ID : MRU_ 435688 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

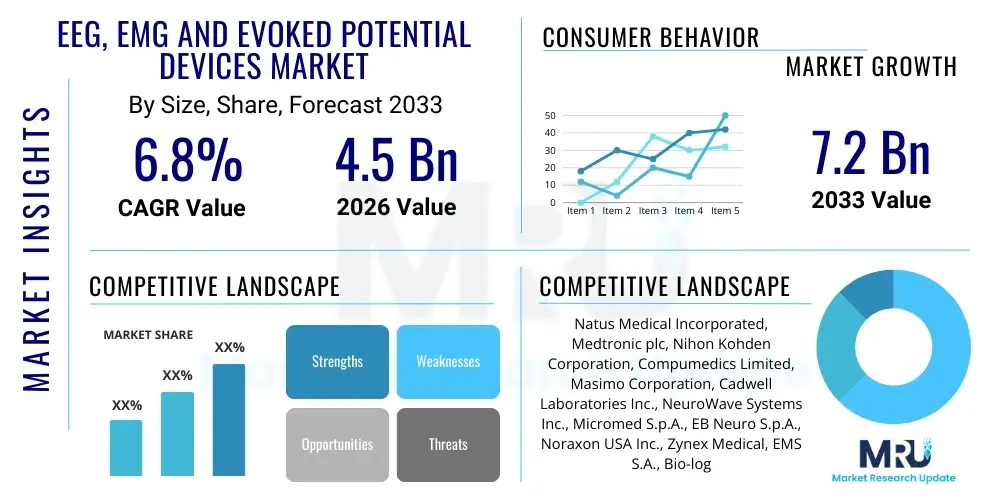

The EEG, EMG and Evoked Potential Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.2 Billion by the end of the forecast period in 2033.

The EEG (Electroencephalography), EMG (Electromyography), and Evoked Potential (EP) Devices Market encompasses advanced neurophysiological monitoring equipment essential for diagnosing and managing a wide array of neurological, neuromuscular, and sleep disorders. These devices are non-invasive tools used by neurologists, neurosurgeons, and clinical physiologists to record and analyze electrical activity in the brain, spinal cord, peripheral nerves, and muscles. The core product offering includes sophisticated digital systems, specialized electrodes, portable devices, and integrated software platforms that facilitate signal acquisition, artifact removal, and quantitative analysis, enabling precise diagnostic accuracy for conditions like epilepsy, peripheral neuropathy, multiple sclerosis, and various sleep disorders. The versatility and specificity of these technologies ensure their indispensable role in clinical diagnostics, intraoperative monitoring, and neuroscientific research worldwide, driving consistent demand across diverse healthcare settings.

Major applications for EEG, EMG, and EP devices span across clinical diagnostics, specialized neurological testing centers, and surgical monitoring environments. EEG devices are critically used for diagnosing seizure disorders, monitoring brain activity during coma, and studying sleep architecture, necessitating high-density electrode arrays and robust data processing capabilities. EMG and Nerve Conduction Studies (NCS) are fundamental for assessing the health of muscles and the nerve cells that control them, providing vital information for patients suffering from carpal tunnel syndrome, radiculopathy, or motor neuron diseases. Evoked Potential devices, including Visual Evoked Potentials (VEP), Auditory Evoked Potentials (AEP), and Somatosensory Evoked Potentials (SSEP), are paramount for evaluating sensory pathways and detecting central nervous system dysfunction, often employed during complex spinal and brain surgeries to prevent iatrogenic injury, thereby ensuring patient safety and improving surgical outcomes through real-time physiological feedback.

The primary driving factors sustaining market growth include the escalating global prevalence of neurological diseases such as Alzheimer's, Parkinson's disease, and stroke, coupled with a rapidly aging global population which inherently requires more frequent neurophysiological assessments. Furthermore, continuous technological advancements, particularly in miniaturization, portability (leading to the rise of wearable and home-based devices), and the integration of advanced software for automated interpretation, are significantly enhancing the accessibility and utility of these diagnostic tools. Governments and private healthcare providers are increasingly investing in sophisticated diagnostic infrastructure, especially in emerging economies, recognizing the imperative need for early and accurate diagnosis in neurological care. The demonstrated clinical benefits—including non-invasiveness, relatively low cost compared to advanced imaging, and high diagnostic specificity—solidify the market position of EEG, EMG, and EP devices as cornerstone technologies in modern neurology.

The EEG, EMG, and Evoked Potential Devices Market is experiencing robust expansion, fundamentally driven by technological innovation centered on improving signal quality, enhancing portability, and integrating machine learning algorithms for automated analysis. Key business trends indicate a strong move towards subscription-based software models and integrated platform solutions that combine multiple neurophysiological modalities into a single system, offering streamlined workflow and reducing infrastructural complexity for hospitals and clinics. Strategic mergers, acquisitions, and partnerships are prevalent, particularly those focused on acquiring specialized sensor technology or advanced cloud-based data management capabilities to capture growing segments such as remote patient monitoring and tele-neurology services. Furthermore, compliance with increasingly stringent regulatory standards, particularly in North America and Europe concerning medical device cybersecurity and data privacy (like GDPR and HIPAA), necessitates significant R&D investment, shaping competitive dynamics towards established players capable of meeting these complex requirements.

Regionally, North America maintains its dominance due to high healthcare expenditure, established clinical guidelines promoting the use of these diagnostics, and the presence of major industry innovators. However, the Asia Pacific (APAC) region is poised for the fastest growth, fueled by massive population bases, increasing awareness of neurological disorders, and rapid expansion of healthcare infrastructure, especially in countries like China and India, which are rapidly adopting advanced neurodiagnostic equipment through government procurement and foreign direct investment. Europe demonstrates stable growth, primarily driven by strong academic research funding and public health initiatives focused on managing chronic conditions like epilepsy and sleep apnea. The Middle East and Africa (MEA) and Latin America are emerging markets, characterized by increasing access to specialized medical training and a gradual transition from outdated analog systems to modern digital neurophysiology equipment, presenting substantial opportunities for market penetration by multinational corporations.

In terms of segmentation trends, the Product segment indicates a decisive shift towards digital EEG systems and portable EMG devices, which offer superior data handling and flexible deployment compared to older analog versions. The End-Use segment is highly dynamic, with hospitals retaining the largest share, yet the fastest growth is observed in specialized neurological centers and ambulatory surgical centers, reflecting the decentralization of diagnostic services. Application-wise, the demand for devices used in Sleep Monitoring is escalating significantly, capitalizing on the rising diagnosis rates of obstructive sleep apnea and other sleep-related movement disorders, closely followed by critical applications in Intraoperative Monitoring (IOM), which mandates real-time, highly reliable neurophysiological feedback to mitigate surgical risks during complex procedures involving the central nervous system.

User inquiries regarding the impact of Artificial Intelligence (AI) on the EEG, EMG, and Evoked Potential Devices Market frequently center on automation, diagnostic accuracy, and the changing role of the clinical physiologist. Common concerns revolve around how AI algorithms, specifically deep learning models, are being integrated to automatically detect epileptic spikes, classify sleep stages (polysomnography), and identify subtle pathological patterns in EMG signals that might be missed by human observers. Users are keen to understand the validation standards for these AI-driven diagnostic aids and whether they truly reduce the burden of manual waveform analysis, which is traditionally time-intensive and susceptible to inter-reader variability. Furthermore, there is significant interest in AI's role in predictive diagnostics, particularly leveraging longitudinal neurophysiological data combined with clinical metadata to forecast disease progression or treatment responsiveness, moving the field beyond purely descriptive diagnostics toward personalized neurology.

The integration of AI, machine learning (ML), and deep learning (DL) models is fundamentally revolutionizing the workflow associated with neurophysiological data analysis. AI systems are increasingly being utilized for enhanced signal processing, significantly improving the quality of raw data by filtering out noise and movement artifacts automatically, a critical challenge in clinical settings, especially in pediatric or intensive care units. This technological evolution allows clinicians to focus on complex cases rather than routine data cleaning. Moreover, AI aids in rapid interpretation, providing preliminary reports and quantitative metrics (QEEG, Quantitative EMG) that standardize diagnostic measurements and accelerate throughput, thereby addressing the growing global shortage of highly specialized neurophysiologists. This shift translates into more efficient use of resources and quicker turnaround times for patient results, directly impacting clinical efficacy.

Beyond automation, AI is fostering the development of entirely new diagnostic parameters derived from complex patterns that are otherwise opaque to conventional analysis. For instance, sophisticated algorithms can analyze spectral power changes in EEG associated with cognitive load or early stages of neurodegeneration, potentially creating novel biomarkers for conditions currently lacking definitive, early detection methods. However, the regulatory path for these AI-driven software as a Medical Device (SaMD) products remains a key challenge, requiring rigorous clinical validation to ensure safety and reliability. As AI tools become more integrated, ethical considerations regarding algorithmic bias and the accountability of diagnostic outcomes become paramount, necessitating transparent, explainable AI (XAI) models to maintain clinician trust and ensure widespread clinical adoption across diverse patient populations and healthcare systems globally. The net impact is one of augmentation, enhancing the expertise of the neurophysiologist rather than replacing it.

The EEG, EMG, and Evoked Potential Devices Market is primarily driven by the increasing incidence and prevalence of neurological disorders globally, which necessitates highly reliable, non-invasive diagnostic tools for accurate patient stratification and monitoring. This demographic shift, coupled with an aging population, significantly expands the base of patients requiring neurophysiological assessment. Furthermore, technological leaps in device miniaturization, which enable the creation of highly portable and wireless EEG and EMG systems, are dramatically improving patient comfort and expanding the use of these devices into home-care settings and remote monitoring scenarios, thereby overcoming traditional logistical barriers associated with hospital-based diagnostics. The growing recognition of the economic benefits of early and accurate diagnosis in reducing long-term healthcare costs also acts as a powerful driver, encouraging government and institutional investment in advanced neurodiagnostic infrastructure across both developed and developing regions.

However, the market faces significant restraints, chiefly the high initial cost associated with advanced digital systems, particularly high-density EEG systems and specialized intraoperative monitoring platforms, which can deter adoption in lower-resource healthcare settings and smaller clinics. A second critical restraint is the need for highly skilled, specialized technical personnel to operate, maintain, and accurately interpret the complex data generated by these devices; the global shortage of trained neurophysiologists and neurophysiology technologists limits the scalability of these services, particularly in rural and underserved areas. Moreover, data management and interoperability challenges arise from the large volumes of complex waveforms generated, requiring sophisticated storage, security, and integration with existing Electronic Health Records (EHR) systems, presenting technical hurdles that must be consistently addressed by manufacturers.

Opportunities for exponential market growth lie in the rapid expansion of tele-neurology and remote patient monitoring services, accelerated by favorable regulatory changes and increased acceptance following recent global events. The development of advanced, dry electrode technology presents a significant opportunity by eliminating the need for abrasive skin preparation and conductive gels, making devices simpler and faster to use, which is critical for continuous monitoring and consumer applications. Furthermore, the application of these devices in non-traditional fields, such as Brain-Computer Interface (BCI) research and neuro-marketing, represents niche, high-growth potential segments. The impact forces acting on this market include intensifying competitive pressure leading to pricing instability, rapid obsolescence due to technological cycling, and profound influence from regulatory bodies dictating safety standards and clinical efficacy requirements, compelling manufacturers to adhere to global quality benchmarks while constantly innovating to maintain market relevance.

The EEG, EMG, and Evoked Potential Devices Market is systematically segmented based on Product Type, Application, and End-Use, offering a nuanced view of market dynamics and adoption patterns across the global healthcare landscape. Product segmentation is crucial as it reflects the technological maturity and specific clinical utility of the devices, ranging from stationary, multi-channel hospital systems to wearable, wireless devices optimized for long-term ambulatory monitoring. The distinction between devices based on modality—EEG, EMG, or EP—further allows manufacturers to tailor their R&D efforts to specific neurological or neuromuscular requirements. The market is increasingly trending towards integrated platforms that offer multimodal capabilities, reducing the overall equipment footprint and improving workflow efficiency within clinical diagnostic settings.

Application analysis highlights the primary clinical domains driving demand, with Neurology, Sleep Monitoring, and Intraoperative Monitoring (IOM) representing the largest and most critical segments. The growth in IOM is particularly noteworthy due to the increasing complexity of spine and brain surgeries, where real-time nerve function assessment is non-negotiable for mitigating surgical complications and improving long-term patient function. The End-Use segmentation reveals that hospitals, due to their capacity for high-volume diagnostics and specialized surgical suites, remain the largest consumers. However, the fastest growth is projected in specialized neurological centers and ambulatory settings, reflecting a broader trend towards decentralized care and specialized outpatient services, where cost-effectiveness and rapid access to diagnostics are key differentiating factors.

Further granularity in segmentation involves considering the type of technology—digital versus analog systems, with digital platforms dominating—and the nature of the electrodes used (wet electrodes being standard in high-precision clinical settings, while dry electrodes are gaining traction in research and continuous monitoring). These segments provide critical insights into purchasing behaviors, reflecting the trade-off between signal quality, ease of use, and cost. Understanding these subtle segment differences allows stakeholders, including manufacturers, investors, and healthcare providers, to accurately forecast demand curves, allocate resources strategically, and focus on developing products that meet the specific needs of high-growth niche areas such as pediatric neurophysiology or advanced neuro-rehabilitation.

The value chain for the EEG, EMG, and Evoked Potential Devices Market begins with the highly specialized Upstream Activities, primarily involving the research and development of core sensor technology, advanced microelectronics, and proprietary software algorithms. Manufacturers rely heavily on specialized suppliers for high-quality components, including sophisticated digital signal processors, analog-to-digital converters, biocompatible materials for electrodes, and robust system casings. Significant R&D investment is channeled into enhancing signal-to-noise ratio (SNR), reducing device footprint (miniaturization), and ensuring data security protocols. This upstream phase is crucial, as the quality and innovation of the core components directly determine the clinical reliability and performance of the final device, creating a high barrier to entry for new market participants due to the required technical expertise and regulatory compliance.

The Midstream phase involves the manufacturing, assembly, and rigorous quality control of the final devices. This segment is characterized by complex regulatory requirements, particularly compliance with international standards such as ISO 13485 and regional clearances (e.g., FDA, CE Mark). The manufacturing process requires precision engineering to ensure electrode consistency and system durability, especially for portable and intraoperative monitoring devices exposed to demanding clinical environments. Following assembly, comprehensive software validation and integration, often including proprietary analysis platforms and cloud connectivity features, are performed. The competitive advantage at this stage often lies in operational efficiency, supply chain resilience, and the ability to seamlessly integrate hardware components with user-friendly, feature-rich analytical software packages tailored to diverse clinical needs.

The Downstream activities focus on Distribution, Sales, and Post-Sales Service. Distribution channels are typically hybrid, involving both Direct Sales forces for major hospital systems and academic centers, ensuring specialized technical support and clinical training, and Indirect Sales via third-party distributors, particularly for accessing international markets and smaller clinics. Effective distribution requires robust logistics for delivering sensitive electronic equipment and ensuring the timely supply of high-volume consumables like electrodes and gels. Post-sales service, including maintenance, software updates, and advanced technical support, is a critical value differentiator, ensuring high device uptime and customer satisfaction. Potential customers (end-users) are primarily reached through specialized medical device conferences, clinical training workshops, and peer-reviewed publications that validate the technology's clinical efficacy and cost-effectiveness, emphasizing the educational aspect of market penetration.

The primary and most significant potential customers for EEG, EMG, and Evoked Potential devices are large academic medical centers and specialized regional hospitals. These institutions require high-end, multi-channel stationary systems for complex diagnostics, long-term continuous monitoring (LTM) units in Epilepsy Monitoring Units (EMUs), and robust intraoperative neurophysiological monitoring (IONM) setups for surgical procedures. Their purchasing decisions are driven by the need for clinical accuracy, integration capabilities with existing hospital information systems (HIS/EHR), comprehensive service contracts, and adherence to strict regulatory and accreditation standards. The volume of patients requiring specialized neurodiagnostics, combined with the presence of teaching and research faculties, makes these centers the cornerstone market segment, commanding the highest utilization rates for sophisticated devices.

A rapidly growing segment of potential customers includes specialized neurological clinics, independent diagnostic testing facilities, and ambulatory surgical centers (ASCs). These smaller entities often prioritize cost-effectiveness, portability, and ease of use, leading to higher demand for compact, portable EEG and EMG units that can be rapidly deployed in outpatient settings. Their need centers around efficient workflow management and faster patient throughput, making devices with automated reporting features and minimal setup time highly attractive. Furthermore, sleep clinics dedicated to the diagnosis of sleep apnea and related disorders represent a specialized customer base heavily reliant on Polysomnography (PSG) systems, which combine EEG, EMG, and other vital parameter monitoring capabilities, often requiring robust data storage and remote access functionalities for home-based testing.

Finally, a crucial emerging segment comprises academic and research institutions, pharmaceutical companies conducting clinical trials, and increasingly, specialized neuro-rehabilitation centers. Research institutions drive the demand for high-density EEG systems and advanced experimental platforms used in cognitive neuroscience, Brain-Computer Interface (BCI) development, and non-invasive neuromodulation studies, where the primary driver is data resolution and technological flexibility. Pharmaceutical companies utilize these devices as reliable biomarkers in clinical trials for new neurological drugs, requiring standardized, reproducible data acquisition protocols across multiple global sites. As technology progresses towards wearables, direct-to-consumer health technology providers also emerge as potential buyers for simplified, consumer-grade neurofeedback and monitoring devices, although this segment requires different regulatory pathways and device designs focused more on user experience than clinical precision.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Natus Medical Incorporated, Medtronic plc, Nihon Kohden Corporation, Compumedics Limited, Masimo Corporation, Cadwell Laboratories Inc., NeuroWave Systems Inc., Micromed S.p.A., EB Neuro S.p.A., Noraxon USA Inc., Zynex Medical, EMS S.A., Bio-logic Systems Corp. (a subsidiary of Natus Medical), BrainScope Company Inc., Electrical Geodesics, Inc. (EGI), Advanced Brain Monitoring, Inc., Grael, and Grass Technologies (now part of Natus). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the EEG, EMG, and Evoked Potential Devices Market is undergoing rapid transformation, largely characterized by the transition from analog to fully digital systems, offering enhanced signal resolution, massive data storage capabilities, and superior connectivity. A pivotal innovation is the development of high-density EEG systems (typically 128 channels or more) which provide enhanced spatial resolution for localizing epileptic foci or studying complex cognitive function, previously unattainable with standard clinical setups. Furthermore, the integration of wireless communication technologies, such as Bluetooth and Wi-Fi, facilitates truly ambulatory and wearable neurophysiological monitoring, freeing patients from fixed clinical environments and enabling long-term data collection that yields richer diagnostic information, particularly for transient neurological events that might be missed during short, in-clinic sessions. This digital infrastructure supports the growing trend of remote data review and tele-consultation, democratizing access to specialized neurophysiology expertise across geographic barriers.

Another area of significant technological advancement involves electrode materials and design. Traditional wet electrodes, requiring conductive paste and skin abrasion, are being challenged by innovative dry electrode technologies. Dry electrodes use materials like silver/silver chloride (Ag/AgCl) or conductive polymers, designed to maintain stable contact with the skin without prep, dramatically improving device setup time, patient comfort, and suitability for long-duration or home-based monitoring. While wet electrodes still offer superior signal quality for critical, short-term diagnostics, dry electrode solutions are gaining rapid acceptance in consumer health, BCI applications, and rapid screening environments due to their ease of use. Parallel advancements in active shielding and sophisticated differential amplification circuitry embedded directly into the electrode caps are effectively mitigating movement artifacts and environmental noise, ensuring clinical-grade data collection even in highly challenging, non-controlled settings like ambulances or intensive care units (ICUs).

The software and analytical ecosystem surrounding these devices is arguably the most dynamic area of innovation. Advanced Quantitative Analysis Software (Q-EEG, Q-EMG) is becoming standard, providing automated metrics and statistical comparisons against normative databases, reducing the subjectivity inherent in manual waveform interpretation. Crucially, the embedding of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is accelerating the diagnostic process, enabling automated detection of seizures, burst suppression patterns, and subtle neuropathy signs. This technological convergence is paving the way for advanced multimodal integration, where neurophysiological data (EEG/EMG) is correlated automatically with structural imaging (MRI/CT), clinical scales, and genetic information, providing a holistic and highly precise neurodiagnostic profile. Continuous software updates and cloud-based processing capabilities are becoming essential features, ensuring that installed hardware systems remain technologically current throughout their operational lifespan and facilitate real-time collaborative diagnostics.

The primary driver is the accelerating global prevalence of neurological and neuromuscular disorders, such as epilepsy, stroke, and peripheral neuropathy, compounded by the rapidly increasing aging population requiring extensive diagnostic monitoring. Technological innovation in device portability and advanced signal processing also significantly contributes to broader market adoption.

AI algorithms, particularly deep learning, are enhancing accuracy by automating artifact removal, standardizing quantitative analysis (QEEG/QEMG), and objectively identifying complex pathological patterns, thereby reducing inter-reader variability and significantly accelerating the overall diagnostic interpretation time for clinical specialists.

The Consumables and Accessories segment, specifically advanced dry electrodes and specialized high-density sensor arrays, is projected to show high growth due to continuous utilization alongside device sales and the shift towards easier, faster setup required for long-term and ambulatory monitoring applications.

EEG (Electroencephalography) measures electrical activity in the brain, primarily used for seizure disorders and sleep studies. EMG (Electromyography) assesses muscle response to nerve stimulation, diagnosing neuromuscular diseases. Evoked Potentials (EP) test sensory pathways (visual, auditory, somatosensory) to detect central nervous system lesions, often used in intraoperative monitoring.

APAC's rapid growth is fueled by substantial investments in healthcare infrastructure modernization, rising public awareness regarding neurological conditions, and the immense patient pool in countries like China and India. Increasing accessibility to advanced medical devices and favorable government policies supporting technology adoption are key catalysts for this regional expansion.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.