ID : MRU_ 437451 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

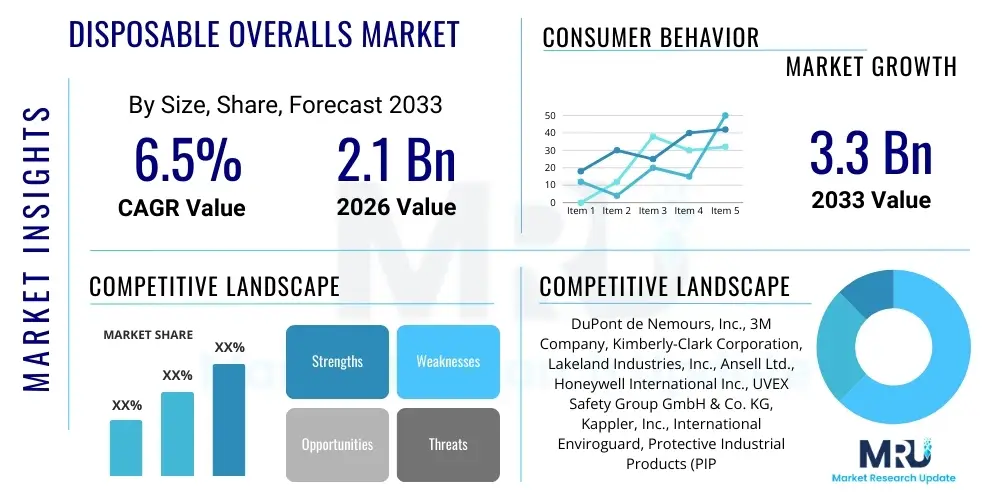

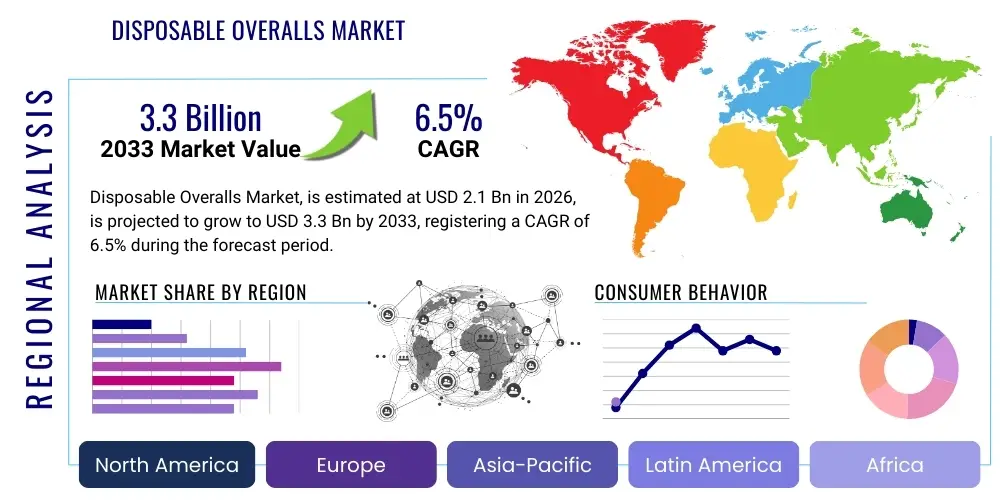

The Disposable Overalls Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at $2.1 Billion in 2026 and is projected to reach $3.3 Billion by the end of the forecast period in 2033.

The Disposable Overalls Market encompasses protective garments designed for single-use applications across various industrial, healthcare, and hazardous environments. These garments are crucial components of Personal Protective Equipment (PPE), offering effective barriers against particulate matter, chemicals, biological agents, and non-hazardous contaminants. The primary function of disposable overalls is to shield the wearer’s clothing and skin from external contaminants while also preventing the wearer from contaminating sterile or sensitive environments. Products typically vary based on material type, ranging from lightweight spunbond polypropylene for dust protection to high-performance multilayer laminates offering chemical splash resistance, fulfilling rigorous safety standards mandated by global regulatory bodies like OSHA and the European Union directives concerning workplace safety and infectious disease control.

Major applications driving market demand include the healthcare sector, particularly during surgical procedures, pandemic responses, and laboratory work, where cross-contamination risks are high. Furthermore, the industrial sector, covering automotive painting, chemical processing, pharmaceuticals manufacturing, and asbestos abatement, relies heavily on disposable protection to comply with operational safety protocols. The increasing global focus on worker safety and the stringent enforcement of occupational health standards directly correlate with the rising adoption of these protective suits. Benefits associated with disposable overalls include reduced laundering costs, guaranteed sterility or cleanliness for each use, and simplified hazard management due to immediate, safe disposal after exposure, thereby minimizing the risk of secondary contamination.

Driving factors fueling this market expansion are multifaceted. A primary driver is the recurring necessity for stringent infection control measures, particularly in light of recent global health crises which dramatically highlighted the importance of readily available PPE. Secondly, rapid industrialization, especially in developing economies, leads to increased manufacturing activities in chemical, electronics, and construction sectors, necessitating compliance with enhanced safety standards. Furthermore, continuous product innovation, focused on enhancing breathability, antistatic properties, and chemical barrier performance without compromising comfort or cost-effectiveness, continues to broaden the acceptance and utility of disposable overalls across new and existing end-user industries, securing consistent demand throughout the forecast period.

The Disposable Overalls Market demonstrates robust growth, primarily driven by escalating global health concerns and mandatory industrial safety standards. Business trends indicate a strong focus on supply chain resilience, necessitated by volatile raw material costs and heightened demand variability seen in recent years. Manufacturers are investing heavily in geographically diversified production capabilities, particularly expanding operations in Asia Pacific to optimize logistics and reduce lead times for high-volume orders. Strategic partnerships between PPE manufacturers and large purchasing organizations, such as national healthcare systems and major industrial conglomerates, are becoming commonplace to ensure stable procurement and preferred vendor status, thereby solidifying market positions amidst increasing competition and standardization pressures.

Regional trends reveal significant shifts in consumption patterns, with Asia Pacific emerging as the fastest-growing market segment. This accelerated growth is attributable to rapid infrastructural development, burgeoning manufacturing bases, and improving awareness regarding occupational health and safety across countries like China, India, and Southeast Asia. North America and Europe, while mature markets, maintain high market shares driven by stringent regulatory environments and established healthcare infrastructures that mandate the highest quality protective apparel. Furthermore, regulatory harmonization efforts across major trading blocs are influencing product design, pushing manufacturers towards universally accepted high-performance standards, which enhances market accessibility and global trade flow for specialized disposable suits.

Segment trends highlight the dominance of non-woven material types, particularly composite materials combining breathability with superior barrier performance, such as SMS (Spunbond-Meltblown-Spunbond) fabrics, which offer an optimal balance of protection and wearer comfort. In terms of application, the healthcare sector remains the largest consumer, though the manufacturing and construction industries exhibit the highest incremental growth due to increased activity levels and stricter dust/particulate control regulations. Key segment analysis suggests a growing preference for specialty overalls designed for specific hazard types, such as Type 3 (liquid tight) and Type 4 (spray tight) classifications, indicating a market maturation toward risk-specific protective solutions rather than general-purpose attire, thereby driving up the average selling price and market value.

User queries regarding the integration of Artificial Intelligence (AI) in the disposable overalls sector primarily center on how sophisticated automation can optimize manufacturing processes, improve quality control, and streamline supply chain logistics. Common concerns revolve around predictive maintenance for non-woven fabric machinery, utilizing machine vision systems for flawless seam sealing inspection, and deploying AI algorithms to forecast regional demand surges (e.g., during flu seasons or industrial upticks) to prevent stockouts or overstocking. Users anticipate that AI-driven process optimization will lead to significant cost reductions in high-volume production, potentially making high-barrier overalls more accessible, while simultaneously enhancing product integrity through constant, automated quality monitoring that surpasses manual inspection capabilities.

The market for disposable overalls is significantly shaped by dynamic forces rooted in health crises, regulatory mandates, and technological advancements. A primary driver is the consistently rising global awareness and implementation of stringent occupational safety standards, particularly in emerging industrial economies, which necessitates the habitual use of protective apparel across hazard-prone sectors. Opportunities are robustly present in the development and scaling of sustainable materials, such as bio-based or easily recyclable polymers, addressing growing environmental concerns and regulatory pressures against non-biodegradable waste. Conversely, the market faces significant restraints from the volatile cost structure of petroleum-derived raw materials (like polypropylene), which forms the core component of most non-woven fabrics, often leading to fluctuating profit margins and pricing instability.

Impact forces currently influencing the market structure are dominated by the ripple effects of pandemic preparedness protocols adopted globally. This preparedness has created a foundational baseline demand much higher than pre-2020 levels, ensuring sustained investment in manufacturing capacity and strategic national stockpiling mandates in many developed nations. Furthermore, the imperative for advanced barrier protection is intensifying as industrial chemical usage broadens and the threat landscape evolves, pushing manufacturers to innovate beyond standard Type 5/6 classifications toward enhanced Type 3/4 chemical protection suits. This drive toward specialization and superior performance acts as a powerful lever, mitigating some of the traditional price-based competition.

The inherent limitations regarding the comfort and breathability of highly protective suits remain a key challenge, particularly in hot and humid operational environments, influencing user compliance and demanding continuous research into breathable membrane technologies. Despite these challenges, the overarching regulatory framework—which dictates zero-tolerance for workplace contamination and high standards for infection prevention—acts as the ultimate non-negotiable driver, ensuring that disposable overalls remain an essential, recurring expenditure for all relevant end-user sectors. Therefore, the market trajectory is strongly upward, moderated slightly by material cost volatility and the technical difficulty in combining absolute barrier protection with maximum wearer comfort.

The Disposable Overalls Market is extensively segmented based on material, type, application, and end-user, reflecting the diverse protective needs across industries. Segmentation by material is critical as it determines the level of protection offered, ranging from basic protection via Spunbond Polypropylene (SPP) suitable for dust and light grime, to advanced chemical resistance provided by high-density polyethylene (HDPE) films, often laminated with specialized films for superior barrier properties. The complexity of regulatory compliance and the specificity of hazards encountered across different sectors necessitate this granular segmentation, allowing manufacturers to tailor products precisely to regulatory Type classifications (e.g., Type 3, 4, 5, 6).

Application-based segmentation divides the market primarily into healthcare (including surgical and examination use), industrial manufacturing (covering automotive, chemical, and general processing), construction, and environmental cleanup/remediation. The industrial segment, while highly diversified, emphasizes specialized properties such as anti-static treatment and flame resistance, crucial for mitigating risk in explosive or high-heat environments. In contrast, the healthcare segment prioritizes fluid resistance and biological barrier efficacy, often requiring sterile packaging and specialized cuff designs to interface seamlessly with other PPE components like gloves and respirators.

Understanding these segments is vital for market participants, as pricing strategies, distribution channels, and marketing efforts must align with the specific requirements of the target application. For instance, high-volume, lower-cost polypropylene suits dominate construction and general maintenance, requiring efficient, cost-optimized distribution, whereas niche, high-performance chemical suits (e.g., encapsulating suits) are sold through specialized safety distributors to specific industrial sites, commanding a premium price reflective of their certified protective capabilities and low-volume nature. The continuous evolution of environmental and biological hazards ensures ongoing demand variability within these specialized segments.

The value chain for the Disposable Overalls Market begins with the upstream sourcing of raw materials, primarily petrochemical derivatives such as polypropylene granules, polyethylene resin, and specialized chemical barrier films. This phase is characterized by high sensitivity to global oil and gas prices, which directly impacts the cost of non-woven fabric production. Key upstream activities involve polymerization, spinning, and melt-blowing processes conducted by specialized textile and chemical companies that provide high-quality base materials optimized for barrier and breathability specifications. Strategic supplier relationships and long-term contracts are essential for manufacturers to stabilize input costs and maintain consistent quality standards for the production of compliant protective fabrics, particularly those requiring specific weights and hydrostatic pressure resistance.

The core manufacturing stage involves converting these raw materials into finished garments. This midstream activity includes cutting, ultrasonic welding (for high-barrier suits), stitching, zipper attachment, quality assurance testing (crucial for regulatory compliance), and final packaging. Efficiency in manufacturing relies heavily on automation and adherence to Good Manufacturing Practices (GMP), especially for sterile products intended for the healthcare sector. Following manufacturing, the distribution channel acts as the crucial link to end-users. The distribution landscape is multifaceted, encompassing direct sales for large, institutional buyers (e.g., national healthcare systems or major chemical companies) and indirect distribution through a robust network of safety equipment distributors and industrial supply houses for smaller clients and localized construction projects.

Downstream analysis focuses on the end-user consumption pattern and post-use disposal methods. Direct channels offer manufacturers greater control over branding and pricing, ensuring specialized technical support reaches high-risk clients who require tailored protective solutions. Indirect channels, leveraging established regional distributors, provide broad market penetration and logistical efficiency for standardized, high-volume products. The increasing emphasis on sustainability is beginning to influence the downstream market, pressuring manufacturers and users alike to adopt improved disposal methods, including incineration or chemical recycling, particularly for contaminated overalls, thereby adding complexity and cost to the final stage of the product lifecycle.

Potential customers for disposable overalls span virtually every industry where physical contaminants, particulate matter, hazardous chemicals, or biological agents pose risks to workers or sensitive processes. The healthcare segment constitutes the single largest end-user group, driven by hospitals, clinics, emergency medical services, and pharmaceutical manufacturing facilities. These buyers prioritize barrier integrity against pathogens and fluids (e.g., Type 6 and Type 4 protection), demanding products that are often sterile and compliant with stringent medical device regulations. Their purchasing decisions are heavily influenced by clinical efficacy, bulk pricing, and reliable supply chain logistics, given the critical nature of PPE in preventing infectious disease transmission.

Industrial customers form the second major purchasing group, encompassing diverse sectors such as automotive finishing (where particle-free environments are mandatory), chemical processing (requiring Type 3 or Type 4 resistance), electronics assembly (demanding anti-static properties), and aerospace manufacturing. These end-users are highly sensitive to regulatory compliance (OSHA, EPA mandates) and seek solutions that offer maximum mobility and durability over extended shifts, balancing protection with ergonomic factors. Procurement in this segment is often centralized and guided by industrial safety officers who conduct thorough risk assessments to select the appropriate chemical and particulate protective classification for specific operational tasks.

Furthermore, niche but rapidly growing customer segments include construction and infrastructure maintenance, particularly for activities involving asbestos or lead abatement, and the environmental services sector focused on hazardous waste management, spill cleanup, and mold remediation. For these buyers, the cost-to-protection ratio is crucial for high-volume, temporary projects, necessitating robust, cost-effective suits that meet particulate barrier standards (Type 5). The common thread across all potential customer groups is the non-negotiable requirement for regulatory certified protection, making documented proof of compliance and third-party testing certifications mandatory elements in all purchasing decisions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $2.1 Billion |

| Market Forecast in 2033 | $3.3 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DuPont de Nemours, Inc., 3M Company, Kimberly-Clark Corporation, Lakeland Industries, Inc., Ansell Ltd., Honeywell International Inc., UVEX Safety Group GmbH & Co. KG, Kappler, Inc., International Enviroguard, Protective Industrial Products (PIP), Derekduck Industry Corp., Microgard Limited, Drägerwerk AG & Co. KGaA, Sioen Industries NV, Delta Plus Group, TIDI Products, LLC, Halyard Health, Inc., Dynarex Corporation, Medline Industries, Inc., Ambu A/S |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Disposable Overalls Market is primarily focused on enhancing two critical performance metrics: barrier protection efficiency and wearer comfort. Significant advancements have been made in non-woven fabric engineering, particularly the refinement of Spunbond-Meltblown-Spunbond (SMS) composites. Manufacturers are utilizing proprietary melt-blowing techniques to create finer microfibers, resulting in superior filtration efficiency against particulate matter while maintaining high levels of breathability. This technological evolution allows for the production of lighter, more flexible materials that still meet demanding regulatory standards, such as Type 5 protection against hazardous dry particles, which is essential for sectors like asbestos removal and pharmaceutical powder handling.

The development of advanced chemical barrier technology represents another pivotal area of innovation. Traditional disposable suits often rely on basic coatings or heavy films, which compromise comfort. Modern technology involves multilayered laminates and specialized polymeric films (such as microporous films) that utilize molecular structures to block liquid penetration (meeting Type 3 and Type 4 standards) while allowing water vapor to escape, thereby reducing heat stress and improving user compliance during long operational periods. Furthermore, ultrasonic welding and heat-sealing technologies are continuously being perfected to eliminate potential leak points inherent in traditional stitching, ensuring liquid-tight and pressure-tested seams necessary for handling hazardous liquid chemicals and maintaining maximum biological protection.

Sustainability and smart integration are emerging technological frontiers. Research is intensifying into bio-based plastics and easily recyclable materials to minimize the environmental footprint of single-use items, driven by consumer preference and regulatory mandates in Europe. Concurrently, though still nascent, the concept of "smart PPE" is gaining traction. This involves integrating miniature sensors into disposable overalls to monitor environmental factors (e.g., chemical exposure levels, temperature) or wearer vital signs. While these features add cost, they offer unprecedented safety data and real-time risk mitigation capabilities, particularly in highly toxic or confined industrial environments, representing the future direction for high-end protective solutions.

North America maintains a commanding position in the Disposable Overalls Market, characterized by early adoption of stringent occupational safety standards (enforced by OSHA and NIOSH) and a highly sophisticated, volume-driven healthcare sector. The demand is consistently high across pharmaceutical R&D, advanced manufacturing, and biological hazard control. The region’s mature regulatory infrastructure mandates the use of high-specification, certified PPE, driving preference towards premium brands and advanced protective technologies, such as chemical-resistant suits and high-filtration particle barriers. Continuous investment in high-tech industrial sectors and the centralized purchasing power of large hospital networks ensure sustained, robust market value and innovation in material science and garment design within this region.

Asia Pacific (APAC) is projected to exhibit the highest Compound Annual Growth Rate (CAGR) throughout the forecast period. This acceleration is primarily fueled by rapid urbanization, significant growth in the manufacturing and construction industries (especially in China, India, and Southeast Asian nations), and a consequential, although delayed, implementation of Western-style safety and health regulations. As local regulatory bodies mandate better worker protection, the demand for affordable, yet certified, disposable overalls skyrockets. Furthermore, the APAC region has become a crucial global production hub for non-woven fabrics and finished garments, benefiting from cost-effective labor and proximity to raw material suppliers, leading to a dual role as both a major producer and the fastest-growing consumer market.

Europe represents a stable and highly demanding market, primarily driven by strict environmental, health, and safety (EHS) directives set by the European Union. Regulatory frameworks such as REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) enforce rigorous testing and compliance requirements for protective clothing, ensuring a constant demand for high-quality, specialty chemical barrier suits (Type 3 and Type 4). The European market is also at the forefront of the sustainability transition, with a strong consumer and regulatory push towards products incorporating recycled content or designed for minimized environmental impact, influencing material choices and end-of-life disposal considerations for PPE manufacturers operating within the continent.

The Disposable Overalls Market is projected to experience a robust growth trajectory with a Compound Annual Growth Rate (CAGR) estimated at 6.5% between the forecast period of 2026 and 2033, driven by regulatory mandates and expanded industrial safety protocols globally.

The segment dominated by SMS (Spunbond-Meltblown-Spunbond) and Polypropylene Laminates holds the largest market share. These materials offer an optimal balance of cost-effectiveness, particulate filtration efficiency (Type 5), and liquid splash protection (Type 6), meeting the needs of both healthcare and industrial end-users.

Regulatory compliance is the primary, non-negotiable market driver. Standards set by organizations such as OSHA, NIOSH, and EU directives concerning chemical handling and infection control necessitate the mandatory use of certified protective apparel, thereby ensuring sustained and predictable demand across all regulated sectors.

The Asia Pacific (APAC) region is forecasted to exhibit the highest growth rate, fueled by rapid industrialization, large-scale infrastructural development, and increasing local enforcement of occupational safety regulations, particularly in emerging economies like China and India.

Key innovations focus on advanced microporous film technology and breathable multilayer laminates. These technologies maintain high barrier integrity against liquids and particulates (Type 3/4) while allowing water vapor transmission, significantly reducing heat stress and improving wearer compliance during extended shifts.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.