adoption of cloud-based DMS and CRM systems among large dealer groups. Europe, characterized by diverse national markets and high consumer expectation regarding data privacy (GDPR), shows strong growth in platforms specializing in secure, transparent transaction processing and compliance management. Asia Pacific (APAC) is emerging as the fastest-growing region, fueled by massive market volumes in China and India, escalating smartphone penetration rates among consumers, and government initiatives promoting digitalization in the retail sector. Investments in localized content and language support are critical success factors for vendors operating across the diverse APAC landscape.

Segment trends highlight the dominance of cloud-based deployment models due to their scalability, lower Total Cost of Ownership (TCO), and rapid implementation cycles compared to legacy on-premise systems. Functionality-wise, the Digital Retailing segment is witnessing explosive growth as dealers race to offer end-to-end digital transaction capabilities, including remote documentation signing and home delivery scheduling. Large dealer groups (Enterprise segment) represent the highest revenue capture, demanding highly customized, integrated solutions, while Small and Medium Dealers (SMDs) are increasingly adopting modular, Software-as-a-Service (SaaS) offerings that provide essential functionality without prohibitive capital expenditure, thus democratizing access to high-end digital tools.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Digital Dealer Platform Market frequently revolve around optimizing customer interaction, improving predictive analytics accuracy, and enhancing operational efficiency. Common user questions include: "How can AI personalize the car buying journey better than current systems?", "What role does Machine Learning play in dynamic pricing and inventory forecasting?", "Will AI automate sales roles, and how can platforms ensure lead quality using AI?", and "What are the ethical implications of using AI in automotive financing and recommendation engines?" Based on these themes, key user concerns center on the tangible return on investment (ROI) from AI implementation, the complexity of integrating advanced algorithms into existing DMS/CRM infrastructure, and ensuring that AI-driven personalization respects customer data privacy while delivering meaningful, relevant vehicle recommendations and service reminders. Expectations are high regarding AI's ability to drive significant competitive advantages, particularly in areas requiring complex data analysis, such as identifying fraud risks and predicting vehicle servicing needs before component failure.

AI is fundamentally transforming the DDP market by embedding intelligence into every module, moving beyond basic automation to true predictive and prescriptive capabilities. AI-powered chatbots and virtual sales assistants handle initial qualification and repetitive inquiries 24/7, freeing up human staff for complex sales negotiations. Machine learning models analyze historical sales data, web traffic patterns, and external economic indicators to provide dynamic pricing recommendations, ensuring inventory competitiveness and maximizing margin potential. Furthermore, sophisticated algorithms are used for enhanced F&I product recommendations tailored precisely to individual buyer risk profiles and historical preferences, improving both penetration rates and compliance adherence. This shift elevates the platform from a management tool to a strategic intelligence hub, offering dealers unprecedented foresight into market shifts and consumer demands.

The Digital Dealer Platform Market is shaped by a powerful confluence of drivers and restraining factors, alongside compelling opportunities that dictate its future growth trajectory. The principal drivers include the pervasive consumer shift toward conducting vehicle research and purchasing transactions online, demanding end-to-end digital retailing capabilities from dealerships. Furthermore, the intense competitive pressure within the automotive retail landscape mandates the adoption of advanced platforms to reduce operational inefficiencies, streamline complex regulatory compliance procedures, and gain a holistic, data-driven view of the customer lifecycle. The rapid expansion of connected vehicle technology also acts as a major driver, generating vast amounts of data that DDPs must integrate and analyze to enable proactive service offerings and personalized marketing.

Conversely, significant restraints hinder market acceleration, most notably the high initial implementation costs and the complexity associated with integrating new digital platforms with often outdated legacy Dealer Management Systems (DMS) still operational in many smaller dealerships. Concerns regarding data security and privacy remain paramount, particularly in regions with strict regulations, requiring vendors to invest heavily in robust cybersecurity measures, which increases the overall platform cost. Furthermore, resistance to technological change among long-tenured dealership staff and the associated steep learning curve often necessitate substantial training investments, presenting a practical barrier to rapid, large-scale adoption, particularly among independent dealers.

Opportunities for market growth are abundant, primarily revolving around the expansion of AI and Machine Learning capabilities to unlock deeper predictive insights for inventory management, financing risk assessment, and customer churn reduction. The untapped potential in the used car market, requiring sophisticated digital platforms for rapid valuation, certification, and listing across multiple channels, presents a substantial revenue stream. Additionally, the proliferation of electric vehicles (EVs) and hybrid models necessitates specialized platform features for managing battery health data, charging infrastructure integration, and unique maintenance schedules, offering DDP providers a fertile area for product differentiation and specialized segment growth, particularly in emerging economies where EV adoption is projected to soar dramatically post-2025.

The Digital Dealer Platform Market is meticulously segmented based on Deployment Model, Application, and Dealer Size, reflecting the diverse operational needs and technological maturity across the global automotive retail industry. Understanding these segmentations is critical for vendors to tailor their offerings, pricing structures, and go-to-market strategies effectively. The deployment split between Cloud-based (SaaS) and On-premise solutions highlights the ongoing migration away from traditional server-dependent infrastructure, favoring the flexibility and scalability offered by the cloud. Application segmentation reveals the crucial functional areas where dealers seek immediate digital transformation benefits, ranging from core ERP functions (DMS) to strategic customer engagement tools (CRM/Marketing) and vital financial services (F&I). Finally, segmentation by dealer size determines the necessary complexity, integration depth, and pricing models required, distinguishing the needs of massive multinational dealer groups from those of independent or small regional dealerships.

Cloud-based solutions dominate the growth trajectory due to lower upfront capital requirements and the ability to receive continuous, seamless software updates, ensuring compliance and access to the latest security protocols and feature enhancements. Within the application segment, the rise of true digital retailing modules, enabling customers to complete the entire transaction—including valuation, credit checks, and documentation—online, is generating the largest revenue contribution growth. For dealer size, the large dealer group segment drives the highest overall value, often requiring comprehensive, highly integrated platforms that can manage complex multi-franchise, multi-location operations, while the small and medium dealer segment is characterized by rapid adoption rates of simplified, affordable subscription-based platforms that streamline essential operations like inventory syndication and basic lead management, offering scalability as their businesses grow.

The value chain for the Digital Dealer Platform Market commences with Upstream Activities involving software development and intellectual property creation, where technology providers focus on R&D for AI, cloud architecture, data security, and specialized automotive retail APIs. This stage requires significant investment in data scientists, cloud engineers, and automotive domain experts to build robust, scalable, and compliant software modules. Key upstream components include core database infrastructure, advanced analytics engines, and third-party integrations with vehicle manufacturers' data feeds (OEM systems) and major financial institutions for real-time credit application processing. Strategic alliances and partnerships at this stage are crucial for vendors to acquire specialized technologies, such as advanced fraud detection algorithms or sophisticated geospatial mapping tools necessary for logistics management.

Moving through the value chain, the Midstream involves the crucial activities of platform integration, customization, and implementation. Given the variability in dealership operations and legacy systems, professional services related to configuring the platform—including data migration from old DMS systems, workflow optimization, and employee training—represent a significant portion of the total project value. Distribution channels are generally categorized into Direct and Indirect methods. Direct distribution involves platform vendors selling and servicing the software directly to large dealer groups, offering highly customized enterprise contracts and dedicated support teams. Indirect distribution relies heavily on channel partners, Value-Added Resellers (VARs), and system integrators who market modular solutions, particularly to the SMD segment, often bundling the software with local support and specialized hardware if required.

The Downstream segment focuses on deployment, ongoing support, and continuous feature enhancement. Post-implementation support, including managed services, help desk assistance, and software updates (especially critical for compliance and security patches), ensures customer satisfaction and high renewal rates. The effectiveness of the DDP is directly tied to the quality of the technical support and the vendor's ability to quickly adapt the platform to evolving market demands, such as new vehicle models, regulatory shifts, or emerging digital marketing channels. This phase emphasizes high availability, rapid response times, and proactive monitoring to ensure the platform remains the reliable operational backbone of the dealership, maximizing the dealer's ongoing ROI from the technology investment.

The primary End-Users or Buyers of Digital Dealer Platforms are diverse entities within the automotive ecosystem, centrally encompassing franchised new vehicle dealerships and large, independent used vehicle superstores. These entities require comprehensive platforms to manage their high-volume sales processes, extensive inventory portfolios, and complex customer service schedules. Franchised dealerships, often representing multiple Original Equipment Manufacturers (OEMs), specifically require platforms that can integrate seamlessly with proprietary OEM interfaces for parts ordering, warranty claims processing, and vehicle recall tracking, necessitating specialized compliance modules within the DDP suite. Their purchasing decisions are driven by the need for operational synergy between their sales, F&I, and service departments.

A second significant customer segment includes large automotive dealer groups and enterprise chains operating across multiple regions or countries. These customers demand highly scalable, centralized DDP solutions that offer consolidated reporting, standardized operational protocols across all locations, and specialized tools for inter-dealership inventory transfers and centralized marketing campaign management. For these enterprise clients, features like robust multi-currency and multi-language support, alongside sophisticated security architecture, are non-negotiable requirements. The procurement cycle for this segment is typically longer, involving complex RFP processes and proof-of-concept stages to ensure the platform meets their extensive, customized needs.

Finally, niche segments such as specialized commercial fleet operators, rental car agencies managing large fleets, and even large service and parts distributors are emerging as potential customers. Although their needs are less focused on consumer sales transactions, they require DDP elements like advanced inventory tracking, automated fleet maintenance scheduling, and sophisticated parts management modules to optimize their asset utilization and minimize vehicle downtime. The increasing sophistication of the DDP market is enabling vendors to create specialized, modular solutions that cater to the unique logistics and lifecycle management requirements of these B2B-focused end-users, expanding the overall addressable market beyond traditional consumer dealerships and offering substantial growth opportunities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 11.5 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | CDK Global, Reynolds and Reynolds, Cox Automotive (Dealertrack), DealerSocket, Salesforce (Automotive Cloud), Microsoft (Dynamics 365), VinSolutions, Dealer.com, Tekion, AutoManager, Dominion Enterprises, Quorum Information Technologies, AutoAlert, Dealer Inspire, Snap-on Business Solutions, Xtime, PureCars, Serti, Autosoft, NetLook |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological backbone of the Digital Dealer Platform Market is rapidly evolving, moving away from monolithic, proprietary software toward flexible, API-driven, and highly scalable cloud architectures. Core technology involves the widespread adoption of multi-tenant, microservices-based cloud platforms (primarily AWS, Azure, and Google Cloud Platform) which enable vendors to offer Software-as-a-Service (SaaS) models with superior uptime and faster deployment cycles. Critical technological requirements include robust data integration frameworks that utilize standardized APIs (such as those for Vehicle Identification Number – VIN decoding and OEM data synchronization) to ensure seamless flow of information between a dealership’s internal systems and external market data sources, including third-party listing sites and consumer credit bureaus. This shift facilitates real-time data synchronization, which is paramount for maintaining accurate inventory listings and instant F&I approval processes.

A second major technological trend is the deep integration of Artificial Intelligence (AI) and Machine Learning (ML) across all platform modules. Key AI implementations include natural language processing (NLP) for advanced sentiment analysis of customer communications, predictive modeling for demand forecasting, and computer vision technologies deployed for automated vehicle photography processing and damage assessment during trade-in evaluations. Furthermore, the adoption of blockchain technology is beginning to gain traction, particularly in applications related to secure digital document transfer, verifiable vehicle history reports, and transparent financing contracts, offering enhanced security and reducing the potential for fraud, though its implementation remains nascent compared to established cloud and AI technologies.

Crucially, the user interface (UI) and user experience (UX) are being prioritized through the implementation of responsive design frameworks and mobile-first development strategies, ensuring that dealer staff can manage operations seamlessly whether they are on a desktop in the finance office or utilizing a tablet on the lot. Security remains foundational, relying on technologies such as multi-factor authentication (MFA), continuous penetration testing, and compliance-focused data encryption (both in transit and at rest) to protect sensitive consumer financial data and proprietary dealership operational information from escalating cyber threats, guaranteeing adherence to global standards like ISO 27001 and regional mandates like CCPA and GDPR.

The Dealer Management System (DMS) historically focuses on core internal operational tasks like accounting, parts inventory, and payroll. A comprehensive Digital Dealer Platform (DDP) is an integrated ecosystem that incorporates the DMS functions while adding customer-facing digital retailing, advanced CRM, AI-driven marketing, and omnichannel engagement tools to manage the entire modern customer journey seamlessly, bridging the gap between online and in-store operations.

AI significantly impacts profitability by optimizing pricing strategies (dynamic pricing based on real-time market data), improving lead conversion rates through intelligent scoring and automated follow-up, and reducing operational costs via predictive service scheduling and workflow automation. AI ensures resources are allocated to the most valuable opportunities, directly boosting gross margins and improving overall operational efficiency.

Key challenges include migrating complex historical data from outdated legacy systems (DMS/CRM), ensuring seamless API connectivity with third-party services (OEMs, lenders, advertising channels), and managing organizational change resistance among long-term staff, necessitating intensive training and robust post-implementation support to achieve high user adoption and data integrity.

Cloud-based (SaaS) deployment is rapidly dominating market growth. Cloud models offer superior scalability, lower initial capital expenditure, continuous automated updates (crucial for security and feature parity), and enhanced accessibility, which appeals particularly to Small and Medium Dealers (SMDs) and large dealer groups seeking centralized management across disparate geographical locations.

DDPs are evolving to support EV requirements by integrating specialized modules for managing battery health diagnostics, optimizing service workflows tailored to less frequent but highly specialized EV maintenance needs, and facilitating compliance with new agency sales models often favored by EV manufacturers, ensuring the platform remains future-proofed against industry shifts.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.