ID : MRU_ 432429 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

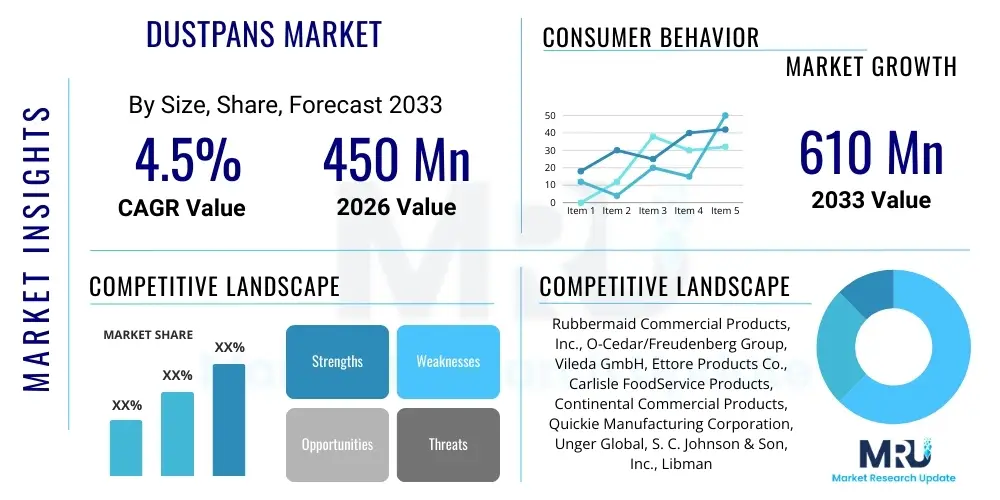

The Dustpans Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 610 Million by the end of the forecast period in 2033.

The Dustpans Market encompasses the manufacturing, distribution, and sale of manual cleaning tools designed to collect debris, dust, and sweepings after brushing. These tools are fundamental components of household, commercial, and industrial cleaning processes globally. The product description spans various designs, including traditional flat dustpans, lobby dustpans with long handles, automatic sensor dustpans, and specialized industrial versions made from durable materials like plastic, metal, and composite polymers. Market penetration is universal, driven by the constant need for basic hygiene and cleanliness across all end-user segments.

Major applications for dustpans are highly diversified, ranging from residential home maintenance and quick cleanups to heavy-duty commercial use in hospitality, healthcare, retail, and manufacturing sectors. The inherent simplicity and low cost of dustpans ensure their continued relevance despite the rise of automated vacuuming systems. Key benefits include portability, lack of reliance on electrical power, ease of use, durability, and effectiveness in collecting fine debris that automated systems might miss on certain surfaces. The market is crucial for supporting rapid cleanup needs in high-traffic areas and ensuring safety by quickly removing hazards.

Driving factors supporting the market’s moderate growth include increasing urbanization, which boosts demand for cleaning tools in dense residential and commercial complexes, and rising awareness regarding sanitation standards, particularly in emerging economies. Furthermore, innovations in dustpan design, focusing on ergonomics, long handles to reduce back strain (lobby dustpans), and integrated brushes or seals to prevent debris slippage, continue to maintain consumer interest. The expansion of the professional cleaning services industry, requiring robust and efficient manual tools, acts as a significant demand catalyst.

The Dustpans Market exhibits stable growth driven primarily by steady demand in the commercial and residential cleaning sectors, counterbalancing the slower growth often associated with mature product categories. Business trends indicate a shift towards ergonomic and eco-friendly designs, with manufacturers focusing on using recycled plastics and sustainable materials to appeal to environmentally conscious consumers. Consolidation among major cleaning tool manufacturers is a noticeable trend, aimed at streamlining supply chains and achieving economies of scale. Furthermore, the rising adoption of professional cleaning services is elevating the demand for high-durability, professional-grade lobby dustpans over basic household models.

Regional trends highlight the Asia Pacific (APAC) region as the fastest-growing market, largely due to rapid infrastructural development, burgeoning middle-class populations, and improving hygiene standards in countries like China and India. North America and Europe remain mature markets characterized by replacement demand and a strong preference for high-quality, branded products with advanced ergonomic features. Investment in automated manufacturing processes in these regions helps maintain competitive pricing, while distribution channels are heavily skewed towards large retail chains, e-commerce platforms, and specialized janitorial supply distributors.

Segmentation trends indicate that the Plastic Dustpans segment maintains the largest market share due to cost-effectiveness and versatility, although the Metal/Composite segment is experiencing above-average growth owing to its superior durability for industrial and heavy commercial applications. From an application perspective, the Commercial segment, encompassing hotels, offices, and hospitals, is the dominant revenue generator, necessitating robust, long-handled solutions. The E-commerce distribution channel is rapidly gaining prominence, offering consumers wider choices and competitive pricing, challenging traditional brick-and-mortar retail dominance, especially for niche or specialized ergonomic models.

User inquiries regarding AI's influence on the Dustpans Market typically center on whether advanced automation technologies will render manual tools obsolete, or if AI can be integrated into low-tech cleaning aids. Users frequently question the role of smart sensors in augmenting traditional cleaning, specifically how predictive maintenance and optimization of cleaning routes (driven by AI in robotic vacuums) might indirectly affect the demand for manual spot-cleaning equipment like dustpans. The general expectation is that while AI won't replace the physical dustpan, it will influence product design through enhanced materials science recommendations and optimized supply chain logistics.

The core themes reveal concerns about the potential for complete cleaning automation through sophisticated robotics, which could reduce the need for manual sweeping. However, there is also acknowledgment that manual tools are indispensable for quick spills, areas inaccessible to robots (e.g., stairs, tight corners), and heavy debris not suitable for robotic suction. Therefore, AI's impact is less about direct product enhancement and more about indirect market efficiency, such as optimizing inventory levels based on real-time consumer purchasing patterns and predicting regional demand shifts for cleaning supplies, thereby ensuring better stock management for dustpan manufacturers and retailers.

Furthermore, while the dustpan itself is not smart, AI tools are increasingly used in the commercial cleaning industry to train staff, manage labor resources, and assess cleaning efficacy. This professionalization of cleaning services, supported by AI-driven operational tools, paradoxically increases the demand for high-quality, reliable, manual tools used by trained professionals. Manufacturers can leverage machine learning to analyze material stress points, leading to the development of stronger, lighter, and more efficient dustpan designs tailored for professional use, enhancing the product without directly integrating the technology.

The dynamics of the Dustpans Market are shaped by a balanced set of drivers, restraints, and opportunities, influencing its steady but moderate growth trajectory. Key drivers include heightened public and commercial focus on hygiene, particularly post-pandemic, which increases the frequency and thoroughness of cleaning across all sectors. Restraints primarily involve the maturity of the product category and the intense price competition, especially from low-cost manufacturers in Asia, which limits margin expansion for established brands. Opportunities lie in developing specialized, ergonomic, and sustainable product lines, targeting niche commercial markets, and leveraging the rapid expansion of e-commerce channels for direct consumer access.

Impact forces on the market include the substitution threat posed by alternative cleaning technologies, such as advanced robotic vacuum cleaners and powerful industrial wet/dry vacuums, which can partially replace the need for sweeping and dustpan usage in certain environments. Supplier power remains relatively low due to the abundance of raw material suppliers (plastics, metals), making manufacturing input costs manageable. However, buyer power is high, especially in the B2B segment, where large janitorial distributors and retail chains command significant discounts and influence product specifications.

Furthermore, environmental regulations regarding plastic use and waste management are emerging as a significant force, pushing manufacturers to innovate toward recycled content or bioplastics, incurring initial R&D costs but offering long-term market differentiation. The overall competitive rivalry is intense, characterized by numerous global and regional players competing primarily on price, design functionality, and distribution network strength, necessitating constant product refinement and marketing expenditure to maintain market visibility and brand loyalty among consumers.

The Dustpans Market is systematically segmented based on material type, product design, application (end-user), and distribution channel, providing a clear map of market dynamics and consumer preferences. Analyzing these segments helps stakeholders understand where specific demand pressures are concentrated, allowing for targeted product development and marketing strategies. The market structure reveals a preference for durable and large-capacity designs in commercial settings, contrasting with the demand for compact, aesthetically pleasing, and easy-to-store models in residential applications. Material segmentation is crucial as it directly correlates with longevity and price point, impacting segment profitability.

The value chain for the Dustpans Market commences with upstream analysis, focusing on the procurement of raw materials, primarily various grades of plastics (polypropylene and high-density polyethylene) and metals (steel, aluminum). Raw material sourcing involves standard commodity markets, leading to low supplier differentiation but ensuring stable supply. Key upstream activities include material processing, such as molding plastic pellets and shaping metal sheets, which are highly standardized and often outsourced or handled by specialized industrial contractors to manage costs effectively and maintain production scalability. Efficient inventory management of these raw materials is crucial to mitigating price volatility.

Downstream analysis covers the final manufacturing, assembly, branding, and distribution processes. Manufacturing involves injection molding for plastic dustpans or stamping/welding for metal variants, followed by assembly with handles and brushes. Distribution channels are highly fragmented yet critical for market penetration. Direct channels primarily include large B2B contracts with janitorial supply houses, major retailers (like Walmart or Home Depot), and increasingly, direct-to-consumer sales via dedicated e-commerce platforms. These channels allow manufacturers to control branding and pricing but require significant logistical infrastructure.

Indirect distribution relies on wholesalers, regional distributors, and localized retailers who purchase in bulk and cater to smaller commercial entities and individual consumers. The strong emphasis on indirect distribution, especially through mass-market retailers and online marketplaces, necessitates competitive pricing and strong trade marketing support. Effective logistics management, particularly in large markets like North America and APAC, is vital to ensure timely delivery and reduce warehousing costs, directly impacting the final retail price and consumer accessibility of the product.

Potential customers and end-users of dustpans span a vast spectrum, categorized primarily into residential users, who prioritize convenience, aesthetics, and affordability for daily household maintenance, and commercial/institutional buyers, who demand durability, ergonomic design, and specialized features suitable for heavy, repetitive use. Residential buyers are highly influenced by retail promotions and online reviews, seeking integrated storage solutions and modern designs that complement home decor. This segment drives demand for standard hand dustpans and specialized whisk-and-pan sets used for light, quick cleaning tasks in kitchens and living spaces.

The largest volume and value customers are found within the professional domain, including facility management companies, contract cleaning services, and institutional purchasing departments (hospitals, universities, government buildings). These buyers require robust, long-handled lobby dustpans that minimize physical strain on staff and offer large debris capacity. Their purchasing decisions are based on total cost of ownership, product longevity, ergonomic certifications, and compliance with institutional hygiene standards, often leading to bulk procurement through B2B distributors and tenders.

Furthermore, specialized industrial end-users, such as manufacturing plants, construction sites, and warehouses, represent a distinct segment requiring heavy-duty, often metal-reinforced dustpans capable of handling industrial debris, metal shavings, and heavy litter. These customers prioritize industrial strength and chemical resistance over ergonomic convenience, purchasing through specialized industrial supply houses. Successful market players must therefore tailor material quality and size specifications to meet the rigorous demands of these varied end-user groups, managing a diverse product portfolio.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 610 Million |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Rubbermaid Commercial Products, Inc., O-Cedar/Freudenberg Group, Vileda GmbH, Ettore Products Co., Carlisle FoodService Products, Continental Commercial Products, Quickie Manufacturing Corporation, Unger Global, S. C. Johnson & Son, Inc., Libman Company, Casabella Holdings LLC, Fuller Brush Company, OXO International, Lola Products, Swiffer (P&G), Madesmart, F. B. P. Srl, Chicopee, Wypall, and Brushtech. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

While the dustpan itself is a low-tech manual tool, the "technology landscape" surrounding its manufacturing and design centers on material science, ergonomic engineering, and subtle functional innovations aimed at maximizing debris capture efficiency and user comfort. A primary focus involves advanced polymer engineering, utilizing high-grade, durable plastics like ABS or specialized polypropylenes resistant to cracking and harsh cleaning chemicals, particularly important for commercial models. Manufacturers are also employing co-injection molding techniques to integrate rubber or soft polymer lips (dust seals) seamlessly into the pan edge, ensuring optimal surface contact and preventing fine particles from escaping underneath the pan during sweeping, which is a critical consumer requirement.

Ergonomic technology is crucial, especially in the lobby dustpan segment. This includes the development of lightweight yet rigid aluminum or steel handles, coupled with swivel or locking joints that allow the user to manage the pan without bending over. The goal is to adhere to professional janitorial standards concerning repetitive strain injury (RSI) prevention. Furthermore, brush-and-pan systems often incorporate "teeth" or comb features integrated into the dustpan rim, utilizing material technology optimized for stiff resistance, allowing the user to clean the sweeping brush bristles directly into the pan without physically touching the debris, thus enhancing hygiene and efficiency.

The technology driving sustainability in manufacturing is also gaining traction. This involves investing in recycling infrastructure to process post-consumer and post-industrial plastic waste for use in new dustpan production, appealing to environmentally conscious municipal and commercial buyers. Production technologies emphasize automation for consistent quality and precision in molding the critical angles of the pan base and lip, ensuring uniform performance across high-volume production runs. Advanced coating technologies are sometimes used on metal dustpans to enhance rust resistance and extend product life in moisture-prone environments.

The global Dustpans Market exhibits varied consumption patterns and growth rates across different geographical regions, heavily influenced by urbanization levels, labor costs, and adherence to professional cleaning standards. North America (NA) and Europe represent mature markets characterized by high per capita spending on advanced cleaning tools, strong penetration of branded, ergonomic products, and a significant demand base from large commercial and institutional sectors. These regions prioritize quality and sustainability, driving innovations in recycled materials and durable designs suitable for intensive professional use, and maintenance of competitive pricing through efficient retail supply chains.

Asia Pacific (APAC) is positioned as the primary growth engine for the forecast period, fueled by massive increases in residential construction, expanding commercial real estate development, and a rapidly professionalizing cleaning industry. While demand here encompasses both high-end and budget-friendly products, the sheer volume of new households and commercial establishments translates into substantial market expansion. Countries like China and India are seeing rapid adoption of Western-style cleaning protocols, although local manufacturers often dominate the lower-cost, volume-based segments, leading to intense internal competition.

Latin America (LATAM) and the Middle East and Africa (MEA) are emerging markets showing consistent, albeit segmented, growth. In MEA, infrastructure development related to hospitality and major events (e.g., in the UAE and Saudi Arabia) spurs commercial demand for quality cleaning tools. LATAM’s market is influenced by economic stability and urbanization rates, with strong opportunities existing in modernizing cleaning practices within commercial and retail spaces. Penetration in these regions is heavily reliant on effective distribution networks that can overcome logistical challenges and cater to price-sensitive consumer segments.

The market growth is primarily driven by heightened global awareness of sanitation and hygiene, the rapid expansion and formalization of the professional cleaning services industry, and continuous product innovations focused on ergonomics and specialized design for commercial use, particularly long-handled lobby dustpans.

The market is segmented into Hand Dustpans (Standard/Household), Lobby Dustpans (Upright/Long Handle), and Whisk/Brush Combos. While Hand Dustpans hold the largest volume share due to universal household use, the Lobby Dustpan segment is experiencing faster growth in terms of value, driven by high demand from the profitable commercial and institutional sectors.

Automated cleaners, such as robotic vacuums, provide a significant substitution threat for general floor cleaning, potentially limiting residential demand for basic sweeping. However, dustpans remain indispensable for quick spot spills, heavy debris (which can damage vacuum motors), areas inaccessible to robots (e.g., stairs), and specialized commercial cleaning, thus maintaining steady demand.

The Asia Pacific (APAC) region, particularly emerging economies like China and India, offers the most significant growth opportunities. This is due to increasing urbanization, massive investments in commercial and institutional infrastructure, and the growing adoption of standardized professional cleaning practices, leading to high-volume procurement.

Yes, sustainability is a critical trend. Manufacturers are increasingly adopting recycled polymers (Post-Consumer Resin or PCR) and developing products using bioplastics to meet rising consumer demand and regulatory pressures in mature markets like Europe and North America, positioning eco-friendly materials as a key competitive differentiator.

Commercial-grade lobby dustpans, often constructed from heavy-duty plastics and aluminum, are designed for longevity under frequent use. Their expected lifespan typically ranges from 18 months to 3 years, depending heavily on the intensity of use, adherence to maintenance protocols, and environmental factors like exposure to corrosive cleaning agents or extreme temperatures.

Online retail, including major e-commerce platforms and specialized janitorial websites, is experiencing the fastest shift. This channel offers consumers and small businesses the benefit of competitive pricing, extensive product reviews, and convenient home or office delivery, challenging the historical dominance of traditional offline hardware and mass retail stores.

Key innovations include incorporating advanced rubberized lips (dust seals) on the pan edge to ensure maximum contact with the floor, integrating cleaning combs or "teeth" into the pan structure to easily remove debris from the broom bristles, and enhancing ergonomics through adjustable, lightweight, and long-handled designs to reduce physical strain on the user.

Plastic dustpans are the most common and cost-effective, suitable for residential and light commercial use. Metal (steel/aluminum) dustpans are significantly more durable and higher priced, primarily serving heavy-duty industrial and certain high-volume commercial applications where resistance to damage and chemical exposure is required. Composite materials balance cost and durability for mid-range professional products.

The healthcare sector (hospitals, clinics) is a crucial institutional buyer. Demand here is characterized by the need for color-coded cleaning systems (to prevent cross-contamination), high standards of durability, and products that are easy to sterilize or sanitize, contributing significantly to the commercial segment's revenue, driven by rigorous sanitation protocols.

The main restraints include the inherent maturity of the product—limiting radical innovation opportunities—and intense price competition, particularly from numerous regional and local manufacturers. Additionally, the increasing reliance on advanced automated floor cleaning technology in developed nations poses a competitive restriction.

In the residential segment, there is a strong preference for sets (combos) due to the convenience of integrated storage and matched aesthetics. However, commercial buyers frequently prefer separate purchases, often pairing specialized, heavy-duty lobby dustpans with specific brooms (e.g., angle brooms or push brooms) optimized for their cleaning environment.

Polypropylene (PP) is widely used for its cost-effectiveness and good chemical resistance, making it suitable for general household use. High-Density Polyethylene (HDPE) offers superior impact strength and rigidity, making it preferred for high-wear areas and commercial dustpans where resisting cracking from drops or heavy loads is essential for longevity.

The Impact Forces analysis is vital for understanding competitive intensity and profitability. High buyer power (large retailers), moderate threat of substitutes (robotics), and intense competitive rivalry mandate that manufacturers focus on cost-efficiency and product differentiation to maintain viable margins against market pressures.

Yes, niche innovations include sensor-activated "electric dustpans" that suction debris swept to them (often marketed under the vacuum category), and designs incorporating internal reservoirs or sealed systems. However, these represent a small, higher-priced segment, while the core market remains dominated by passive, manually operated designs due to cost and reliability.

Manufacturers target the institutional segment through specialized B2B distribution channels and participation in procurement tenders. Key requirements include compliance with safety standards, bulk pricing discounts, product durability suitable for high-traffic environments, and often, specific color-coding mandated by facility management protocols.

A professional-grade dustpan is defined by superior material quality (often heavy-gauge metal or high-impact plastics), reinforced handles, larger capacity, a precision rubber lip seal, and enhanced ergonomic features. They command a premium due to their extended durability, ability to withstand harsh commercial environments, and features that improve cleaning staff efficiency and comfort.

While basic dustpan design is generic, patent protection for unique features—such as proprietary locking mechanisms for lobby dustpans, integrated comb designs, or specialized lip materials—is crucial for brand differentiation, preventing immediate copying, and justifying premium pricing in highly competitive segments like professional cleaning tools.

Volatility in plastic resin prices (a key input cost) directly impacts manufacturing margins. Since the final product is often price-sensitive, manufacturers must manage profitability by securing long-term supply contracts, utilizing automated production lines to minimize operational costs, and passing on minimal increases only through specialized, high-value product lines.

Urban areas drive high-volume demand, characterized by a mix of residential, high-rise commercial, and institutional needs, leading to strong sales of both compact and professional lobby models. Rural areas show more moderate demand, often favoring traditional, basic models purchased through local hardware stores, with less emphasis on specialized ergonomic features.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.