ID : MRU_ 432299 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

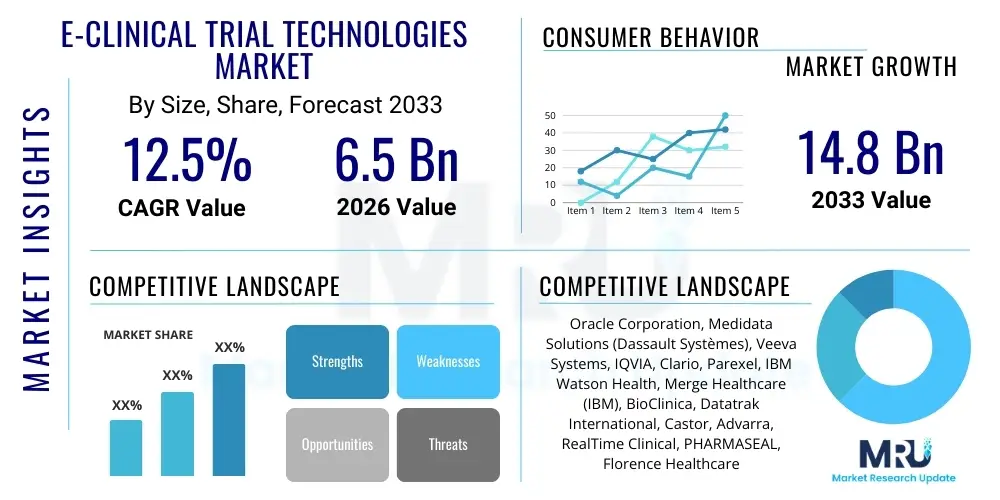

The E-Clinical Trial Technologies Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 14.8 Billion by the end of the forecast period in 2033.

The E-Clinical Trial Technologies Market encompasses a sophisticated suite of software solutions and services designed to streamline and manage the complex processes inherent in clinical research. These technologies facilitate the digital transformation of traditional paper-based trials, enhancing efficiency, improving data quality, and accelerating the drug development lifecycle. Key product categories include Electronic Data Capture (EDC) systems, Clinical Trial Management Systems (CTMS), Electronic Clinical Outcome Assessments (eCOA), Randomization and Trial Supply Management (RTSM), and Electronic Trial Master File (eTMF) solutions. The fundamental premise of these technologies is to create an integrated, secure, and globally accessible platform for all stakeholders, including sponsors, contract research organizations (CROs), site investigators, and regulatory bodies.

Major applications of E-Clinical Trial Technologies span across all phases of clinical development, from Phase I feasibility studies to Phase IV post-marketing surveillance, with significant penetration observed in therapeutic areas such as oncology, cardiology, central nervous system disorders, and infectious diseases. The increasing complexity of clinical protocols, coupled with the rising global incidence of chronic diseases and the resulting imperative to rapidly bring innovative treatments to market, drives the adoption of these platforms. Furthermore, the shift towards personalized medicine necessitates the collection and analysis of massive, diverse datasets, making manual processing infeasible and positioning e-clinical solutions as indispensable tools for modern research.

The principal benefits derived from deploying these advanced technologies include substantial reductions in operational costs, minimization of manual data entry errors, improved compliance with stringent global regulatory standards (such as FDA and EMA guidelines), and facilitation of Decentralized Clinical Trials (DCTs). Key driving factors bolstering market expansion involve the industry-wide embrace of virtualization in clinical operations, the critical need for real-time data monitoring and source data verification, and technological advancements focusing on interoperability and seamless integration across various clinical systems. This digital infrastructure is essential for managing the dispersed nature of global clinical research and ensuring the integrity and auditability of trial data.

The E-Clinical Trial Technologies Market is characterized by robust growth, primarily fueled by the accelerating trend toward Decentralized Clinical Trials (DCTs) and the increasing outsourcing of clinical development activities to Contract Research Organizations (CROs). Business trends emphasize consolidation among major technology providers, rapid adoption of Software-as-a-Service (SaaS) models for scalability, and a significant focus on integrating advanced analytics and artificial intelligence to optimize trial design and patient recruitment. Regional trends indicate continued dominance by North America due to early adoption, high R&D spending by pharmaceutical giants, and a mature regulatory environment supportive of digital health innovations. However, the Asia Pacific region is emerging as the fastest-growing market, driven by expanding patient populations, government investments in life sciences infrastructure, and lower operational costs encouraging clinical trial globalization.

Segment trends reveal that the Electronic Data Capture (EDC) segment maintains the largest market share, serving as the foundational platform for data collection, yet specialized segments like eCOA/ePRO and eTMF are exhibiting higher growth rates as sponsors prioritize patient-centric data gathering and compliance efficiency. Delivery modes are overwhelmingly shifting toward cloud-based deployment, offering flexible subscription models and superior system integration capabilities compared to traditional on-premise installations. This transition underscores the industry's need for agile, scalable IT infrastructure that can support multi-country trials and complex data requirements while ensuring stringent security and regulatory adherence across diverse jurisdictions.

User inquiries regarding AI's influence in E-Clinical Trial Technologies frequently center on its practical applications in enhancing operational efficiency and addressing core industry pain points, such as slow patient enrollment, high attrition rates, and the substantial time commitment involved in data cleaning. Common questions involve: "How effectively can AI predict trial success rates?", "What are the regulatory implications of using AI for primary endpoint analysis?", and "Can AI systems truly reduce the workload of site investigators?" The core concern underlying these queries is the balance between leveraging sophisticated algorithms for speed and maintaining the reliability, transparency, and ethical conduct required in regulated research environments.

The prevailing expectation is that AI will fundamentally transform key stages of the clinical lifecycle. In the initial phases, users anticipate AI-driven predictive modeling to select optimal trial sites and patient cohorts based on historical data and real-world evidence, significantly reducing screening failures. Furthermore, AI is expected to automate labor-intensive data management tasks, including continuous quality checks, standardization of diverse data inputs from wearable devices and electronic health records (EHRs), and identification of potential protocol deviations in real-time. This capability moves the industry toward proactive risk-based monitoring rather than reactive issue resolution.

However, the analysis reveals underlying user concerns related to the ‘black box’ nature of some deep learning models, posing challenges for regulatory submissions requiring explainability and audit trails. Therefore, the market is prioritizing the development of transparent, validated AI tools integrated directly into existing e-clinical platforms (EDC, CTMS) to ensure seamless adoption. This integration focuses on augmenting human decision-making—for instance, by flagging high-risk patients or suggesting optimal drug dosing adjustments—rather than replacing the oversight provided by clinical investigators and data review committees.

The E-Clinical Trial Technologies Market is driven by the industry's continuous pivot towards digitalization and decentralization, restrained by high initial investment costs and data security concerns, and presented with significant opportunities arising from emerging markets and therapeutic complexity. The primary Drivers include regulatory mandates promoting electronic data submission and the compelling need for operational efficiency to curb the soaring costs of drug development. Restraints manifest chiefly as challenges related to system interoperability, particularly integrating proprietary e-clinical solutions with diverse Electronic Health Record (EHR) systems globally, and the substantial technical expertise required for implementation and maintenance. Opportunities lie in expanding the adoption of mobile health (mHealth) tools for remote data collection and leveraging advanced analytics platforms to handle the influx of data from wearable technology and connected devices in patient homes.

The interplay of these factors defines the Impact Forces shaping market trajectory. The strong regulatory push (Driver) ensures continuous investment in compliant eTMF and CTMS solutions, overcoming some of the inertia associated with legacy systems. Conversely, while decentralized models offer vast cost savings (Opportunity), they simultaneously introduce heightened risk vectors related to data privacy (Restraint, specifically GDPR and HIPAA), forcing vendors to heavily invest in robust cybersecurity measures and geographically compliant cloud infrastructure. This dynamic interaction accelerates the development of integrated, unified clinical platforms capable of handling heterogeneous data sources while meeting stringent global privacy mandates.

Ultimately, the most potent impact force remains the economic pressure on pharmaceutical sponsors to reduce time-to-market. The competitive landscape necessitates rapid, high-quality execution of trials, placing E-Clinical Technologies, which promise faster enrollment and improved data integrity, squarely at the center of R&D strategy. This forces clinical research organizations to adopt best-in-class technology stacks, driving market penetration beyond initial early adopters toward mid-sized and niche biotechnology firms seeking competitive advantage in complex therapeutic fields such as cell and gene therapies.

The E-Clinical Trial Technologies market is primarily segmented based on Product, Delivery Mode, and End User, reflecting the diverse needs and operational models across the clinical research ecosystem. The Product segmentation is the most critical, comprising core categories like Electronic Data Capture (EDC) systems, Clinical Trial Management Systems (CTMS), Electronic Clinical Outcome Assessment (eCOA) solutions, and Safety and Pharmacovigilance systems. EDC platforms consistently hold the dominant share, serving as the backbone for regulatory submission-ready data collection, verification, and cleaning. However, the fastest-growing segments are those facilitating decentralization, specifically eCOA/ePRO, which enhance patient engagement and remote data collection capabilities, directly addressing the limitations of site-based monitoring.

Regarding Delivery Mode, the market has rapidly transitioned to a predominantly Cloud-based (SaaS) model. This shift is driven by the need for enhanced accessibility, reduced capital expenditure for infrastructure, and the ability to scale computational resources dynamically for large, global trials. While traditional On-Premise deployments still exist, primarily among organizations with legacy systems or extremely stringent, proprietary data governance policies, cloud deployment is becoming the industry standard due to its superior interoperability and support for real-time collaboration among geographically dispersed teams, essential for efficient trial execution and expedited database lock.

End User segmentation reveals that Pharmaceutical and Biotechnology companies are the largest consumers, utilizing these technologies extensively across their R&D pipelines. However, Contract Research Organizations (CROs) represent the fastest-growing end-user segment. As pharmaceutical companies increasingly outsource trial execution, CROs become major technology purchasers and integrators, investing heavily in unified platforms to offer scalable, standardized services to their diverse clientele. This outsourcing trend reinforces the demand for interoperable, vendor-neutral e-clinical systems that can seamlessly integrate across sponsors' varying technology stacks.

The E-Clinical Trial Technologies value chain is complex, starting with specialized software developers and extending through implementation partners to the end-users executing clinical protocols. The upstream segment involves core technology providers responsible for developing and maintaining the foundational software architecture, including database infrastructure, security protocols, and application programming interfaces (APIs) necessary for integration. These vendors continually invest in R&D to incorporate emerging technologies like AI, machine learning, and advanced cloud native architectures, ensuring the platforms remain compliant with global regulatory standards such as 21 CFR Part 11 and ICH GCP. Key activities in this stage include robust software testing, security auditing, and continuous iterative development based on user feedback and evolving regulatory guidelines.

The midstream segment is dominated by system integrators and Contract Research Organizations (CROs). CROs often act as the primary distribution channel and implementation experts, customizing and managing the e-clinical solutions on behalf of their pharmaceutical clients. They provide crucial services such as system validation, training for site staff, data management, and operational support. The effectiveness of the solution heavily relies on the quality of this midstream integration, which must ensure seamless data flow between disparate systems—such as linking CTMS data with EDC and eTMF platforms. Distribution channels are predominantly direct sales for major enterprise platforms, supplemented by partnerships and service agreements through these large CROs, allowing technology vendors to access a wider client base without extensive direct sales infrastructure.

The downstream segment consists of the end-users—pharmaceutical companies, biotech firms, and academic institutions—who consume the integrated technology to run their clinical trials. The focus at this stage is on utilizing the platform for actual data collection, monitoring, risk management, and regulatory submission preparation. Indirect channels, such as specialized consulting firms and value-added resellers (VARs), play a role in helping smaller biotech firms select, implement, and validate the appropriate technology stack, often leading to better optimization and faster time-to-value. The efficacy of the entire value chain is judged by the quality of the resulting clinical data and the overall efficiency achieved in achieving database lock.

The primary consumers of E-Clinical Trial Technologies are organizations deeply invested in the discovery, development, and commercialization of new medical therapies and devices, requiring rigorous regulatory compliance and efficient data management. Pharmaceutical and biotechnology companies constitute the largest customer base, driven by their expansive pipelines and the multi-billion dollar costs associated with bringing a single drug to market. These organizations leverage e-clinical solutions to manage complex global trials, ensure data integrity across numerous sites, and accelerate the regulatory submission process. Their purchasing decisions are highly influenced by system scalability, validated compliance features, and the vendor's reputation for long-term support and advanced security measures, making them consistent, high-value buyers.

Contract Research Organizations (CROs) are rapidly emerging as a critical customer segment, often acting as the decisive gatekeepers for technology adoption. As sponsors increasingly outsource their clinical operations, CROs must possess state-of-the-art, integrated e-clinical platforms to maintain competitiveness and offer standardized, high-quality services. CROs prioritize solutions that offer multi-tenant capabilities, broad therapeutic area expertise, and superior integration features, enabling them to efficiently manage trials for multiple sponsors simultaneously. Their demand drives innovation in platform unification and interoperability, as they require technology that can flexibly adapt to varying client specifications and regional data governance requirements.

Beyond these commercial entities, Academic and Research Institutions represent a vital segment, particularly those conducting investigator-initiated trials or large, government-funded studies. While budget constraints can be a factor, these institutions are increasingly adopting flexible, cloud-based e-clinical tools to manage complex cohort studies, focusing heavily on robust data governance and long-term data archival capabilities. Finally, Medical Device Manufacturers utilize these technologies, especially EDC and eTMF, to streamline their regulatory submissions and post-market surveillance activities, driven by evolving global standards for device safety and efficacy monitoring throughout the product lifecycle.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 14.8 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Oracle Corporation, Medidata Solutions (Dassault Systèmes), Veeva Systems, IQVIA, Clario, Parexel, IBM Watson Health, Merge Healthcare (IBM), BioClinica, Datatrak International, Castor, Advarra, RealTime Clinical, PHARMASEAL, Florence Healthcare, Clinical Data Management (CDM), MaxisIT, Calyx, TrialGrid, Greenlight Guru |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the E-Clinical Trial Technologies market is defined by a shift toward integrated, cloud-native platforms that prioritize interoperability, security, and scalability. The prevalence of the Software-as-a-Service (SaaS) model is paramount, allowing sponsors and CROs to subscribe to comprehensive suites of tools rather than managing disparate, siloed systems. This SaaS architecture facilitates rapid deployment and updates, ensures continuous compliance with evolving data standards (such as CDISC and HL7 FHIR), and dramatically lowers the total cost of ownership compared to traditional on-premise infrastructure. Furthermore, the reliance on robust Application Programming Interfaces (APIs) is critical, enabling seamless data exchange between core e-clinical systems (EDC, CTMS) and external data sources, including Electronic Health Records (EHRs) and patient-generated data from wearables, which is fundamental for effective decentralized trials.

A second major technological trend is the deep integration of advanced analytics, machine learning (ML), and artificial intelligence (AI) across the functional stack. ML algorithms are increasingly used in CTMS to optimize protocol design, forecast enrollment timelines, and manage trial supply logistics by predicting demand fluctuations. Similarly, AI assists in the continuous monitoring and analysis of vast datasets to identify patterns indicative of fraud, protocol deviations, or emerging safety signals that would be missed by human reviewers. This intelligent augmentation of the systems enhances the quality of data and transitions clinical monitoring from periodic, site-based checks to ongoing, risk-based surveillance, thus increasing efficiency and regulatory robustness.

Furthermore, the increased emphasis on patient-centricity drives the adoption of mobile technology, specifically through eCOA/ePRO solutions deployed via smartphones and tablets. These technologies ensure that data is collected directly from the patient in real-time, improving data accuracy and reducing patient burden. Coupled with this is the burgeoning use of blockchain technology, specifically for creating immutable audit trails and securely managing patient consent forms (eConsent). While still nascent, blockchain promises a higher level of data integrity and transparency, addressing industry concerns regarding data provenance and access control in multi-party clinical research environments, potentially revolutionizing how data sharing agreements are managed across global consortia.

The primary driver is the accelerating shift towards Decentralized Clinical Trials (DCTs), which necessitates integrated digital platforms (like ePRO and remote monitoring tools) to collect patient data outside traditional site settings efficiently while maintaining regulatory compliance and data quality.

AI significantly benefits operations by automating key processes such as patient recruitment optimization, predictive risk-based monitoring (identifying sites prone to error), and accelerating data cleaning and quality checks, thereby reducing trial duration and operational expenditure.

The Electronic Data Capture (EDC) segment currently holds the largest market share by product type, as it serves as the foundational system for capturing, managing, and validating clinical data required for regulatory submissions across all trial phases.

Key challenges include ensuring seamless interoperability between proprietary e-clinical systems and diverse Electronic Health Records (EHRs), the high initial capital investment required for implementation, and addressing persistent concerns surrounding global data privacy and security mandates like GDPR and HIPAA.

APAC is poised for the fastest growth due to the immense and largely untapped patient pool, increasing government initiatives promoting life sciences R&D infrastructure modernization, and the rising trend of global pharmaceutical companies conducting trials in the region to leverage lower operational costs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.