ID : MRU_ 432984 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

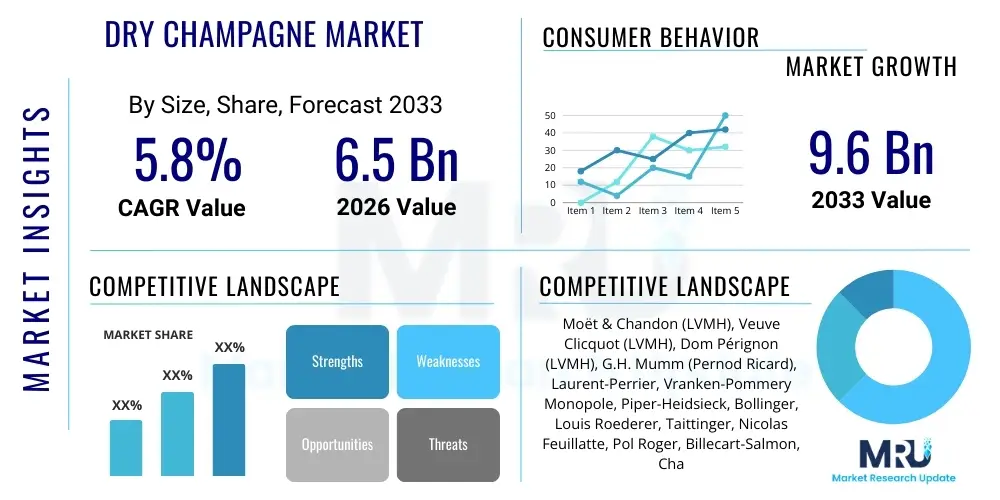

The Dry Champagne Market is projected to grow at a Compound Annualized Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2033.

The Dry Champagne Market encompasses the production, distribution, and consumption of effervescent wines produced within the Champagne region of France, specifically those falling into the Brut Nature, Extra Brut, and Brut categories, characterized by low dosage levels (sugar content). This segment constitutes the largest and most commercially significant portion of the global champagne industry, driven by enduring consumer preference for drier, more sophisticated flavor profiles. Dry Champagne is universally recognized as a premium, luxury product, often associated with celebrations, high-end dining, and affluent lifestyles, solidifying its inelastic demand across major global economies.

The primary applications of Dry Champagne extend beyond traditional celebratory consumption to include pairing with fine cuisine, particularly seafood and white meats, and use in exclusive corporate events. The consistent global demand is fueled by several key benefits, including the perceived high quality derived from stringent Appellation d'Origine Contrôlée (AOC) regulations, the strong brand equity associated with the Champagne name, and the growing trend among Millennial and Gen Z consumers toward lower-sugar alcoholic beverages. Furthermore, the limited availability due to geographical constraints in the Champagne region helps maintain premium pricing and perceived exclusivity.

Key driving factors supporting the market expansion include the increasing disposable income in emerging economies, particularly in Asia Pacific, leading to greater access to luxury goods. The successful marketing efforts by major Champagne houses focusing on heritage and craftsmanship also contribute significantly. Moreover, the trend of premiumization in the alcoholic beverage sector, where consumers seek higher-quality, distinctive products even if they carry a higher price tag, reinforces the dominance of Dry Champagne over other sparkling wine categories, ensuring steady growth across both On-Trade (restaurants, bars) and Off-Trade (retail) channels.

The Dry Champagne market is experiencing robust business trends characterized by strategic vertical integration among large established houses aimed at securing high-quality grape supply amidst increasing climate variability. Technological investments are being directed towards optimizing vineyard management (viticulture) and enhancing cellar operations (oenology) to ensure vintage consistency and minimize environmental impact, aligning with growing consumer scrutiny regarding sustainability. Mergers and acquisitions remain a consistent strategy for smaller, independent growers (vignerons) to gain distribution leverage or for larger luxury groups to consolidate market share and portfolio diversity in the premium segment.

Regionally, Europe, specifically Western Europe, maintains its position as the largest revenue generator due to deep-rooted consumption culture and established distribution networks, although North America exhibits the highest rate of consumption per capita growth, driven by lifestyle changes and strong economic recovery. The Asia Pacific region, led by China and Japan, presents the most significant long-term opportunity, showcasing rapid adoption of luxury goods and an expanding affluent consumer base actively incorporating champagne into gifting and modern celebratory rituals. Market penetration strategies in these regions increasingly focus on digital marketing and e-commerce platforms to bypass traditional import complexities.

Segment trends indicate a pronounced shift toward the Extra Brut and Brut Nature sub-segments, appealing directly to the health-conscious consumer demanding minimal residual sugar. The Non-Vintage (NV) category continues to dominate volume sales, providing accessible entry points, while the Prestige Cuvée and Vintage segments command substantial value growth, reflecting consumer willingness to invest in unique, limited-production offerings. Furthermore, the emergence of personalized offerings, such as bespoke packaging and exclusive limited editions, caters effectively to the demand for differentiated luxury experiences, solidifying segment profitability across the value chain.

Analysis of common user questions reveals strong interest in how AI can safeguard the traditional quality and limited terroir of Champagne while modernizing production and distribution. Users frequently inquire about AI's role in predicting climate-related risks, optimizing vineyard treatments, and authenticating high-value vintage bottles to combat counterfeiting. There is also significant curiosity regarding AI-driven personalization, particularly how large Champagne houses can use predictive analytics to tailor marketing messages and inventory management to highly specific consumer segments globally, maximizing brand loyalty and operational efficiency. The overriding theme is the expectation that AI should enhance sustainability and provenance tracking without diluting the essential craftsmanship and heritage that defines premium Dry Champagne.

The implementation of AI and machine learning (ML) is fundamentally altering precision viticulture. By deploying sensors and satellite imagery analyzed by AI algorithms, growers can achieve highly accurate prediction models for disease outbreaks, harvest timing, and grape yield optimization, minimizing waste and ensuring optimal maturity levels essential for the dry style. This shift allows for reduced reliance on broad chemical treatments and water resources, directly addressing environmental concerns and improving grape quality consistency, which is crucial given the tight regulatory framework of the AOC.

In the consumer-facing sphere, AI is being leveraged for predictive inventory allocation and demand forecasting, helping producers navigate the complex logistics of global distribution and ensuring rare vintages are allocated efficiently to target markets. Furthermore, blockchain technology, often integrated with AI-driven authentication processes, is providing irrefutable traceability from the vine to the consumer, drastically increasing trust in high-end purchases and safeguarding the brand integrity of Dry Champagne houses against illicit parallel markets and fraudulent activity.

The Dry Champagne Market is primarily driven by the robust premiumization trend across global beverage markets, coupled with rising discretionary income among middle and upper-income households, particularly in emerging Asia. The high cultural significance and enduring association of Champagne with success and celebration sustain its market resilience. Opportunities stem from the increasing demand for high-quality, low-sugar alcoholic options (Extra Brut and Brut Nature), catering to health-conscious consumers, and the rapid expansion of e-commerce platforms, which offer direct-to-consumer access and better inventory control. However, the market faces significant restraints, including the severe impact of climate change on grape yield and quality in the protected Champagne region, leading to supply volatility and increased production costs, alongside stringent governmental regulations and high taxation rates on luxury alcohol imports in many large markets.

Key drivers include the global expansion of luxury lifestyle hotels, restaurants, and premium travel retail, which heavily rely on Dry Champagne as a staple luxury offering, thereby consistently increasing On-Trade volume demand. Furthermore, targeted marketing campaigns by major Champagne houses focusing on the heritage, scarcity, and unique terroir of the region effectively reinforce brand desirability and justify the premium price point, counteracting competition from high-quality sparkling wines like Prosecco and Cava by emphasizing product differentiation based on AOC provenance and production methods.

The most substantial impact forces shaping the market are the supply-side constraints imposed by environmental factors, particularly erratic weather patterns that threaten established harvesting cycles and yields, forcing producers to invest heavily in resilient viticulture practices. Demand-side impact forces include shifting consumer preferences towards authentic, sustainable, and transparently sourced luxury goods, compelling houses to adopt comprehensive Environmental, Social, and and Governance (ESG) standards. These forces collectively pressure profit margins while simultaneously validating the premium status of authentic Dry Champagne, necessitating strategic pricing adjustments and continuous innovation in vineyard technology to maintain supply integrity.

The Dry Champagne Market is analyzed across various dimensions including Type, Dosage Level, Distribution Channel, and End-Use, providing a comprehensive understanding of consumer behavior and market dynamics. Segmentation based on dosage (Brut, Extra Brut, Brut Nature) is crucial as it reflects current health and wellness trends impacting consumer purchasing decisions. Distribution channel analysis (On-Trade vs. Off-Trade) highlights the critical roles of hospitality sectors and traditional retail in driving sales volumes and value, while segmentation by end-user (Individual vs. Corporate) differentiates between personal consumption patterns and large-scale, formal event purchasing.

The Dry Champagne value chain is characterized by high control and significant capital investment at the upstream stage, centered on grape cultivation and primary fermentation. Upstream analysis involves highly specialized viticulture within the strictly defined AOC zone. This phase is dominated by independent growers (vignerons) who supply grapes to the large Champagne houses (Négociants Manipulants) or produce their own estate-bottled champagnes (Récoltants Manipulants). The stringent quality control dictated by the Comité Champagne, including mandated pruning, harvesting, and pressing techniques, ensures the foundation of the final product’s quality and exclusivity. Resource management, particularly land and skilled labor, remains a primary upstream cost and constraint.

The core processing stage involves secondary fermentation (prise de mousse), aging (maturation sur lie), riddling (remuage), and dosage application. This middle segment is where the bulk of value addition occurs through time and specialized expertise. Large Champagne houses exert considerable influence here, leveraging centuries of brand heritage and proprietary blending techniques to create their distinctive styles, ensuring uniformity across large volumes of Non-Vintage Brut. The long aging requirement, particularly for Vintage and Prestige Cuvées, ties up capital, making efficient inventory management a critical operational function.

Downstream, the distribution channel is highly bifurcated into direct and indirect routes. Direct sales often involve cellar door sales and high-end e-commerce, offering better margins but limited reach. Indirect distribution through specialized importers, distributors, and finally, retailers (Off-Trade) and the hospitality sector (On-Trade) ensures global market access. Given the product's value and fragility, logistics, temperature control, and secure warehousing are essential. Market influence is consolidated at the indirect retail and wholesale level, where pricing strategies and promotional activities significantly impact consumer uptake, demanding strong brand collaboration between producers and key retail partners.

The primary potential customers for Dry Champagne fall into distinct high-net-worth individual (HNWI) and institutional categories who prioritize luxury, provenance, and exclusivity in their purchasing decisions. HNWIs and Ultra-HNWIs globally are consistent buyers, utilizing Dry Champagne for personal celebrations, as an investment asset (especially rare vintages), and for gifting. This demographic seeks authenticity, detailed historical narratives associated with the brand, and product excellence verified by critical acclaim. Marketing efforts must resonate with aspirations of sophisticated indulgence and cultural significance, often utilizing exclusive member services and private events to build lasting loyalty.

A second major segment comprises the premium hospitality sector, including five-star hotels, Michelin-starred restaurants, and high-end cruise lines (On-Trade). These institutional buyers view Dry Champagne as an essential component of their luxury offering, driving significant volume and maintaining high visibility for the brand. Their purchasing decisions are driven by margin potential, prestige associated with specific labels, and reliable supply chain logistics. Establishing strong relationships with influential sommeliers and procurement managers in this sector is critical for market penetration and perceived quality endorsement.

Furthermore, the expanding corporate market, encompassing major financial institutions, law firms, and international companies, constitutes a growing base for corporate gifting and high-level business events. These buyers require branded, often personalized, presentations and demand strict adherence to quality standards for use in client entertainment and employee recognition programs. The market also sees growth in the Millennial and Gen Z demographics who, despite general economic pressures, exhibit a strong inclination toward spending on experiential luxuries and premium alcoholic beverages, specifically favoring the low-sugar, Brut Nature styles, positioning them as key future buyers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | CAGR 5.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Moët & Chandon (LVMH), Veuve Clicquot (LVMH), Dom Pérignon (LVMH), G.H. Mumm (Pernod Ricard), Laurent-Perrier, Vranken-Pommery Monopole, Piper-Heidsieck, Bollinger, Louis Roederer, Taittinger, Nicolas Feuillatte, Pol Roger, Billecart-Salmon, Charles Heidsieck, Ruinart (LVMH), Ayala, Perrier-Jouët, Gosset, Salon, Krug (LVMH) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Dry Champagne market leverages specialized technologies primarily focused on precision viticulture and quality assurance throughout the cellar process, ensuring that the finished product adheres strictly to AOC standards despite external environmental pressures. In the vineyard, the adoption of advanced sensor networks, integrated with IoT devices and drone technology, allows for hyper-localized monitoring of soil moisture, nutrient levels, and canopy health. This data is fed into predictive analytics models to optimize irrigation schedules, minimize fungicide use, and accurately determine the optimal harvest window, which is critical for maintaining the necessary acidity levels inherent in high-quality dry champagne base wines.

Within the production phase (the cellar), automation technology plays a significant role in handling labor-intensive processes. Automated riddling machines (gyropalettes) have largely replaced traditional manual methods, enhancing efficiency and consistency in moving the yeast sediment towards the neck of the bottle. Furthermore, sophisticated temperature control systems are non-negotiable, employed throughout fermentation and secondary aging to ensure the slow, controlled development of the wine’s complex flavor profile. Pressure sensors and automated bottling lines also maintain precision during disgorgement and dosage application, ensuring the final sugar content meets the stringent requirements for Brut, Extra Brut, or Brut Nature classifications.

Looking ahead, emerging technologies such as Artificial Intelligence (AI) and blockchain are gaining prominence. Blockchain technology is crucial for establishing irrefutable digital provenance, enhancing consumer trust in the authenticity of rare and expensive bottles, a significant challenge in the luxury alcohol sector. Additionally, sustainable technology, including solar energy integration in cellar operations and advanced wastewater management systems, is becoming standard practice, driven by both regulatory pressures and consumer demand for environmentally responsible production, thereby securing long-term brand equity.

The primary difference lies in the dosage, or residual sugar content, added after disgorgement. Brut Champagne contains less than 12 grams of sugar per liter, making it the standard dry style. Extra Brut is significantly drier, containing between 0 and 6 grams of sugar per liter, appealing to consumers seeking a very crisp, low-sugar profile, often highlighting the purity of the base wine.

Climate change causes earlier harvests and increased temperature variability, which can lead to higher sugar levels and lower acidity in the grapes. Maintaining the high acidity necessary for authentic dry champagne requires stringent vineyard management adaptations, increasing production complexity and costs, leading to potential supply volatility for high-quality vintages and non-vintage blends.

The Off-Trade channel, encompassing retail stores, supermarkets, and dedicated wine shops, traditionally accounts for the largest volume of sales, providing accessibility for individual consumption. However, the On-Trade channel (restaurants, hotels, and bars) contributes significantly to the market's overall value and brand visibility due to higher per-bottle markups and premium placement.

The Appellation d'Origine Contrôlée (AOC) designation mandates strict geographical boundaries, specific grape varietals (Chardonnay, Pinot Noir, Pinot Meunier), minimum aging requirements, and production methods (Méthode Champenoise). This stringent regulation ensures unique quality and scarcity, acting as a crucial barrier to entry and justifying the premium pricing of Dry Champagne globally.

Yes, the demand for Brut Nature, or Zero Dosage, Champagne is rapidly increasing, particularly in high-growth markets like North America and specific European luxury segments. This growth is driven by a broader consumer trend toward low-sugar and authentic products, positioning Brut Nature as the ultimate expression of dry champagne purity and a preferred choice for connoisseurs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.