ID : MRU_ 432602 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

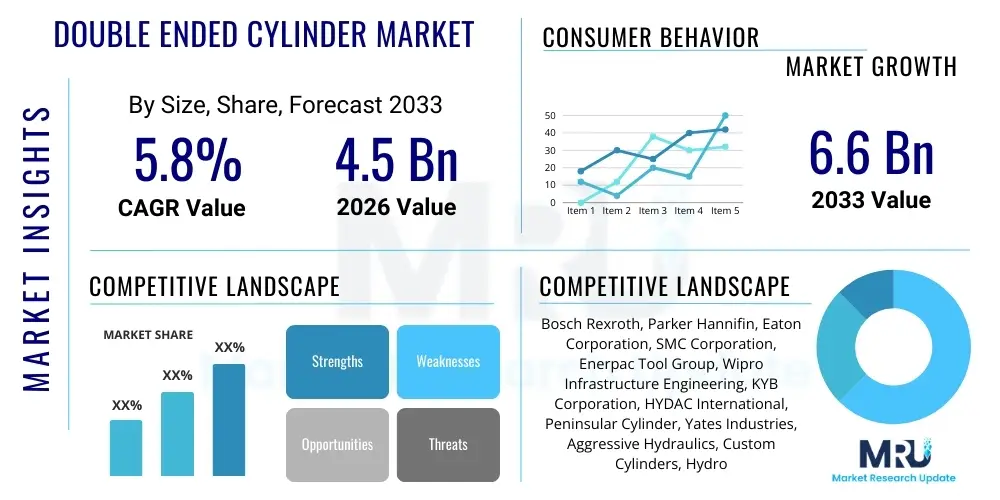

The Double Ended Cylinder Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $4.5 Billion in 2026 and is projected to reach $6.6 Billion by the end of the forecast period in 2033.

The Double Ended Cylinder Market encompasses hydraulic and pneumatic actuators characterized by a piston rod extending from both ends of the cylinder barrel. This design allows for equal force output and speed during both extension and retraction strokes, making them indispensable components in applications requiring precise control, symmetry, and high operational frequency. These cylinders are primarily utilized in heavy industrial machinery, construction equipment, marine steering systems, and sophisticated manufacturing processes where reliability and balanced performance are paramount. Their robust construction and capability to handle large forces under demanding conditions ensure their sustained demand across diversified industrial sectors globally, driving continuous innovation in sealing and material technology.

The product description centers on high efficiency and symmetrical operation. Major applications span industrial automation, mobile hydraulics (especially steering and lift applications in construction and mining vehicles), aerospace testing, and specialized material handling systems. The key benefits derived from using double ended cylinders include increased rigidity, simplified system design due to their symmetrical characteristics, high operational longevity, and superior control accuracy compared to single-rod designs. Furthermore, their design inherently balances side-loading forces, contributing to reduced wear and extended service life in high-cycle environments, positioning them as essential elements in high-performance hydraulic circuits.

Driving factors for market expansion include the global surge in infrastructure development, particularly in emerging economies, which fuels demand for heavy machinery and material handling equipment. Increased adoption of automation and robotics in manufacturing processes requires precise, repeatable actuation, directly boosting the deployment of high-specification double-ended cylinders. Additionally, ongoing technological advancements focused on improving pressure ratings, integrating smart sensing capabilities, and developing corrosion-resistant materials are broadening the scope of application, particularly in harsh environments such as offshore drilling and chemical processing plants, thus ensuring sustained market growth throughout the forecast period.

The Double Ended Cylinder Market exhibits strong momentum, driven primarily by robust business trends centered on industrial digitalization and the push toward high-precision manufacturing. Key business trends include increasing strategic alliances between component manufacturers and major OEMs to customize hydraulic solutions, alongside substantial investments in developing compact, energy-efficient cylinders that meet stringent environmental regulations. The market is also seeing a shift towards cylinders made from lightweight, high-strength materials to improve the overall fuel efficiency and performance of mobile machinery. This trend is further supported by the growing aftermarket service segment, which provides critical maintenance and replacement components, ensuring operational continuity for end-users and stabilizing market revenues.

Regional trends indicate that the Asia Pacific (APAC) region is projected to be the fastest-growing market, largely due to rapid industrialization, massive investments in infrastructure projects, and the expansion of the regional manufacturing base, particularly in China and India. North America and Europe maintain leading market shares, driven by established automotive, aerospace, and advanced manufacturing sectors that prioritize high-quality, smart hydraulic systems integrated with IoT capabilities. Growth in these mature regions is focused more on replacement and technological upgrade cycles rather than sheer volume expansion, emphasizing product performance and compliance with safety standards such as those enforced by OSHA and the European Machinery Directive.

Segment trends highlight the dominance of hydraulic double ended cylinders over their pneumatic counterparts, especially in applications requiring high force and rigidity, such as metal forming and heavy lifting. By application, the construction and mining segment remains the largest consumer, though rapid growth is observed in the marine and offshore sector, driven by increasing global trade and exploration activities necessitating reliable steering and motion control systems. Furthermore, the segment focusing on integrated sensor technology—"smart cylinders"—is experiencing the highest compound annual growth, reflecting the broader industrial shift toward predictive maintenance and real-time operational monitoring across all major end-user verticals, thereby enhancing system reliability and reducing downtime significantly.

User queries regarding AI's impact on the Double Ended Cylinder Market predominantly revolve around themes of predictive maintenance, autonomous operation of machinery, and optimization of manufacturing processes. Users seek to understand how machine learning models can process real-time sensor data (pressure, temperature, position) collected from double-ended cylinders to anticipate failures, thereby minimizing unscheduled downtime. Furthermore, common questions address the role of AI in optimizing the energy consumption of hydraulic systems and how autonomous vehicles (like mining trucks or construction robots) utilize precise, AI-controlled cylinder movements. The key expectation is that AI integration will transform these mechanical components into 'smart actuators', enhancing reliability, operational efficiency, and longevity across highly demanding industrial applications.

The Double Ended Cylinder Market is significantly influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO). Key drivers include the global trend toward increased industrial automation, demanding precise and reliable actuation components, and accelerated infrastructure spending worldwide, particularly in developing nations. Restraints primarily involve the high initial cost of advanced hydraulic systems, the volatility in raw material prices (especially steel and specialized alloys), and the technical complexity associated with integrating smart sensors and electronic control units into traditional hydraulic circuits. Opportunities arise from the transition to energy-efficient fluid power systems, the potential for market expansion in specialized applications such as deep-sea exploration and renewable energy infrastructure (wind turbine pitch control), and the growing demand for retrofit solutions incorporating advanced diagnostics.

The impact forces driving market development are substantial, centered on technological substitution and economic cycles. The rapid pace of technological innovation in sealing materials (reducing friction and improving high-temperature performance) and piston rod coatings (enhancing corrosion resistance) continually elevates product performance standards. Moreover, the stringent regulatory environment regarding industrial safety and environmental impact compels manufacturers to adopt cleaner, leak-free hydraulic systems, favoring high-quality, precision-engineered double ended cylinders. Economic impact forces are tied directly to capital expenditure in the manufacturing and construction sectors; when these sectors experience growth, the demand for new equipment incorporating these specialized cylinders surges proportionally, indicating a strong cyclical correlation between global GDP and market revenue growth.

However, restraining forces, particularly the intense competition from alternative actuation technologies like high-power electric linear actuators, pose a continuous challenge. While hydraulics still offer superior power density for heavy-duty tasks, electric alternatives are gaining ground in medium-duty and precision positioning applications due to their simplified maintenance and enhanced energy efficiency in certain operational profiles. Overcoming these restraints necessitates continuous investment in R&D to maintain the hydraulic advantage in power output while simultaneously addressing energy efficiency concerns and simplifying integration through modular design, thus securing the market position of double-ended cylinders against technological substitutes and ensuring long-term viability in diverse operational environments.

The Double Ended Cylinder Market is segmented comprehensively based on several critical parameters including the type of fluid medium (hydraulic vs. pneumatic), design type (tie rod, welded, or specialized mounting), operating pressure range, and the critical application sectors (end-users). This segmentation allows for a detailed analysis of market dynamics, identifying specific high-growth niches and understanding tailored customer requirements across different industries. The distinction between hydraulic and pneumatic cylinders is fundamental, as hydraulic units dominate applications requiring high force and positional rigidity, whereas pneumatic units are preferred for lighter loads requiring faster cycle times and lower installation costs. Furthermore, understanding the primary end-user segment is vital for strategic market planning, as the demands of the mobile machinery sector differ significantly from those in static industrial automation environments.

The value chain for the Double Ended Cylinder Market begins with upstream activities involving the sourcing and processing of raw materials, primarily high-grade steel, specialized aluminum alloys, and advanced sealing materials (e.g., PTFE, high-performance polyurethanes). Key upstream participants include metal foundries, precision machining firms, and material science companies specializing in coatings and sealing technologies. The efficiency and quality of these raw components directly influence the final product's performance and longevity, making reliable sourcing and consistent quality control at this stage crucial for manufacturers. Price volatility in base metals remains a significant upstream risk that manufacturers must actively manage through forward contracts and supply chain diversification strategies.

The core value addition occurs in the midstream manufacturing phase, involving precision machining of cylinder barrels, piston rods, and heads, followed by complex assembly and rigorous testing (including pressure and leakage tests). Leading manufacturers often integrate advanced technologies, such as robotic welding and automated honing, to achieve micro-level tolerances necessary for high-performance cylinders. Distribution channels represent the downstream segment, involving both direct sales to large Original Equipment Manufacturers (OEMs) and indirect sales through a network of specialized fluid power distributors, system integrators, and maintenance, repair, and overhaul (MRO) service providers. Direct sales facilitate deep customization and long-term supply agreements, whereas indirect channels ensure broad market penetration and provide local technical support and rapid access to spare parts.

Both distribution models play distinct yet complementary roles. Direct channels are critical for securing large, recurring orders from major industrial and mobile equipment manufacturers, where custom specifications and integration support are mandatory. Indirect distribution, leveraging specialized distributors, is essential for reaching smaller end-users, providing localized inventory, and offering technical expertise in system installation and troubleshooting. After-sales service, including maintenance contracts and provision of genuine replacement parts, forms the final layer of the value chain. This service component not only generates stable, long-term revenue streams but also reinforces customer loyalty and provides manufacturers with valuable field data for continuous product improvement, completing the cyclical nature of the market value chain.

The primary end-users, or potential customers, of double ended cylinders are highly diversified, spanning multiple heavy industries that rely on robust, high-force linear motion capabilities. Major segments include Original Equipment Manufacturers (OEMs) within the construction and mining sectors, who require these components for precision steering mechanisms, robust articulation systems, and primary boom actuation in excavators, loaders, and large haul trucks. These buyers prioritize cylinders with high durability, exceptional sealing integrity, and corrosion resistance to withstand challenging outdoor and high-impact operational environments. The purchasing decisions in this segment are heavily influenced by the total cost of ownership (TCO) and the guaranteed mean time between failures (MTBF).

Another significant customer base resides in the industrial manufacturing sector, particularly in metal forming presses, specialized test rigs (aerospace component testing), and high-throughput automation lines where precise, rapid, and symmetrical movements are crucial. Customers in industrial automation often demand cylinders integrated with position sensors (LVDTs or magnetostrictive sensors) to facilitate closed-loop control and integration into sophisticated Programmable Logic Controller (PLC) systems. For these customers, the primary drivers are positional accuracy, repeatability, and seamless compatibility with Industry 4.0 infrastructure, making 'smart' hydraulic solutions particularly attractive for process optimization and quality control.

Furthermore, the marine and offshore industry constitutes a vital customer segment, utilizing double-ended cylinders extensively in ship steering gear, stabilizer fins, and specialized deck machinery such as winches and cranes. Due to the corrosive saltwater environment, these end-users require cylinders manufactured with specialized materials and coatings, demanding compliance with strict international maritime classification standards (e.g., DNV, ABS). The agriculture sector, particularly large-scale smart farming operations utilizing highly articulated implements and high-capacity machinery, also represents a growing customer segment, seeking durable and weather-resistant hydraulic components to ensure field productivity and operational longevity during critical planting and harvesting cycles.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $4.5 Billion |

| Market Forecast in 2033 | $6.6 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bosch Rexroth, Parker Hannifin, Eaton Corporation, SMC Corporation, Enerpac Tool Group, Wipro Infrastructure Engineering, KYB Corporation, HYDAC International, Peninsular Cylinder, Yates Industries, Aggressive Hydraulics, Custom Cylinders, Hydroline, Jiangsu Hengli Hydraulic, Jiangsu Tailong, Komatsu, Caterpillar, John Deere, Vestas, Siemens Gamesa |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Double Ended Cylinder Market is rapidly evolving, moving beyond conventional mechanics to integrate advanced materials science and digital intelligence. A primary focus is the development and implementation of Smart Cylinders, which incorporate embedded position sensors (such as magnetostrictive linear position sensors), pressure transducers, and temperature sensors directly into the cylinder body. These integrated technologies enable real-time monitoring of operational status, stroke position, and internal fluid condition. This digital feedback loop is critical for implementing condition-based monitoring programs, allowing end-users to shift from scheduled maintenance to proactive, predictive maintenance, thereby significantly boosting system uptime and operational reliability across demanding applications like offshore drilling rigs and autonomous mining fleets.

Material innovation represents another cornerstone of the current technology landscape. Manufacturers are increasingly utilizing advanced composite materials and high-strength, lightweight alloys for components such as the piston rod and cylinder barrel. This is driven by the necessity to reduce the overall weight of mobile hydraulic systems without compromising strength or durability, addressing the dual demands for increased payload capacity and improved fuel efficiency in construction and transport sectors. Furthermore, significant advancements are being made in surface treatment technologies, including specialized coatings (e.g., ceramic-metallic coatings, hardened chrome alternatives) that offer superior resistance to corrosion, abrasion, and cavitation, thus extending the cylinder's operational life in highly aggressive environments and reducing the frequency of costly overhauls and replacements.

Furthermore, technology is focused on enhancing sealing performance to minimize internal and external leakage, which is crucial for maximizing hydraulic system efficiency and complying with strict environmental mandates. The adoption of optimized seal geometry, often coupled with new materials like high-durability polyurethanes and proprietary elastomers, ensures tighter sealing under high pressure and temperature fluctuations. Finally, digitalization extends to manufacturing itself, where Computer-Aided Engineering (CAE) and Finite Element Analysis (FEA) tools are used extensively to simulate stress distribution and thermal performance during the design phase. This ensures that new double ended cylinder designs are robustly optimized for maximum performance and minimal material use before physical prototypes are even created, accelerating time-to-market for specialized, high-performance actuation solutions.

The primary advantage is symmetrical operation, meaning the cylinder provides equal force and speed during both extension and retraction strokes because the effective surface area of the piston is identical on both sides, which is essential for steering and precision control applications.

The major end-users are the construction and mining industry, due to their reliance on heavy mobile machinery, followed closely by industrial automation, material handling, and the marine/offshore sector for robust steering and lifting systems.

Technological innovation impacts durability through the use of advanced materials, such as high-strength alloys and specialized piston rod coatings (e.g., chrome alternatives), and improved sealing technologies that resist abrasion and high temperatures, leading to extended MTBF.

Digitalization enables the creation of 'smart cylinders' by integrating sensors for real-time data collection on position, pressure, and temperature. This data is crucial for implementing AI-driven predictive maintenance and closed-loop control systems, optimizing operational efficiency.

Hydraulic cylinders use incompressible fluid to generate significantly higher force and provide better positional rigidity, suitable for heavy lifting. Pneumatic cylinders use compressed air, offering faster cycle speeds and lower installation costs, ideal for lighter loads and rapid automation tasks.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.