ID : MRU_ 433498 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

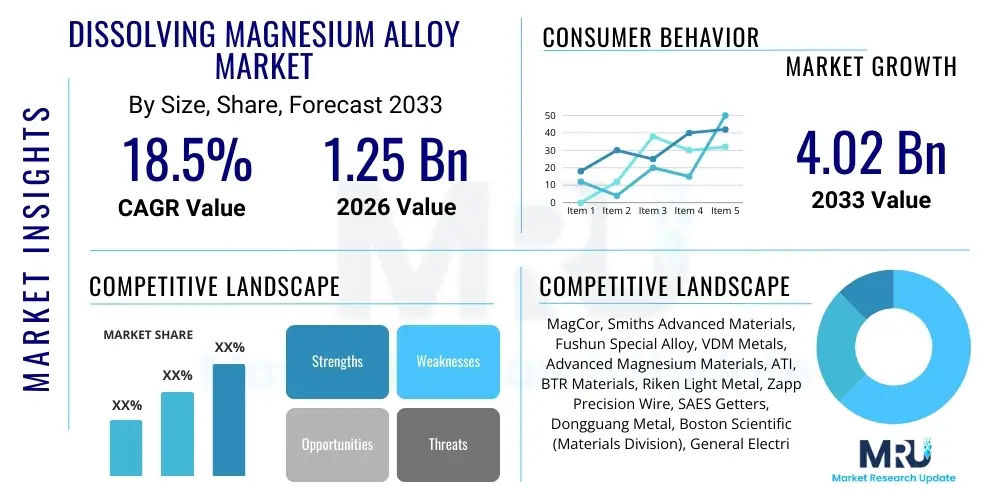

The Dissolving Magnesium Alloy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 4.02 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the escalating demand for temporary, environmentally benign materials, especially within the energy sector for advanced well completion technologies and the medical industry for biodegradable implant solutions.

The Dissolving Magnesium Alloy Market centers on materials engineered to safely degrade and dissolve in specific media (typically water or saline solutions) over predetermined timeframes, leaving minimal residue. These specialized alloys are predominantly composed of magnesium, often enhanced with trace elements like aluminum, zinc, or calcium to modulate mechanical strength, degradation kinetics, and overall biocompatibility. The primary value proposition of these materials lies in their ability to eliminate the need for mechanical retrieval processes, significantly reducing operational time and cost in complex environments such as deep subterranean wells or intricate biological systems.

Product applications are diverse, ranging fundamentally from oil and gas downhole tools, such as fracturing plugs and ball seats, to cutting-edge biomedical devices, including temporary fixation devices and biodegradable stents. In the energy sector, the benefit is optimizing multi-stage hydraulic fracturing by enabling 'frac-and-forget' operations, streamlining the well completion phase. For healthcare, dissolving magnesium alloys offer biocompatible solutions that support tissue healing before safely dissipating, thus preventing the necessity of secondary surgical removal procedures. The underlying material science focuses heavily on controlling the corrosion rate in varied environments, a critical parameter determining product performance and market viability.

The market is experiencing significant tailwinds driven by stringent environmental regulations promoting the adoption of low-residue, temporary materials, coupled with continuous technological advancements in alloying techniques that improve material strength and degradation control. The search for cost-efficient and operationally simplified methods across high-cost industries, particularly energy exploration and medical device manufacturing, acts as a primary catalyst for market expansion. Further adoption is fueled by performance improvements, allowing these alloys to withstand high pressures and temperatures characteristic of deep oil and gas reservoirs, thereby broadening the scope of viable applications globally.

The global Dissolving Magnesium Alloy market demonstrates rapid growth, characterized by significant innovation focused on optimizing degradation rates and mechanical properties. Business trends indicate a strong move towards vertical integration, where raw material suppliers are acquiring specialized processing capabilities to ensure quality control and secure proprietary alloying techniques. Key industry partnerships are forming between material manufacturers and major oilfield service companies (OFS) to co-develop next-generation downhole tools capable of withstanding extreme pressure and temperature (HPHT) environments, directly addressing the expanding complexity of unconventional resource extraction. Furthermore, patent activity is accelerating, particularly concerning novel alloying compositions and surface modification techniques designed to fine-tune dissolution profiles for specific end-use requirements.

Regional dynamics highlight North America, particularly the U.S., as the dominant market, propelled by intensive shale gas and tight oil development requiring extensive hydraulic fracturing utilizing dissolvable bridge plugs and frac balls. Asia Pacific, driven by China and India, is emerging as a critical growth region, primarily due to expanding energy exploration activities and increasing governmental investment in biodegradable medical device research. Europe maintains a strong focus on advanced materials science and regulatory frameworks, particularly concerning environmentally friendly solutions, positioning it as a key hub for research and development, especially in the medical implant segment where biocompatibility standards are exceptionally rigorous.

Segment trends underscore the dominance of the oil and gas application segment, which accounts for the largest share due to the massive volume of temporary components consumed in multi-stage fracturing. However, the medical implant segment is projected to exhibit the highest Compound Annual Growth Rate (CAGR), reflecting a paradigm shift in surgical procedures favoring absorbable materials over permanent fixtures. Technology-wise, powder metallurgy (P/M) routes are gaining traction over traditional casting and extrusion methods, as P/M offers superior control over microstructure, resulting in enhanced mechanical integrity and more predictable dissolution kinetics, crucial attributes for high-performance applications in both energy and healthcare sectors.

User queries regarding the impact of Artificial Intelligence (AI) on the Dissolving Magnesium Alloy market frequently revolve around its potential to revolutionize material discovery, optimize manufacturing processes, and predict material performance under highly variable conditions. Common concerns focus on how AI can accelerate the identification of novel alloy compositions with improved strength-to-dissolution ratios, thereby reducing lengthy and expensive traditional R&D cycles. Users also seek clarity on AI's role in predictive modeling, specifically forecasting the precise degradation timeline of alloys in complex downhole environments characterized by fluctuating pressure, temperature, and salinity, which is a key technical challenge in commercial adoption.

AI's most profound immediate impact lies in computational materials science. Machine learning algorithms are now being deployed to analyze vast datasets relating alloy chemistry, microstructure, and corrosion behavior, enabling researchers to rapidly screen thousands of potential compositions and narrow down the candidates for physical testing. This capability drastically reduces the time-to-market for new, higher-performing alloys, addressing the industry's continuous need for materials that can withstand increasingly harsh operational parameters while still degrading predictably. Furthermore, AI-driven process optimization, particularly in additive manufacturing techniques for complex dissolvable components, is leading to reduced waste, improved consistency, and lowered production costs.

Beyond material R&D, AI enhances quality control and application engineering. By integrating sensor data collected during well completion (e.g., temperature logs, pressure readings), AI models can provide real-time adjustments to completion schedules or recommend specific alloy variations optimized for a particular well profile. This level of predictive maintenance and customized material deployment minimizes failure rates and maximizes operational efficiency. The integration of AI tools, therefore, transitions the market from a reactive supply chain to a proactive, data-driven material management system, securing significant competitive advantages for early adopters in both the manufacturing and end-use sectors.

The Dissolving Magnesium Alloy market is propelled by strong drivers rooted in operational efficiency and environmental imperatives, countered by significant technological restraints, yet offering immense opportunities for diversification. The primary driver is the operational cost savings realized in the oil and gas sector by eliminating intervention methods, such as coil tubing drill-outs, after hydraulic fracturing, directly translating into faster well turnover and lower rig time costs. Furthermore, the global push toward biodegradable and environmentally friendly materials strengthens market adoption, especially as regulatory scrutiny on conventional, non-degradable materials increases.

Restraints primarily revolve around the intrinsic technical challenges of magnesium alloys. These include controlling the hydrogen gas evolution during the dissolution process, which poses risks in both downhole and biological applications if not managed effectively, and the inherent difficulty in achieving reliable mechanical strength retention at the extremely high temperatures and pressures (HPHT) found in deep unconventional wells. Consistency in degradation kinetics across diverse environmental conditions remains a material science hurdle, demanding precise alloying and surface treatments which often escalate production costs, limiting mass adoption in cost-sensitive applications.

Opportunities abound, particularly in broadening application beyond standard oilfield components. The successful integration of these alloys into complex bioresorbable medical implants, such as orthopedic screws and cardiovascular stents, presents a high-value, high-growth avenue. Additionally, the development of transient electronics and sensor packaging that must self-destruct upon mission completion opens new sectors for high-purity, custom-engineered dissolving alloys. The impact forces indicate that the market is currently experiencing high technological push, driven by specialized material science breakthroughs, coupled with moderate pull from end-users seeking enhanced operational sustainability and efficiency.

The Dissolving Magnesium Alloy market is highly segmented based on the specific material composition, the form factor (Product Type), the intended industrial application, and the ultimate end-use industry. Segmentation is crucial as the performance requirements vary dramatically; for example, alloys used in temporary bone plates require stringent biocompatibility and slow, controlled dissolution, while those used in frac plugs prioritize rapid degradation under high-pressure, high-salinity conditions. Detailed analysis of these segments reveals the current revenue concentration in the energy sector but indicates future potential lies in medical and specialized transient electronics applications, necessitating diversified R&D investment strategies.

The value chain for dissolving magnesium alloys begins with upstream analysis focusing on the secure sourcing of high-purity magnesium feedstock and alloying elements (such as rare earth elements, zinc, and calcium), which must adhere to strict quality controls, especially for biomedical applications where impurity levels are critical. Key activities in this stage include primary metal production, refining, and the manufacturing of specialized master alloys. Supply stability and pricing volatility of raw magnesium are key determinants of overall material cost and manufacturing feasibility, making long-term procurement contracts essential for downstream profitability. Specialized production techniques like powder metallurgy or hot extrusion are then employed to convert raw materials into semi-finished products with optimized microstructures.

Midstream activities involve core alloy formulation, component manufacturing, and quality control testing. Component manufacturers, utilizing specialized techniques (e.g., advanced machining, 3D printing, or injection molding), transform the alloy billets or powder into specific end products, such as frac balls or orthopedic fixation devices. Crucial steps here include controlling the grain size and applying protective temporary coatings to manage pre-application corrosion and shelf life. Strict third-party testing is required to validate mechanical integrity under extreme conditions and confirm predictable dissolution kinetics, thereby maintaining product reliability and adhering to industry certifications (e.g., API standards for energy, or FDA/CE Mark for medical devices).

Downstream analysis focuses on the distribution channel and the end-user application. The distribution model typically involves two pathways: the direct channel, where specialized alloy producers supply major original equipment manufacturers (OEMs) or large oilfield service companies (OFS) under strategic agreements; and the indirect channel, involving specialty material distributors who cater to smaller manufacturers or research institutions. End-users in the energy sector are highly sensitive to operational performance and total installed cost, prioritizing reliability and rapid deployment. Conversely, medical device buyers prioritize biocompatibility, long-term clinical efficacy, and regulatory compliance, demonstrating distinct purchasing criteria that influence supplier strategies and pricing models.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 4.02 Billion |

| Growth Rate | CAGR 18.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | MagCor, Smiths Advanced Materials, Fushun Special Alloy, VDM Metals, Advanced Magnesium Materials, ATI, BTR Materials, Riken Light Metal, Zapp Precision Wire, SAES Getters, Dongguang Metal, Boston Scientific (Materials Division), General Electric (OFS Materials), Baker Hughes (Specialty Materials), Halliburton (Materials R&D), Mitsubishi Materials, Posco, Sandvik Materials Technology, Xi'an Material Science & Engineering. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The primary customers for dissolving magnesium alloys fall into two distinct high-value industrial categories: major energy exploration and production companies (E&P) and their associated oilfield service (OFS) providers, and the global medical device manufacturing sector. In the energy sector, OFS giants like Schlumberger, Baker Hughes, and Halliburton are critical buyers, utilizing these alloys to manufacture proprietary dissolvable plugs, sealing components, and instrumentation housing required for multi-stage hydraulic fracturing, aiming for zero-intervention completion processes. These buyers prioritize reliable performance under extreme pressures and temperatures, material consistency, and supply chain security, necessitating high-volume and long-term supply agreements with alloy producers.

In the healthcare sphere, key customers include multinational medical device OEMs specializing in orthopedic trauma, cardiovascular intervention, and general surgery products. Companies such as Zimmer Biomet, Stryker, and specialized cardiovascular stent manufacturers are seeking high-purity magnesium alloys for bioresorbable implants. For these customers, the purchasing decision is heavily influenced by alloy biocompatibility, certified dissolution rates, adherence to strict regulatory standards (FDA/EMEA), and proven clinical trial success. The material must offer sufficient mechanical support during the healing phase before predictably and safely dissolving, thereby eliminating the long-term foreign body risk associated with permanent implants.

A rapidly emerging customer segment includes manufacturers in the transient electronics and defense industries. These niche buyers require small volumes of highly specialized alloys used in temporary sensors, environmental monitoring devices, or defense systems that require self-destruction capabilities to prevent sensitive technology capture. These customers are less price-sensitive than the energy sector but demand extremely precise control over degradation triggers (e.g., time, temperature, humidity) and specialized material forms, often requiring bespoke additive manufacturing solutions or ultra-thin foil production capabilities.

The technological landscape of the Dissolving Magnesium Alloy market is dominated by advancements in material processing methods aimed at achieving precise control over microstructure and surface characteristics, which are the fundamental determinants of degradation kinetics. Key technologies include advanced Powder Metallurgy (P/M) techniques, which involve atomizing the alloy into fine powders, followed by compaction and sintering or hot extrusion. P/M provides superior homogeneity, allows for the incorporation of reinforcing phases or secondary alloying elements in a controlled manner, and minimizes impurity segregation, resulting in components with highly reproducible strength and dissolution profiles compared to traditional casting.

Another crucial technological area is surface engineering and coating application. While the alloy is designed to dissolve, temporary protective coatings (often polymer-based or ceramic) are essential to prevent premature degradation during storage, transportation, and deployment. These coatings must be environmentally friendly and engineered to fail or dissolve predictably only upon reaching the target application environment (e.g., exposure to a specific temperature or fluid type downhole). Furthermore, alloying techniques utilizing rare earth elements (e.g., Yttrium, Cerium) or calcium are crucial for enhancing mechanical properties, reducing the rate of hydrogen evolution, and improving overall corrosion resistance during the crucial initial deployment phase.

The integration of Additive Manufacturing (AM), particularly Laser Powder Bed Fusion (L-PBF) and Binder Jetting, is transforming the market by enabling the production of highly complex, customized dissolvable components previously impossible with traditional machining. AM reduces material waste and allows for rapid prototyping of specialized downhole tools or patient-specific medical implants. Coupled with computational materials modeling (often AI-driven), these technologies allow manufacturers to predict material behavior more accurately and design complex geometries that optimize fluid interaction for controlled dissolution, thus defining the cutting edge of dissolving magnesium alloy material science and engineering.

The primary technical challenge is achieving a balance between high mechanical strength (necessary to withstand extreme operational pressures and loads, especially in deep wells) and predictable degradation kinetics (ensuring safe, timely, and complete dissolution without harmful residue). This requires stringent control over material purity and microstructure using advanced processing techniques like powder metallurgy.

In the oil and gas sector, these alloys are predominantly used in temporary downhole completion tools, specifically dissolvable frac plugs, ball seats, and components for isolation sleeves. Their use eliminates the costly and time-consuming mechanical retrieval (drill-out) process required after hydraulic fracturing, significantly enhancing well completion efficiency and reducing non-productive time (NPT).

Biocompatibility is critical for the medical implant segment. Magnesium alloys are naturally biodegradable and release non-toxic ions, making them suitable for temporary fixation devices and stents. High-purity alloys must be used to ensure minimal inflammatory response and controlled degradation rates that match the physiological healing timeline, avoiding adverse reactions in the human body.

North America, particularly the United States, is the largest consumer. This dominance is directly attributable to the mature and highly active shale gas and tight oil industry, which relies heavily on multi-stage hydraulic fracturing where dissolvable components are essential tools for maximizing completion efficiency and reducing overall operational costs in thousands of unconventional wells annually.

AI significantly contributes by accelerating material discovery through computational modeling, rapidly screening optimal alloy compositions and processing parameters required to achieve specific performance characteristics (strength, dissolution rate). This data-driven approach minimizes the need for extensive physical testing, drastically cutting down R&D cycles for next-generation transient materials.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.