ID : MRU_ 435092 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

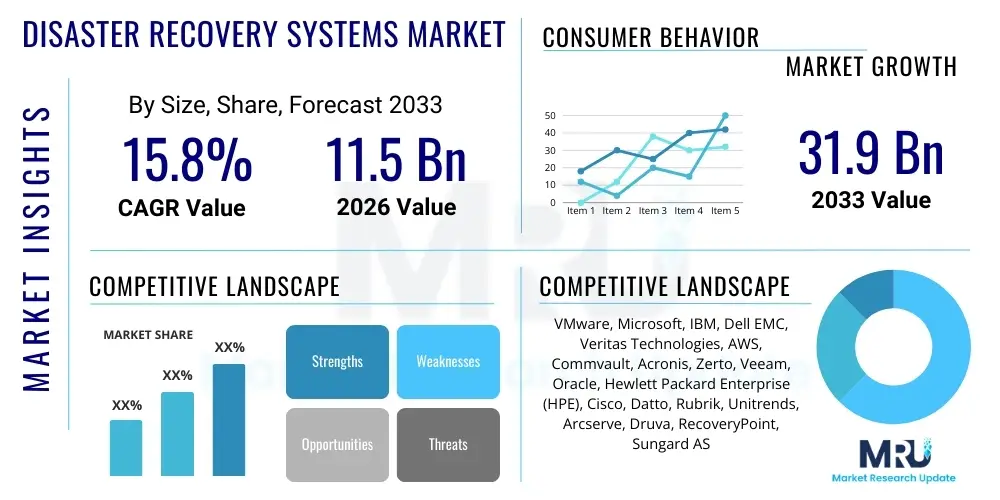

The Disaster Recovery Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 11.5 billion in 2026 and is projected to reach USD 31.9 billion by the end of the forecast period in 2033.

The Disaster Recovery (DR) Systems Market encompasses a wide range of solutions, services, and infrastructure designed to ensure business continuity and resilience following catastrophic events, whether natural (floods, earthquakes) or man-made (cyberattacks, power outages, human error). These systems focus on minimizing downtime and data loss by replicating critical data, applications, and IT infrastructure to a secure, off-site location, often leveraging cloud environments for flexibility and scalability. The core function of these systems is to rapidly restore normal operations within predefined recovery objectives (RTO and RPO), maintaining the integrity and availability of essential business processes across diverse industry verticals globally. The sophistication of modern DR solutions has evolved significantly, integrating advanced technologies such as virtualization, hyper-converged infrastructure, and orchestration tools to automate failover and failback processes, moving beyond traditional tape backup methods toward real-time replication and continuous data protection.

Major applications for disaster recovery systems span across all data-intensive sectors, including Banking, Financial Services, and Insurance (BFSI), IT and Telecommunications, Healthcare, Manufacturing, and Government. In highly regulated industries like BFSI and Healthcare, these systems are not just operational necessities but mandatory requirements dictated by stringent compliance standards (e.g., GDPR, HIPAA, financial regulations) that demand immediate data accessibility and protection. The primary benefits derived from implementing robust DR systems include significant reduction in financial losses associated with downtime, protection of brand reputation, and assurance of regulatory compliance, which are critical differentiators in today's competitive landscape. Moreover, effective DR planning contributes directly to improved organizational resilience, allowing enterprises to adapt quickly to unexpected disruptions and maintain stakeholder trust even during severe crisis periods.

Key driving factors accelerating market growth include the exponential increase in data generation and storage requirements, making data loss exponentially more costly. Furthermore, the rising frequency and sophistication of cyber threats, particularly ransomware attacks targeting critical infrastructure, have elevated disaster recovery from an optional safeguard to a core strategic imperative for C-level executives. The massive shift toward hybrid and multi-cloud environments necessitates more complex, cloud-native DR solutions that can handle distributed workloads, pushing enterprises to invest heavily in advanced Recovery as a Service (DRaaS) models. Regulatory pressures demanding zero tolerance for data unavailability and the need for simplified, automated recovery processes also continue to fuel the adoption of integrated disaster recovery platforms across Small and Medium Enterprises (SMEs) and large corporations alike, cementing the market’s positive trajectory.

The Disaster Recovery Systems Market is experiencing robust expansion driven primarily by critical business trends centered around digital transformation, cloud migration, and escalating cyber risk. Business continuity planning has transitioned from a localized IT concern to an enterprise-wide strategic focus, demanding solutions that offer near-zero Recovery Time Objectives (RTOs) and Recovery Point Objectives (RPOs). A dominant trend is the rapid uptake of Disaster Recovery as a Service (DRaaS), which lowers capital expenditure, reduces complexity, and increases the flexibility required for managing heterogeneous IT environments spanning on-premise, public, and private clouds. Furthermore, market competition is intensifying, focusing on integrated solutions that combine backup, data protection, and recovery orchestration into single, unified platforms, thereby simplifying management and enhancing overall resilience posture for modern enterprises dealing with distributed IT architectures.

Regionally, North America maintains the largest market share due to the early and widespread adoption of cloud technologies, the presence of major technology providers, and highly stringent regulatory landscapes, particularly within the financial and technology sectors. However, the Asia Pacific (APAC) region is poised to exhibit the highest Compound Annual Growth Rate (CAGR) throughout the forecast period. This accelerated growth in APAC is attributed to rapid industrialization, massive investments in cloud infrastructure, and increasing awareness regarding data protection and regulatory compliance among emerging economies like China, India, and Southeast Asian nations. European markets are driven by pervasive compliance requirements related to data governance (such as GDPR), pushing organizations to adopt localized, yet highly resilient, disaster recovery strategies that ensure data residency and rapid restoration capabilities, fostering substantial growth in localized DRaaS offerings.

In terms of segmentation, the Cloud Deployment model is overwhelmingly dominating the market and is expected to grow fastest, primarily because it offers unmatched scalability, cost efficiency, and geographical redundancy compared to traditional on-premise DR sites. Within the component segment, services (including professional services, managed services, and support) are critical, as organizations increasingly seek external expertise for complex DR implementation, testing, and management. Among industry verticals, the BFSI sector remains the largest consumer of disaster recovery systems due to the massive transactional volumes and regulatory mandates requiring continuous operation. However, the Healthcare sector is showing significant growth acceleration, prompted by the increasing digitization of patient records and the severe threat posed by targeted ransomware attacks against vital healthcare systems, driving mandatory investment in robust, compliant recovery solutions.

Common user questions regarding AI's impact on Disaster Recovery Systems typically center on whether AI can automate decision-making during a disaster, reduce recovery time, predict failures before they occur, and ultimately lower the operational costs associated with DR testing and maintenance. Users are concerned about the reliability and trustworthiness of AI systems taking control during a high-stakes failure scenario, and how AI might integrate with complex, multi-cloud recovery orchestration tools. The prevailing expectation is that AI and Machine Learning (ML) will transform disaster recovery from a reactive process into a highly proactive and predictive function. Key themes include the use of AI for anomaly detection, intelligent resource provisioning during failover, optimizing data replication strategies based on usage patterns, and creating 'self-healing' infrastructure that minimizes human intervention, leading to faster, more reliable recovery outcomes and enhancing overall resilience metrics.

The application of Artificial Intelligence within disaster recovery systems represents a paradigm shift toward intelligent resilience. AI and ML algorithms are primarily used to continuously monitor and analyze vast datasets related to system performance, network latency, application dependencies, and historical failure patterns. This continuous analysis allows the DR system to establish dynamic baselines and identify subtle deviations, enabling predictive maintenance and preemptive recovery actions before a minor issue escalates into a catastrophic failure. For instance, AI can detect unusual network traffic or storage I/O patterns that might signal an impending hardware failure or the early stages of a sophisticated cyberattack, triggering automated countermeasures or preparing the recovery site for immediate failover, significantly improving the Mean Time to Recovery (MTTR).

Furthermore, AI plays a crucial role in optimizing the recovery process itself, particularly in complex multi-tier application environments. Traditional DR testing often requires extensive manual scripting and configuration adjustments. AI-powered orchestration tools can dynamically map application dependencies across different environments, intelligently prioritize the restoration sequence of VMs and services based on business criticality, and automatically provision the required compute and storage resources at the recovery site. This automation drastically reduces the human error factor and accelerates the time taken to restore complex enterprise applications, ultimately contributing to lower RTOs and enhancing the confidence in the DR plan's reliability. The integration of AI also simplifies compliance reporting by automating the documentation of recovery testing and providing transparent audit trails.

The market dynamics of Disaster Recovery Systems are governed by a robust interplay of Drivers, Restraints, and Opportunities (DRO), collectively constituting the core Impact Forces. The primary drivers include the relentless growth of enterprise data volumes, the critical necessity for maintaining regulatory compliance across numerous jurisdictions (e.g., PCI DSS, HIPAA, GDPR), and, most importantly, the exponential rise in highly destructive cyberattacks, particularly ransomware, which necessitates robust, immutable recovery capabilities. These drivers exert a strong positive force, making investment in high-availability DR solutions mandatory rather than discretionary. However, restraints such as the high initial deployment costs associated with establishing robust DR infrastructure, complexity in managing hybrid cloud recovery environments, and the challenge of finding skilled IT professionals to configure and maintain advanced DR orchestration tools occasionally impede widespread adoption, particularly among budget-constrained SMEs. The lack of standardized testing protocols across diverse vendor platforms also adds a layer of operational friction.

Counterbalancing the restraints are significant opportunities emerging from technological advancements and market shifts. The rapid expansion of affordable and scalable public cloud infrastructure (AWS, Azure, GCP) has fueled the growth of DRaaS, transforming DR expenditure from a CapEx to an OpEx model, thereby democratizing access to enterprise-grade recovery solutions for smaller businesses. Furthermore, the development of intelligent automation tools, incorporating AI and ML for predictive recovery and simplified orchestration, addresses the complexity restraint directly by streamlining operations and minimizing human error. The increasing move toward highly distributed, edge computing environments also presents a major opportunity for vendors to develop specialized, low-latency recovery solutions tailored to geographically dispersed data assets, ensuring regional resilience and compliance with local data sovereignty laws.

The overall Impact Forces decisively favor market expansion. The high stakes associated with prolonged downtime (leading to massive financial losses and reputational damage) coupled with regulatory pressure far outweigh the perceived complexities and costs of implementation. The impact force of cybersecurity threats, in particular, acts as a continuous, powerful catalyst, forcing organizations across all sectors to continually upgrade and validate their disaster recovery strategies. The widespread availability of flexible DRaaS solutions has mitigated the historical cost restraint, making advanced recovery accessible. Consequently, the market is primarily characterized by rapid technological innovation focused on improving RTO/RPO metrics, integrating cybersecurity defenses directly into the recovery process, and simplifying management through AI-driven automation, ensuring sustained double-digit growth throughout the forecast period.

The Disaster Recovery Systems Market is comprehensively segmented based on several critical factors including Component (Solutions and Services), Deployment Model (On-Premise, Cloud-based, and Hybrid), Enterprise Size (Small & Medium Enterprises and Large Enterprises), and Industry Vertical (BFSI, IT & Telecom, Government, Manufacturing, Healthcare, and Others). This segmentation provides a granular view of market adoption patterns, helping stakeholders understand where investment is most concentrated and identifying high-growth sub-sectors. The market dynamics within each segment are heavily influenced by the specific needs for data security, regulatory compliance mandates, and the budget constraints characteristic of the respective enterprise size or industry. For example, large enterprises often favor hybrid deployments combining existing on-premise infrastructure with cloud scalability, while SMEs are rapidly migrating entirely to the cost-effective Cloud DRaaS model.

The value chain of the Disaster Recovery Systems Market begins with Upstream Analysis, primarily involving core technology providers such as hardware manufacturers (storage and server infrastructure), networking equipment suppliers, and fundamental software developers specializing in virtualization (e.g., VMware, Microsoft Hyper-V) and data protection algorithms. These upstream players invest heavily in research and development to create highly efficient data replication, compression, and de-duplication technologies crucial for minimizing recovery costs and bandwidth usage. Strategic partnerships formed at this stage are critical, ensuring software compatibility with diverse underlying infrastructure, enabling seamless integration of DR tools into existing enterprise IT environments. The competitive edge upstream relies on performance metrics such as immutable storage guarantees and integrated ransomware protection features.

Midstream activities encompass the core software development, integration, and service provision phases. This segment is dominated by specialized DR vendors and large enterprise IT providers who bundle the upstream technologies into complete solutions—including DR Orchestration Platforms and Backup as a Service (BaaS) or DRaaS offerings. Distribution channels play a vital role here, primarily utilizing both direct and indirect models. Direct distribution involves vendors selling complex, customized enterprise solutions directly to large clients through dedicated sales teams. The indirect model, which is pervasive, relies heavily on a network of Value-Added Resellers (VARs), Managed Service Providers (MSPs), and system integrators. MSPs are particularly important as they offer comprehensive managed disaster recovery services, handling the entire lifecycle—from planning and testing to execution—allowing end-users to focus on core business activities while outsourcing DR complexity.

Downstream analysis focuses on the end-users (Potential Customers) and the post-implementation services. The end-users span all industry verticals, seeking solutions that meet specific RTO/RPO targets and compliance requirements. Post-sale support, maintenance, continuous monitoring, and mandatory regular testing of the DR plan constitute crucial downstream services. The quality of ongoing support and the simplicity of the failover/failback processes significantly influence customer retention and loyalty. Furthermore, the role of cloud service providers (AWS, Azure, GCP) has fundamentally altered the downstream landscape by acting as the primary recovery targets, offering the necessary infrastructure elasticity that traditional dedicated recovery sites lacked, thereby solidifying the shift towards utility-based consumption of recovery resources.

The primary potential customers and buyers of Disaster Recovery Systems are organizations across all industry sizes and verticals that rely heavily on continuous data availability and mission-critical applications to conduct business operations. Large enterprises, including multinational corporations in BFSI, Telecom, and Manufacturing, constitute the largest segment of potential customers due to their enormous data footprints, complex IT environments, and the astronomical cost associated with downtime. These buyers typically seek high-end, customized hybrid DR solutions featuring advanced automation, centralized orchestration, and guaranteed Service Level Agreements (SLAs) for recovery times. Their purchasing decisions are heavily influenced by regulatory compliance requirements and the need for geographical redundancy, often favoring established vendors with global infrastructure reach and proven track records in managing large-scale, complex disaster scenarios.

Small and Medium Enterprises (SMEs) represent a rapidly expanding segment of potential customers, driven by the increasing affordability and simplicity of cloud-based Disaster Recovery as a Service (DRaaS). SMEs often lack the internal resources, expertise, and capital expenditure budget required for traditional on-premise DR setup. Therefore, they are highly receptive to subscription-based, fully managed DRaaS offerings that provide enterprise-grade protection with minimal upfront investment and simplified management interfaces. The critical need for SMEs to protect against common threats like localized hardware failure and opportunistic ransomware attacks, which can be existential for a smaller business, makes them increasingly critical buyers, particularly those utilizing centralized, managed IT service providers (MSPs) as their primary channel for DR procurement and management.

Furthermore, highly regulated sectors such as Healthcare and Government are pivotal potential customers. Healthcare organizations, facing mounting pressure to secure Electronic Health Records (EHR) against cyberattacks and meet strict compliance standards (like HIPAA), require immutable backup and extremely rapid recovery capabilities to ensure patient safety and operational continuity. Government agencies, operating vital public services, need highly secure, localized DR solutions that ensure data sovereignty and resilience against national infrastructure threats. These customers often prioritize security certifications, vendor trustworthiness, and compliance features above pure cost efficiency, making them premium buyers focused on solution robustness and vendor stability rather than just the lowest price point for achieving business continuity mandates.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 31.9 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | VMware, Microsoft, IBM, Dell EMC, Veritas Technologies, AWS, Commvault, Acronis, Zerto, Veeam, Oracle, Hewlett Packard Enterprise (HPE), Cisco, Datto, Rubrik, Unitrends, Arcserve, Druva, RecoveryPoint, Sungard AS |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Disaster Recovery Systems Market is rapidly evolving, driven by the demand for reduced recovery times, simplified management, and cost efficiency. Cloud-based Disaster Recovery (DRaaS) has emerged as the most disruptive technology, leveraging the immense scalability and pay-as-you-go model of public cloud providers to serve as the recovery site. This shift eliminates the need for organizations to maintain expensive, proprietary secondary data centers. DRaaS relies on sophisticated replication mechanisms that move data continuously to the cloud and utilizes powerful cloud orchestration tools to automate the spinning up of compute resources only when a disaster event occurs, dramatically lowering operational costs and increasing the geographical reach and redundancy of the recovery architecture.

Another pivotal technology is advanced Virtualization and Hyper-converged Infrastructure (HCI). Virtualization platforms (like VMware and Hyper-V) are foundational, enabling hardware-agnostic replication and recovery, ensuring that virtual machine workloads can be instantly migrated and restored onto disparate hardware at the recovery site. HCI further integrates computing, storage, and networking into a single system, streamlining the backup and recovery process and providing native data protection capabilities at the primary site. The tight coupling of data protection capabilities directly into the infrastructure layer simplifies administration and drastically improves the efficiency of snapshotting and replication required for continuous data protection (CDP), moving closer to near-zero data loss objectives.

Furthermore, the focus on automation and intelligence is reshaping the market through AI and Machine Learning integration. DR Orchestration tools are now incorporating ML algorithms to automate complex failover workflows, test recovery plans non-disruptively, and provide proactive alerts based on predictive failure analysis. Technologies such as immutable storage and deep integration with ransomware detection systems are also becoming standard features, ensuring that even if the production environment is compromised by malicious encryption, the recovery copies remain clean, secure, and instantly accessible. The combination of these technologies—Cloud DRaaS, advanced virtualization, and intelligent orchestration—forms the bedrock of modern, resilient disaster recovery strategies required by digital-first businesses.

DRaaS is a cloud computing model where a third-party provider manages the replication, hosting, and failover of an organization's mission-critical data and applications to a public or private cloud environment. It is preferred because it significantly lowers capital expenditure (eliminating dedicated secondary sites), offers superior scalability and geographical redundancy, and simplifies testing and maintenance through subscription-based, automated services, leading to better Recovery Time Objectives (RTOs) compared to legacy tape or manual systems.

Ransomware attacks are a primary catalyst for DR investment, as they render traditional backup files vulnerable. Modern DR systems address this by incorporating immutable storage technology and integrated data protection features, ensuring that recovery copies cannot be encrypted, modified, or deleted by attackers. This necessitates investment in next-generation DR solutions that focus on rapid, verifiable restoration from a clean, secure point, turning DR into a critical cybersecurity measure.

The two most critical metrics are the Recovery Time Objective (RTO) and the Recovery Point Objective (RPO). RTO defines the maximum acceptable duration of downtime after a failure, aiming for near-instantaneous recovery in critical systems. RPO defines the maximum tolerable amount of data loss measured in time, often pushing for zero or near-zero data loss (Continuous Data Protection). Other factors include failover success rate, cost efficiency, and compliance adherence during recovery.

The market is moderately concentrated, dominated by major players like VMware, Microsoft, IBM, and AWS, which offer comprehensive hybrid and cloud DR solutions. However, the market also features fragmentation driven by specialized innovators (like Veeam and Zerto) focusing on niche areas such as replication efficiency and orchestration. Key growth drivers include regulatory pressure, the shift to multi-cloud environments, and the increasing incorporation of AI to automate recovery workflows.

The shift necessitates more complex, flexible, and unified DR planning. Organizations require orchestration tools that can seamlessly manage failover and failback processes across heterogeneous environments—from on-premise servers to multiple public clouds (multi-cloud). This complexity drives demand for integrated DR software solutions that provide centralized visibility and management, ensuring consistent security policies and compliance across disparate infrastructure platforms during a disaster event.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.