ID : MRU_ 436420 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

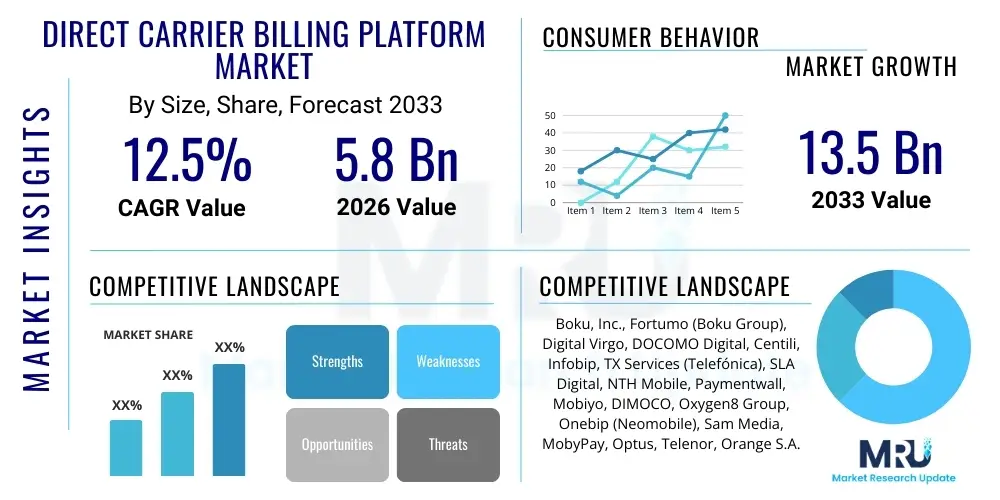

The Direct Carrier Billing Platform Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at $5.8 Billion in 2026 and is projected to reach $13.5 Billion by the end of the forecast period in 2033.

The Direct Carrier Billing (DCB) Platform Market encompasses sophisticated technological solutions that enable consumers to purchase digital goods and services by charging the cost directly to their mobile phone bill. This mechanism serves as a crucial alternative payment method, particularly favored in regions with low banking penetration or where consumers prioritize transaction speed and simplicity. DCB platforms act as intermediaries, integrating mobile network operators (MNOs) with digital merchants, handling complex processes such as secure authentication, transaction routing, and settlement. The reliability and ubiquitous nature of mobile phones position DCB as a high-potential payment method for the expanding global digital economy.

Major applications for DCB platforms span a wide range of digital consumption categories, including mobile gaming, subscription video-on-demand (SVOD) services, digital music streaming, mobile app purchases, and micro-transactions for virtual goods. Key benefits driving the market include unparalleled payment accessibility, instantaneous transaction completion leading to reduced customer friction, and enhanced security compared to sharing credit card details online. The inherent trust relationship between the customer and their MNO further bolsters adoption rates. Moreover, DCB significantly lowers the barrier to entry for digital purchases among the globally unbanked or underbanked populations, making it a powerful tool for market expansion.

The primary driving factors fueling the expansion of the DCB platform market include the exponential rise in smartphone penetration across emerging economies, coupled with increasing consumption of digital content and micro-services. Furthermore, the persistent growth of the mobile gaming industry, which relies heavily on low-friction payment systems for in-app purchases, provides a sustained revenue stream. The evolution of DCB technology to support subscription models and premium services, alongside governmental initiatives promoting digital financial inclusion, solidifies its position as a vital element of the modern digital payments ecosystem.

The Direct Carrier Billing (DCB) Platform Market is witnessing robust growth, driven primarily by the global shift towards mobile-first commerce and the necessity for frictionless payment solutions in the digital content space. Business trends indicate a strong focus on platform interoperability and enhanced fraud detection capabilities, with major platform providers aggressively pursuing partnerships with tier-one Mobile Network Operators (MNOs) to expand their geographical footprint. Strategic mergers and acquisitions are common as companies seek to consolidate market share and integrate complementary technologies, particularly those focused on risk management and regulatory compliance, such as adherence to revised payment directives like PSD2 in Europe. The market is also evolving towards supporting higher average transaction values (ATVs) and facilitating utility payments, moving beyond traditional low-cost digital goods.

Regionally, the Asia Pacific (APAC) market dominates in terms of transaction volume due to the vast mobile subscriber base and high proportion of unbanked consumers, particularly in Southeast Asia and India. However, Europe exhibits high revenue per user, driven by stringent regulatory frameworks that ensure consumer protection and sophisticated integration with premium digital content providers. North America focuses on high-value digital subscriptions and leverages DCB as a complementary payment method alongside conventional banking services. Segment trends show that the Digital Content and Gaming application segment remains the primary revenue contributor, though the emergence of IoT applications requiring micro-payments and the adoption of DCB for transit and parking services represent significant areas of future diversification.

Overall, the market is characterized by increasing technological sophistication. Platform providers are heavily investing in Application Programming Interface (API) development to simplify merchant integration and time-to-market. The competitive landscape is intense, favoring providers that offer scalability, multi-currency support, and robust back-office features including detailed reporting and analytics for MNOs and merchants. The future trajectory suggests a closer integration between DCB and emerging payment technologies, potentially bridging the gap between traditional telecom billing infrastructure and modern fintech solutions.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Direct Carrier Billing (DCB) Platform Market revolve heavily around improving security, optimizing transaction flow, and enhancing personalization. Users frequently ask: "How can AI reduce the rising incidence of fraudulent DCB transactions?" or "Will AI enable personalized content recommendations based on DCB purchase history?" and "How does machine learning improve the efficiency of MNO revenue assurance processes?" These questions highlight key themes: the urgent need for sophisticated fraud prevention, the potential for using rich purchase data for customer engagement, and the necessity of automating complex operational tasks like billing reconciliation.

AI's most immediate and critical impact lies in transforming risk management and fraud detection within DCB ecosystems. Traditional rule-based fraud systems often struggle against complex, evolving attacks such as Account Takeover (ATO) and unauthorized third-party transactions. AI and machine learning algorithms can analyze billions of historical transactions in real-time, identifying subtle behavioral anomalies, geographical inconsistencies, and transaction patterns indicative of fraud with far greater accuracy than human analysts or static models. This capability significantly reduces financial losses for MNOs and merchants, thereby boosting confidence in DCB as a secure payment method.

Furthermore, AI is pivotal in optimizing the customer experience and enhancing revenue opportunities. By analyzing user purchasing behavior data collected through the DCB platform, machine learning models can segment customers effectively and predict the optimal time, price point, and type of content a user is likely to purchase next. This drives highly effective personalized marketing and targeted promotions by both MNOs and integrated merchants, improving conversion rates and Average Revenue Per User (ARPU). Operationally, AI also streamlines dispute resolution and compliance checks, leading to faster settlements and reduced operational expenditure for platform providers.

The Direct Carrier Billing (DCB) Platform Market is shaped by a complex interplay of Drivers, Restraints, and Opportunities, which collectively constitute the critical impact forces steering its evolution. A primary driver is the necessity for digital payment solutions that bypass traditional banking infrastructure, especially in emerging markets characterized by high mobile penetration but low credit card adoption. This factor significantly enhances market reach for digital merchants. Coupled with this is the extreme convenience offered to banked users who prefer the one-click, low-friction payment process for micro-transactions, avoiding the repeated input of card details. However, the market faces substantial restraints, primarily regulatory complexities which vary widely across countries, demanding continuous technological adaptation for compliance, such as GDPR and region-specific payment mandates. Furthermore, the persistent threat of mobile payment fraud and chargeback liability poses a significant financial risk to MNOs and platforms, often necessitating high investment in security infrastructure.

Opportunities for growth are abundant, particularly in integrating DCB capabilities into new sectors like the Internet of Things (IoT), where micro-payments for connected devices and services (e.g., smart home utilities, connected cars) will become commonplace. Another major opportunity lies in expanding DCB acceptance within B2B environments, facilitating secure internal transactions or low-value supplier payments. The standardization of payment APIs and the global rollout of 5G networks, which promises lower latency and higher data speeds, will further accelerate the adoption of real-time digital services that rely on DCB for instantaneous monetization.

The overall impact forces are strongly positive, suggesting sustained expansion, provided the industry successfully navigates the regulatory fragmentation and continuously enhances its fraud mitigation strategies. The growing digital appetite globally, particularly for content and gaming, ensures a steady demand base, making DCB a crucial utility rather than merely an alternative payment method. Strategic partnerships between telecom operators, platform vendors, and global content providers will be key determinants of future market dominance.

The Direct Carrier Billing Platform Market is strategically segmented to provide a detailed view of its composition, revenue generation mechanisms, and application areas. Primary segmentation is based on Transaction Type, focusing on whether purchases are one-time or subscription-based, which significantly impacts revenue assurance and platform complexity. Further categorization relies on the Application vertical, identifying the major end-use sectors driving transaction volume, such as gaming, digital content, and utilities. Analyzing these segments helps stakeholders understand prevailing consumer spending habits and identify high-growth areas for platform investment and merchant acquisition strategies. The complexity inherent in managing differing regulatory and tax requirements across various geographic regions also necessitates robust regional segmentation.

The Direct Carrier Billing platform value chain is complex and involves multiple interconnected entities, starting from upstream infrastructure providers and culminating in the end consumer. Upstream activities are dominated by Mobile Network Operators (MNOs) who own the billing relationship with the consumer and the crucial network infrastructure. Platform providers sit centrally in the chain, offering the technological backbone—including secure APIs, aggregation services, and settlement engines—that bridges MNO capabilities with merchant demands. The efficiency and security of this central platform are paramount, as they determine the success rate of transactions and the speed of integration.

Midstream involves payment gateways and aggregation services provided by the DCB platforms themselves. These entities are responsible for fraud management, regulatory compliance checks, tax calculation, and accurate billing transmission to the MNOs. Downstream activities involve digital merchants and content providers (the direct clients of the platform), who integrate the DCB option into their checkout processes. The final recipient is the end consumer, who relies on a seamless and trustworthy payment experience. Effective distribution channels are characterized by both direct integration (large merchants connecting directly to a platform) and indirect distribution, where smaller merchants utilize third-party aggregators or payment facilitators who, in turn, leverage the core DCB platform.

The value generated is shared primarily through revenue splits between the MNO (who takes the largest share for customer ownership and billing risk), the DCB platform provider (for technology and aggregation services), and the merchant (for the content/service provided). Transparency, low latency, and robust reconciliation systems are critical for maintaining trust and efficiency across this multi-party ecosystem. The trend leans towards platform providers offering more sophisticated ancillary services, such as data analytics and dynamic pricing tools, to capture greater value share.

Potential customers and primary end-users of Direct Carrier Billing platforms are fundamentally divided into two major groups: the enterprises that utilize the technology for monetization, and the consumers who employ it for purchases. The primary enterprise buyers are digital content providers, notably those in mobile gaming and subscription video or music services, requiring frictionless global payment collection. Telecom operators themselves are also key customers, leveraging platforms to manage third-party service billing efficiently and securely, often seeking enhanced fraud mitigation tools provided by the platform vendors.

Beyond traditional media, emerging buyers include utility companies seeking simplified micro-payment collection for IoT services and smart city applications. Furthermore, global application stores and marketplaces use DCB platforms to facilitate purchases for users without traditional bank cards. From the consumer perspective, the most frequent buyers are mobile users located in emerging economies (the underbanked population) and youth demographics globally who prefer using their mobile balance or bill for spontaneous digital purchases.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $5.8 Billion |

| Market Forecast in 2033 | $13.5 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Boku, Inc., Fortumo (Boku Group), Digital Virgo, DOCOMO Digital, Centili, Infobip, TX Services (Telefónica), SLA Digital, NTH Mobile, Paymentwall, Mobiyo, DIMOCO, Oxygen8 Group, Onebip (Neomobile), Sam Media, MobyPay, Optus, Telenor, Orange S.A., Vodafone Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Direct Carrier Billing (DCB) market is defined by robust, highly scalable infrastructure designed to handle billions of transactions annually while ensuring regulatory compliance and paramount security. Central to this landscape is the widespread adoption of standardized Application Programming Interfaces (APIs), which allow merchants and content providers to integrate the payment option quickly and reliably across various MNOs globally. Modern DCB platforms rely heavily on RESTful APIs for real-time authentication, transaction processing, and status feedback, minimizing latency crucial for enhancing the consumer experience. Furthermore, the underlying infrastructure often utilizes cloud-native architectures to ensure elasticity and geographic distribution of processing power, essential for supporting peak traffic loads, especially during major gaming or content releases.

Security and compliance technology represent another cornerstone. This includes sophisticated mechanisms for fraud prevention, often incorporating advanced AI/ML algorithms to analyze transactional metadata in milliseconds. Compliance technology is heavily focused on adherence to regulations such as the EU’s Payment Services Directive 2 (PSD2), requiring Strong Customer Authentication (SCA) for many transaction types. Platforms utilize tokenization and encryption techniques to safeguard customer data during the billing process, ensuring that sensitive information is never exposed to the merchant. The necessity for high-level data security drives continuous investment in advanced security protocols and monitoring systems, often certified to meet stringent industry standards.

Moreover, the technological evolution is moving towards sophisticated data analytics and reporting tools. DCB platforms now offer MNOs and merchants granular, real-time insights into consumer behavior, conversion rates, and revenue performance across different countries and content types. These reporting dashboards are critical for optimizing pricing strategies and managing chargeback rates effectively. The ongoing integration with 5G technology is expected to further enhance the speed and reliability of these platforms, enabling entirely new use cases requiring ultra-low latency billing, such as instantaneous payment for augmented reality (AR) or virtual reality (VR) content accessed via mobile devices.

The transition toward greater financial transparency mandates better integration with core MNO Business Support Systems (BSS) and Operations Support Systems (OSS). Modern DCB platforms must seamlessly interface with these legacy systems, utilizing microservices architecture to ensure modularity and scalability. This technological evolution allows for rapid deployment of new payment rules, tariff changes, and promotional campaigns, thereby maintaining competitive agility in a fast-moving digital market. The capacity to handle recurring billing reliably and manage the intricacies of subscription lifecycle management (e.g., failed payments, renewals, cancellations) is a key technical differentiator among leading platform providers.

The Direct Carrier Billing (DCB) Platform Market demonstrates significant regional variation in terms of maturity, regulatory complexity, and primary growth drivers.

Direct Carrier Billing (DCB) is a mobile payment method where purchases of digital content, apps, or services are charged directly to the user's mobile phone bill or deducted from their prepaid balance. It works by having the DCB platform securely authenticate the transaction with the user’s Mobile Network Operator (MNO), bypassing the need for credit cards or bank details, offering a high-frictionless payment experience.

The most significant revenue drivers for DCB platforms globally are the Digital Content and Mobile Gaming segments. Mobile gaming, including in-app purchases and virtual currency sales, benefits immensely from DCB's speed and convenience, while subscription services for video streaming and music also contribute substantially, particularly in mature markets.

The primary security concerns revolve around mobile payment fraud, including "clickjacking," account takeover (ATO), and unauthorized third-party charges. Market solutions increasingly rely on sophisticated AI and machine learning techniques to analyze behavioral data in real-time, enhancing fraud detection and risk scoring to mitigate these financial liabilities.

Regulations like PSD2 (Payment Services Directive 2) in Europe impose stringent requirements, primarily demanding Strong Customer Authentication (SCA) for most DCB transactions. This has necessitated technological upgrades for platform providers to maintain compliance and security while preserving the low-friction user experience crucial for DCB adoption.

The Asia Pacific (APAC) region, specifically Southeast Asia and India, is currently exhibiting the fastest growth in the DCB market in terms of transaction volume. This accelerated expansion is fueled by the region's massive mobile penetration rates and the large population of consumers who remain unbanked or underbanked, relying on mobile credit as their primary purchasing power.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.