ID : MRU_ 431854 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

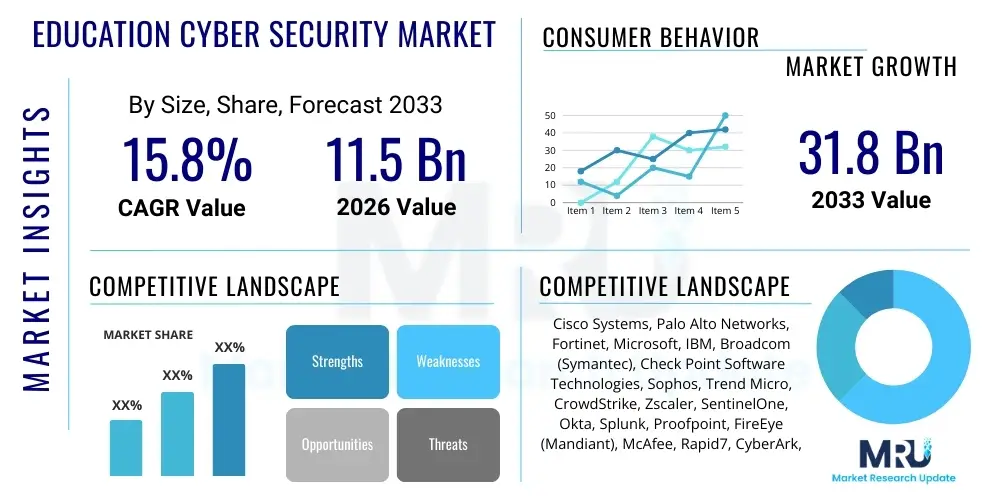

The Education Cyber Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 11.5 Billion in 2026 and is projected to reach USD 31.8 Billion by the end of the forecast period in 2033.

The Education Cyber Security Market encompasses specialized security solutions and services designed to protect the increasingly digitalized infrastructure, sensitive data, and network integrity of academic institutions, ranging from K-12 schools to large universities and burgeoning EdTech companies. Driven by the proliferation of Bring Your Own Device (BYOD) policies, the necessity for remote learning environments (accelerated post-2020), and the transition to cloud-based learning management systems, educational entities now manage vast amounts of personally identifiable information (PII) belonging to students and faculty, making them prime targets for malicious actors. Effective cyber defense strategies in this sector focus on multilayered protection, encompassing identity and access management (IAM), endpoint security, robust network monitoring, and mandatory compliance with data privacy regulations such as GDPR, FERPA, and various regional standards.

Key market drivers include the rising sophistication of cyberattacks, particularly phishing, ransomware, and Distributed Denial of Service (DDoS) attacks, which frequently target resource-constrained school districts and universities due to perceived vulnerabilities and high-value research data. The market offerings span software solutions like firewall protection, intrusion detection systems (IDS), and specialized education-focused security platforms, alongside professional services such as security consulting, managed security services (MSS), and incident response planning. Major applications center around securing campus networks, protecting research intellectual property, ensuring the continuity of online learning operations, and mitigating internal threats stemming from student and faculty network usage. The primary benefit derived by institutions is maintaining trust, ensuring regulatory adherence, and preventing significant financial and reputational damage resulting from a data breach.

The Education Cyber Security Market is experiencing accelerated growth fueled by the mandated shift towards digital learning ecosystems and the escalating threat landscape specific to academic environments. Business trends indicate a strong move toward integrated security frameworks, prioritizing Security as a Service (SaaS) models and adoption of Zero Trust Architecture (ZTA) to manage thousands of diverse endpoints and users, including transient student populations accessing resources from varied locations. Vendors are focusing on developing AI-enhanced threat detection tools tailored to educational traffic patterns and the unique challenges associated with managing minors' data, driving significant investment in automation and predictive intelligence within security operations centers (SOCs) dedicated to the education sector. Furthermore, mergers and acquisitions among established cybersecurity firms and niche EdTech security providers are shaping the competitive landscape, aiming to offer comprehensive, one-stop solutions.

Regional trends highlight North America and Europe as the dominant markets, largely due to stringent regulatory environments like FERPA and GDPR, coupled with high digital penetration rates in higher education. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth CAGR, driven by massive government initiatives promoting digital education infrastructure in countries like India and China, creating a large, emerging surface area for cyber defense requirements. Segment trends reveal that Cloud Security and Managed Security Services (MSS) are the fastest-growing segments, reflecting institutions' struggles to recruit and retain in-house cybersecurity talent, thereby outsourcing complex monitoring and incident response functions. Additionally, the proliferation of specialized IoT devices within smart campuses, such as surveillance systems and digital classroom tools, is significantly boosting the demand for endpoint and network access control solutions across all educational levels.

Common user questions regarding AI's impact on education cybersecurity revolve around how AI can handle the sheer volume of alerts generated by large campus networks, whether it can effectively identify sophisticated social engineering attacks targeting students and staff, and the ethical implications of using AI for surveillance or behavior analysis in educational settings. Users are concerned about the dual-use nature of AI—that it can both enhance defense mechanisms and simultaneously empower advanced attackers to create more personalized and evasive malware. The consensus theme is a strong expectation that AI should provide proactive defense capabilities, automate tedious compliance monitoring, and offer enhanced anomaly detection specifically tuned for the unique, often unpredictable, user behavior typical of academic environments, ensuring faster response times to novel threats while minimizing false positives.

The Education Cyber Security Market is primarily driven by the mandatory digital transformation of learning environments, escalating regulatory compliance requirements (particularly concerning student PII), and the demonstrated vulnerability of educational institutions to high-profile ransomware and data exfiltration events. Restraints include significant budget constraints common across public education systems globally, a pervasive skills gap in dedicated cybersecurity staff within academic IT departments, and the difficulty of implementing security policies that do not impede the necessary openness required for academic collaboration and research. Opportunities lie in the shift towards cloud-centric security architectures, the emergence of highly specialized EdTech security solutions, and the potential for public-private partnerships to subsidize advanced security deployment in lower-income school districts. These factors collectively exert powerful impact forces, forcing institutions to transition from basic perimeter defenses to proactive, multi-layered security models.

The impact forces are largely characterized by the intensity of competitive rivalry among security vendors, focusing on differentiation through managed services tailored to education-specific needs (e.g., student monitoring compliant with specific local laws). The bargaining power of buyers is high, especially among large university systems that can negotiate favorable terms for enterprise security suites, while the threat of substitutes is relatively low, as custom-built internal security solutions are generally cost-prohibitive compared to specialized commercial offerings. Crucially, the external threat landscape, driven by increasingly organized cybercrime syndicates targeting education, acts as the most significant external force, constantly compelling institutions to increase their cybersecurity expenditure despite budgetary challenges. This dynamic environment ensures sustained demand for sophisticated, specialized security tools and outsourced security expertise.

The Education Cyber Security Market is comprehensively segmented across several key dimensions, providing clarity on where investment priorities are being placed within the sector. Segmentation by Component distinguishes between hardware, software, and services, reflecting the shift from physical security appliances to subscription-based software and outsourced security expertise. By Deployment Model, the market recognizes the rapid move from traditional on-premise security towards cloud and hybrid models, particularly for LMS and student data storage. The application segment details the specific areas of protection, such as endpoint security, network security, and application security, while the end-user segmentation clearly separates K-12, Higher Education, and other EdTech providers, each having distinct compliance and attack surface requirements.

The value chain for the Education Cyber Security Market starts with the upstream activities of core technology providers, including hardware manufacturers and specialized software developers focused on encryption, authentication algorithms, and threat intelligence. These firms invest heavily in R&D to maintain cutting-edge defenses against evolving threats. Midstream activities involve the integration and solution providers, often large system integrators or Managed Security Service Providers (MSSPs), who package disparate security technologies into comprehensive, education-specific frameworks, ensuring compatibility with common academic software environments like Moodle or Blackboard. This stage is crucial for translating complex technology into manageable, compliant solutions for school districts.

Downstream analysis focuses on distribution channels and direct engagement with the end-users. Direct channels involve major cybersecurity firms selling large, customized enterprise licenses directly to university CIOs or large governmental education bodies. Indirect distribution relies heavily on regional value-added resellers (VARs) and dedicated education technology consultants who possess localized knowledge of funding mechanisms and regulatory mandates pertinent to local school boards. These indirect partners often provide the necessary post-sales support and ongoing monitoring. The efficiency of the downstream distribution, particularly the availability of highly skilled MSSPs specializing in FERPA or GDPR compliance, determines the successful adoption and effectiveness of cybersecurity measures within the diverse educational landscape.

The primary potential customers and end-users of education cyber security solutions are broadly categorized into three distinct groups: K-12 institutions, Higher Education bodies (universities and colleges), and emerging EdTech platforms. K-12 school districts represent a vast, though often budget-constrained, customer base requiring foundational security measures, content filtering, and robust protection against student data privacy breaches (COPPA and FERPA compliance being critical). Their purchasing decisions are often centralized by district IT managers looking for cost-effective, scalable, and easy-to-manage solutions suitable for non-technical administrative staff.

Higher Education institutions, encompassing major research universities and large community colleges, constitute the most lucrative customer segment due to the complexity of their networks, high volume of sensitive research intellectual property, and extensive reliance on cloud environments and IoT devices across large campuses. These entities demand advanced persistent threat (APT) defense, strong Identity and Access Management (IAM) solutions, and sophisticated data loss prevention (DLP) to protect multi-million-dollar research grants. Lastly, EdTech companies, ranging from massive open online course (MOOC) providers to specialized learning software developers, represent a rapidly growing customer base that requires security integration into their product development cycle (DevSecOps) to ensure their platforms comply with global data handling standards, protecting both corporate IP and client PII.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 31.8 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems, Palo Alto Networks, Fortinet, Microsoft, IBM, Broadcom (Symantec), Check Point Software Technologies, Sophos, Trend Micro, CrowdStrike, Zscaler, SentinelOne, Okta, Splunk, Proofpoint, FireEye (Mandiant), McAfee, Rapid7, CyberArk, Varonis |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Education Cyber Security market heavily relies on several foundational and emerging technologies tailored to address the unique challenges of academic networks. Core infrastructure protection still mandates next-generation firewalls (NGFWs) and Intrusion Detection/Prevention Systems (IDPS) capable of handling massive bandwidth demands generated by simultaneous users accessing diverse applications (video conferencing, research databases, streaming media). Crucially, the rise of remote and hybrid learning has accelerated the deployment of Secure Access Service Edge (SASE) frameworks, which converge network security functions (like firewall as a service and secure web gateway) with Wide Area Networking (WAN) capabilities, simplifying security management for geographically dispersed students and faculty while ensuring consistent policy enforcement regardless of the access location.

Furthermore, Identity and Access Management (IAM) technologies, particularly Multi-Factor Authentication (MFA) and Single Sign-On (SSO), are paramount given the high turnover rate of user accounts (students graduating, staff changing roles). Educational institutions are increasingly adopting robust IAM solutions integrated with learning management systems (LMS) to enforce strong password policies and manage user access lifecycle automatically, significantly reducing the risk of credential stuffing attacks. The adoption of Zero Trust Architecture (ZTA) is gaining traction, driven by the need to treat every user and device, whether on campus or remote, as potentially untrusted, requiring continuous verification before granting access to resources, essential for protecting high-value research data from both external breaches and internal threats.

On the data protection front, Data Loss Prevention (DLP) tools, often integrated with AI to classify sensitive PII (like student IDs or health records), are essential for maintaining regulatory compliance (FERPA). These systems monitor data movement both in transit and at rest, preventing accidental or malicious exfiltration of student records or proprietary research intellectual property. Coupled with these defenses, Security Information and Event Management (SIEM) solutions, enhanced with Security Orchestration, Automation, and Response (SOAR) capabilities, provide the necessary visibility and automated response mechanisms required for lean IT teams to effectively monitor complex environments, prioritizing genuine threats among the deluge of daily security alerts.

The K-12 sector is predominantly targeted by ransomware attacks aiming to disrupt operations and phishing campaigns designed to steal sensitive student and staff PII. Since K-12 IT teams often have limited resources, they are increasingly susceptible to basic, high-volume attacks, necessitating strong endpoint protection and mandatory staff training on threat recognition.

Higher education implements ZTA by enforcing strict least-privilege access and continuous verification, crucial for securing transient users (students) and highly sensitive research data. ZTA helps manage the complex network access needs arising from BYOD policies and the use of numerous specialized IoT devices across large campus networks, ensuring internal segmentation.

MSS providers allow educational institutions, especially smaller districts, to outsource sophisticated security operations, monitoring, and incident response functions to specialized third parties. This allows institutions to access 24/7 expert coverage and advanced technology without incurring the prohibitive costs and challenges associated with recruiting and retaining highly skilled in-house cybersecurity professionals.

In North America, the Family Educational Rights and Privacy Act (FERPA) is paramount, protecting student educational records. Globally and across Europe, the General Data Protection Regulation (GDPR) dictates stringent requirements for handling personal data, significantly driving investment in Data Loss Prevention (DLP) and enhanced data governance policies within academic IT systems.

The shift to cloud-based LMS platforms necessitates a move from traditional perimeter security to robust cloud security posture management (CSPM) and strong Identity and Access Management (IAM). Institutions must ensure that shared responsibility models are clearly understood and that data stored in the cloud remains encrypted and compliant with regional data sovereignty laws.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.