ID : MRU_ 436181 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

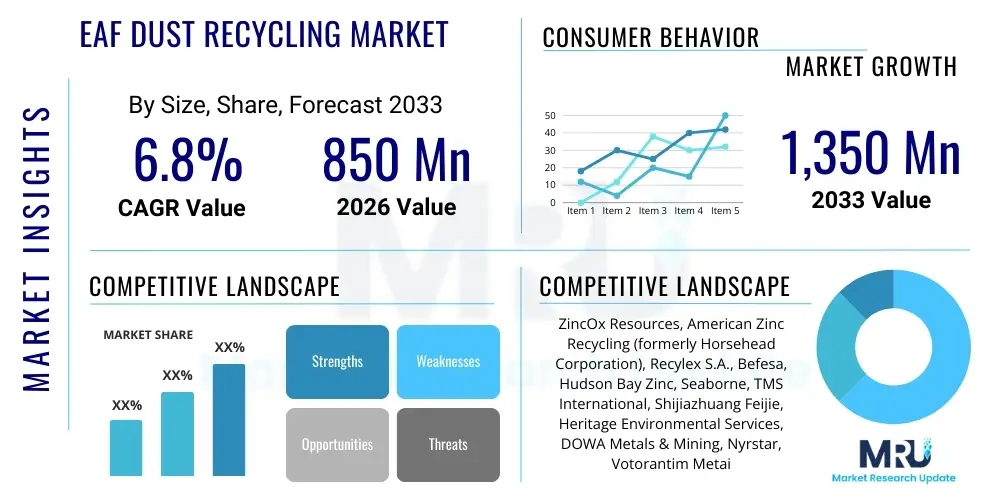

The EAF Dust Recycling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 850 million in 2026 and is projected to reach USD 1,350 million by the end of the forecast period in 2033.

The EAF Dust Recycling Market encompasses the processes and technologies utilized to treat and valorize Electric Arc Furnace (EAF) dust, a hazardous waste byproduct generated during the production of steel. EAF dust, typically classified as K061 waste by the U.S. EPA due to its high concentration of heavy metals, particularly zinc, lead, and cadmium, presents significant environmental disposal challenges. The recycling process aims to recover valuable elements, primarily zinc, and stabilize the remaining matrix, transforming a liability into a resource. This market is fundamentally driven by stringent environmental protection laws, the rising cost and scarcity of primary resources like zinc, and the steel industry’s ongoing commitment to circular economy principles and waste minimization.

The primary product derived from EAF dust recycling is marketable zinc oxide, which serves as a crucial input for zinc metal production, galvanizing processes, and chemical applications. Other recovered materials can include stabilized iron-bearing residues (suitable for aggregate or cement production) and other non-ferrous metals, depending on the feedstock composition and the chosen recycling technology. The major applications for recycled materials are deeply embedded within the metallurgical and construction sectors, providing sustainable alternatives to conventionally mined ores. The increasing global steel production, particularly utilizing the EAF route due to its lower carbon footprint compared to blast furnaces, ensures a sustained supply of EAF dust, thereby solidifying the necessity and growth trajectory of the recycling market.

Key benefits driving market adoption include significant reductions in landfill volume and associated disposal costs, compliance with global environmental mandates (such as the Basel Convention regarding hazardous waste movement), and the establishment of a robust secondary supply chain for strategic raw materials. Driving factors are multifaceted, ranging from technological advancements that improve recovery efficiency and lower operational costs—making recycling economically competitive against primary mining—to heightened corporate social responsibility (CSR) initiatives compelling steel producers to adopt sustainable waste management practices. Furthermore, governmental incentives and subsidies for waste valorization projects provide substantial financial momentum to market participants, promoting investment in specialized infrastructure and advanced processing capabilities across major steel-producing regions globally.

The EAF Dust Recycling Market demonstrates robust business trends characterized by consolidation and technological specialization. Leading market players are focusing on vertical integration, securing long-term contracts with major steel producers, and investing heavily in advanced thermal treatment and hydrometallurgical recovery systems to maximize zinc yield and purity. A significant trend is the shift towards on-site or near-site processing facilities, reducing logistical costs and optimizing the supply chain for waste feedstock. Furthermore, the market is experiencing increasing interest from diversified materials companies aiming to capitalize on the circular economy transition, leading to innovative partnership models between waste management specialists and raw material consumers. Profitability is increasingly tied to the ability to efficiently process dust with varying compositions and to successfully market the recovered zinc products under volatile commodity pricing conditions, necessitating flexible operational strategies and high-quality output standards.

Regionally, the market is spearheaded by established economies in North America and Europe, primarily due to rigorous environmental legislation and a mature regulatory framework that effectively mandates recycling or stabilization. These regions possess advanced technological infrastructure, including multiple large-scale Waelz process facilities, ensuring high recycling rates. However, the Asia Pacific (APAC) region, driven by massive growth in steel production (particularly in China and India) and rapidly evolving environmental standards, is projected to exhibit the fastest growth. APAC countries represent both the largest source of EAF dust generation and a rapidly expanding area for capacity development, often favored by international recycling firms seeking new growth avenues. Meanwhile, Latin America and the Middle East and Africa (MEA) are emerging markets, primarily focusing on basic stabilization methods, but are increasingly exploring sophisticated recovery technologies as local regulatory pressure increases.

Segmentation trends highlight the continued dominance of the Waelz process as the mainstream and commercially proven technology, especially for high-volume, continuous processing. However, hydrometallurgical and other novel pyrometallurgical methods are gaining traction, particularly for smaller-scale operations or for dust streams requiring higher purity zinc oxide or the recovery of other valuable minor elements (e.g., precious metals or specialized alloys). By source, the recycling of Carbon Steel EAF Dust dominates the volume segment, given its overwhelming prevalence in global steel production. Nevertheless, the Stainless Steel EAF Dust segment, while smaller in volume, attracts premium technological solutions due to the presence of high-value elements like nickel and chromium, which require specialized recovery techniques, thus demanding niche market expertise and optimized chemical processing methods for effective valorization.

User queries regarding AI's impact on EAF Dust Recycling frequently center on four main areas: optimizing process efficiency, improving material characterization for tailored recycling, enabling predictive maintenance to reduce downtime in capital-intensive recycling plants, and enhancing supply chain logistics for dust collection. Users are keen to understand how AI-driven analytics can handle the heterogeneity of EAF dust composition, which significantly affects recovery yields and reagent consumption in complex processes like Waelz or hydrometallurgy. Key themes emerging from user expectations involve utilizing machine learning for real-time sensor data interpretation within furnaces and reactors to dynamically adjust operating parameters (temperature, flow rates, reductant addition), thereby maximizing metal recovery rates, minimizing energy consumption, and ensuring the final product meets stringent quality specifications without manual intervention. The integration of AI is seen not as a replacement for core recycling technologies but as a sophisticated optimization layer essential for achieving economic viability and environmental excellence in a high-variability processing environment.

The EAF Dust Recycling Market is profoundly shaped by a unique combination of Drivers, Restraints, and Opportunities, collectively forming the Impact Forces determining its trajectory. Key drivers include rigorous global environmental regulations that categorize EAF dust as hazardous, necessitating mandatory treatment or valorization, coupled with the escalating demand for high-purity zinc in key industrial applications, solidifying the economic imperative for recovery. The opportunities lie primarily in technological innovation, such as the commercial scaling of advanced hydrometallurgical processes that promise higher recovery efficiency and purity compared to conventional methods, and the expansion into emerging markets where steel production is growing rapidly but recycling infrastructure is nascent. However, the market faces significant restraints, notably the high capital expenditure required for sophisticated recycling plants, the volatility of zinc commodity prices which directly impacts the return on investment, and the consistent challenge posed by the heterogeneous and variable composition of EAF dust feedstock, complicating stable process operation.

The impact forces exert pressure on stakeholders to balance economic viability with regulatory compliance. Strong government support through extended producer responsibility schemes and tax incentives acts as a significant positive force, mitigating the risk associated with large initial investments. Conversely, the operational costs, particularly energy consumption in pyrometallurgical processes and chemical reagent costs in hydrometallurgy, act as restraining forces, requiring continuous optimization and efficiency gains. The inherent circularity of the market—where recycled zinc replaces primary mined zinc—positions it favorably against sustainability trends, serving as a powerful long-term driver. Successful navigation of these forces depends heavily on technological differentiation, securing stable feedstock supply through long-term contracts, and achieving economies of scale in processing operations to withstand commodity price fluctuations and maintain profitability.

A critical impact force is the necessity for regionalized solutions. Due to the high logistics cost associated with transporting bulky hazardous waste like EAF dust, market development often favors localized processing hubs. This provides opportunities for specialized regional players but can restrain global expansion for standardized mega-facilities unless located strategically near large steel clusters. The continuous evolution of steelmaking practices, which may alter the characteristics of the dust, necessitates adaptable recycling technologies, making innovation a constant market imperative. Ultimately, the market is driven by the confluence of waste management legislation and commodity economics; as regulatory standards tighten globally and the demand for sustainably sourced materials increases, the inherent value proposition of EAF dust recycling becomes undeniably stronger, pushing the market towards further growth and technological maturity, overcoming existing barriers related to CAPEX and price volatility.

The EAF Dust Recycling Market is systematically segmented based on Technology, Source of Dust, and Application of the recovered materials. The technology segment is critical as it defines the capital cost, operational complexity, and the purity of the recovered products. The primary technologies, including Pyrometallurgical (Waelz), Hydrometallurgical, and emerging integrated methods, each address specific needs related to dust composition and economic goals. Segmentation by source differentiates between dust generated from carbon steel production, which constitutes the bulk of the volume, and stainless steel production, which, although smaller, contains higher-value elements like nickel and chromium, dictating specialized recovery paths. Application segmentation tracks where the market value is ultimately realized, primarily focusing on the use of recovered zinc oxide in various industries, thereby linking the recycling market directly to the global zinc commodity cycle and construction aggregates demand.

The value chain for the EAF Dust Recycling Market is structured around the transformation of a hazardous waste stream (upstream) into high-value secondary raw materials (downstream). Upstream analysis involves the generation and collection of EAF dust, primarily originating from steel mills. This stage is dominated by logistics, environmental compliance, and securing long-term waste handling contracts between steel producers and recycling operators. The quality and volume consistency of the dust feedstock are critical upstream factors, heavily influenced by the specific scrap mix and operational procedures of the EAF facility. Efficient collection, handling, and transportation (often requiring specialized, secure transport due to the hazardous nature of the dust) dictate a substantial portion of the initial operational cost for recyclers.

The core of the value chain is the processing stage, where specialized recycling companies convert the collected dust using technologies like the Waelz process or hydrometallurgy. This conversion stage adds the most significant value, transforming unusable waste into marketable intermediate products, primarily impure zinc oxide (Waelz oxide) or purer zinc compounds. Downstream analysis focuses on the end-use applications of these recovered materials. The primary downstream consumers are zinc refineries that process the Waelz oxide into pure zinc metal, galvanizing companies, or chemical manufacturers utilizing zinc compounds. The stability of the downstream market—dictated by global zinc prices and demand from the automotive and construction sectors—is crucial for the profitability of the entire chain. Secondary downstream outputs, such as inert iron residues, are often channeled into the construction industry for use as aggregates or supplementary cementitious materials.

The distribution channel often involves both direct and indirect routes. Direct distribution typically occurs when large, vertically integrated recyclers (or those with dedicated processing partnerships) supply their recovered zinc oxide directly to a handful of large, established zinc refiners under long-term supply agreements. This provides stability but requires stringent quality control. Indirect distribution involves using commodity brokers and specialized metal traders to sell the recovered product into the global market, particularly for smaller volumes or specialized niche products. Given the global nature of both steel production and zinc commodity trading, the distribution network is highly internationalized, relying on established global logistics networks and adherence to international trade standards for metallic raw materials. The ability of the recycling firm to consistently meet end-user purity specifications is the ultimate determinant of success in the downstream market.

The primary potential customers and end-users in the EAF Dust Recycling Market are diverse, ranging from integrated zinc producers who require zinc oxide feedstock to various heavy industries utilizing processed residues. The most significant buyers are global metallurgical facilities and specialized chemical companies that rely on high-purity zinc compounds for their manufacturing processes. These customers value the recycled material not only for its competitive pricing compared to primary ores but also for the environmental credentials associated with using secondary resources, which helps them meet their own sustainability targets.

Specifically, zinc metal refineries represent the core market for the primary recovered product (Waelz oxide). These refineries, utilizing electro-winning or other refining techniques, convert the oxide into zinc metal used predominantly for galvanizing steel to prevent corrosion, a high-volume application in infrastructure and automotive manufacturing. Additionally, the construction industry serves as a crucial buyer for the residual, stabilized slag and aggregate materials resulting from the recycling processes. Cement manufacturers utilize these inert residues as inputs to reduce their reliance on virgin clinker production, thereby supporting low-carbon concrete initiatives.

A smaller, yet high-value, segment of potential customers includes specialized chemical and pharmaceutical manufacturers that require highly purified zinc compounds derived through advanced hydrometallurgical processes. These niche applications, often requiring specific grades and low impurity levels, offer recyclers a premium price point, emphasizing the importance of technology selection. Essentially, the customer base spans the entire industrial ecosystem reliant on zinc and bulk construction materials, meaning the market viability is closely linked to macro-economic indicators affecting global construction, infrastructure spending, and automotive production.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 million |

| Market Forecast in 2033 | USD 1,350 million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ZincOx Resources, American Zinc Recycling (formerly Horsehead Corporation), Recylex S.A., Befesa, Hudson Bay Zinc, Seaborne, TMS International, Shijiazhuang Feijie, Heritage Environmental Services, DOWA Metals & Mining, Nyrstar, Votorantim Metais, Global Steel Dust (GSD), Metallurgical Zinc, Boliden Group, Korea Zinc, Umicore, Trafigura, Glencore, Toxfree. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The EAF Dust Recycling market is defined by several core technological pathways, each designed to address the challenges of dust heterogeneity and heavy metal recovery. The Waelz process, a specialized pyrometallurgical technique utilizing rotary kilns, remains the dominant global technology due to its established commercial maturity, ability to handle large volumes, and relatively broad tolerance for varying dust compositions. This high-temperature process volatilizes zinc and lead into a crude intermediate product known as Waelz oxide, which then requires further refining. However, the Waelz process is energy-intensive and may not achieve the highest purity levels required by specific end-users, prompting exploration into complementary or alternative methods to improve overall resource efficiency and recovery rates for complex dust streams.

Hydrometallurgical technologies, involving acid or base leaching followed by purification steps like solvent extraction or electrolysis, represent the cutting-edge of the technological landscape. These processes offer superior control over product purity, often yielding zinc metal directly or highly pure zinc compounds, and are particularly effective for recovering multiple valuable non-ferrous metals simultaneously, especially from stainless steel EAF dust. While hydrometallurgy generally involves lower operating temperatures, reducing energy costs, it typically requires more intensive pre-treatment and specialized reagent handling, increasing operational complexity and initial capital outlay. The trend is moving towards integrating pyro- and hydro- approaches, where a initial pyrometallurgical step stabilizes the iron fraction while a subsequent hydrometallurgical circuit purifies and extracts the non-ferrous components with high precision.

Other emerging technologies include plasma smelting and various rotary hearth furnace (RHF) applications. Plasma technology utilizes extremely high temperatures to decompose the dust matrix, offering excellent environmental control and the ability to produce highly stable iron residue, but it is generally reserved for niche, high-value dust streams due to the high energy costs and operational complexity. RHF technology is often employed for specialized dust compositions or for smaller scale operations, producing metallic iron and zinc vapor. Technological innovation is continuously focused on reducing the environmental footprint (e.g., minimizing sludge waste), lowering energy consumption, and increasing the overall economic yield by recovering more minor elements. The competitive advantage in the market is increasingly held by companies that can deploy modular, flexible technologies capable of processing variable feedstock with high efficiency and low environmental emissions, moving beyond the traditional constraints of the single-process Waelz model.

EAF Dust (Electric Arc Furnace Dust) is a hazardous waste byproduct (K061) generated during the melting of scrap steel. It contains high concentrations of heavy metals, predominantly zinc, lead, and cadmium. Recycling is essential to comply with strict environmental regulations, prevent landfill contamination, and recover valuable metals, primarily zinc, supporting the circular economy by creating secondary raw materials for industrial use.

The Pyrometallurgical Waelz process is the most commercially dominant technology globally. It uses a high-temperature rotary kiln to volatilize zinc and lead into an impure oxide product (Waelz oxide). Its popularity stems from its proven reliability, ability to handle high volumes, and tolerance for varying dust compositions, despite being relatively energy-intensive.

The profitability of EAF dust recycling is directly linked to global zinc commodity prices, as recovered zinc oxide is the primary marketable product. Low zinc prices reduce the economic incentive for recycling and can negatively impact the return on investment for large-scale facilities, making long-term stable feedstock contracts and efficiency optimization crucial for maintaining margins.

The Asia Pacific (APAC) region, led by major steel-producing nations like China and India, is projected to exhibit the highest growth rate. This accelerated growth is driven by the region's vast and increasing generation of EAF dust and the rapid implementation of stringent governmental environmental policies that are pushing steel mills toward mandatory waste valorization and advanced recycling solutions.

Beyond the primary recovery of zinc oxide, EAF dust recycling processes, particularly advanced hydrometallurgical and specialized pyrometallurgical methods, can recover lead, cadmium, and stabilize the iron matrix. For stainless steel dust, high-value elements like nickel and chromium are recovered, often utilized as inputs for stainless steel alloying or chemical production, adding significant economic value to the process.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.