ID : MRU_ 434331 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

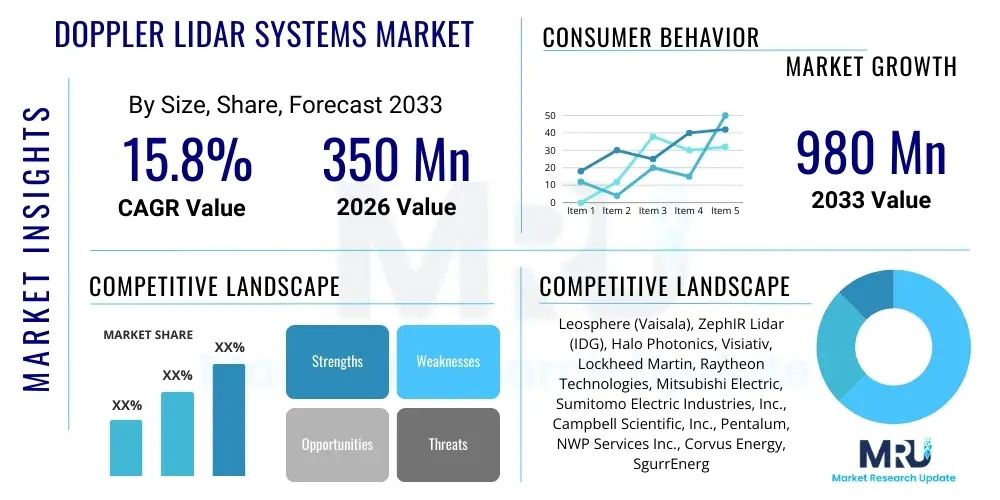

The Doppler Lidar Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at $350 Million USD in 2026 and is projected to reach $980 Million USD by the end of the forecast period in 2033.

The Doppler Lidar Systems Market encompasses advanced remote sensing technologies utilizing the Doppler effect to measure the velocity and characteristics of aerosols, particles, and air molecules within the atmosphere. These systems operate by emitting laser light and analyzing the frequency shift (Doppler shift) of the backscattered light, providing precise, real-time measurements of wind speed, turbulence, and atmospheric boundary layer height. This capability is critical for applications demanding high spatial and temporal resolution, such as wind energy forecasting, aviation safety, weather monitoring, and environmental compliance.

Doppler Lidar systems are categorized based on their technical implementation, primarily distinguishing between coherent and incoherent (or direct detection) technologies. Coherent systems are typically favored for long-range wind speed measurements in clean air environments, leveraging heterodyne detection for high sensitivity. In contrast, incoherent systems often excel in measuring aerosol scattering and particle characteristics, finding significant utility in atmospheric research and pollution monitoring. The primary benefits driving market adoption include enhanced prediction accuracy for renewable energy output, improved safety margins in air traffic control due to real-time wake vortex detection, and superior data quality compared to traditional sensor technologies like anemometers or radar for localized atmospheric phenomena.

Major applications span atmospheric science, where researchers monitor cloud dynamics and pollutant transport; defense and security, involving wind shear detection and target tracking; and the rapidly expanding wind energy sector, where these systems optimize turbine placement, monitor performance, and inform operational strategies. Driving factors include global commitments to renewable energy expansion, increasing investment in autonomous and unmanned aerial vehicle (UAV) navigation requiring high-fidelity environmental data, and regulatory pressures necessitating more precise meteorological data for public safety and infrastructure planning.

The Doppler Lidar Systems Market is experiencing robust growth fueled by the convergence of industrial automation needs and the imperative for high-resolution environmental sensing across critical infrastructure sectors. Key business trends indicate a significant shift towards solid-state and fiber-optic based systems, offering greater durability, reduced maintenance overhead, and a smaller footprint, thereby enabling broader deployment in remote and harsh environments, particularly for offshore wind farms and terrestrial grid management. Furthermore, strategic alliances between Lidar manufacturers and specialized software providers are centralizing data processing capabilities, translating raw wind data into actionable predictive insights for energy traders and utility operators, positioning integrated solutions as a primary revenue driver.

Regionally, the market is highly dynamic. Asia Pacific (APAC) stands out as the fastest-growing region, driven by massive investments in offshore and onshore wind capacity, notably in China, India, and Vietnam, alongside increasing requirements for localized severe weather forecasting. North America maintains market leadership in terms of technological adoption and research & development, propelled by governmental defense expenditures and the expansion of the commercial aviation sector seeking advanced wake vortex detection and terminal area monitoring. Europe, supported by stringent climate goals and a mature wind energy sector, focuses heavily on implementing Lidar for operational efficiency and site assessment of renewable projects, often utilizing ground-based and nacelle-mounted configurations.

Segment trends highlight the dominance of the Wind Energy application segment due to favorable regulatory landscapes promoting renewable generation, driving demand for both short-range and long-range measuring capabilities. Technology-wise, Coherent Doppler Lidar systems hold the largest market share, valued for their long-range accuracy essential for pre-construction site assessment and power performance verification. However, the direct-detection Lidar segment is projected to exhibit the highest CAGR, primarily due to its increasing utility in atmospheric research and lower cost points, making it attractive for large-scale network deployment for localized weather data collection. The convergence of Lidar technology with Artificial Intelligence (AI) for enhanced signal processing and data interpretation represents a major vertical segment growth opportunity, redefining measurement precision and system autonomy.

Common user questions regarding AI's impact on Doppler Lidar Systems revolve around three core themes: improving signal-to-noise ratio (SNR) in complex atmospheric conditions, automating data interpretation for predictive maintenance and operational planning, and the potential for AI-driven sensor fusion to enhance situational awareness beyond the capabilities of a single sensor. Users frequently inquire about how machine learning algorithms can accurately distinguish between atmospheric phenomena noise and actual wind vector signals, especially in turbulent or low-visibility settings, seeking improvements in data fidelity and reliability. Furthermore, there is significant interest in utilizing neural networks to analyze vast streams of Lidar data to predict localized weather events (e.g., microbursts, wind shear) or optimize dynamic turbine control in real time, moving beyond traditional deterministic models to AI-enabled probabilistic forecasting, thereby reducing latency and increasing the economic value of the generated data.

The integration of Artificial Intelligence, specifically deep learning and computer vision techniques, is transforming the operational paradigm of Doppler Lidar Systems. AI algorithms are instrumental in filtering out environmental noise, compensating for atmospheric inhomogeneities, and drastically improving the speed and accuracy of target detection and tracking, which is crucial in defense and aviation applications. By processing complex backscatter profiles, AI models can rapidly classify atmospheric layers, identify boundary layer heights with unprecedented precision, and correct for systematic measurement errors that previously required extensive manual calibration. This automated processing not only enhances the technical performance of the Lidar unit but also lowers the required expertise for operational deployment, democratizing the technology.

Furthermore, AI is pivotal in maximizing the utility of the collected Lidar data in end-user applications. In the wind energy sector, machine learning models analyze historical Lidar measurements combined with SCADA (Supervisory Control and Data Acquisition) data to create highly refined digital twins of wind farms, optimizing energy capture and minimizing load variations. For meteorological agencies, AI facilitates the rapid assimilation of Lidar observations into numerical weather prediction (NWP) models, significantly improving short-term forecast accuracy for localized, high-impact weather. This shift towards AI-powered data analytics transforms the Lidar system from a mere measurement device into a sophisticated predictive asset, driving greater ROI across all vertical markets.

The Doppler Lidar Systems Market is principally driven by the explosive growth in the renewable energy sector, which demands precise pre-construction site assessments and continuous operational monitoring to maximize efficiency and secure financing. However, the market faces significant restraints, primarily stemming from the high capital expenditure required for sophisticated coherent Lidar units and the technical complexity associated with deploying and maintaining these sensitive instruments in harsh environments. Opportunities emerge from the miniaturization of components and solid-state advancements, which promise cost reduction and increased reliability, opening doors for widespread adoption in autonomous vehicles and distributed urban atmospheric networks. These internal dynamics are constantly influenced by the external impact forces of technological advancement, regulatory mandates, and macroeconomic trends related to energy transition and climate adaptation strategies globally.

Key drivers include the global push for decarbonization and the resultant surge in wind and solar farm development, requiring highly accurate wind resource assessments (WRAs) that Lidar systems reliably provide, especially at nacelle height or offshore. The continuous improvement in Lidar technology, such as the introduction of pulsed fiber lasers and robust optical components, also lowers the total cost of ownership over time, making Lidar increasingly competitive against traditional meteorological masts, particularly at heights exceeding 100 meters. Furthermore, aviation safety regulations increasingly require real-time detection of hazardous phenomena like wake vortices and low-level wind shear around airports, creating a niche but highly demanding market segment for specialized Doppler Lidar systems.

Restraints center around the vulnerability of complex optical systems to contamination (dust, humidity, fog), which requires advanced filtration and climate control mechanisms, escalating maintenance costs. The inherent high cost of specialized components, such as high-power lasers and sophisticated detection electronics, remains a barrier to entry for smaller users. Opportunities lie in developing integrated Lidar solutions for autonomous mobility (e.g., Level 4 and 5 ADAS requiring 4D wind sensing for stability) and leveraging governmental funding for climate resilience and atmospheric research programs, particularly those focused on monitoring greenhouse gas fluxes and regional air quality. The impact forces underscore that policy shifts favoring clean energy investment or imposing stricter environmental monitoring requirements will directly accelerate market growth, while global supply chain disruptions impacting high-precision optical components pose continuous operational risks.

The Doppler Lidar Systems Market is meticulously segmented across several critical dimensions, enabling a granular understanding of demand dynamics and technological uptake across various end-user industries. Primary segmentation includes Technology Type (Coherent vs. Incoherent/Direct Detection), Application (Wind Energy, Aviation, Meteorology, Research), and Deployment (Ground-based, Nacelle-mounted, Airborne/Mobile). Analyzing these segments reveals that technological maturity and application-specific performance requirements dictate market share distribution. For instance, the demand for Coherent Lidar is largely tied to commercial applications requiring long-range velocity measurement, while the affordability and atmospheric profiling capability of Incoherent Lidar drive its adoption in governmental research institutions and weather services.

The application segment focused on Wind Energy currently represents the largest revenue share, primarily utilizing Doppler Lidar for crucial tasks such as turbine power curve measurements, site suitability assessments, and operational wind field mapping necessary for wake steering. The Meteorology segment, though smaller in revenue, is critical for future innovation, as government agencies invest heavily in developing networks for enhanced weather forecasting and pollution transport modeling. Furthermore, the deployment segment highlights a strategic shift; while ground-based systems remain essential for pre-construction site work, nacelle-mounted units are gaining traction for operational optimization and performance monitoring throughout the turbine lifecycle, reflecting the industry's focus on maximizing efficiency post-commissioning.

Future growth is expected to be concentrated in segments benefiting from miniaturization and cost reduction. Specifically, the integration of Doppler Lidar into airborne and mobile platforms, including UAVs and autonomous land vehicles, is anticipated to experience accelerated growth, driven by the need for dynamic, real-time environmental data acquisition that traditional fixed-site systems cannot fulfill. This continuous evolution in application requirements necessitates that manufacturers focus on developing hybrid systems that offer robust performance across varying ranges and atmospheric conditions, ensuring flexibility in deployment and maximizing cross-sector applicability, particularly in the intersection of climate science and smart infrastructure.

The value chain for Doppler Lidar Systems is characterized by high levels of specialization and technical complexity, beginning with the highly integrated supply of upstream components. The upstream segment involves the production of critical enabling technologies, including specialized fiber optic components, high-power pulsed lasers (often near-infrared), high-sensitivity photodetectors (e.g., avalanche photodiodes or balanced detectors), and advanced microprocessors for signal processing. Since precision optics and laser sources are highly proprietary and often sourced from a limited number of specialized vendors, cost control and supply chain stability in this segment are paramount to the downstream manufacturing process. Manufacturers must maintain deep partnerships here to ensure component quality and reliability, directly impacting the final system performance.

The midstream involves the core manufacturing, assembly, integration, and stringent calibration of the Lidar system itself. Companies focus on sophisticated integration techniques to package complex optics and electronics into rugged, environmentally sealed enclosures suitable for field deployment. This stage includes developing proprietary software for real-time data acquisition, noise filtering, and wind vector calculation. Distribution channels are varied: direct sales are common for large government or utility contracts, allowing manufacturers to provide customization and integration support. Indirect distribution utilizes specialized value-added resellers (VARs) and integrators, particularly in the fragmented wind energy consulting market, where local expertise in site assessment and regulatory compliance is crucial.

The downstream segment centers on installation, data analysis, maintenance, and providing consulting services. End-users require highly specialized support to interpret the vast data generated by the Lidar systems and integrate it into their operational models (e.g., SCADA systems for wind farms or NWP models for weather services). The trend is moving towards Lidar-as-a-Service (LaaS), where the Lidar manufacturer or third-party service provider retains ownership of the hardware, providing only the processed, actionable data to the client, thereby lowering the client's capital expenditure burden. This shift significantly enhances the service component of the value chain, focusing on data intelligence rather than merely hardware provision.

Potential customers for Doppler Lidar Systems are diverse, spanning multiple high-stakes sectors that rely critically on accurate, high-fidelity atmospheric and wind data. The largest single buyer segment remains the renewable energy industry, specifically utility-scale wind farm developers and independent power producers (IPPs). These customers require Lidar for comprehensive pre-construction wind resource assessments to secure project financing, and increasingly, for nacelle-mounted units used for operational performance testing (power curve measurements) and real-time wind field monitoring to optimize turbine arrays and implement wake steering strategies effectively. Lidar offers a cost-effective, high-altitude alternative to traditional met masts, making it essential for complex terrains and offshore projects.

Another crucial end-user group comprises governmental agencies, encompassing national meteorological services (e.g., NOAA, ECMWF) and defense organizations. Meteorological agencies purchase Lidar systems for research into atmospheric boundary layers, cloud dynamics, and severe weather prediction, integrating the data directly into national weather models. Defense customers utilize specialized, high-power Lidar for applications such as counter-UAV defense, long-range wind field mapping for ballistic calculations, and surveillance, emphasizing robustness and mobility. These customers prioritize system reliability, long-term support, and strict compliance with national security and data protocols.

Furthermore, the aviation sector represents a growing customer base, including airport authorities and air navigation service providers (ANSPs). These entities invest in Doppler Lidar for airport terminal area safety, specifically for the real-time detection and mitigation of dangerous wind shear and wake vortices generated by heavy aircraft during takeoff and landing. The need to improve air traffic capacity and safety margins in congested airspace drives the demand for specialized, short-range pulsed Lidar systems. Lastly, academic and private research institutions constitute a consistent buyer base, utilizing Lidar for environmental monitoring, air quality studies, and climate change impact assessments, typically focusing on flexible, research-grade systems that allow for custom integration and experimentation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $350 Million USD |

| Market Forecast in 2033 | $980 Million USD |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Leosphere (Vaisala), ZephIR Lidar (IDG), Halo Photonics, Visiativ, Lockheed Martin, Raytheon Technologies, Mitsubishi Electric, Sumitomo Electric Industries, Inc., Campbell Scientific, Inc., Pentalum, NWP Services Inc., Corvus Energy, SgurrEnergy (Wood Group), NRG Systems, Avent Lidar Technology, Optiflux Lidar Solutions, Coherent Inc., OptiSense, LDI Technologies, Sigma Space Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Doppler Lidar Systems Market is defined by continuous innovation focused on improving range, reliability, spectral purity, and reducing overall system size and cost. A primary technological area is the transition from bulk optics to fiber-optic based systems, which offers superior alignment stability, ruggedness, and reduced vulnerability to environmental fluctuations. Fiber Lidar leverages high-power fiber lasers coupled with advanced single-mode optical fibers for beam delivery and collection, significantly simplifying the system architecture and enabling modular design, which is essential for deployments in challenging environments like offshore wind platforms where maintenance access is limited.

Furthermore, significant research and development efforts are concentrated on the advancement of solid-state Doppler Lidar, often utilizing integrated photonics or micro-electromechanical systems (MEMS) scanning mirrors. Solid-state technology aims to eliminate moving parts, which are the primary failure points in traditional mechanical scanning systems. This innovation is critical for unlocking mass-market applications, particularly in the autonomous vehicle sector where small, robust, and cost-effective sensors are mandatory. While solid-state Lidar for atmospheric wind measurement is still maturing, breakthroughs in array detectors and chip-scale frequency stabilization are rapidly enhancing their performance capabilities, promising a substantial decrease in system size and power consumption.

A third critical development involves the sophistication of signal processing and data retrieval algorithms. Modern systems rely heavily on advanced digital signal processing (DSP) to extract coherent Doppler information from weak, noisy backscatter signals, particularly at extended ranges. Recent integration of Artificial Intelligence and deep learning techniques (as mentioned previously) enables better rejection of atmospheric noise and automated calibration routines, resulting in higher data availability and accuracy. Key technologies also include frequency-modulated continuous-wave (FMCW) Lidar, which offers high resolution and superior measurement stability compared to traditional pulsed systems, becoming increasingly favored for short- to medium-range applications requiring precise velocity mapping.

The North American market benefits from strong regulatory support for renewable energy projects, particularly through state-level mandates and federal incentives that necessitate rigorous site assessment studies, often favoring Lidar over traditional masts due to its cost-efficiency at high altitudes. Academic research institutions, heavily funded by government grants, continuously drive demand for cutting-edge Lidar systems used in climate modeling and boundary layer studies, ensuring sustained technological adoption. While the market is technologically mature, the focus remains on enhancing operational resilience, reducing the size and weight of airborne systems, and integrating Lidar data into wider smart grid infrastructure platforms.

Specific growth areas include the integration of Doppler Lidar for airport operations (e.g., Dallas/Fort Worth, JFK) to manage increasing air traffic density safely by mitigating wind shear and wake turbulence hazards. The market growth here is moderated slightly by the initial high capital cost but is sustained by the high value placed on data fidelity and long-term system reliability, positioning North America as a leader in high-performance system adoption.

Regulatory frameworks, such as IEC standards for power performance testing (PPT), explicitly recognize Lidar as an acceptable measurement tool, accelerating its incorporation into standard industry practices. Beyond wind energy, European meteorological services (like EUMETSAT) are significant users, deploying Lidar networks for advanced pollution monitoring, particularly in urban areas, and integrating high-resolution wind data into regional Numerical Weather Prediction models. Innovation is often driven by collaborative projects involving industry and EU-funded research, focusing on developing highly durable and autonomous systems for remote, often sub-zero, environments.

The market faces challenges related to intense pricing pressure due to saturation in certain segments, but opportunities abound in the emerging hydrogen economy and further expansion into the deep-sea offshore wind market. European emphasis on environmental stewardship ensures a consistent demand for advanced atmospheric sensing capabilities beyond purely commercial energy applications, supporting a strong ecosystem of specialized Lidar consulting and service providers.

The APAC market is characterized by a mix of domestic manufacturing capability (especially in China) and reliance on imports of high-end, coherent Lidar systems from Western manufacturers for high-precision applications. Price sensitivity is higher in this region compared to North America and Europe, leading to strong competition and a growing focus on developing cost-effective, medium-range Lidar solutions suitable for large-scale network deployment. India’s aggressive push for solar and wind capacity, coupled with the necessity for better pollution monitoring in highly congested metropolitan areas, positions it as a significant emerging market for Doppler Lidar.

Key growth catalysts include governmental modernization initiatives in air traffic management (ATM) and defense, particularly in nations facing complex territorial security challenges. The region's diverse and often challenging topography, coupled with high atmospheric aerosol loading, creates specific technical demands for Lidar systems that can reliably operate in dusty, humid, and turbulent conditions, driving innovation in robust direct-detection Lidar technology.

In Latin America, regulatory environments are maturing, and project developers are increasingly relying on high-quality Lidar data to de-risk investments and secure project financing, moving away from reliance on short-term data collection methods. South Africa, with its strong climate science institutions and commitments to energy transition, uses Lidar extensively for atmospheric research and solar forecasting, complementing its growing wind sector. However, market adoption can be volatile due to macroeconomic instability and reliance on imported technology and technical expertise.

Opportunities in MEA are focused on environmental monitoring related to oil and gas operations (e.g., flare stack emissions) and addressing regional challenges like dust storms and sand movement, requiring Lidar systems built for extreme heat and high particulate concentrations. The market remains smaller than other regions but shows high potential growth correlated directly with successful execution of national renewable energy targets (e.g., Saudi Arabia's Vision 2030 and Brazil's wind expansion plans).

Coherent Doppler Lidar systems utilize heterodyne detection, mixing the backscattered light with a local oscillator to measure the frequency shift, providing high sensitivity and long-range capability, essential for wind energy assessment. Incoherent (or Direct Detection) systems measure the spectral profile directly, often using high-spectral-resolution filters, and are typically better suited for measuring aerosol and molecular backscatter, common in atmospheric research and pollution monitoring.

Offshore wind projects heavily rely on Lidar for comprehensive Wind Resource Assessment (WRA) prior to construction, often deploying them on buoys or fixed platforms to accurately measure wind profiles up to 200 meters. Operationally, nacelle-mounted Lidar systems are used for real-time wind field mapping and wake steering strategies to maximize energy yield and reduce structural loads on massive offshore turbines.

Doppler Lidar systems are crucial for airport safety by providing real-time, three-dimensional mapping of the atmospheric environment around runways. They are specifically deployed to detect hazardous micro-phenomena such as wake vortices (air turbulence left by aircraft) and low-level wind shear, allowing air traffic controllers to adjust approach and departure schedules promptly, significantly reducing accident risk.

While mechanical-scanning Lidar dominates current atmospheric measurement, solid-state (non-moving parts) Doppler Lidar is rapidly emerging, especially as technological advances are ported from the autonomous vehicle sector. Solid-state systems promise significant cost reduction, improved durability, and miniaturization, which will accelerate adoption in large-scale urban sensor networks, UAV integration, and potentially lower the barrier to entry for smaller developers.

The primary restriction is the high initial capital investment required for high-performance coherent systems, which can deter smaller organizations or projects with limited budgets. Additionally, the sensitivity of the complex optical components to environmental factors (e.g., dust, heavy precipitation) necessitates specialized maintenance procedures and robust system enclosures, contributing to a higher total cost of ownership compared to simpler meteorological instruments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.