ID : MRU_ 433168 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

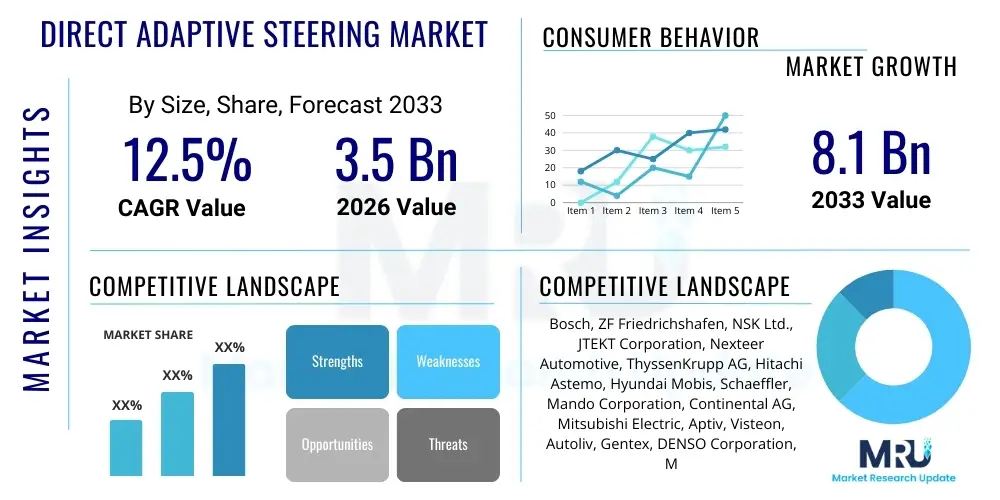

The Direct Adaptive Steering Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 8.1 Billion by the end of the forecast period in 2033. This robust expansion is primarily driven by the increasing global demand for enhanced vehicle safety systems, coupled with the rapid adoption of semi-autonomous and fully autonomous driving technologies across major automotive manufacturing regions.

Direct Adaptive Steering (DAS) represents a significant evolution in vehicular control, moving beyond traditional mechanical linkages to electronic control systems. This technology, often utilized in premium and high-performance vehicles, provides drivers with an unparalleled level of precision and customization regarding steering feel and response. DAS fundamentally improves maneuverability at low speeds by requiring less steering input, while simultaneously enhancing stability and comfort at high speeds by adjusting the steering ratio dynamically based on vehicle speed, road conditions, and driver preference. The system operates through sophisticated electronic control units (ECUs), actuators, and sensors, ensuring reliability and redundancy, which are critical features for its deployment in safety-critical applications.

The core product in the DAS market includes the steer-by-wire (SBW) components, specialized sensors (torque, position, speed), and high-reliability software. Major applications of DAS span across luxury sedans, sports utility vehicles (SUVs), and emerging electric vehicles (EVs), where its integration optimizes energy efficiency and packaging flexibility not possible with conventional steering columns. The primary benefits realized by adopting DAS include superior vehicle handling, reduced driver fatigue, and crucial enablement of advanced driver-assistance systems (ADAS) that require precise and instantaneous steering adjustments, such paving the path for higher levels of autonomous capability.

Driving factors for the market expansion encompass stringent governmental regulations mandating advanced safety features, accelerating research and development investments by Original Equipment Manufacturers (OEMs) into autonomous mobility solutions, and rising consumer awareness regarding the advantages of personalized and dynamically responsive vehicle control. Furthermore, the decreasing cost of high-performance microcontrollers and sensors, coupled with advances in system integration, makes DAS increasingly viable for mid-range vehicle segments, pushing market penetration beyond its current premium niche and solidifying its position as a foundational technology for future automotive architecture.

The Direct Adaptive Steering (DAS) market is characterized by rapid technological innovation and strategic partnerships between automotive Tier 1 suppliers and software specialists. Business trends highlight a strong shift towards modular and scalable DAS solutions that can be easily integrated into diverse vehicle platforms, particularly those utilizing electric powertrains. The ongoing global shortage of critical semiconductor components has momentarily challenged production volumes; however, long-term business projections remain exceedingly positive, fueled by the irreversible trend towards autonomous vehicles. Key industry players are focusing on achieving high levels of redundancy and cybersecurity certification for their steer-by-wire technologies, recognizing these as fundamental requirements for market acceptance in Level 3 and Level 4 autonomous driving environments.

Regionally, the market exhibits dominance by Europe and Asia Pacific, with Europe leading in the initial adoption of high-end DAS systems due to established luxury vehicle manufacturing hubs and stringent Euro NCAP safety standards. Asia Pacific, particularly China and Japan, is anticipated to demonstrate the fastest growth rate, propelled by massive government investment in smart infrastructure and aggressive plans by domestic OEMs to introduce autonomous and electric vehicles at scale. North America remains a crucial market, driven by consumer demand for technologically advanced vehicles and significant investments in AV (Autonomous Vehicle) testing and deployment, particularly in urban mobility sectors.

Segmentation trends reveal a strong preference for high-performance electronic control units (ECUs) and sophisticated actuator assemblies, reflecting the increasing complexity and demands placed on the steering system for real-time responsiveness. The OEM channel continues to account for the largest share of revenue, given the safety-critical nature of DAS systems which necessitate factory integration and rigorous testing. However, the aftermarket segment is projected to gain traction, primarily focusing on diagnostic tools, software updates, and advanced replacement parts as the global fleet utilizing DAS technology matures and requires specialized maintenance and repair services.

User queries regarding AI's influence on the Direct Adaptive Steering market predominantly revolve around three critical themes: system safety and redundancy, real-time performance optimization, and the transition to full autonomy. Users frequently question how AI algorithms enhance the reliability of decoupling the steering wheel from the wheels, and whether machine learning (ML) models can predict component failure better than traditional diagnostics. The expectation is that AI will move DAS systems beyond simple adaptive ratios to truly predictive steering, where the system anticipates driver intention and road hazards milliseconds before a conventional system would react. Concerns are focused on the cybersecurity vulnerabilities introduced by complex, AI-driven software, and the regulatory framework needed to certify AI-driven steering logic as safe.

AI's primary function within DAS is to elevate the system from an adaptive mechanism to an intelligent, predictive controller. Machine Learning models process massive datasets from internal sensors (torque, yaw rate, speed) and external ADAS sensors (LiDAR, radar, cameras) simultaneously. This holistic data processing allows the system to instantaneously determine the optimal steering ratio, damping characteristics, and feedback torque required for current driving dynamics, often exceeding human reaction capabilities. For instance, in dynamic cornering situations or sudden lane changes, AI ensures precise, calibrated responses that maximize vehicle stability and passenger comfort, making the driving experience safer and more seamless.

Furthermore, AI algorithms are vital for maintaining system redundancy and health monitoring within the safety-critical steer-by-wire architecture. By continuously analyzing performance metrics, ML models can detect subtle deviations indicating potential component degradation long before they trigger error codes, facilitating proactive maintenance. This predictive maintenance capability is essential for increasing the mean time between failures (MTBF) and securing consumer trust in fully decoupled steering systems. The integration of robust, certified AI enhances the overall functional safety of DAS, proving its necessity for achieving higher levels of autonomy where human fallback is eliminated.

The Direct Adaptive Steering market is influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively constituting the market's Impact Forces. Key drivers include the global push towards autonomous vehicles (AVs), for which DAS/SBW systems are foundational, and the increasing consumer preference for personalized vehicle dynamics and enhanced safety features. Restraints primarily involve the high initial cost associated with the research, development, and integration of redundant electronic systems, along with the significant regulatory hurdles required for the certification of safety-critical steer-by-wire technology. Opportunities lie in expanding into the high-volume electric vehicle segment, where DAS offers packaging advantages, and developing robust, standardized software platforms compatible across multiple OEMs, thereby reducing complexity and cost barriers.

A primary driver is the operational necessity of DAS within Levels 3 and 4 autonomy. Unlike conventional steering, DAS allows the vehicle's computer to take over steering control completely and smoothly, offering precise control inputs required for complex autonomous maneuvers, such as automated parking and highway pilot functions. Furthermore, the technology enables variable feedback mechanisms, drastically reducing the physical effort required for parking maneuvers while providing firm, communicative feedback at highway speeds, directly addressing consumer demands for both convenience and dynamic performance. This dual advantage across the speed spectrum is a compelling force promoting rapid integration.

However, the market faces significant restraints related to consumer perception and cybersecurity concerns. The complete removal of the mechanical link between the steering wheel and the road wheels generates anxiety regarding catastrophic system failure, necessitating highly redundant, dual or triple-path electronic architectures, which drives up component costs. The critical nature of the steering software also makes it a prime target for cyber threats, requiring continuous, sophisticated defense mechanisms and over-the-air (OTA) update capabilities, which add complexity and regulatory scrutiny. Overcoming these safety and security perceptions through rigorous testing and standardization remains paramount for sustained market growth.

The most compelling opportunities revolve around maximizing the architectural flexibility afforded by DAS, especially in the booming EV market. Since DAS systems eliminate the need for a physical steering column, vehicle designers gain greater flexibility in designing the interior cabin, allowing for innovative features like retractable steering wheels necessary for lounge-like autonomous vehicle interiors. Moreover, the inherent electronic nature of DAS allows for rapid software customization and differentiation, enabling OEMs to offer unique, brand-specific driving dynamics simply through firmware updates, opening new avenues for product innovation and revenue generation beyond hardware sales.

The Direct Adaptive Steering market is comprehensively segmented based on its technological components, vehicle application, and the sales channel through which the systems are distributed. Analyzing these segments provides strategic insights into investment areas and growth trajectories. Component segmentation, covering sensors, actuators, and electronic control units (ECUs), reveals where innovation and cost reduction efforts are most concentrated. Application segmentation differentiates between passenger vehicles and commercial vehicles, reflecting diverse requirements regarding system robustness and responsiveness. Finally, the distinction between OEM and aftermarket channels highlights the dominance of factory installation versus repair and replacement cycles.

The core segment driving technological advancements remains the component segment, specifically the Electronic Control Unit (ECU) sub-segment. ECUs in DAS systems require significantly higher processing power, memory, and safety certifications (ASIL D) compared to conventional steering electronics, driving premium pricing and intensive R&D. Furthermore, the actuator sub-segment, responsible for physically turning the wheels based on ECU commands, demands high precision, instantaneous response times, and resilience under extreme operating conditions. Manufacturers are prioritizing the development of smaller, lighter, and more powerful actuators that can be easily packaged within increasingly complex engine bay layouts, especially in compact or electric vehicles.

From an application standpoint, the passenger vehicle segment holds the dominant market share, primarily driven by the mass adoption of advanced driver assistance systems (ADAS) in mid-to-high-end sedans and SUVs. However, the commercial vehicle segment (including heavy trucks and buses) is anticipated to demonstrate accelerated growth in the latter half of the forecast period. This growth is linked to the deployment of autonomous long-haul trucking and urban platooning applications, where the precise electronic control offered by DAS is crucial for maximizing fuel efficiency, reducing driver stress over long distances, and enabling sophisticated coupling of trailers, demanding robust, high-torque DAS solutions tailored for heavy-duty environments.

The value chain for the Direct Adaptive Steering market begins with the procurement of highly specialized raw materials, primarily focusing on high-grade metallic alloys for robust mechanical components and advanced semiconductor materials for the sophisticated electronic control units. Upstream activities are dominated by specialized suppliers of ASIL D certified microcontrollers, high-precision sensors, and rare-earth magnets essential for powerful, lightweight electric motors used in the actuators. The quality and reliability of these upstream inputs directly dictate the performance and functional safety rating of the final DAS system, necessitating stringent quality control and long-term supply agreements with validated vendors.

Midstream activities involve Tier 1 automotive suppliers who integrate these disparate components into a cohesive, safety-certified DAS module. This stage encompasses complex software development, functional safety engineering (adhering to ISO 26262), rigorous testing protocols, and calibration specific to OEM requirements. These system integrators act as the crucial link, taking raw components and delivering ready-to-install steering systems to vehicle manufacturers. Distribution channels are predominantly direct, with Tier 1 suppliers delivering units just-in-time (JIT) to OEM assembly lines globally, reflecting the criticality and high integration level of DAS within the vehicle's architecture.

Downstream analysis focuses on the Original Equipment Manufacturers (OEMs) who integrate the DAS system into the final vehicle platform, conducting final validation and performance tuning. The indirect distribution channel pertains primarily to the aftermarket segment, involving authorized service centers and specialist repair shops that handle diagnostics, repair, and replacement of failed or damaged DAS components. Given the safety implications, general repair shops are largely excluded from complex DAS servicing, cementing the importance of manufacturer-certified service networks and ensuring that the expertise for software updates and sensor calibration remains centralized, thereby maintaining system integrity throughout the vehicle’s lifecycle.

The primary and most significant end-users and buyers of Direct Adaptive Steering systems are Original Equipment Manufacturers (OEMs) across the global automotive industry. This encompasses manufacturers specializing in premium and luxury vehicles (who were the initial adopters), high-volume passenger vehicle producers increasingly integrating ADAS features, and manufacturers of next-generation electric vehicles. These OEMs procure DAS systems in large volumes directly from Tier 1 suppliers for integration during the assembly phase. Their purchasing decisions are driven by factors such as system reliability, functional safety certifications (ASIL D), cost-per-unit, and the supplier's ability to provide customized software interfaces for brand differentiation.

A rapidly growing segment of potential customers includes specialized manufacturers focused on autonomous transportation and logistics solutions, such as autonomous shuttle providers, self-driving taxi fleet operators, and heavy-duty autonomous trucking companies. For these customers, the benefits of DAS—namely, precise electronic control, rapid responsiveness, and elimination of the mechanical column—are critical enablers for their Level 4 and Level 5 self-driving systems. They prioritize systems offering robust cyber resilience and seamless integration with complex sensor arrays (LiDAR and radar) and central compute platforms necessary for truly driverless operations.

The third key customer group includes authorized dealership service centers and independent, certified automotive repair specialists who serve the aftermarket segment. As the installed base of DAS-equipped vehicles expands, these entities become crucial buyers of replacement components (e.g., actuators, sensor modules) and specialized diagnostic equipment and software licenses required to service and recalibrate these sophisticated systems. The demand here is cyclical, tied to the lifespan and maintenance requirements of the DAS components in the aging vehicle fleet, and focuses on Genuine OEM parts or certified high-quality replacements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 8.1 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, ZF Friedrichshafen, NSK Ltd., JTEKT Corporation, Nexteer Automotive, ThyssenKrupp AG, Hitachi Astemo, Hyundai Mobis, Schaeffler, Mando Corporation, Continental AG, Mitsubishi Electric, Aptiv, Visteon, Autoliv, Gentex, DENSO Corporation, Magna International, Infineon Technologies, STMicroelectronics. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Direct Adaptive Steering market is defined by the migration from hydraulic and electro-hydraulic systems to purely electronic, steer-by-wire (SBW) architectures. Central to this evolution is the development of robust, high-availability electronic redundancy. Since SBW systems eliminate the mechanical failsafe, contemporary designs incorporate parallel electronic paths, dual power supplies, and often two separate ECUs that monitor each other in real-time. This redundancy is mandatory for achieving the highest automotive safety integrity level (ASIL D), ensuring that a single-point failure does not lead to a loss of steering control. Innovations in failure detection algorithms and seamless transition logic are paramount for maintaining driver confidence and meeting stringent regulatory demands for autonomous readiness.

Another crucial technological area involves advanced sensor fusion and communication protocols. DAS systems rely heavily on inputs not just from dedicated steering sensors (torque and position) but also from the vehicle's broader sensor suite (camera, radar, LiDAR) to interpret driving context and adjust the steering ratio predictively. This massive data exchange requires high-speed, reliable in-vehicle networking, leading to the adoption of standards like CAN-FD (Controller Area Network Flexible Data-rate) and Automotive Ethernet. Furthermore, the development of specialized algorithms that filter out noise and prioritize safety-critical inputs ensures the steering system reacts accurately to complex, fast-changing environmental stimuli, such as unexpected road hazards or slippery conditions.

Future technology focuses heavily on miniaturization, power efficiency, and software reconfigurability. Reducing the size and weight of actuators and ECUs is critical for packaging flexibility, especially in compact electric vehicles where every cubic centimeter is valuable. Moreover, the integration of over-the-air (OTA) update capabilities is becoming standard, allowing OEMs to rapidly deploy security patches, refine steering feel, and introduce new dynamic driving modes post-sale. This shift transforms the steering system from a static hardware component into an adaptive, software-defined entity, enabling continuous improvement and customer personalization throughout the vehicle’s lifecycle, marking a significant inflection point in automotive control technology.

The market dynamics for Direct Adaptive Steering vary significantly across geographical regions, influenced by localized manufacturing capabilities, regulatory environments, and consumer adoption rates of luxury and autonomous vehicles. Europe currently holds a leading position in terms of technology penetration and market value, primarily due to the strong presence of major German luxury automotive manufacturers (such as BMW, Mercedes-Benz, and Audi) who were early adopters and integrators of DAS and SBW technology into their high-performance models. This region is also characterized by rigorous functional safety standards (driven by NCAP) and a proactive approach to developing next-generation autonomous driving legislation, fostering a favorable environment for advanced steering system suppliers.

Asia Pacific (APAC) represents the fastest-growing region, driven predominantly by China and Japan. China's enormous domestic electric vehicle market and aggressive government mandates for smart mobility solutions are fueling massive demand for foundational technologies like DAS. Japanese and South Korean OEMs are heavily investing in autonomous vehicle research, positioning them as major customers for robust, high-reliability steering systems. The competitive landscape in APAC is increasingly intense, with local Tier 1 suppliers rapidly closing the technology gap with established Western counterparts, often focusing on cost-effective, scalable solutions tailored for the high-volume electric and urban mobility segments within the region.

North America is a significant market, characterized by high consumer acceptance of technology and substantial investment in autonomous vehicle testing, particularly in states like California and Arizona. The demand here is split between premium vehicle adoption and the burgeoning commercial autonomous trucking sector, which requires heavy-duty DAS systems for platooning and long-haul efficiency. The region emphasizes seamless integration with connectivity features and cybersecurity standards, necessitating suppliers to adhere to rigorous safety protocols and provide solutions that are resilient to external interference and malicious attacks, making reliability and regulatory compliance key success factors in the North American market.

DAS is an advanced steering system that electronically adjusts the steering ratio and effort dynamically based on vehicle speed, offering greater maneuverability at low speeds and stability at high speeds. Unlike traditional mechanical systems, DAS often utilizes steer-by-wire (SBW) technology, eliminating the fixed mechanical link between the steering wheel and the road wheels, relying instead on high-redundancy electronic commands for control.

Yes, DAS systems are designed to meet the highest automotive functional safety standards (ASIL D certification). Safety is ensured through extensive electronic redundancy, typically involving dual or triple backup ECUs, parallel wiring, and segregated power supplies. These fail-operational architectures guarantee that if one component fails, the backup system takes over instantaneously, preventing a loss of control and maintaining high system availability.

DAS is foundational for autonomous driving (Level 3 and higher) because it allows the vehicle's control unit to execute precise, instantaneous steering inputs without driver intervention. The electronic nature of DAS facilitates seamless transitions between manual and automated driving modes, essential for highway pilot features and automated parking, providing the necessary precision and responsiveness for complex AI control.

The primary components include the Steering Wheel Input Mechanism (providing haptic feedback and driver input), the Electronic Control Unit (ECU) for processing control logic, high-power electric Actuators (motors) positioned at the road wheels to execute the steering angle, and various high-precision Sensors (torque, position, speed, and yaw rate) essential for real-time monitoring and feedback to the central ECU.

The highest adoption is currently driven by the premium and luxury Passenger Vehicle segment, where consumers demand superior handling and advanced safety features. However, the fastest growth is anticipated in the Electric Vehicle (EV) segment and the Autonomous Commercial Vehicle segment (trucking and logistics), where DAS provides significant packaging advantages, weight reduction, and the precise control necessary for advanced fleet operations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.