ID : MRU_ 432578 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

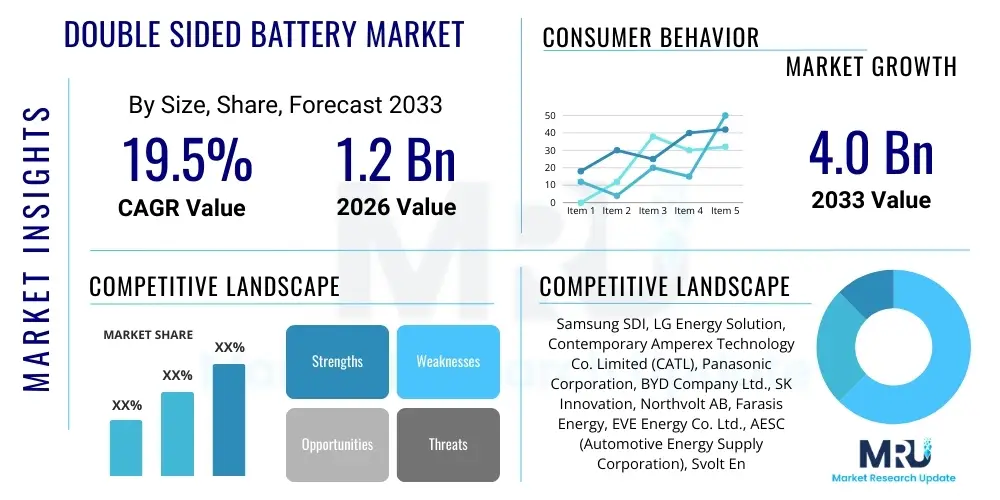

The Double Sided Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.5% between 2026 and 2033. The market is estimated at $1.2 Billion in 2026 and is projected to reach $4.0 Billion by the end of the forecast period in 2033.

The Double Sided Battery Market encompasses advanced energy storage solutions characterized by current collection tabs or connections situated on both the top and bottom surfaces of the cell. This design fundamentally differs from traditional single-sided configurations by enhancing power density, improving thermal dissipation capabilities, and optimizing cell utilization within compact module architectures. The product is primarily an evolution in lithium-ion and emerging solid-state battery technology, aiming to overcome inherent limitations related to high-rate charge and discharge cycles, which often generate significant internal heat in standard battery designs. The improved current pathway management facilitated by the double-sided configuration allows for superior performance characteristics essential for high-demand applications, particularly within the electric vehicle (EV) sector and utility-scale energy storage systems.

Major applications of double sided batteries span across high-performance electric vehicles, premium consumer electronics requiring extended operational lifetimes and rapid charging, and large-scale grid storage facilities where efficiency and longevity are paramount. In EVs, this architecture enables faster acceleration, longer range retention under stress, and better integration into structural battery packs (cell-to-pack designs). The primary benefits derived from adopting double-sided structures include significantly reduced internal resistance, leading to less energy loss during operation and thereby improving overall battery efficiency. Furthermore, the enhanced thermal management inherent in this design substantially extends the cycle life of the battery, addressing a critical concern for both consumers and commercial operators regarding battery durability and replacement costs.

Key driving factors propelling the expansion of this market include the relentless global push toward electrification in transportation, stringent governmental regulations mandating higher energy efficiency in battery systems, and rapid advancements in battery materials science that support thinner, lighter, and more complex internal cell designs. The increasing investment by major automotive OEMs and battery manufacturers (Giga factories) into next-generation battery technologies further validates the commercial viability and technological necessity of double-sided solutions. As manufacturing processes become more refined and scalable, the cost parity with single-sided cells is expected to converge, accelerating mass adoption across various high-value market segments.

The Double Sided Battery Market is experiencing robust expansion driven primarily by escalating demand from the Electric Vehicle sector, necessitating battery architectures capable of delivering higher power output and superior thermal stability. Business trends indicate a strong focus on strategic collaborations between established battery manufacturers and emerging technology firms specializing in advanced cell packaging and material integration. Companies are investing heavily in intellectual property related to cell-to-chassis and cell-to-pack integration methods, leveraging the double-sided design to minimize module complexity and maximize volumetric energy density. Furthermore, sustainability requirements are pushing manufacturers toward materials and processes that support the enhanced lifespan and safety features offered by these advanced battery configurations, making efficient thermal management a competitive differentiator among key players.

Regionally, the Asia Pacific (APAC) continues to dominate the market, anchored by leading production hubs in China, South Korea, and Japan, which control a significant portion of global lithium-ion cell manufacturing capacity and deployment. Europe is emerging as the fastest-growing region, fueled by ambitious decarbonization goals, substantial government subsidies for EV adoption, and the establishment of numerous domestic battery Gigafactories (e.g., in Germany and Sweden) aiming for self-sufficiency in battery production. North America shows steady growth, propelled by policy support like the Inflation Reduction Act (IRA) in the US, which incentivizes domestic sourcing and production of high-performance battery components, favoring sophisticated designs like the double-sided architecture for premium EV models.

Segment trends highlight the dominance of the Lithium-ion chemistry, particularly in prismatic and pouch cell formats tailored for high-energy density requirements in automotive applications. However, the future trajectory shows significant investment toward solid-state double sided batteries, promising breakthroughs in safety and energy density that could redefine the market beyond the forecast period. Application-wise, the EV segment maintains its position as the largest consumer, but utility-scale grid storage is rapidly gaining momentum as grid modernization efforts globally require increasingly efficient and durable battery systems capable of managing intermittent renewable energy sources effectively. This trend underscores the versatility of the double-sided design in catering to both high-power (automotive) and high-energy (stationary storage) needs.

User inquiries regarding AI's influence on the Double Sided Battery Market typically center around how artificial intelligence can accelerate material discovery, optimize complex manufacturing processes, and improve battery performance management during operation. Key themes include the use of machine learning to predict cell degradation rates (vital for optimizing the dual thermal paths of double-sided designs), simulation of advanced cell chemistries to identify ideal parameters for dual connectivity, and automating quality control checks during high-precision assembly. Concerns frequently arise about data privacy in collecting real-time operational battery data and the need for standardized AI models to ensure reliability across different manufacturing lines. Expectations are high that AI will significantly shorten the R&D cycle for next-generation double-sided cells, moving battery technology closer to theoretical performance limits while ensuring enhanced safety protocols.

The Double Sided Battery Market is primarily propelled by the exponential growth in global electric vehicle adoption and the corresponding necessity for energy storage systems that offer superior power output, faster charging capabilities, and extended lifespans. Key drivers include significant governmental incentives supporting electrification and the continual technological push by OEMs to differentiate their products through superior battery performance. Restraints predominantly involve the initial complexity and higher manufacturing costs associated with integrating dual current collectors and perfecting the sealing mechanisms required for the double-sided structure, demanding high-precision equipment and specialized expertise. Additionally, the supply chain volatility for key raw materials (lithium, cobalt, nickel) poses a persistent challenge, potentially affecting scalability and cost competitiveness against simpler cell designs.

Opportunities in this market are vast, centered around the rapid development of next-generation solid-state batteries, where the double-sided architecture is particularly advantageous for managing internal resistance and heat generation inherent in high-density solid electrolytes. Furthermore, the integration of these batteries into emerging fields such as eVTOL (electric Vertical Take-Off and Landing) aircraft and high-end industrial robotics offers specialized, high-margin applications. The industry is also poised to benefit from increased focus on second-life applications and battery recycling, where the durable nature of double-sided cells ensures longer potential usage before end-of-life processing, creating a more sustainable value loop.

The impact forces influencing the market are high, driven by technological evolution and regulatory pressure. Regulatory mandates for battery safety and minimum energy density standards globally force manufacturers to adopt superior designs like the double-sided system. Simultaneously, the pace of technological innovation, particularly in advanced materials and packaging, dictates market leadership. The balance between achieving superior performance and maintaining cost-effective production methods is the central strategic challenge defining the competitive landscape. Success hinges on scalability, standardization, and effective integration into complex vehicle platforms.

The Double Sided Battery Market is systematically segmented based on Type (Pouch, Prismatic), Material (Lithium-ion, Solid State), and Application (Electric Vehicles, Consumer Electronics, Grid Storage). This segmentation helps in analyzing distinct market dynamics, recognizing the different technical requirements demanded by various end-use sectors, and evaluating the competitive positioning of manufacturers across specific product categories. The Prismatic cell format, for instance, is increasingly favored in structural EV battery packs due to its robust casing, which aligns well with the structural demands placed on double-sided designs, while the Lithium-ion chemistry remains the foundational technology powering current commercialization efforts.

The value chain for the Double Sided Battery Market is complex, beginning with the upstream sourcing and refinement of highly specialized raw materials, including high-purity lithium compounds, nickel, cobalt, manganese, and graphite. The stringent performance requirements of double-sided designs necessitate premium-grade components, particularly separator films and electrolytes optimized for enhanced thermal stability and high-rate capability. Upstream activities involve significant capital investment in mining, chemical processing, and material synthesis, often dominated by a few major players in Asia Pacific, creating potential choke points in the supply chain for materials like high-grade lithium hydroxide and specialized anode materials essential for long cycle life.

Midstream manufacturing focuses on the sophisticated cell production process, where the proprietary design of double-sided current collectors is implemented. This stage requires high-precision lamination, stacking, or winding techniques, followed by intricate assembly, casing, and formation steps. The adoption of double-sided architecture increases the technical complexity and precision demanded during assembly compared to standard cells, driving higher operational expenditure (OpEx) but resulting in a superior quality product. Distribution channels are highly dependent on the end application; for Electric Vehicles, distribution is primarily direct to major automotive OEMs or through specialized Tier 1 battery pack integrators. For stationary storage, distribution often involves energy solution providers and system integrators who customize battery modules for utility or commercial installations.

Downstream activities center on the end-use and service life management of the batteries. Direct channels involve OEMs procuring cells directly for integration into their structural battery packs (e.g., Tesla, BYD). Indirect channels, prevalent in consumer electronics and smaller industrial applications, utilize wholesalers and specialized electronics distributors. A crucial part of the downstream value chain is the rapidly growing sector of battery recycling and repurposing (second life), which is vital for securing long-term material sustainability and minimizing environmental impact. Manufacturers are increasingly integrating design-for-recyclability features, which are supported by the robust, controlled architecture of double-sided batteries, ensuring material recovery is efficient at the end of the battery’s first life cycle.

The primary customers and end-users of double sided batteries are concentrated in sectors demanding high energy density, rapid charging, and exceptional thermal stability, performance metrics which this specific battery architecture excels at delivering. The automotive industry, particularly manufacturers of high-performance and premium electric vehicles, represents the largest and most valuable customer segment. These OEMs (e.g., Porsche, Lucid, high-end models from BMW, Mercedes-Benz, and Tesla) require batteries that can handle intensive duty cycles, offer extended range, and integrate seamlessly into structural chassis designs, making the double-sided design highly attractive for maximizing pack efficiency and minimizing weight.

Another significant customer base lies within the burgeoning utility-scale energy storage sector. Grid operators, independent power producers, and renewable energy developers (solar and wind farms) are heavy buyers of double sided cells and modules, seeking highly durable and efficient solutions for peak shaving, frequency regulation, and integrating intermittent power sources reliably. The enhanced lifespan and reduced internal heating offered by these batteries translate directly into lower Levelized Cost of Storage (LCOS) over decades of operation. Furthermore, the specialized segments of consumer electronics and advanced industrial applications, such as high-end drones, medical devices, and heavy-duty industrial robotic systems, serve as niche, high-margin customers requiring batteries with exceptional power density in compact form factors.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.2 Billion |

| Market Forecast in 2033 | $4.0 Billion |

| Growth Rate | 19.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Samsung SDI, LG Energy Solution, Contemporary Amperex Technology Co. Limited (CATL), Panasonic Corporation, BYD Company Ltd., SK Innovation, Northvolt AB, Farasis Energy, EVE Energy Co. Ltd., AESC (Automotive Energy Supply Corporation), Svolt Energy Technology Co. Ltd., StoreDot, QuantumScape Corporation, Enovix Corporation, Factorial Energy, Sion Power, Tesla Inc., BMW Group, Rivian Automotive, Lucid Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Double Sided Battery Market is highly specialized, revolving around achieving optimal current distribution and thermal pathway management through sophisticated cell design. A core enabling technology is the implementation of dual current collection systems, which requires precise manufacturing techniques like laser welding or ultrasonic bonding to ensure robust connections on both sides of the cell stack. This structural modification necessitates advancements in cell packaging to maintain hermetic sealing and structural integrity despite the added complexity of dual terminals. Furthermore, significant research and development efforts are focused on improving electrode material loading and porosity specifically for double-sided cells, ensuring uniform utilization across the entire electrode surface area and maximizing the benefit of reduced internal impedance.

Advanced thermal management remains a critical technology driver. Since double-sided designs inherently handle higher power throughput, effective heat dissipation is crucial for longevity and safety. Technologies such as integrated microchannel cooling plates and specialized dielectric fluids are being customized to maximize heat extraction efficiency from both sides of the cell simultaneously. This enhanced thermal control not only extends the battery's cycle life but also enables ultra-fast charging capabilities without triggering thermal runaway risks. The successful deployment of double-sided batteries is intrinsically linked to the sophistication of the Battery Management Systems (BMS), which must be advanced enough to monitor and control the two distinct current paths and associated thermal gradients precisely.

Looking ahead, the fusion of double-sided architecture with solid-state battery (SSB) technology represents the next major technological leap. Solid-state electrolytes eliminate the need for flammable liquid components, drastically improving safety, while the double-sided structure complements SSBs by minimizing the interfacial resistance that typically hinders their high-power performance. Companies are focusing on optimizing the interfacial contact between the solid electrolyte and the dual current collectors, often involving complex pressure application techniques and specialized coatings. Innovations in dry electrode manufacturing are also vital, reducing the environmental footprint and operational costs associated with conventional slurry coating processes, thereby supporting the scaled production of these high-performance, next-generation cells.

The primary advantage is significantly reduced internal resistance achieved through the use of dual current collectors (tabs on both sides). This design improves thermal dissipation efficiency and allows for higher charge/discharge rates, crucial for ultra-fast charging in electric vehicles and maximizing power output in grid storage systems, leading to enhanced cell longevity and safety.

The double sided architecture generally increases manufacturing complexity due to the need for precise alignment, stacking, and specialized bonding techniques for dual connection points. This often requires higher initial capital investment in specialized automated equipment. However, the resulting gains in performance and lifespan often justify the higher unit cost, particularly for high-end automotive applications.

High-performance Electric Vehicles (EVs) and utility-scale Grid Energy Storage Systems benefit most. EVs gain superior fast-charging capability and better thermal stability under high-stress driving conditions, while grid storage benefits from enhanced durability, reduced cooling requirements, and longer operational life necessary for decades of service.

Yes, the integration is highly compatible and often complementary. The double sided architecture is being actively researched for Solid State Batteries (SSBs) because it helps mitigate the high interfacial resistance inherent in some solid electrolytes. By creating dual pathways, the design helps manage the thermal and power demands of future high-density solid-state cells effectively.

The Asia Pacific (APAC) region, primarily driven by China, South Korea, and Japan, currently leads in both the development and commercialization of double sided batteries. This dominance is attributed to the presence of major global battery manufacturing giants and established robust supply chains for advanced lithium-ion technologies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.